- Electric Mobility

- Self-Driving Bus Market

Self-Driving Bus Market Size, Share, and Growth Forecast, 2026 - 2033

Self-Driving Bus Market by Level of Automation (Level 3, Level 4, Level 5), Component (Hardware, Software, Services), Propulsion Type (Internal Combustion Engine (ICE), Electric Self-Driving Buses (BEV), Hybrid Buses), and Regional Analysis for 2026 - 2033

Self-Driving Bus Market Size and Trends Analysis

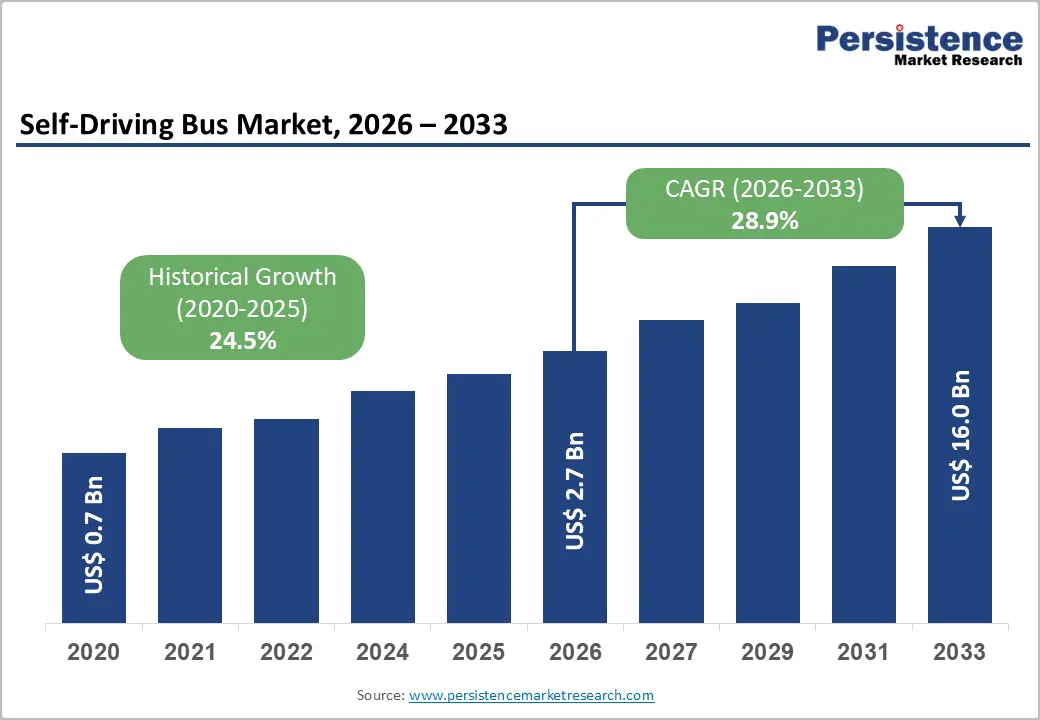

The global Self-Driving Bus market size is valued at US$ 2.7 Bn in 2026 and is projected to reach US$ 16.0 Bn by 2033, growing at a CAGR of 28.9% between 2026 and 2033. The market is experiencing robust expansion, propelled by the convergence of artificial intelligence (AI), advanced sensor ecosystems, and electric drivetrain technologies that collectively lower deployment barriers for driverless public transport.

Governments across North America, Europe, and the Asia Pacific are embedding autonomous transit within wider smart-city frameworks; in January 2024, China's Ministry of Industry and Information Technology (MIIT) and four other ministries jointly launched Vehicle-Road-Cloud Integration pilot projects across 20 cities, while the European Union committed €2.5 billion (US$ 2.8 billion) to autonomous bus projects in May 2025. Rising urbanisation, labour cost pressures on transit operators, and zero-emission mobility mandates further reinforce demand across both fixed-route and on-demand corridor deployments worldwide.

Key Industry Highlights:

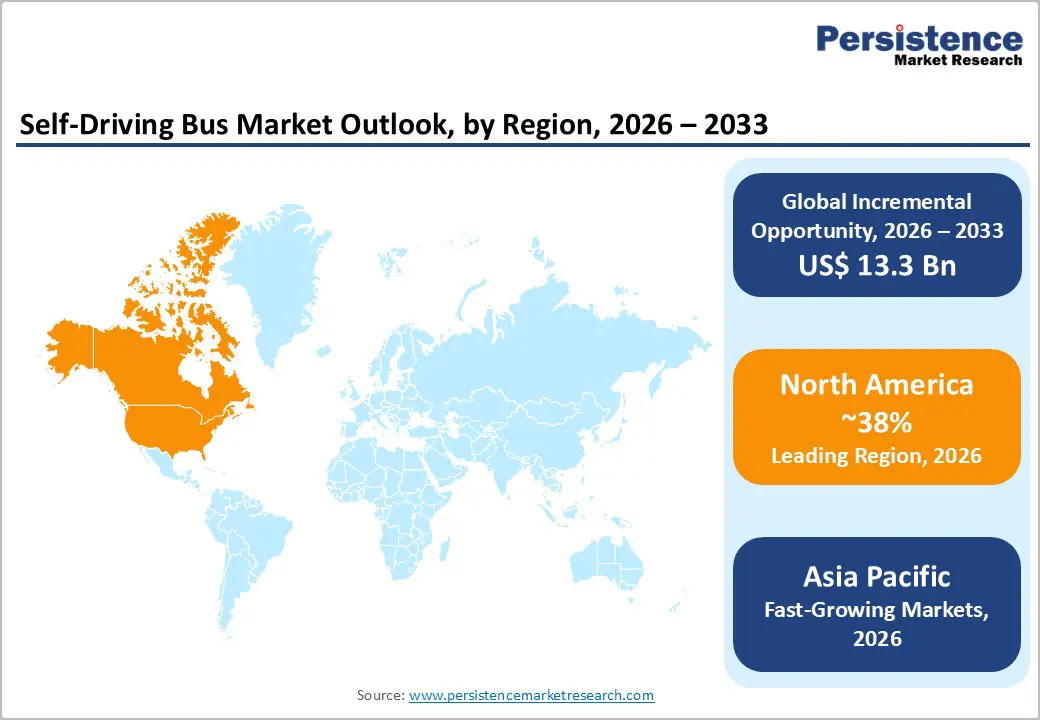

- Leading Region: North America leads the global self-driving bus market, commanding approximately 38% of the autonomous bus software segment. The U.S. innovation ecosystem, California's progressive AV regulatory environment, and government-backed pilot programs sustain its market leadership position.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by China's aggressive Level 4 commercialization across 20+ cities, Japan's autonomous bus deployment target for the 2025 Osaka Expo, South Korea's US$ 1 billion AV commitment, and India's 2024 AV testing framework.

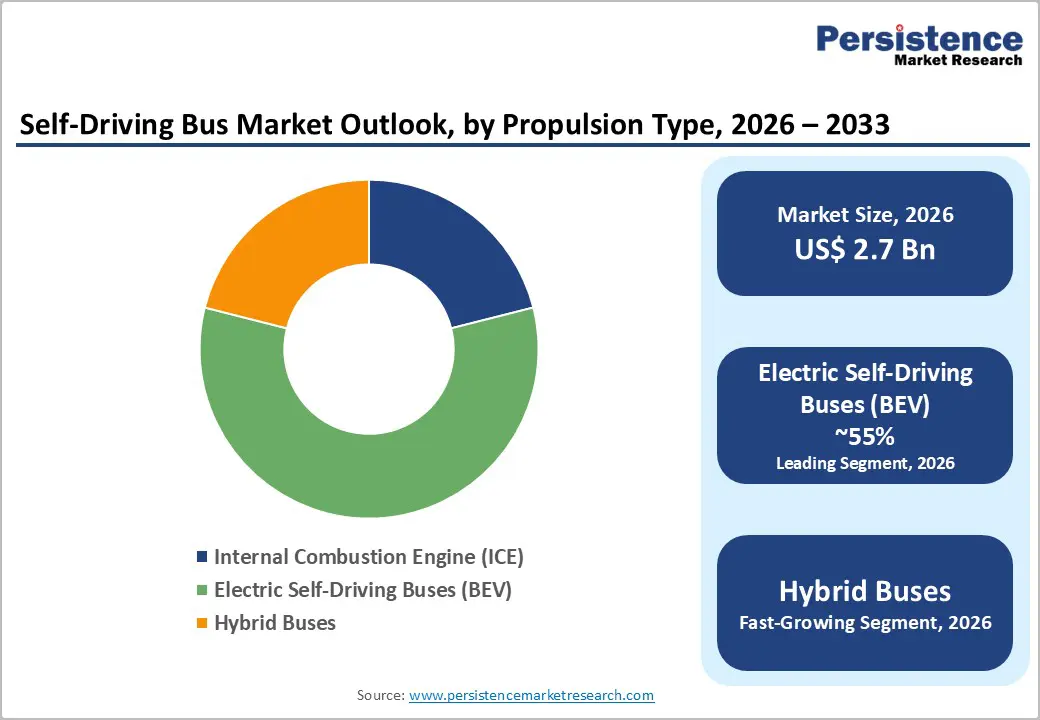

- Dominant Segment: The Electric Self-Driving Bus (BEV) propulsion segment leads with approximately 53% market share in 2026, propelled by zero-emission mandates, declining battery costs, and its status as the preferred autonomous bus development platform globally.

- Fastest Growing Segment: The Software component segment is the fastest-growing category, as MaaS platform revenues, AI navigation stack licences, and over-the-air update subscription models scale rapidly alongside commercial Level 4 fleet deployments worldwide.

- Key Market Opportunity: Level 4 autonomous bus commercialization in geo-fenced urban transit corridors offers the largest near-term revenue opportunity, with recurring MaaS, software subscription, and fleet management revenues projected to generate significant long-term value for early market entrants across 40–80 cities globally by 2035.

| Key Insights | Details |

|---|---|

|

Self-Driving Bus Market Size (2026E) |

US$ 2.7 Bn |

|

Market Value Forecast (2033F) |

US$ 16.0 Bn |

|

Projected Growth CAGR (2026–2033) |

28.9% |

|

Historical Market Growth (2020–2025) |

24.5% |

Market Dynamics

Drivers - Smart City Investments and Government-Led Autonomous Transit Frameworks

The rapid global proliferation of smart city programmers is among the most powerful demand catalysts for the self-driving bus market. National and municipal governments are channeling substantial capital into autonomous public transportation infrastructure, providing both funding certainty and regulatory clarity for operators. In January 2024, China's MIIT and four other ministries launched Vehicle-Road-Cloud Integration pilot programs across 20 cities, including Beijing and Shanghai, specifically promoting Level 4 unmanned commercial applications.

In December 2024, Germany adopted its "Strategy for Autonomous Driving in Road Traffic" and published an operational area approval guideline, translating the country's pioneering Autonomous Vehicles Approval and Operation Ordinance (AFGBV) into actionable deployment pathways. Meanwhile, Japan has set a national target for nationwide Level 4 rollout and prioritized autonomous bus services at the 2025 Osaka Expo. These government-backed ecosystems reduce regulatory risk, offer co-investment models, and supply the infrastructure backbone, including dedicated autonomous corridors that create a reliable commercial runway for accelerating fleet adoption at scale.

Advancements in AI, LiDAR Sensing, and 5G Connectivity

Continuous innovation in artificial intelligence, LiDAR perception, V2X communication, and onboard compute platforms is transforming the cost and reliability profile of autonomous buses. Driverless bus platforms equipped with 360-degree LiDAR arrays and AI-powered decision-making algorithms can now navigate complex urban environments with a measurable level of dependability. Alphabet's Waymo invested approximately US$ 5 billion into its sixth-generation autonomous driving system in 2024, while in January 2025, NVIDIA secured a strategic investment of US$ 200 million from SoftBank Vision Fund 2 to accelerate the deployment of its Drive AGX autonomous platform. Approximately 45% of new autonomous bus models launched in 2023–2024 incorporate embedded 5G hardware modules, enabling real-time communication with traffic management systems. Published research indicates that autonomous bus services have the potential to reduce transit travel costs by 6%–11%, strengthening the economic justification for fleet transition and driving accelerated commercialization across urban transit corridors globally.

Restraint - High Capital Expenditure and Complex Technology Integration

One of the foremost structural barriers to mass self-driving bus deployment is the prohibitive upfront cost associated with redundant sensor arrays, AI compute hardware, and multi-supplier system integration. LiDAR units, RADAR modules, high-definition cameras, and V2X communication hardware collectively raise bus production costs significantly above those of conventional vehicles.

Survey data indicates that approximately 37% of public transit operators cite high acquisition costs as the primary obstacle to autonomous fleet adoption. For agencies operating under constrained public budgets, economics remain challenging without substantial subsidies or innovative leasing structures. The engineering complexity of certifying diverse multi-vendor hardware and software stacks to safety standards, compounded by heterogeneous urban operating environments, further extends development timelines and adds commercialization risk for both OEMs and independent technology providers.

Cybersecurity Vulnerabilities and Public Acceptance Deficit

As inherently connected systems, self-driving buses present expanded attack surfaces for cyber threats. Driverless platforms depend on continuous data exchange across V2X networks, cloud platforms, and fleet management systems, creating potential vectors for compromising safety-critical vehicle functions. Technavio research identifies cybersecurity risks as a primary market challenge, with autonomous buses particularly vulnerable to intrusions targeting navigation and communication systems.

Concurrently, public acceptance remains a significant structural restraint. Studies indicate that approximately 37% of potential commuters express hesitancy toward boarding driverless buses, citing safety concerns. Building the trust required for mass adoption demands rigorous third-party safety certification, transparent publication of operational data, and continued accumulation of incident-free service hours from live pilot deployments across diverse urban environments.

Opportunities - Electric Self-Driving Buses (BEV) as the Fastest-Growing Deployment Platform

The convergence of vehicle electrification and autonomous driving represents the most commercially compelling near-term opportunity in the self-driving bus market. Battery-electric autonomous buses are emerging as the preferred development and procurement platform globally, driven by tightening urban emissions regulations, declining battery costs, and operator demand for lower total cost of ownership. In March 2024, Transdev launched the world's first autonomous electric bus line in the Netherlands, marking a milestone in the commercialization of BEV autonomous public transit. Yutong Group, recognized as the world's largest bus manufacturer by volume as of 2026, had cumulatively sold over 210,000 new energy buses by the end of 2025, underscoring the scale of the electric bus transition already underway. As battery energy density improves and charging infrastructure expands across the EU, China, and key ASEAN nations, BEV autonomous buses are positioned to dominate fleet procurement, offering market participants a structural revenue opportunity in both vehicle sales and the associated MaaS platform ecosystems.

Level 4 Autonomous Bus Commercialization in Urban Transit Corridors

The transition from pilot deployments to large-scale commercial operations of Level 4 autonomous buses represents a transformative revenue opportunity for technology providers, OEMs, and transit operators. In December 2025, China issued its first national approvals for Level 3 automated driving to Changan Group (Deepal SL03) and BAIC Group (Arcfox Alpha S), establishing the policy precedent for progressive Level 4 commercial expansion in Chinese cities. Baidu's Apollo RT6, unveiled in 2024, demonstrated mass-producible Level 4 autonomous bus capability. According to a World Economic Forum/Boston Consulting Group white paper on autonomous vehicles, fleets of robotaxis are expected to operate at scale in 40 to 80 cities worldwide by 2035. For market participants, this transition unlocks recurring revenue from software subscriptions, over-the-air updates, fleet management platforms, and Mobility-as-a-Service (MaaS) models. Companies that establish early commercial presence in Level 4 urban corridors, particularly in geo-fenced smart city zones, will secure structural competitive advantages as regulatory frameworks mature globally.

Category-wise Analysis

Level of Automation Insights

Within the Level of Automation category, the Level 4 segment holds the leading position, accounting for approximately 42% of the global self-driving bus market revenue in 2026. Level 4 systems, characterized by full automation within defined operational design domains without requiring human intervention, represent the commercial sweet spot where safety certification, investor confidence, and transit agency procurement strategies converge.

China's ambitious urban deployment programme extending Level 4 robotaxi and robobus services across major cities, including Beijing, Shanghai, Shenzhen, and Wuhan, has created the world's most commercially mature Level 4 operating environment. The MIIT's January 2024 directive explicitly targets Level 4 unmanned commercial applications within its Vehicle-Road-Cloud Integration pilots, reinforcing institutional and infrastructure support. Meanwhile, Germany's AFGBV provides the EU's first comprehensive national approval pathway specifically for Level 4 public transport vehicles, validating the tier's commercial viability across diverse regulatory environments and confirming its dominant position over the Level 3 and Level 5 segments in near-to-medium-term revenue generation.

Component Insights

The Hardware segment dominates the Component category, accounting for approximately 47% of the global self-driving bus market in 2026. Hardware encompasses LiDAR systems, RADAR sensors, high-definition cameras, V2X communication modules, and onboard compute platforms, including NVIDIA's Drive AGX, which constitute the essential physical backbone of autonomous operation. The capital-intensive nature of hardware procurement, combined with the mandatory deployment of redundant sensor arrays required for functional safety certification, sustains the segment's revenue primacy across the value chain.

Approximately 45% of new autonomous bus models launched in 2023–2024 incorporate embedded 5G hardware modules, underscoring V2X hardware as a critical and rapidly growing sub-component. While the Software segment is projected to grow faster as MaaS platforms, AI navigation stacks, and over-the-air update revenues scale with commercial fleet expansion, Hardware will remain the highest-value component category throughout the near-to-medium-term forecast horizon.

Propulsion Type Insights

The Electric Self-Driving Bus (BEV) segment dominates the Propulsion Type category with an estimated 53% share of the global self-driving bus market in 2026, consistent with Persistence Market Research's estimate that electric fuel type accounts for approximately 52.9% of the broader autonomous bus market. The alignment of vehicle electrification trends with autonomous driving technology has made BEV platforms the preferred base for virtually all leading autonomous bus manufacturers and operators globally.

Battery capacity for self-driving buses has advanced to a maximum of 630 kWh as of early 2025 (per Yutong platform specifications), enabling extended operational ranges matched to fleet deployment requirements. The zero-emission profile of BEV autonomous buses aligns directly with tightening EU and major Asian economy urban emission regulations. Lower per-kilometer energy costs and reduced drivetrain mechanical complexity relative to ICE platforms further improve the economic case, particularly as predictive, optimized autonomous routing maximizes battery efficiency and reduces operational expenditure for transit agencies.

Regional Insights and Trends

North America Leads Autonomous Bus Software Growth

North America holds a leading position in the global self-driving bus market, anchored by the United States' advanced innovation ecosystem, robust venture and corporate R&D investment, and progressively supportive regulatory framework. The region commands approximately 38% of the global autonomous bus software segment, with the U.S. generating US$ 273.6 million in autonomous bus software revenue in 2024 alone. Active pilot programs in cities including Las Vegas, Austin, and San Francisco are generating critical real-world operational datasets that accelerate commercial validation and regulatory confidence.

The regulatory environment is increasingly constructive: as of December 2024, approximately half of U.S. states have enacted some form of autonomous vehicle legislation. Waymo continues to operate the world's most commercially advanced Level 4 ride-hailing service across multiple U.S. cities, with Alphabet having invested US$5 billion in its sixth-generation autonomous driving system in 2024. Canada's Ontario province contributes to the AV ecosystem through suppliers such as BlackBerry QNX and Magna International. North America is expected to register the highest growth rate among all regions during the 2026–2033 forecast period.

European Autonomous Bus Market Driven by Regulation

Europe is consolidating its position as a structurally organized market for the commercialization of self-driving buses, underpinned by progressive national legislation and emerging regional harmonization frameworks. Germany remains the continent's regulatory vanguard: building upon its landmark AFGBV (2022), the government published a comprehensive operational area approval guideline in 2024 and adopted its national "Strategy for Autonomous Driving in Road Traffic" in December 2024, the first EU nation to establish a full end-to-end Level 4 public transit approval and deployment pathway. The United Kingdom's Automated Vehicles Act 2024, which received Royal Assent in May 2024, introduced one of the world's most comprehensive AV legal frameworks outside China and Germany.

In March 2024, Transdev launched the world's first autonomous electric bus line in the Netherlands, a landmark for the integration of BEV-autonomous buses in European public transit. The EU announced its €2.5 billion (US$ 2.8 billion) investment in autonomous bus projects in May 2025, aiming to secure European leadership in autonomous public transportation. France mandated event data recorders in all autonomous vehicles from 2025, while Spain and the Nordic countries are advancing AV pilot environments with structured government-backed frameworks. Europe's stringent zero-emission mandates, reinforced by the EU's prohibition on new ICE vehicle sales beyond 2035, are compelling transit operators to pursue simultaneous electrification and automation, creating a powerful dual-transition dynamic underpinning BEV autonomous bus adoption across the region.

Asia Pacific Leads Autonomous Bus Expansion

Asia Pacific represents both the fastest-growing and most strategically diverse region in the global self-driving bus market. China leads with the world's most extensive commercial autonomous vehicle deployment ecosystem, operating Level 4 robobus and robotaxi services across major metropolises including Beijing, Shanghai, Shenzhen, and Wuhan. Baidu's Apollo Go platform has reached 22 cities globally with a cumulative autonomous driving mileage exceeding 240 million kilometres as of December 2025. Shanghai's autonomous driving action plan targets 6 million Level 4 passenger trips by 2027, with 5,000+ kilometres of roads open for autonomous operation.

Japan targeted the launch of full-scale autonomous bus services in time for the 2025 Osaka Expo as part of a national Level 4 deployment programme. BYD and All Nippon Airways (ANA) conducted a successful ten-day autonomous bus trial at Haneda Airport in Japan a global first for BYD in real-world autonomous operations. South Korea has committed over US$ 1 billion in government support for autonomous vehicle development, enabling commercial AV pilot services in Seoul. India launched its AV testing regulations framework in 2024, targeting commercial deployment by 2030. Singapore and other ASEAN nations maintain structured regulatory environments for AV trials. The region's unmatched manufacturing scale, led by Yutong, which produces approximately 150,000 buses annually, combined with cost-competitive component ecosystems, gives Asia Pacific a durable advantage in autonomous bus production economics.

Competitive Landscape

The global self-driving bus market exhibits a fragmented competitive structure, with the top ten players collectively accounting for approximately 16% of market share as of 2024. This fragmentation reflects the early-stage nature of commercial deployments and the diversity of value chain participants ranging from traditional bus OEMs (AB Volvo, Yutong, MAN Truck & Bus) to pure-play autonomy technology firms (EasyMile, Navyo) and integrated AI platform providers (Baidu Apollo).

Key competitive strategies include cross-industry technology partnerships (e.g., Waymo–Volvo signed October 2024), MaaS business model development, and geographic expansion into smart city pilot zones. R&D investment in AI stack refinement, sensor fusion, and over-the-air update capabilities differentiates market leaders, while emerging players leverage niche segment focus and open-platform strategies to gain commercial footholds in fast-growing urban markets.

Key Industry Developments:

- In March 2026, Tier IV and Isuzu deployed Level 4 autonomous buses on NVIDIA DRIVE Hyperion, integrating Autoware software and DRIVE AGX Thor chip, enabling high-capacity, flexible electric and diesel public transit operations.

- In March 2026, Macau launched an AI-powered autonomous bus route connecting Hengqin border and Guangzhou Medical University hospital, advancing cross-border medical mobility and demonstrating real-world deployment of driverless public transportation systems.

- In August 2025, WeRide and Shenzhen Bus Group introduced Shenzhen’s first Level 4 fully driverless robobus line in Luohu District, marking a major milestone in urban autonomous public transport within high-density commercial zones.

- In May 2025, the European Union announced a €2.5 billion investment in autonomous bus projects, strengthening infrastructure development, accelerating commercialization, and positioning Europe as a global leader in next-generation public transportation systems.

- In January 2025, Level 3 autonomous bus technologies expanded into public transit networks, supporting robotaxi ecosystem integration and enabling gradual transition toward higher autonomy levels within urban mobility and smart city transportation frameworks.

- In October 2024, Waymo partnered with Volvo Buses to integrate autonomous driving systems into bus platforms, expanding deployment beyond ride-hailing into mainstream public transit and strengthening OEM–technology collaboration in autonomous mobility ecosystems.

- In March 2024, Transdev launched the world’s first autonomous electric bus line in the Netherlands, validating commercial viability of BEV-autonomous integration and marking a significant milestone in sustainable, driverless public transportation deployment.

Companies Covered in Self-Driving Bus Market

- AB Volvo

- Volkswagen AG

- Proterra

- Hyundai Motor Company

- Hino Motors, Ltd

- Apollo Baidu

- MAN Truck & Bus

- EasyMile

- New Flyer

- Toyota Motor Corporation

- Yutong Group

- Navyo

- Novus Hi-Tech Robotic Systemz

- COAST AUTONOMOUS, INC.

- W-Scope Corporation

- Waymo LLC

- Transdev

- WeRide

- Pony.ai

- Karsan Otomotiv

Frequently Asked Questions

The global Self-Driving Bus market is valued at US$ 2.7 Bn in 2026 and is projected to reach US$ 16.0 Bn by 2033, growing at a CAGR of 28.9% over the 2026–2033 forecast period. This robust trajectory is underpinned by Level 4 commercialisation, smart city infrastructure investments, and the accelerating convergence of autonomous and electric bus technologies worldwide.

The principal demand drivers include government-backed smart city transit investments exemplified by China's MIIT Vehicle-Road-Cloud Integration pilot across 20 cities and the EU's €2.5 billion (US$ 2.8 billion) autonomous bus investment alongside rapid advancements in AI, LiDAR, and 5G connectivity.

The Level 4 automation segment is the clear leader, holding approximately 42% of global self-driving bus market revenue in 2026. Commercially active Level 4 deployments in China operated by Baidu Apollo, Pony.ai, and WeRide and Germany's comprehensive AFGBV regulatory framework providing the EU's first Level 4 public transit approval pathway confirm this segment's dominant commercial position.

North America leads the global self-driving bus market, commanding approximately 38% of the global autonomous bus software segment and generating US$ 273.6 million in U.S. autonomous bus software revenue in 2024. The region's leadership is supported by the world's most advanced AV innovation ecosystem, progressive state and federal regulatory frameworks, and substantial government-backed pilot programmes across multiple major metropolitan areas.

The greatest near-term opportunity lies in the commercialisation of Level 4 autonomous bus operations across geo-fenced urban transit corridors particularly in China and European smart cities. This transition unlocks recurring revenue from MaaS platforms, software subscriptions, and over-the-air update services. The Electric Self-Driving Bus (BEV) segment simultaneously represents a structural procurement opportunity as electrification mandates and falling battery costs converge to accelerate fleet replacement globally.