- Automotive

- Self Balancing Technology Market

Self Balancing Technology Market Size, Share, and Growth Forecast, 2026 - 2033

Self Balancing Technology Market by Product Type (Double-Wheeled, Unicycle, Others), Balance Mechanism (Active Mass Control, Control Momentum Gyros, Reaction Wheels), End-user Application (Personal, Commercial, Security & Patrol), and Regional Analysis 2026 - 2033

Self Balancing Technology Market Size and Trends Analysis

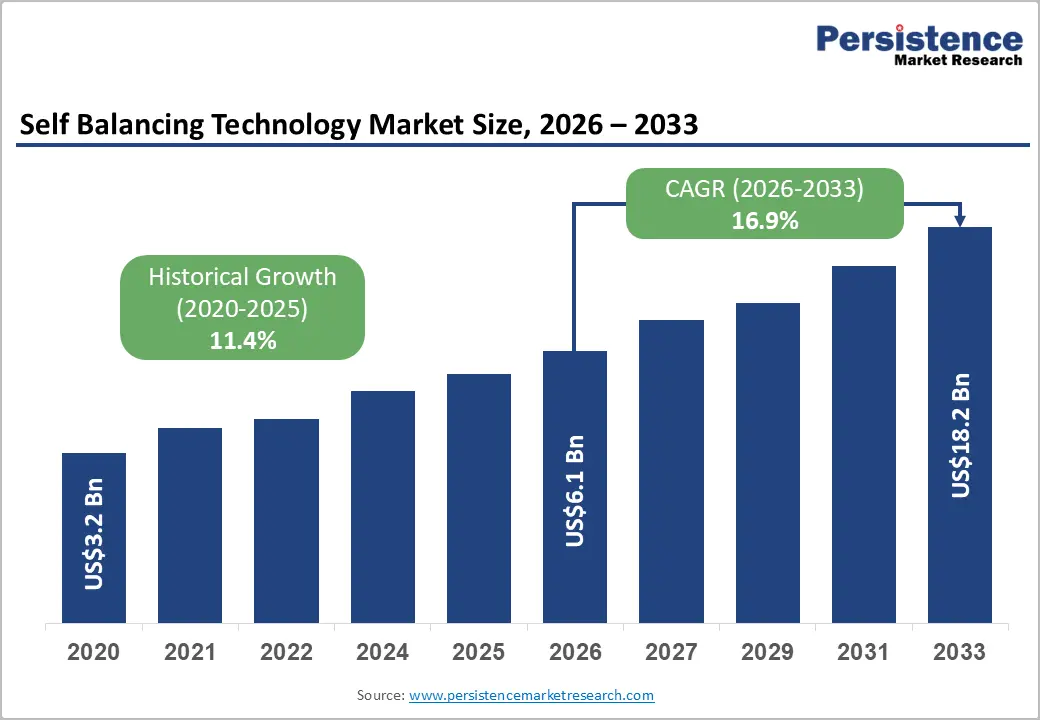

The global self balancing technology market size is likely to be valued at US$6.1 billion in 2026 and is expected to reach US$18.2 billion by 2033, growing at a CAGR of 16.9% during the forecast period from 2026 to 2033, driven by the rising demand for eco-friendly personal mobility, urbanization pressures, and advancements in battery and sensor technologies.

Urban populations favor compact transporters for short commutes, while industrial applications expand via AI integration. This growth is further supported by advancements in MEMS (Micro-Electro-Mechanical Systems) sensors and AI-driven attitude control algorithms, which have significantly reduced the cost while enhancing the safety profiles of self-balancing mechanisms.

Key Industry Highlights:

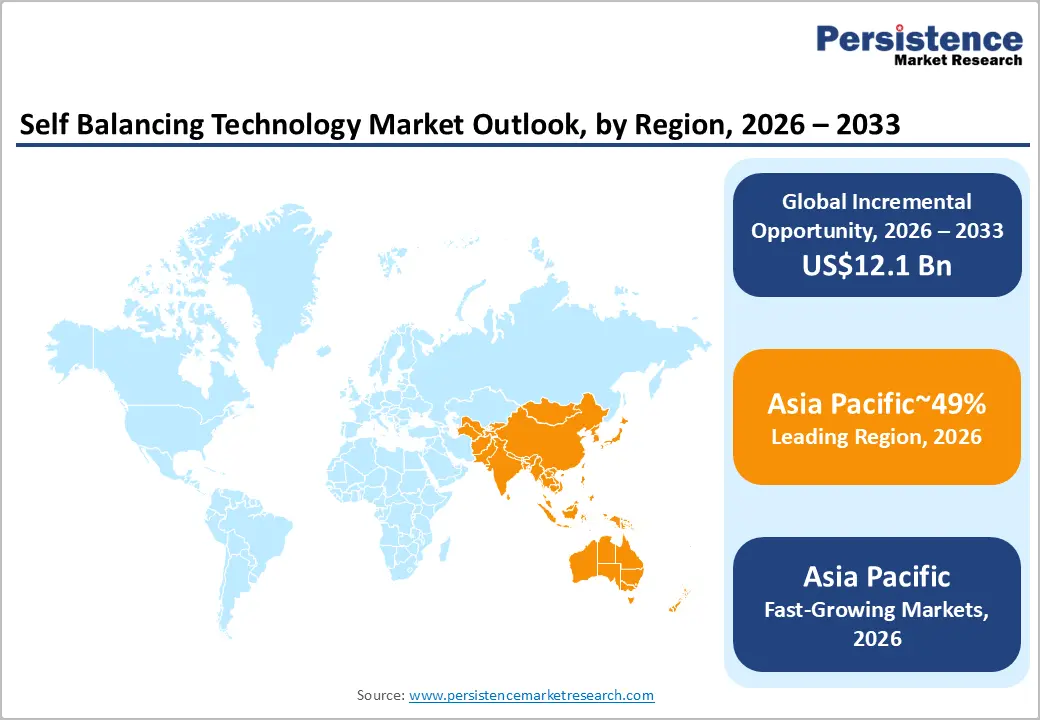

- Leading Region: Asia Pacific is expected to lead the market region with approximately 49.0% share, underpinned by large-scale manufacturing capacity, cost-efficient component ecosystems, and China-led production scale.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region, supported by rapid urbanization, micro-mobility adoption, and domestic innovation in robotics and personal transport systems.

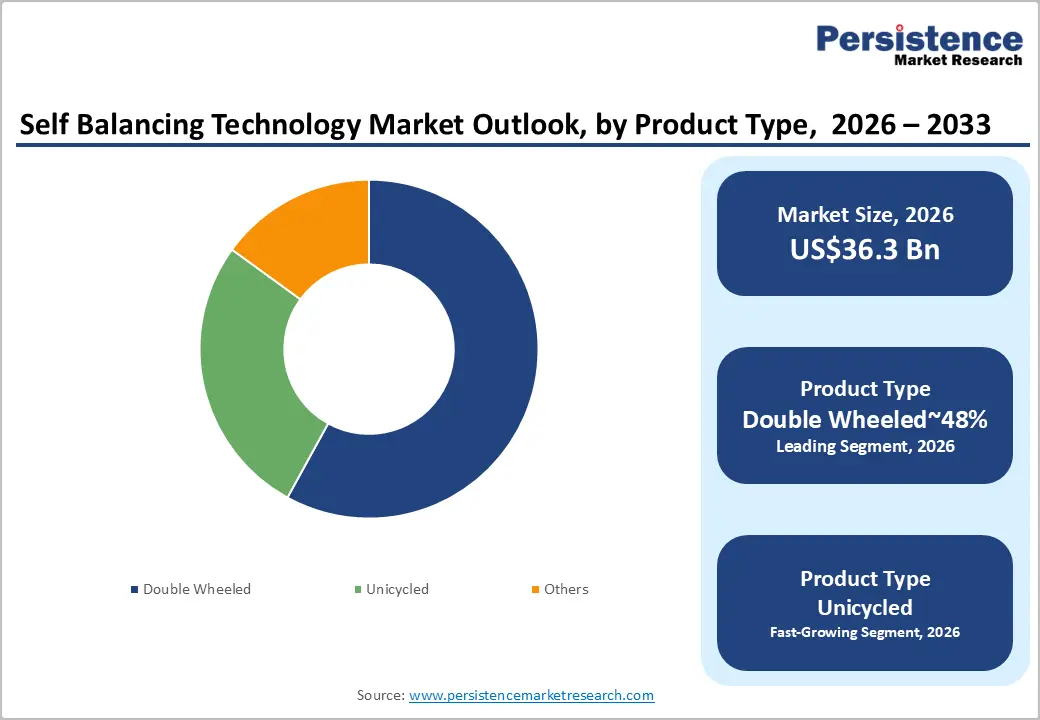

- Leading Product Type: Double-wheeled platforms are anticipated to lead with 59% share, supported by superior stability, user familiarity, and widespread deployment in consumer mobility devices

- Leading Balance Mechanism: The active mass control segment is expected to lead with 54% share, reflecting proven dynamic stabilization performance across consumer and light commercial self-balancing platforms.

| Key Insights | Details |

|---|---|

|

Self Balancing Technology Market Size (2026E) |

US$6.1 Bn |

|

Market Value Forecast (2033F) |

US$18.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

16.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Urbanization and Micro-Mobility Demand

Accelerating urban concentration is restructuring short-distance travel demand and elevating micro mobility as a functional extension of public transport. Self balancing devices align with dense corridors where parking scarcity, congestion management, and curb governance policies favor compact electric platforms. At the value chain level, this shifts procurement toward standardized platforms, battery modules, and control stacks optimized for fleet duty cycles rather than discretionary use. Municipal pilots and shared fleets normalize usage patterns, compress adoption friction, and create predictable utilization profiles that improve asset turnover while stabilizing service and parts revenue across operators and suppliers.

Technology maturation in sensors, power electronics, and embedded control lowers reliability risk and supports integration with traffic management and payment systems. Regulatory frameworks emphasizing safety certification and sidewalk governance further formalize demand, encouraging operators to scale compliant fleets instead of fragmented ownership. These dynamics reallocate margins toward software, maintenance, and refurbishment, while manufacturing benefits from learning curves and modular sourcing. As commuting patterns favor short trips and intermodal transfers, self balancing platforms become infrastructure complements, expanding addressable demand through recurring fleet replacement cycles and long term service contracts.

Industrial Automation and Robotics

The acceleration of warehouse automation under Industry transformation agendas is structurally increasing demand for mobile robotic platforms capable of stable vertical load handling within constrained operating envelopes. Self balancing autonomous mobile robots enable axial pivoting and high maneuverability, supporting dense aisle configurations and flexible layout reconfiguration without extensive fixed infrastructure. At the value chain level, this shifts procurement toward integrated mobility stacks combining inertial sensing, real-time control software, and power management architectures optimized for continuous duty cycles. As fulfillment networks pursue higher throughput within fixed footprints, material handling systems increasingly prioritize space efficiency and motion precision, reinforcing the adoption of dynamically stabilized platforms over conventional cart-based transport modalities.

Technology evolution in sensor fusion, edge computing, and safety-certified control firmware improves operational reliability and supports compliance with workplace safety frameworks governing human-robot collaboration. These advances reduce downtime risk and enable standardized deployment across heterogeneous facility layouts, improving asset utilization and lifecycle economics. Regulatory emphasis on operational safety and traceability elevates qualification requirements for mobile platforms, favoring engineered self balancing systems with validated stability envelopes. Margin structures consequently migrate toward software, integration, and service layers, while hardware commoditization pressures manufacturers to differentiate through reliability, interoperability, and total cost of ownership performance across automated logistics environments.

Barrier Analysis - Control-Loop Latency and Sensor Fusion Synchronization

The requirement for tightly synchronized sensor fusion across inertial measurement units and ranging modalities imposes structural constraints on the scalable deployment of self balancing platforms. Static and dynamic balance depend on low-latency control loops that must reconcile heterogeneous data streams under variable compute loads and communication overhead. At the value chain level, this elevates integration complexity across sensing hardware, embedded processors, firmware, and real-time operating environments, increasing validation burdens and extending qualification cycles. As systems scale across diverse form factors and duty profiles, maintaining deterministic performance becomes operationally fragile, constraining platform standardization and slowing fleet-level rollouts.

Technology evolution toward higher bandwidth sensors and richer perception stacks compounds timing sensitivity and increases susceptibility to jitter across software scheduling and middleware layers. Regulatory and safety certification frameworks governing autonomous operation and human proximity raise the evidentiary bar for stability assurance, lengthening compliance timelines and elevating non-recurring engineering costs. These factors shift cost structures toward verification, testing, and safety assurance, while limiting the reuse of generic compute modules. Margin pressure emerges as manufacturers absorb integration overhead to meet safety thresholds, structurally moderating deployment velocity across logistics, industrial automation, and shared mobility applications.

Actuator Saturation and Mechanical Recovery Limits

Mechanical end stops and finite torque envelopes in actuation systems impose intrinsic constraints on the dynamic stabilization range of self balancing platforms. When platforms encounter lateral perturbations or steep surface discontinuities, actuators may saturate before corrective control authority is restored, constraining recovery envelopes under real-world operating conditions. At the value chain level, this necessitates tighter co-design of motors, gear trains, power electronics, and structural components to expand usable torque margins without materially inflating mass or energy consumption. These engineering tradeoffs increase bill of materials complexity and constrain platform standardization across payload classes and terrain profiles.

Technology evolution toward higher torque density motors and advanced power stages introduces thermal management and durability challenges under continuous duty cycles. Regulatory and safety frameworks governing personal mobility and industrial equipment impose stability performance thresholds that elevate qualification requirements, extending validation timelines for platforms intended for mixed environment operation. These constraints reallocate costs toward materials, thermal solutions, and endurance testing, compressing margins in entry-tier configurations. The resulting performance ceilings moderate adoption in uneven terrain use cases and limit addressable demand where recovery robustness is a prerequisite for operational safety and liability compliance.

Opportunity Analysis - Steer by Wire Retrofitting for Heavy Motorcycle Platforms

Modular gyroscopic stability retrofits for existing heavy motorcycle platforms create an aftermarket pathway to extend usability and compliance for legacy fleets facing rising safety and accessibility expectations. Retrofitting decouples steering input from mechanical linkages, enabling software-mediated stability augmentation that improves low-speed controllability and balance under load variability. At the value chain level, this opportunity shifts value capture toward kits integrating sensors, actuators, control firmware, and vehicle interface modules that can be installed without full platform redesign. Standardized retrofit architectures also reduce integration friction for service networks, enabling scalable deployment across heterogeneous vehicle geometries and duty profiles.

Technology maturation in compact actuators, fault-tolerant control, and redundant sensing enables automotive-grade steer-by-wire architectures suitable for two-wheel platforms operating under variable terrain and payload conditions. Regulatory acceptance of electronically mediated steering, alongside evolving safety certification pathways, lowers adoption barriers for retrofit solutions that demonstrate fail-safe behavior and predictable degradation modes. These dynamics reallocate margins toward software calibration, installation services, and lifecycle support, while expanding the addressable aftermarket for stability enhancement across existing vehicle populations. The resulting ecosystem supports recurring revenue through updates, maintenance, and compliance revalidation over extended vehicle lifecycles.

AI Enhanced Stabilization in Software-Defined Mobility Platforms

The convergence of learning based control with classical feedback architectures is restructuring stabilization performance envelopes across self balancing mobility platforms. Hybrid control stacks that fuse adaptive models with deterministic loops enable anticipatory compensation for surface irregularities, load shifts, and transient disturbances, reducing reliance on purely reactive actuation. At the value chain level, this elevates the role of software-defined functionality within hardware-centric platforms, shifting differentiation toward control algorithms, data pipelines, and continuous model validation. As platforms migrate toward updatable control firmware, vendors capture recurring value through calibration services, safety certification maintenance, and lifecycle software support rather than one-time hardware margins.

Technology evolution in on-device inference, sensor fusion, and real-time compute supports the deployment of adaptive control under tight latency and safety constraints. Regulatory frameworks governing assistive mobility and autonomous operation emphasize fail-safe behavior, explainability, and deterministic fallback modes, shaping system architecture toward verifiable hybrid control designs. These requirements increase development and validation overhead while strengthening barriers to entry for uncertified solutions. Margin structures consequently favor vertically integrated control stacks that internalize software assurance costs, enabling expansion into assistive mobility segments where stability performance directly underpins safety compliance and institutional procurement acceptance.

Category-wise Analysis

Product Type Insights

The double-wheeled is expected to lead the accounting for approximately a 59% share in 2026, underpinned by its entrenched role across recreational mobility, commercial patrol, and facility transport workflows. The configuration delivers inherent lateral stability, a lower learning curve, and predictable handling under variable payloads, which supports qualification readiness for enterprise and shared fleet deployments. Adoption remains anchored by operational reliability and workflow integration within campuses, logistics perimeters, and controlled public environments. Ongoing platform evolution in battery management, embedded control firmware, and connected diagnostics reinforces replacement cycles and utilization intensity across high-volume deployments. Vendors such as Segway and Ninebot continue to broaden portfolios with standardized platforms and fleet management ecosystems, locking in service contracts and aftermarket workflows across security, hospitality, and corporate mobility use cases.

Unicycle is expected to be the fastest-growing segment, driven by unmet needs around portability, storage constraints, and multimodal commuting efficiency in dense urban corridors. The compact form factor reduces storage friction and supports seamless integration with public transport, addressing workflow gaps left by bulkier platforms. Growth is catalyzed by improvements in motor torque density, battery energy density, and control algorithms that enhance ride stability without materially increasing device mass. Accelerating adoption is supported by mobile connectivity, route optimization, and digital calibration tools that lower onboarding friction for first-time users. Companies, including InMotion and King Song, are scaling high-performance platforms to embed switching costs and capture early-cycle demand across commuter and enthusiast segments.

Balance Mechanism Insights

Active mass control is expected to lead, accounting for approximately a majority 54% share in 2026, anchored by its entrenched deployment across personal mobility devices and compact transport platforms. The mechanism’s inverted pendulum architecture enables reliable low-speed stabilization through controlled weight shifting, reducing dependence on high-density sensing and complex perception stacks. This structural simplicity supports manufacturability at scale, a predictable bill of materials, and high field reliability across consumer-grade electronics and shared mobility fleets. Platform evolution in embedded control firmware and low-cost inertial sensing further reinforces replacement cycles and utilization intensity in high-volume recreational and short-range transport use cases. Vendors, including Segway and Ninebot, continue to standardize active mass architectures within integrated mobility ecosystems, locking in workflows across device platforms, aftermarket components, and service networks.

Control momentum gyros are expected to be the fastest-growing segment, driven by performance limitations of ground reaction-dependent stabilization in aerospace, maritime, and constrained mobility environments. Internal torque generation enables attitude control without reliance on surface contact, expanding applicability across micro satellite platforms, marine stabilization systems, and emerging hybrid mobility concepts. Growth is catalyzed by advances in compact high-torque actuators, precision bearings, and real-time control software that improve responsiveness and durability under continuous duty cycles. Accelerating adoption is supported by digital twins and simulation-driven calibration workflows, reducing commissioning friction for mission-critical deployments. Organizations such as NASA and ESA underpin technology validation pathways, while industrial suppliers scale modular gyro platforms to embed switching costs across next-generation stabilization architectures.

Regional Insights

Asia Pacific Self Balancing Technology Market Trends

Asia Pacific is expected to remain both the leading market and the fastest growing region, approximating the 49% share of global revenue, supported by unmatched manufacturing concentration, dense urban consumption corridors, and vertically integrated mobility supply networks. The region is positioned to consolidate structural dominance through scale-driven production economics, rapid platform iteration cycles, and tight coupling between component ecosystems and device assemblers. Demand formation is anticipated to be shaped by everyday mobility use cases in high-density cities, where compact self balancing platforms are likely to be absorbed into routine commuting and short-range transport behaviors. Production capacity, component self-sufficiency, and fast design-to-market cycles are projected to reinforce regional leadership, while platform differentiation through embedded intelligence, energy management optimization, and ruggedized form factors is expected to elevate replacement intensity and utilization frequency across consumer and fleet deployments.

China is expected to serve as the regional anchor, positioning Asia Pacific to set the pace for platform commoditization, component integration, and global supply coordination. The country is projected to shape regional momentum through deep upstream control over motors, batteries, power electronics, and control modules, enabling rapid scaling of self balancing architectures across personal mobility and light robotic applications. Vendor strategies led by Ninebot are anticipated to emphasize ecosystem lock-in across hardware platforms, firmware layers, and aftermarket services, embedding switching costs within distributor and fleet networks. These dynamics position the region to define future cost-performance frontiers and normalize self balancing mobility as a functional urban transport layer.

North America Self Balancing Technology Market Trends

North America is expected to remain a mature and structurally stable market, with demand positioned to be anchored in replacement cycles, certified fleet refresh programs, and institutional procurement rather than broad-based greenfield adoption. The region is projected to sustain structural relevance through high-value deployments in security patrol, controlled mobility environments, and enterprise robotics, where reliability, safety assurance, and total lifecycle performance are prioritized over low-cost device proliferation. Dynamics are likely to be reinforced by a deep innovation ecosystem spanning robotics software, embedded control systems, and perception stacks, which positions the region to influence global platform architectures and validation pathways. Policy alignment around consumer safety and operational certification is expected to continue shaping product design toward robust, compliance-oriented configurations, favoring vendors capable of sustaining qualification cycles, software maintenance, and service-led monetization.

The U.S. is expected to function as the regional anchor, positioning North America to retain influence over algorithm development, platform validation, and institutional adoption trajectories. The country is projected to shape regional momentum through the concentration of advanced robotics developers such as Boston Dynamics and Agility Robotics, which are likely to advance stabilization control stacks and mobile manipulation architectures applicable to self balancing platforms. Regulatory oversight by the Consumer Product Safety Commission is anticipated to continue structuring market access around certified safety performance, reinforcing demand for compliant, enterprise-grade systems over informal consumer deployments.

Europe Self Balancing Technology Market Trends

Europe is expected to remain a mature and structurally stable market, with demand positioned to be anchored in certified device replacement cycles, compliance-driven upgrades, and premiumization across regulated urban mobility environments. The region is projected to sustain structural relevance through strong alignment between environmental policy objectives and electric personal mobility adoption, reinforcing demand for high-quality, safety-certified self-balancing platforms. Supply-side positioning is expected to benefit from manufacturing depth, advanced mechatronics capabilities, and integration of software-defined control stacks that elevate reliability and lifecycle performance. Policy coordination across member states is likely to continue driving standardization of device categorization and operating frameworks, shaping vendor roadmaps toward compliant architectures and exportable platform designs.

Germany is expected to function as the regional anchor, positioning Europe to retain manufacturing-led influence over platform qualification, component sourcing, and certification pathways. Regulatory convergence initiatives and emerging governance frameworks around autonomous and intelligent systems are anticipated to steer vendor strategies toward explainable control logic, documented safety cases, and service-led lifecycle support. Platform providers such as InMotion are expected to adapt product architectures to harmonized operating standards, while medical mobility innovation, exemplified by Genny Mobility, is likely to expand clinical-grade use cases. These dynamics position Europe to sustain a compliance-led, export-capable ecosystem with growing emphasis on certified mobility platforms and assistive stabilization technologies.

Competitive Landscape

The global self balancing technology market is expected to exhibit a bifurcated competitive structure, with the consumer mobility segment remaining moderately consolidated while industrial and robotics-oriented applications remain structurally fragmented. Scale advantages in manufacturing, component sourcing, and global distribution allow leading vendors to exert functional influence over safety certification pathways and reference architectures for balance control systems.

Competitive positioning is expected to differentiate along vertical integration depth in consumer mobility and application-specific specialization in industrial robotics. Platform leaders such as Segway-Ninebot are likely to continue expanding ecosystem control through integrated hardware, firmware, and service layers, reinforcing switching costs for distributors and fleet operators. Industry dynamics are projected to feature selective consolidation around control software, sensing modules, and safety certification competencies, while niche players persist in unicycle and robotics subsegments where customization and application-specific performance remain decisive.

Key Industry Highlights:

- In June 2025, Yamaha Motor Co.'s MOTOROiD2 concept won the Red Dot Award for Design Concept, 2025, for its organic self-balancing evolution. The updated AMCES balance technology allowed the vehicle to move autonomously with natural rider-coordinated movements, even at extremely low speeds where balance is typically hardest.

- In June 2025, ABB expanded its portfolio by integrating AI-powered 3D Visual SLAM navigation into its Flexley Mover autonomous mobile robots. This upgrade allowed for infrastructure-free navigation and faster deployment, as the robots can autonomously map facilities and share data across fleets to improve scalability.

- In August 2024, Unitree Robotics released the Go2-W, a wheeled-quadruped robot with specialized dynamic balancing algorithms. The hybrid wheel-leg design allows the robot to balance on two wheels (standing upright) to reach high shelves while maintaining the stability of a four-legged animal on stairs.

Companies Covered in Self Balancing Technology Market

- Segway-Ninebot

- InMotion

- Airwheel

- Future Motion

- Razor

- Swagtron

- King Song

- CHIC

- Agility Robotics

- Unitree Robotics

- Honda Motor Co., Ltd.

- LG Electronics

- Samsung Electronics

- DEKA Research & Development

- Gausium

- Mobileye

Frequently Asked Questions

The global self balancing technology market is projected to be valued at US$6.1 billion in 2026 and is expected to reach US$18.2 billion by 2033, driven by urbanization-fueled micro-mobility demand and the integration of AI and advanced sensors into industrial automation and robotics platforms.

Rising urban density and congestion are creating a structural need for compact, agile personal transporters. Self balancing devices address last-mile connectivity gaps, align with shared mobility fleet models, and benefit from municipal policies favoring sustainable transport, shifting procurement toward standardized, high-durability platforms optimized for continuous urban duty cycles.

The self balancing technology market is forecast to grow at a CAGR of 16.9% from 2026 to 2033, reflecting rapid adoption across consumer mobility, warehouse robotics, and the convergence of AI-enabled stabilization in software-defined platforms.

Asia Pacific is both the leading and fastest-growing regional market, accounting for approximately 49.0% share, underpinned by its role as the global manufacturing hub, cost-efficient component ecosystems, and high-density urban adoption across China and other major cities.

The self balancing technology market features a bifurcated structure. Segway-Ninebot dominates the consumer mobility segment through vertical integration and global distribution. Specialized players such as InMotion and King Song lead in high-performance unicycles, while Agility Robotics and Unitree Robotics represent the frontier in industrial and legged-robot applications where advanced stabilization is critical.