- Advanced Materials

- Self-Compacting Concrete Market

Self-Compacting Concrete Market Size, Share, and Growth Forecast, 2025 - 2032

Self-Compacting Concrete Market By Product Type (Powder, Viscosity, Combination), End-use (Oil & Gas, Infrastructure, Building & Construction), and Regional Analysis for 2025 - 2032

Self-Compacting Concrete Market Size and Trends Analysis

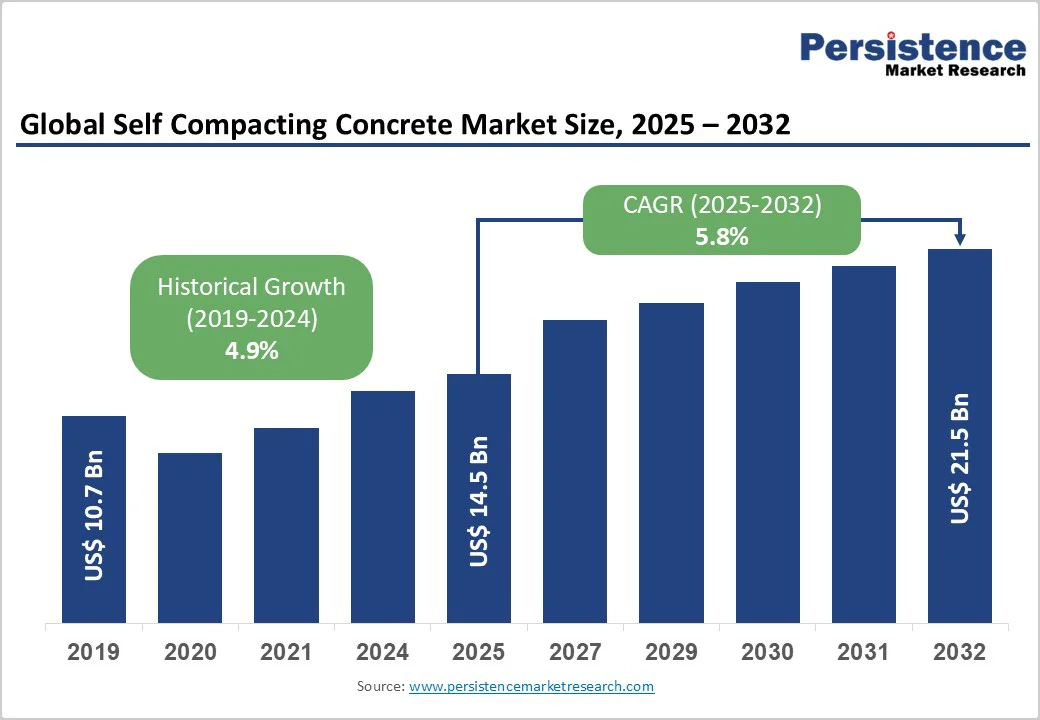

The global self-compacting concrete market size is likely to be valued at US$14.5 billion in 2025, expected to reach US$21.5 billion by 2032, growing at a CAGR of 5.8% during the forecast period from 2025 to 2032, driven by increasing demand for high-performance concrete in complex construction projects, rising adoption of sustainable building materials, and advancements in mix design technologies.

The market is further propelled by innovations in eco-friendly formulations and high-strength combination mixes, catering to preferences for durable and sustainable construction solutions. The growing acceptance of self-compacting concrete as a time-saving and labor-efficient alternative to traditional concrete is a key growth factor.

Key Industry Highlights:

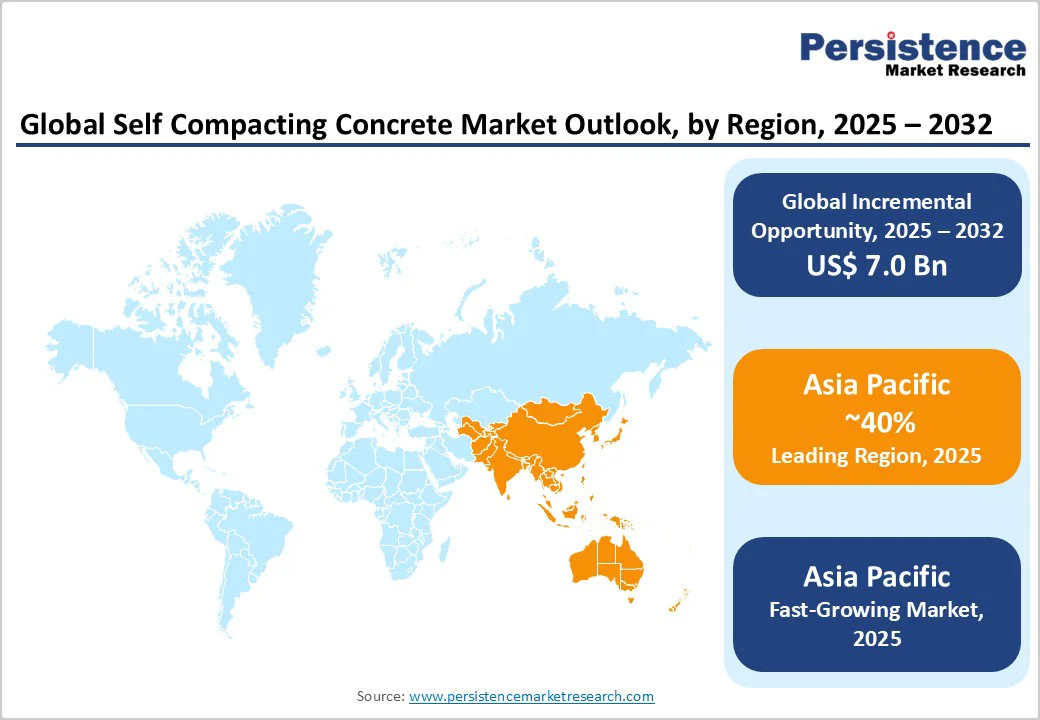

- Leading Region: Asia Pacific, commanding a 40% market share in 2025, driven by rapid urbanization and infrastructure investments in China and India.

- Fastest-growing Region: Asia Pacific, fueled by government-led smart city projects and sustainable construction initiatives.

- Dominant Product Type: Combination, holding approximately 45% of the market share, due to its versatility in flowability and strength.

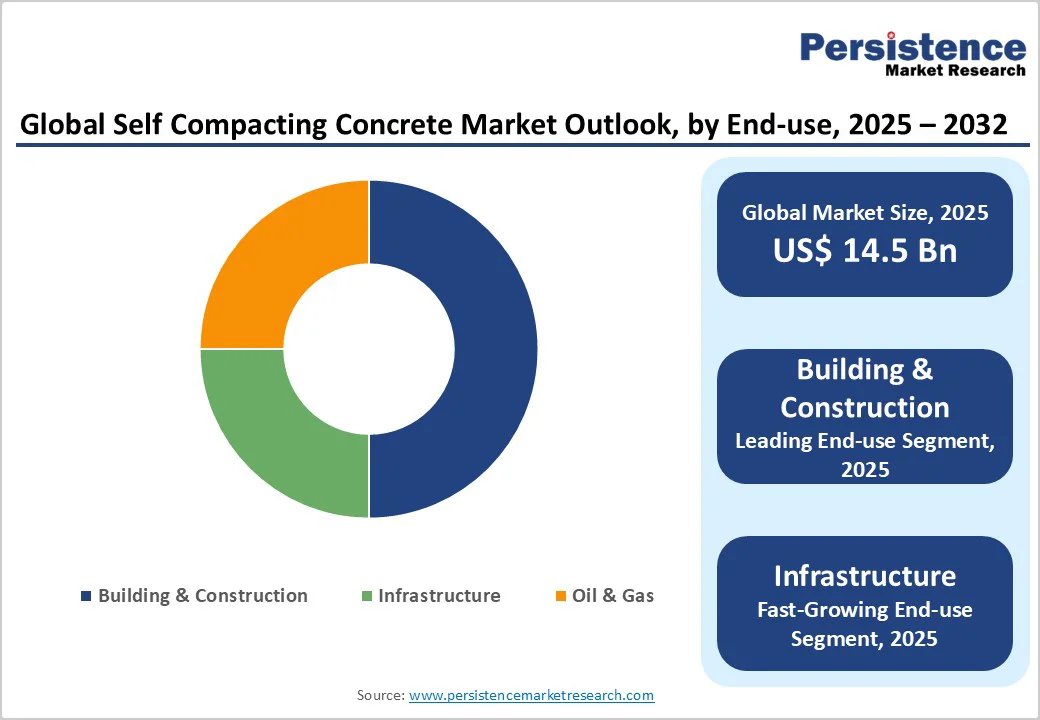

- Leading End-use: Building & Construction, accounting for over 50% of market revenue, driven by demand for high-rise and architectural projects.

- Key Market Driver: Adoption of AI-driven mix designs for optimized performance in complex structures.

- Growth Opportunity: Expansion in green building certifications with recycled aggregate mixes, supporting sustainability goals.

| Key Insights | Details |

|---|---|

|

Self-Compacting Concrete Market Size (2025E) |

US$14.5 Bn |

|

Market Value Forecast (2032F) |

US$21.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for High-Performance Concrete in Complex Structures

The increasing demand for high-performance concrete in complex construction projects is a primary driver of the self-compacting concrete market. Urbanization, high-rise buildings, infrastructure expansion, and large-scale industrial projects require materials that provide superior strength, durability, and workability compared to conventional concrete. SCC, as a form of HPC, offers excellent flowability without segregation, allowing it to fill intricate formworks and densely reinforced structures with minimal labour and vibration. This capability makes it ideal for bridges, tunnels, high-rise towers, and other demanding structural applications where uniformity and precision are critical.

The need for reduced construction time and improved quality further supports SCC adoption. Complex designs, such as curved facades, precast components, or heavily reinforced slabs, demand a concrete that maintains stability while flowing easily into all voids. Additionally, environmental and sustainability concerns push builders to use HPC with supplementary cementitious materials, recycled aggregates, and low-carbon cements, combining performance with eco-friendliness.

Higher Material Costs and Technical Expertise Requirements

The higher costs of superplasticizers and viscosity-modifying agents in self-compacting concrete pose significant restraints on market growth. SCC requires precise proportions of cement, fine aggregates, admixtures, and supplementary materials to achieve its unique flowability and stability characteristics. The incorporation of high-quality chemical admixtures and additives, such as superplasticizers and viscosity-modifying agents, increases production costs compared to conventional concrete. Additionally, sourcing low-carbon or recycled materials for sustainable SCC formulations can further elevate expenses, particularly in regions where these materials are limited or expensive.

Another critical factor is the technical expertise required for mix design, handling, and placement. SCC’s high fluidity demands skilled personnel to manage batching, transportation, and on-site pouring to prevent segregation, bleeding, or over-vibration. Contractors and labourers must be trained in specific techniques, such as controlled pouring rates and formwork preparation, to ensure consistent quality. Moreover, quality control measures such as rheology testing, slump flow assessment, and setting time monitoring add complexity and increase operational costs.

Expansion in Sustainable and Green Construction Practices

Advancements in eco-friendly self-compacting concrete mixes with recycled aggregates present significant growth opportunities. As governments and developers increasingly focus on reducing carbon emissions and promoting resource efficiency, SCC is gaining traction for its eco-friendly attributes. It minimizes vibration during placement, reducing noise and on-site energy consumption. SCC can incorporate recycled materials such as fly ash, slag, and recycled aggregates, lowering the overall carbon footprint of construction projects.

For instance, in Japan and several European countries, SCC is widely used in green building certifications such as LEED and BREEAM due to its ability to enhance durability and minimize maintenance over time. Similarly, in India, sustainable urban projects under the Smart Cities Mission are adopting SCC to improve efficiency and reduce environmental impact. Additionally, leading companies such as LafargeHolcim and Sika AG are developing low-carbon SCC formulations using alternative binders and supplementary cementitious materials.

Category-wise Analysis

Product Type Insights

Combination dominates the market, accounting for 45% of the market share in 2025. Its dominance stems from its balanced flowability and stability, enabling excellent performance across varied applications, including high-rise buildings, bridges, and precast components. This mix design ensures optimal strength, durability, and ease of placement in demanding construction environments.

Viscosity is the fastest-growing segment, driven by the rising need for segregation-resistant and stable mixes suitable for complex structural designs. These high-viscosity formulations enhance uniformity, prevent bleeding, and ensure consistent performance in congested reinforcement areas, making them ideal for intricate architectural and large-scale infrastructure projects.

End-use Insights

Building & Construction leads with 50% share, driven by rapid urbanization and the growing demand for architectural precision in high-rise, residential, and commercial projects. Its superior finish, ease of placement, and ability to form intricate designs without vibration make SCC a preferred choice for modern construction applications.

Infrastructure is the fastest-growing sector, driven by increased investments in bridges, tunnels, highways, and transportation networks. Governments worldwide are prioritizing durable, low-maintenance materials to enhance construction efficiency and longevity. SCC’s superior flowability, strength, and reduced labour needs make it ideal for large-scale, complex infrastructure projects.

Regional Insights

Asia Pacific Self-Compacting Concrete Market Trends

The Asia Pacific commands around a 40% share and is the fastest-growing region, driven by rapid urbanization and massive infrastructure investments. China’s Belt and Road Initiative has significantly boosted cross-border infrastructure development, creating strong demand for high-performance concrete that ensures speed, durability, and cost efficiency in large-scale projects such as highways, bridges, and rail networks. Similarly, India’s Smart Cities Mission, focusing on sustainable urban development and modernized construction practices, has accelerated the adoption of SCC due to its reduced labor requirements and superior surface finish.

Countries such as Japan, South Korea, and Indonesia are investing heavily in residential and commercial construction, further fueling regional growth. The use of SCC in complex architectural structures, coupled with growing awareness of sustainable materials, has strengthened its market presence. Local manufacturers are collaborating with international players to enhance material formulations and supply chains.

North America Self-Compacting Concrete Market Trends

North America accounts for 25% in 2025, supported by the U.S. Infrastructure Investment and Jobs Act, which allocates substantial funding to modernize roads, bridges, and public transport systems. The region’s growing adoption of SCC is driven by its efficiency in high-rise construction and large-scale urban infrastructure, where reduced labour needs and superior structural performance are key advantages. Major metropolitan areas in the U.S. and Canada are witnessing increased demand for sustainable and durable concrete solutions that align with green building standards and LEED certifications.

The U.K. market, though part of Europe, reflects similar dynamics. The ongoing HS2 high-speed rail project and multiple urban regeneration programs are driving the need for high-performance SCC that ensures strength, uniformity, and reduced noise pollution during construction. Supported by stringent government sustainability policies and carbon-reduction goals, the U.K. is rapidly incorporating SCC into both public and private developments.

Europe Self-Compacting Concrete Market Trends

Europe holds approximately 30% of the market share, led by Germany and France, leading regional growth. The dominance of these countries is driven by strict EU sustainability directives promoting environmentally responsible construction practices and the adoption of advanced building materials. European nations are increasingly prioritizing low-carbon, durable, and energy-efficient concrete solutions to meet emission reduction targets outlined in the European Green Deal.

Germany’s strong industrial base and ongoing investments in transportation, housing, and renewable energy infrastructure have accelerated the adoption of SCCs in both public and private construction. France’s emphasis on modern architectural designs and infrastructure renovation has encouraged the adoption of SCC for its superior workability and aesthetic finish. The region also benefits from extensive R&D activities focused on developing self-healing and fiber-reinforced SCC formulations.

Competitive Landscape

The global self-compacting concrete market is highly competitive, with a few major players dominating production and distribution across key regions. Companies are increasingly focusing on sustainable innovations and advanced mix designs to enhance the material’s flowability, strength, and durability while reducing environmental impact. Continuous R&D efforts are directed toward developing eco-friendly formulations incorporating recycled aggregates, industrial by-products, and low-carbon cements. These initiatives align with growing global emphasis on green construction practices and infrastructure modernization.

Strategic collaborations between manufacturers, research institutions, and construction firms are further driving product advancements and expanding market reach. Leading companies are also investing in automated batching systems and digital quality monitoring to ensure consistency and reduce wastage on-site. Rising urbanization, large-scale infrastructure projects, and demand for high-performance concrete in bridges, tunnels, and high-rise buildings continue to support market growth.

Key Industry Developments

- In April 2024, Kilsaran introduced two Volvo FM electric concrete trucks, the first of their kind in Ireland and the UK. These zero-emission vehicles, based in Ringsend, Dublin, are equipped with five batteries each and offer a range of approximately 300 kilometers per charge, depending on the load. The initiative aims to reduce noise pollution and carbon emissions in urban areas.

- In January 2024, ACC Limited, a subsidiary of Ambuja Cements within the Adani Group, completed the acquisition of the remaining 55% equity stake in Asian Concretes and Cements Pvt Ltd (ACCPL). This strategic move enhances ACC's cement production capacity by 2.8 million tons per annum, elevating its total capacity to 38.6 million tons per annum. When combined with Ambuja Cements, the Adani Group's consolidated cement capacity reaches 76.1 million tons per annum.

Companies Covered in Self-Compacting Concrete Market

- BASF SE

- CEMEX S.A.B. de C.V

- ACC Limited

- SIKA AG

- LafargeHolcim

- Kilsaran

- HEIDELBERGCEMENT AG

- Tarmac

- Unibeton Ready Mix

- Ultratech Concrete

- Ambuja Cements Ltd.

Frequently Asked Questions

The global self-compacting concrete market is projected to reach US$ 14.5 Bn in 2025, driven by demand for high-performance concrete.

The market is driven by construction market growth to US$ 15 Tn by 2030 and need for vibration-free concrete in complex projects.

The market is poised to witness a CAGR of 5.8% from 2025 to 2032, supported by sustainable mix innovations.

Eco-friendly self-compacting concrete with recycled aggregates offers opportunities for green building certifications.

BASF SE, CEMEX, SIKA AG, LafargeHolcim, and HEIDELBERGCEMENT AG lead through sustainable and high-performance SCC solutions.