- Advanced Materials

- Self-Cleaning Glass Market

Self-Cleaning Glass Market Size, Share, and Growth Forecast, 2026 – 2033

Self-Cleaning Glass Market by Coating Type (Hydrophilic, Hydrophobic), Application (Facades, Windows, Roofs, Skylights, Automotive Windows, Solar Panels), End-User (Buildings & Construction, Automotive & Transportation, Solar Energy, Others), and Regional Analysis for 2026-2033

Self-Cleaning Glass Market Share and Trends Analysis

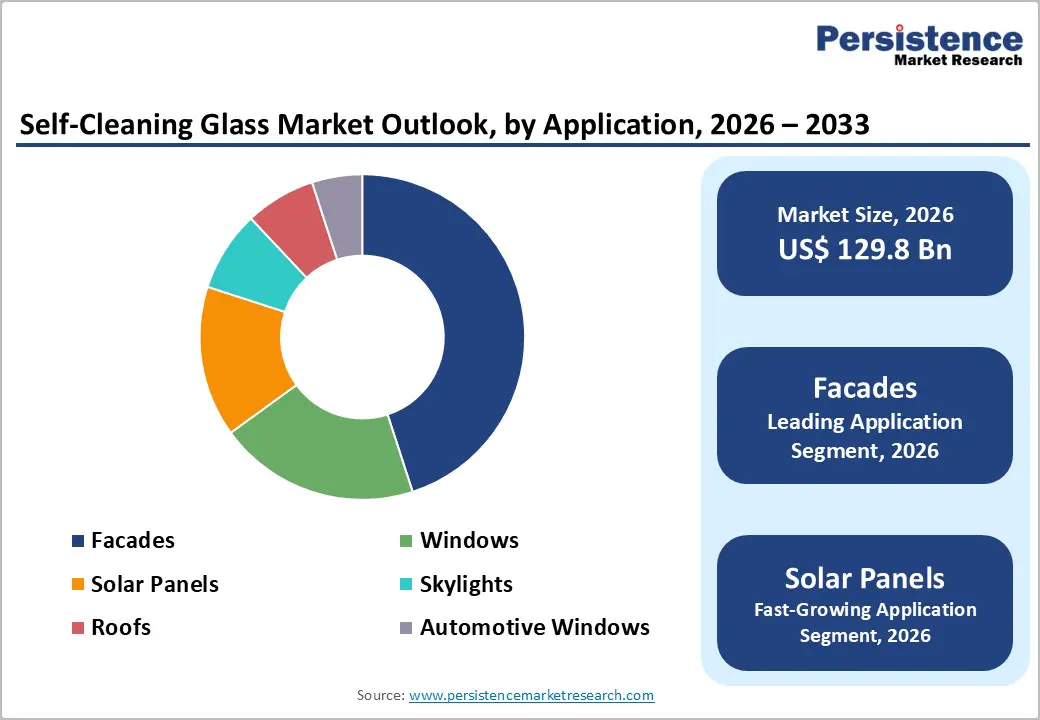

The global self-cleaning glass market size is likely to be valued at US$ 129.8 billion in 2026, and is projected to reach US$ 176.6 billion by 2033, growing at a CAGR of 4.5% during the forecast period 2026−2033.

The promising growth trajectory of the market is supported by increasing urban density, vertical construction activity, and long-term cost optimization priorities across commercial and residential infrastructure. Growth reflects rising demand for building materials that reduce maintenance intensity while aligning with sustainability mandates and lifecycle cost management objectives. Adoption strengthens as asset owners, facility managers, and developers prioritize materials that minimize manual cleaning, water consumption, and chemical usage across large surface installations. Technological integration represents a decisive factor, as advances in nanotechnology-enabled coatings improve durability, optical clarity, and functional lifespan under varied climatic conditions. Regulatory frameworks promoting green buildings and energy-efficient construction further reinforce demand, particularly in public infrastructure and commercial real estate developments. Increasing awareness regarding occupational safety contributes to reduced reliance on high-risk façade cleaning practices, creating additional adoption incentives.

Key Industry Highlights

- Dominant Region: By 2026, Europe is expected to lead with around 36% share, driven by strict building codes, dense vertical construction, and sustainability-focused procurement.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market from 2026 to 2033, owing to large-scale infrastructure expansion and rising demand for maintenance-efficient glazing in high-density developments.

- Leading Application: Facades are expected to lead with about 45% share in 2026 as large commercial and mixed-use developments prioritize durable, low-maintenance glazing to manage high exposure and long-term performance requirements.

- Fastest-growing Application: Solar panels are anticipated to be the fastest-growing segment through 2033, fueled by efficiency optimization, digital performance monitoring, and factory-level coating integration.

| Key Insights | Details |

|---|---|

|

Self-Cleaning Glass Market Size (2026E) |

US$ 129.8 Bn |

|

Market Value Forecast (2033F) |

US$ 176.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Urban Infrastructure Expansion and Maintenance Cost Rationalization

Urbanization trends intensify demand for high-rise buildings, commercial complexes, transportation hubs, and public infrastructure with extensive glass surface areas. As building height and façade complexity increase, traditional cleaning methods generate higher labor costs, safety exposure, and operational disruption. Self-Cleaning Glass directly addresses these structural challenges by reducing cleaning frequency through photocatalytic and hydrophilic surface mechanisms activated by natural light and rainwater. This functional attribute aligns with long-term asset management strategies focused on operating expenditure reduction rather than upfront material cost minimization.

Government-backed urban development programs and smart city initiatives reinforce adoption by prioritizing materials that enhance building efficiency and safety compliance. Construction authorities increasingly recognize façade maintenance risks associated with manual cleaning at elevation, leading to greater acceptance of passive cleaning technologies. Reduced dependency on scaffolding, suspended platforms, and chemical agents lowers liability exposure for property owners and contractors. The driver effect strengthens further as large-scale commercial developments seek predictable maintenance budgets and improved building uptime, creating sustained demand for self-cleaning glass across new construction and renovation cycles.

Sustainability Regulations and Green Building Frameworks

Environmental policy frameworks play a central role in driving self-cleaning glass adoption across developed and emerging markets. Green building certification systems emphasize water conservation, chemical reduction, and lifecycle environmental impact, positioning self-cleaning glass as a compliant architectural material. Photocatalytic coatings contribute to lower water usage by enabling rain-assisted cleaning, supporting compliance with municipal water conservation regulations in urban centers experiencing supply constraints.

Public procurement standards increasingly integrate sustainability criteria for government buildings, transport terminals, and educational institutions, reinforcing material selection bias toward low-maintenance, environmentally responsible glazing solutions. Regulatory encouragement of energy-efficient envelopes also indirectly supports self-cleaning glass integration, as advanced coatings maintain optical clarity and daylight transmission over time. These policy-driven shifts translate into higher baseline demand across institutional and commercial projects, embedding self-cleaning glass within regulatory-aligned construction specifications rather than optional upgrades.

Barriers Analysis- Performance Variability across Climatic and Environmental Conditions

Operational reliability weakens when functional outcomes fluctuate across diverse environmental settings, reducing confidence among specifiers, developers, and facility managers. The self-cleaning mechanism depends on stable interaction between surface chemistry, ultraviolet activation, moisture availability, and contaminant characteristics. Variations in sunlight exposure, rainfall frequency, temperature cycles, and airborne pollutant composition directly influence reaction efficiency and surface wetting behavior. In low-irradiance regions or prolonged dry climates, activation cycles slow and natural rinsing remains insufficient, resulting in residue buildup and visible streaking. Industrial dust, traffic-related particulates, and organic deposits further interfere with surface reactions, creating inconsistent visual and functional results.

Environmental diversity across geographies and seasons intensifies performance uncertainty during large-scale deployment. Coastal salinity, desert dust abrasion, tropical humidity, and cold-climate condensation cycles interact differently with coating layers, accelerating functional degradation in some locations while maintaining acceptable performance in others. These variations complicate standardized specification across multinational construction programs and increase risk exposure for warranty and service commitments. Discrepancies between controlled testing conditions and real-world exposure challenge validation processes delay regulatory and stakeholder acceptance.

Limited Long-Term Durability under Harsh Exposure

The restraint stems from intrinsic limitations in surface engineering used to enable self-cleaning functionality. The technology relies on ultra-thin active coatings that interact with light, moisture, and contaminants to maintain cleanliness. Under continuous exposure to ultraviolet radiation, airborne particulates, chemical pollutants, and temperature fluctuations, these coatings experience gradual chemical and structural degradation. Mechanical abrasion from wind-borne dust and routine environmental contact erodes surface properties that support water dispersion and contaminant breakdown. Thermal expansion mismatch between coating layers and the glass substrate introduces micro-level stress, leading to surface defects and reduced functional stability over time. These degradation pathways shorten effective service life in demanding outdoor environments.

From a business and asset management perspective, durability limitations weaken the long-term value proposition in large-scale architectural and transportation installations. Performance inconsistency across climates raises concerns around reliability, particularly in urban and industrial regions where pollution levels are elevated. As cleaning efficiency declines, end users face increased maintenance intervention that offsets expected operational savings. This dynamic complicates lifecycle cost planning and increases perceived risk for developers, facility operators, and infrastructure investors.

Opportunity Analysis- Integration with Solar Energy and Renewable Infrastructure

Alignment with solar installations and clean power assets elevates strategic relevance through sustained performance, operational discipline, and return optimization. Energy-generating surfaces face continuous exposure to dust, airborne particulates, salts, and industrial residues that suppress light transmission and create output volatility. Maintenance-intensive cleaning schedules increase operating expenditure, water consumption, and safety risk, challenging efficiency targets set by asset owners and utilities. Advanced surface solutions address these constraints by limiting contaminant adhesion and enabling passive cleaning under natural conditions. Stable transparency supports predictable energy yield, strengthens compliance with performance-linked contracts, and safeguards equipment warranties tied to output thresholds.

Renewable infrastructure expansion across buildings, transport corridors, urban utilities, and energy-integrated façades amplifies demand for materials that support sustainability mandates and automated asset management. Infrastructure planners favor components that reduce lifecycle maintenance, conserve water resources, and integrate seamlessly into digital monitoring frameworks. Passive cleanliness supports remote performance assessment, lowers downtime exposure, and enhances reliability across geographically dispersed assets. Procurement strategies increasingly emphasize compatibility with large-scale manufacturing, standard glazing systems, and regulatory certifications to enable rapid deployment across project portfolios.

Emerging Market Urban Development and Commercial Real Estate Growth

Urbanization and commercial real estate expansion in emerging markets are creating scale and quality-driven demand for premium building materials that minimize maintenance costs while supporting modern architectural and sustainability goals. Government strategies are allocating substantial resources to urban transformation, such as a 1 lakh crore urban challenge fund to promote cities as growth hubs under the Union Budget 2025-26, which directly stimulates large-scale redevelopment, infrastructure upgrades and private-sector engagement in urban projects. As population concentrations in cities increase, office and mixed-use developments require glass facades that reduce lifecycle service burdens and align with government policies favoring sustainable and low-maintenance infrastructure.

The quality and pace of construction in emerging economies also shape procurement criteria for façade materials. As urban centers densify, stakeholders prioritize materials that offer demonstrable operational efficiencies and long-term resilience under varied environmental conditions. Public-private partnerships and regulatory frameworks encouraging green building practices further embed performance-oriented specifications in commercial developments. Self-cleaning glass meets these criteria by reducing manual cleaning frequency, preserving visual appeal and supporting energy efficiency goals in high-rise and commercial settings.

Category-wise Analysis

Coating Type Insights

Hydrophilic coating is anticipated to secure around 60% of the self-cleaning glass market share in 2026, reflecting established commercial acceptance and proven functional reliability across architectural applications. The segment benefits from widespread adoption in building façades and windows, where rainwater-assisted cleaning provides consistent performance under diverse environmental conditions. Market participants value this technology for its dependable dirt dispersion mechanism that enables uniform water sheeting and efficient removal of contaminants. Specification rates remain high in commercial and institutional projects that prioritize façade appearance and long-term performance. Compatibility with existing glazing configurations supports seamless incorporation into new construction and renovation activities.

Clinical acceptance analogs apply through demonstrated effectiveness and repeat specification across commercial projects. Provider preference strengthens as hydrophilic coatings reduce streaking and residue formation, maintaining optical clarity over extended periods. Performance consistency across climatic zones supports repeat deployment in high-rise and large-surface installations. Broad supplier participation enhances procurement flexibility and supports competitive pricing structures, reinforcing adoption at scale. Standardised manufacturing and application processes improve quality assurance and installation efficiency. Ongoing advancements in coating chemistry improve abrasion tolerance and ultraviolet stability, extending service life.

Application Insights

Facades are likely to be the leading segment with a projected 45% of the self-cleaning glass market revenue share in 2026 due to extensive surface area deployment and high maintenance exposure. Large commercial buildings, institutional complexes, and mixed-use developments rely heavily on façade performance to maintain aesthetic consistency and asset value. Continuous exposure to dust, pollution, and weathering elevates cleaning frequency, operational disruption, and labor risk. Clinical credibility equivalents apply through validated long-term performance across landmark projects, where sustained transparency and surface integrity have been demonstrated over multiple years. Provider referrals within architectural and engineering communities reinforce specification momentum, supported by accumulated project references and technical validation.

Solar panels are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by technology-enabled service delivery models and efficiency optimization. Power generation output remains directly linked to surface cleanliness, positioning advanced coatings as a performance-enhancing input rather than a maintenance accessory. Digitalization of energy asset management highlights cleanliness-performance correlations, accelerating adoption among utility operators and commercial energy producers. Real-time monitoring platforms increasingly quantify output losses from soiling, strengthening investment justification. Accessibility improves through integration at manufacturing stage, lowering retrofit complexity and cost for large solar installations. Standardized application during panel production supports scalability across utility-scale and distributed energy systems.

Regional Insights

North America Self-Cleaning Glass Market Trends

North America maintains a strong position in the market for self-cleaning glass, supported by high-value commercial construction activity and a pronounced focus on operational efficiency across large building assets. Elevated labor costs and strict safety compliance standards materially increase the expense of manual façade and glazing maintenance, strengthening the economic case for low-intervention surface technologies. Asset owners and facility managers prioritize predictable maintenance budgets and reduced liability exposure, driving preference toward solutions that limit access-related risks in high-rise and complex structures. Diverse climatic exposure, ranging from arid urban zones to regions with heavy precipitation and pollution, further amplifies demand for glazing systems capable of sustaining optical clarity and surface performance under varied environmental stress. These conditions embed advanced glass solutions into long-term asset planning rather than short-term aesthetic upgrades.

Adoption momentum is reinforced through alignment with sustainability objectives, retrofit-driven investment, and technology validation across institutional projects. Building performance frameworks emphasize water conservation, durability, and lifecycle efficiency, positioning self-cleaning surfaces as contributors to compliance targets. Extensive retrofit activity across aging commercial and public infrastructure creates repeat demand, as modernization strategies seek performance enhancement without structural disruption. Collaboration between coating developers, architectural practices, and construction technology providers accelerates specification confidence through demonstrated in-field results. Integration with digital building management systems supports performance monitoring and outcome verification, strengthening trust among decision-makers.

Europe Self-Cleaning Glass Market Trends

By 2026, Europe is expected to lead with an estimated 36% of the self-cleaning glass share, owing to stringent building codes and enforceable performance standards across commercial and public infrastructure. Regulatory frameworks mandate energy efficiency, façade durability, and reduced maintenance intensity, creating structural demand for advanced glazing solutions that deliver measurable operational benefits. High concentration of dense urban developments and vertical construction increases exposure to pollution and weathering, intensifying lifecycle maintenance costs for conventional glass. Self-cleaning variants align with procurement priorities focused on long-term asset performance, safety risk reduction, and predictable operating expenditure. Widespread adoption of green building certification systems further embeds such materials into project specifications, as developers pursue compliance-driven performance metrics rather than aesthetic differentiation alone. These conditions elevate self-cleaning glass from a premium option to a functional requirement within large-scale architectural applications.

Market leadership is reinforced through manufacturing sophistication, early technology validation, and integration within established construction ecosystems. Coating technologies benefit from rigorous field testing across transport hubs, commercial landmarks, and institutional buildings, strengthening confidence among architects, façade engineers, and asset managers. Innovation investment prioritizes coating durability, ultraviolet stability, and compatibility with complex glazing assemblies, supporting repeat specification across projects with extended design lives. Supply chain proximity between glass processors, coating specialists, and construction firms enables efficient customization and consistent quality delivery. Retrofit activity driven by building modernization programs and sustainability targets sustains demand beyond new construction cycles.

Asia Pacific Self-Cleaning Glass Market Trends

Asia Pacific is forecasted to be the fastest-growing market for self-cleaning glass between 2026 and 2033, stimulated by rapid urbanization and accelerated infrastructure capitalization across high-density economies. Large-scale commercial developments, transport corridors, industrial parks, and institutional buildings expand façade surface intensity, increasing exposure-related maintenance costs. Project owners prioritize materials that stabilize operating expenditure and reduce dependence on manual cleaning in challenging environments marked by dust load, humidity variation, and air pollution. Capital allocation frameworks increasingly emphasize asset durability and service continuity, positioning advanced glazing as a performance input rather than a design enhancement. High-rise construction concentration and mixed-use megaprojects amplify the economic relevance of maintenance-reducing technologies, driving specification momentum at early design stages.

Growth acceleration is further reinforced through localized manufacturing scale, supply chain optimization, and integration at production stage. Regional glass processors expand coated glass capacity, enabling competitive pricing and shortening lead times for large commercial orders. Integration of self-cleaning functionality during fabrication reduces retrofit dependency, improving adoption feasibility across cost-sensitive developments. Public investment programs linked to industrial modernization, clean energy deployment, and smart infrastructure indirectly stimulate demand by prioritizing lifecycle efficiency and operational reliability. Solar installations present a parallel catalyst as surface cleanliness directly influences energy output metrics, strengthening value justification for performance coatings.

Competitive Landscape

The global self-cleaning glass market structure reflects moderate fragmentation with several global leaders and a broad base of regional manufacturers. Leading players collectively account for a significant portion of revenue through technological differentiation and project-based contracts. Market structure favors organizations with advanced coating capabilities, strong architectural relationships, and capacity to deliver consistent performance at scale. Competitive advantage increasingly depends on proven durability under real-world exposure, long service life, and reliability across varied climatic conditions. Large commercial and infrastructure projects prioritize suppliers with demonstrated execution capability, technical certification, and integration with complex façade systems.

Competitive positioning emphasizes coating durability, performance reliability, and compliance with sustainability standards. Saint-Gobain Glass (United Kingdom) Limited leverages deep material science expertise and integration with advanced building envelope solutions, strengthening specification across premium commercial developments. AGC Asia Pacific Pte Ltd benefits from scale manufacturing, coating innovation, and alignment with high-growth construction and solar applications. Nippon Sheet Glass Co., Ltd maintains competitiveness through precision coating technologies, quality assurance, and strong relationships with architectural and industrial customers. Guardian Industries Holdings Site. focuses on performance-driven glazing solutions supported by global supply reach and technical support capabilities. Across these players, investment priorities center on extending coating lifespan, enhancing ultraviolet resistance, and reducing maintenance dependency.

Key Industry Developments

- In February 2026, iecam completed a new coated glass production line at its Bulgaria facility, enhancing its capacity to manufacture high-performance architectural and automotive glass. The investment strengthens iecam’s regional footprint and supports expanded market supply for energy-efficient and specialty glass solutions.

- In August 2025, researchers at Zhejiang University developed a novel self-cleaning glass that uses embedded electric fields to remove up to 98% of dust and other particles in seconds without water or chemicals, offering a rapid and sustainable surface-maintenance solution for buildings, solar panels, and other glass applications.

- In June 2025, Pilkington United Kingdom Limited launched a new glass production line at its Greengate Works site in St Helens to secure rolled texture glass manufacturing, cutting about 15,000 tons of COe annually through consolidation of operations and supporting broader industrial decarbonization efforts.

Companies Covered in Self-Cleaning Glass Market

- Saint-Gobain Glass (United Kingdom) Limited

- AGC Asia Pacific Pte Ltd

- Nippon Sheet Glass Co., Ltd

- Guardian Industries Holdings Site.

- Xinyi Glass Holdings Limited.

- Central Glass Ltd.

- CARDINAL GLASS INDUSTRIES, INC

- TAIWAN GLASS INS. CORP.

- Asahi India Glass Limited.

Frequently Asked Questions

The global self-cleaning glass market is projected to reach US$ 129.8 billion in 2026.

Demand is driven by rising emphasis on low-maintenance building materials, increasing high-rise construction, higher labor and safety costs for manual cleaning, and stronger sustainability and efficiency requirements.

The market is poised to witness a CAGR of 4.5% from 2026 to 2033.

Expanding urban high-rise construction, growing solar installations requiring maintenance efficiency, stricter sustainability standards, and rising adoption of low-maintenance glazing across commercial and public infrastructure represent key market opportunities.

Some of the key market players include Saint-Gobain Glass (United Kingdom) Limited, AGC Asia Pacific Pte Ltd, Nippon Sheet Glass Co., Ltd, and Guardian Industries Holdings Site.