- Beauty & Personal Care

- Self-tanning Products Market

Self-tanning Products Market Size, Share, and Growth Forecast 2026 - 2033

Self-tanning Products Market by Product Type (Lotions, Gels, Spray, Serum, Others), by Skin Type (Normal Skin, Dry Skin, Oily Skin, Sensitive Skin, Others), by Application (Men, Women), by Distribution Channel (Supermarkets or Hypermarkets, Convenience Stores, Brand Outlets, Online Sales, Others), by Regional Analysis, 2026 - 2033

Self-tanning Products Market Size and Trend Analysis

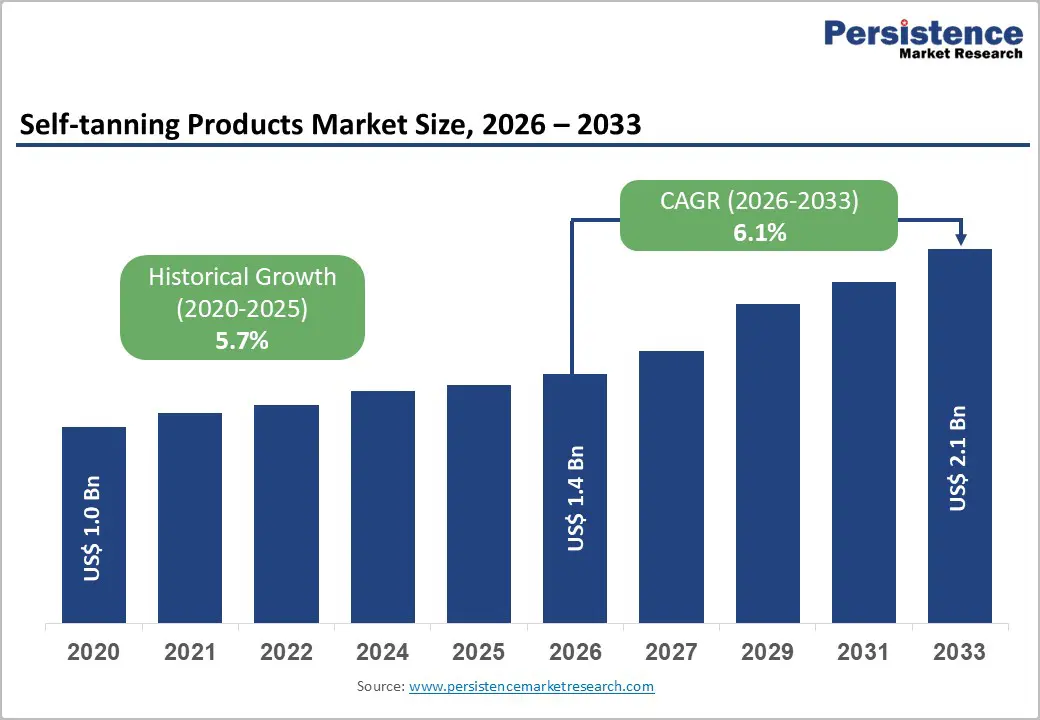

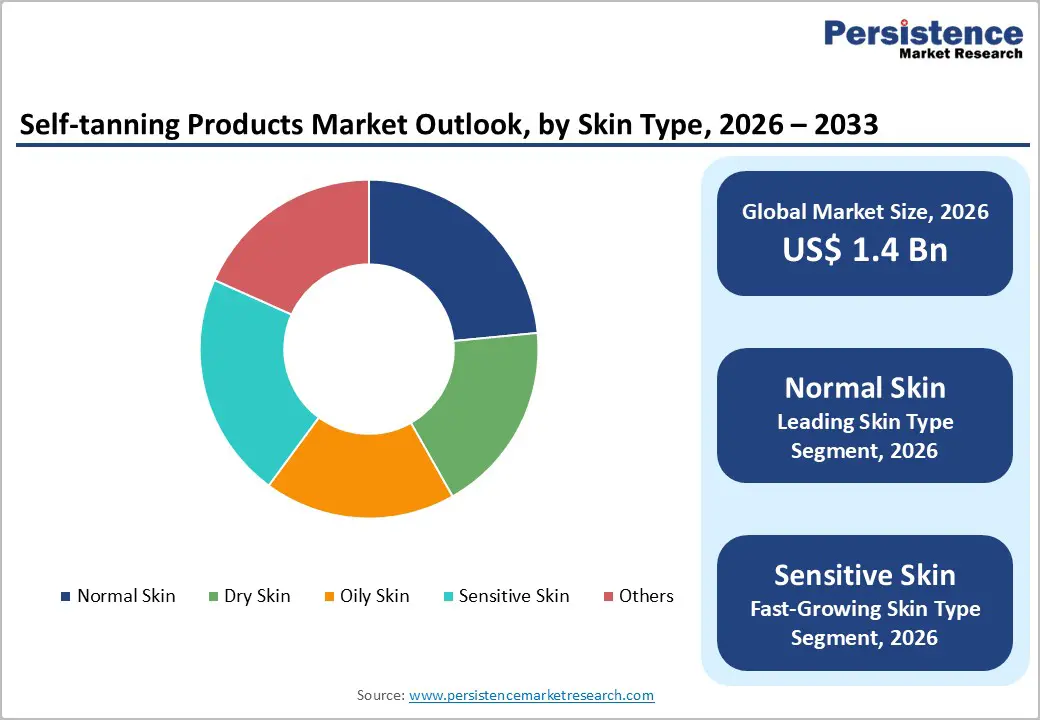

The global Self-tanning Products market size is expected to be valued at US$ 1.4 billion in 2026 and projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

Consumers worldwide are increasingly choosing self-tanning products as safer alternatives to sun exposure, motivated by growing awareness of UV radiation risks highlighted by public health organizations. Rising concerns about skin cancer and premature aging have shifted preferences toward DHA-based bronzers, offering a sun-free tanning solution. Social media trends, influencer recommendations, and dermatologist endorsements have further popularized these products. Additionally, the demand for clean, natural formulations aligns with broader skincare and wellness movements, driving adoption across diverse age groups and regions.

Key Market Highlights

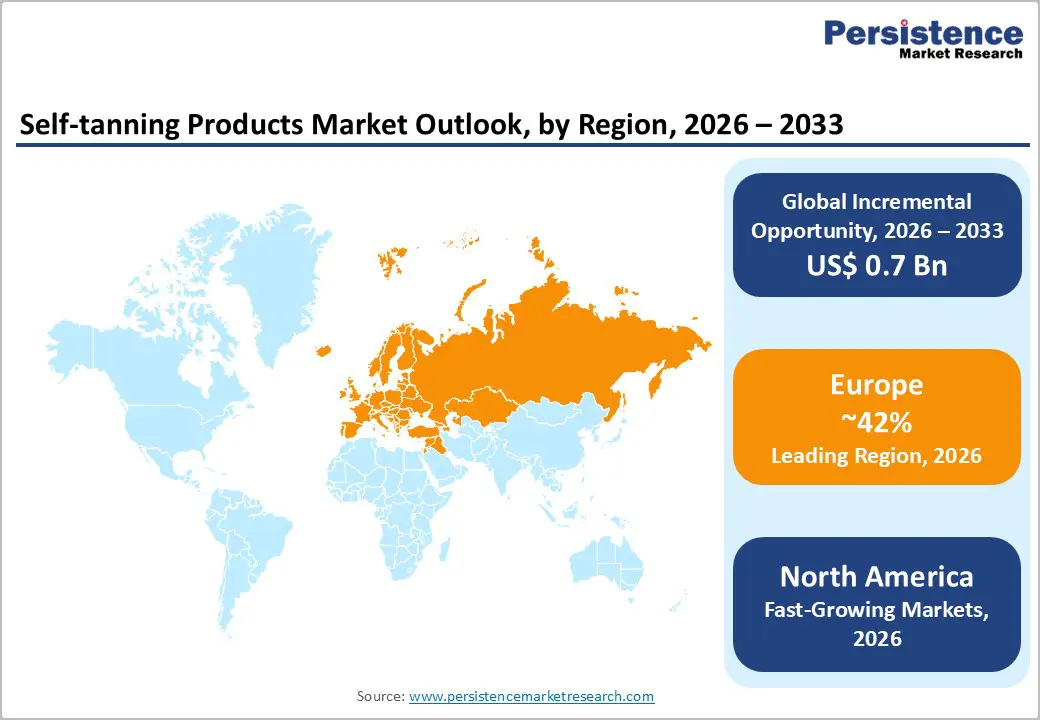

- Leading Region: Europe leads the self-tanning products market with a 41% share in 2025, driven by regulatory support and clean beauty trends.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market, fueled by urbanization, rising middle class, K-beauty influence, and e-commerce adoption.

- Leading Product Category: Lotions dominate the market with 45% share in 2025, preferred for hydration and ease of application.

- Fastest-Growing Distribution Channel: Specialty retail and direct-to-consumer channels are expanding rapidly through personalized experiences.

- Key Market Opportunity: Men’s grooming segment offers 22% potential for growth with tailored quick-dry, matte formulations.

| Key Insights | Details |

|---|---|

|

Self-tanning Products Size (2026E) |

US$ 1.4 billion |

|

Market Value Forecast (2033F) |

US$ 2.1 billion |

|

Projected Growth CAGR (2026-2033) |

6.1% |

|

Historical Market Growth (2020-2025) |

5.7% |

Market Dynamics

Drivers - Rising Consumer Health Awareness and Safety Concerns Driving Shift Toward Self-Tanning Products

Escalating concerns about skin cancer and premature aging caused by UV exposure are significantly motivating consumers to adopt self-tanning solutions. Public education initiatives and awareness campaigns emphasize the link between UV rays and long-term skin damage, encouraging safer alternatives. Dermatologists increasingly endorse sun-free tanning, positioning DHA-based bronzers as reliable preventive cosmetics. This awareness has shifted daily skincare routines, with a growing focus on sun protection.

As a result, consumers now consider self-tanners not only a cosmetic choice but also a health-conscious decision. The widespread acknowledgment of self-tanners’ safety profile has led to more consistent usage, integration into regular beauty regimens, and heightened demand among individuals seeking both aesthetic appeal and skin protection from harmful UV exposure.

Rising Popularity of Clean, Organic, and Natural Self-Tanning Formulations Influencing Market Demand

The surge in demand for clean beauty and natural ingredients has reshaped consumer preferences toward organic and vegan self-tanning products. Transparency in formulations and the use of plant-derived ingredients resonate strongly with Millennials and Gen Z, who prioritize sustainability and ethical production practices. Erythrulose-DHA combinations are increasingly used to achieve realistic, streak-free tans while avoiding harsh chemicals.

Regulatory encouragement and the rise of chemical-free mandates in various regions further drive innovation in clean formulations. Vegan and cruelty-free claims influence purchasing decisions, with consumers actively seeking environmentally responsible, skin-friendly products. This growing focus on natural ingredients ensures continuous expansion in adoption and loyalty for self-tanning products across diverse demographic groups.

Restraints - Skin Allergies and Formulation Complexities Limiting Wider Adoption of Self-Tanning Products

Allergic reactions to DHA and other formulation additives remain a significant restraint for the self-tanning market. Many users experience irritation or sensitivity, particularly those with delicate skin types. Common ingredients like propylene glycol and synthetic fragrances can trigger adverse responses, leading to product discontinuation. Despite efforts to produce hypoallergenic variants, these challenges limit acceptance among sensitive consumers.

Consequently, the prevalence of skin reactions elevates return rates and reduces overall consumer confidence. The need for safer, gentler formulations creates pressure on manufacturers to innovate while maintaining efficacy. Until these challenges are consistently addressed, broader mass-market adoption and sustained growth remain constrained, particularly among consumers seeking both performance and skin safety in self-tanning products.

High Pricing and Premium Positioning Creating Barriers for Price-Sensitive Consumers

The premium pricing of self-tanning products, often ranging from US$20-50 per unit, restricts access for cost-conscious buyers. Short product longevity leads to noticeable wastage during use, making repeated purchases expensive. Economic factors such as inflation further exacerbate affordability challenges, particularly in developing markets where disposable income is limited.

This price barrier reduces trial and repeat purchase rates, constraining market penetration and slowing adoption. As a result, the perceived premium nature of self-tanning products positions them as a niche segment, accessible mainly to affluent or urban consumers, and limits broader acceptance among price-sensitive demographics seeking more economical sun-free tanning options.

Opportunities - Expansion of the Men’s Grooming Segment Creating New Opportunities in Self-Tanning Products

The men’s self-tanning segment is showing strong growth potential as male consumers increasingly embrace personal care and grooming routines. Younger men, particularly those aged 18–34, are seeking bronzing solutions influenced by lifestyle trends and public figures. Quick-dry, matte formulations designed for active lifestyles appeal to this demographic, presenting a chance to capture untapped demand and expand the market beyond traditional female consumers.

By developing products and marketing campaigns specifically for men, brands can diversify portfolios and build loyalty. Tailoring textures, fragrances, and application methods to male preferences enables wider adoption, helping companies engage a segment that has historically been underserved in sunless tanning products.

Growth of E-Commerce and Digital Personalization Driving Self-Tanning Market Adoption

The rise of e-commerce has transformed consumer access to self-tanning products, with online platforms seeing significant spikes in searches and purchases. Digital tools like AI-powered shade matching and virtual try-on experiences improve selection accuracy and reduce product returns, enhancing customer satisfaction.

Subscription models and online-exclusive offerings cater to convenience-oriented shoppers, particularly in regions such as Asia-Pacific. Personalization and digital engagement enable brands to reach broader audiences, increase repeat purchases, and strengthen consumer loyalty, making e-commerce a critical growth channel for self-tanning products.

Category-wise Analysis

Product Type Insights

Lotions command the largest share in the self-tanning market, accounting for 45% in 2025. Their dominance is driven by superior hydration, even application, and stability of DHA, making them reliable for daily use across diverse climates. User feedback highlights preference for moisturizing bases that glide smoothly over body surfaces, contributing to consistent, natural-looking results. Lotions have become a staple in self-tanning routines, particularly for consumers seeking both cosmetic and skin-nourishing benefits.

While lotions lead, sprays, mousses, and serums are emerging as the fastest-growing formats. These categories appeal to users seeking quick-dry, customizable, and precision application options. Sprays offer convenience for hard-to-reach areas, and serums allow intensity control, attracting tech-savvy and younger consumers who prioritize flexibility, speed, and innovative product experiences.

Skin Type Insights

Normal skin secures the largest share in 2025 at 40%, reflecting broad compatibility with various formulations. Representing a significant portion of the population, normal skin supports extensive product ranges without irritation risks. Trials indicate optimal color development and uniform coverage, driving leadership in reliable outcomes. Consumers with normal skin enjoy predictable results, which reinforces consistent product use and preference for mainstream self-tanning solutions.

In contrast, sensitive skin is emerging as the fastest-growing category. Manufacturers are increasingly formulating gentle, hypoallergenic products tailored for delicate skin types. These innovations, often free from harsh chemicals and fragrances, are attracting cautious users seeking sun-free tanning options without compromising safety, highlighting the market’s responsiveness to inclusivity and skin-specific needs.

Application Insights

Women dominate self-tanning usage with a 75% share in 2025, reflecting deep integration into daily beauty and skincare routines. High female consumption is influenced by cultural standards linking a tan to health and attractiveness, alongside significant media exposure and social events. Women account for a majority of skincare spending, further reinforcing their leadership in market adoption. The 3:1 female-to-male purchase ratio underscores the gendered nature of current consumption patterns.

The male segment is the fastest-growing application category. Increasing awareness of grooming, influence from lifestyle trends, and product designs catering to male preferences—such as matte finishes and quick-dry formulations—are driving adoption. Men are gradually embracing self-tanning as part of everyday personal care, opening new avenues for market expansion and targeted product development.

Distribution Channel Insights

Online sales hold the largest share at 35% in 2025, fueled by convenience, guided tools, and widespread e-commerce adoption. Platforms have seen a 40% increase in beauty product sales since 2020, with consumers benefiting from tutorials, reviews, and personalized recommendations. Pandemic-related shifts further validated the reach and accessibility of online channels, establishing them as a dominant route to market.

While online dominates, specialty retail outlets and direct-to-consumer channels are expanding rapidly. These formats offer immersive brand experiences, personalized consultations, and trial opportunities that appeal to consumers seeking hands-on interaction. Salons, spas, and boutique stores provide tailored advice and exclusive products, enhancing engagement and fostering loyalty among discerning users.

Regional Insights

North America Self-tanning Products Market Trends and Insights

North America holds a 32% share, making it the second-largest self-tanning market. Adoption is fueled by U.S. FDA safety regulations, which cap DHA levels at 15% and enhance consumer confidence. Dermatologist endorsements and public health awareness campaigns promote sun-free tanning alternatives. California and other innovation hubs drive premium product launches with organic certifications, advanced serums, and high-quality formulations appealing to health-conscious consumers.

While the market is mature, sprays, serums, and customizable products are gaining popularity among consumers seeking convenience and precision. Online channels and e-commerce platforms provide accessibility, enabling wide-reaching distribution and sustained adoption of both mainstream and premium self-tanning products.

Europe Self-tanning Products Market Trends and Insights

Europe leads the global self-tanning market with a 41% share, driven by high consumer awareness and strict regulatory standards such as EC No 1223/2009. Countries like Germany, the U.K., France, and Spain are at the forefront, benefiting from harmonized regulations that ensure safe and consistent formulations. Clean beauty trends have boosted retail adoption, with eco-friendly and sustainable luxury products gaining traction, particularly in France, where organic and natural innovations are prioritized.

The market continues to expand steadily with a CAGR of 6.5%, supported by innovations in multifunctional products, texture improvements, and dermatologist-endorsed formulations. Specialty retail and e-commerce channels complement traditional outlets, allowing brands to reach a broad audience and maintain leadership in premium self-tanning solutions across Europe.

Asia Pacific Self-tanning Products Market Trends and Insights

Asia Pacific is the fastest-growing self-tanning market, with rapid expansion driven by China, Japan, India, and ASEAN countries. Rising middle-class populations, increasing disposable incomes, and K-beauty influence are accelerating adoption of both natural and innovative self-tanning products. Regulatory approvals in the region support safe, herbal-based formulations, while manufacturing hubs help reduce costs and facilitate broader distribution.

Consumer awareness about UV safety and cosmetic wellness is increasing, particularly among younger demographics. E-commerce, social media engagement, and influencer marketing amplify reach, while trends toward organic, vegan, and multifunctional products cater to evolving preferences. These factors position Asia Pacific as the region with the highest growth potential globally.

Competitive Landscape

The self-tanning products market is moderately consolidated, with major players maintaining strong positions while niche brands compete through innovation. Companies focus on developing streak-free, quick-dry, and customizable formulations to differentiate themselves. Continuous R&D and product innovation remain central to capturing consumer attention and building brand loyalty in a competitive environment.

Key strategies include influencer marketing, clean and natural labeling, and sustainability initiatives to appeal to conscious consumers. Direct-to-consumer subscriptions and online engagement are increasingly adopted to strengthen customer relationships, expand reach, and drive repeat purchases, creating a dynamic and evolving competitive landscape.

Key Developments:

- In June 2025, L’Oréal enhanced the St. Tropez mist to improve water-resistance, making it more suitable for active users and outdoor activities. The upgrade ensures longer-lasting results while maintaining streak-free, natural-looking coverage.

- In March 2024, Bondi Sands launched Vegan Society-certified serums targeting millennials, combining cruelty-free ingredients with effective bronzing. These formulations provide customizable tanning intensity while appealing to eco-conscious consumers who prioritize ethical and sustainable beauty products.

- In October 2023, Tan-Luxe introduced hyaluronic sprays, designed for hydration and streak-free application. Trial results confirmed improved skin moisture and smooth, even color development, enhancing user experience while maintaining natural-looking sunless tanning results.

Companies Covered in Self-tanning Products Market

- St. Tropez

- Bondi Sands

- Tan-Luxe

- L'Oréal Paris

- Estée Lauder

- The Body Shop

- Lancôme

- Jergens

- Coola

Frequently Asked Questions

US$ 1.4 billion in 2026, expected to reach US$ 2.1 billion by 2033.

Rising awareness of UV damage and skin safety, with consumers shifting to sun-free DHA-based bronzers.

Europe leads with a 41% share in 2025, supported by regulatory compliance, clean beauty trends, and premium offerings.

Asia Pacific is the fastest-growing region, driven by urbanization, rising middle-class populations, K-beauty influence, and e-commerce expansion.

The men’s grooming segment offers significant potential, with tailored quick-dry and matte formulations targeting untapped demand.