- Advanced Materials

- Self-Healing Polymer Market

Self-Healing Polymer Market Size, Share, and Growth Forecast, 2026 - 2033

Self-Healing Polymer Market By Product Type (Polyurethane (PU), Epoxy, Polylactide (PLA), Others), End-user (Automotive, Construction & Infrastructure, Aerospace & Defence, Electronics & Electrical, Medical / Healthcare, Textiles & Consumer Products) and Regional Analysis from 2026 to 2033

Self-Healing Polymer Market Size and Trends Analysis

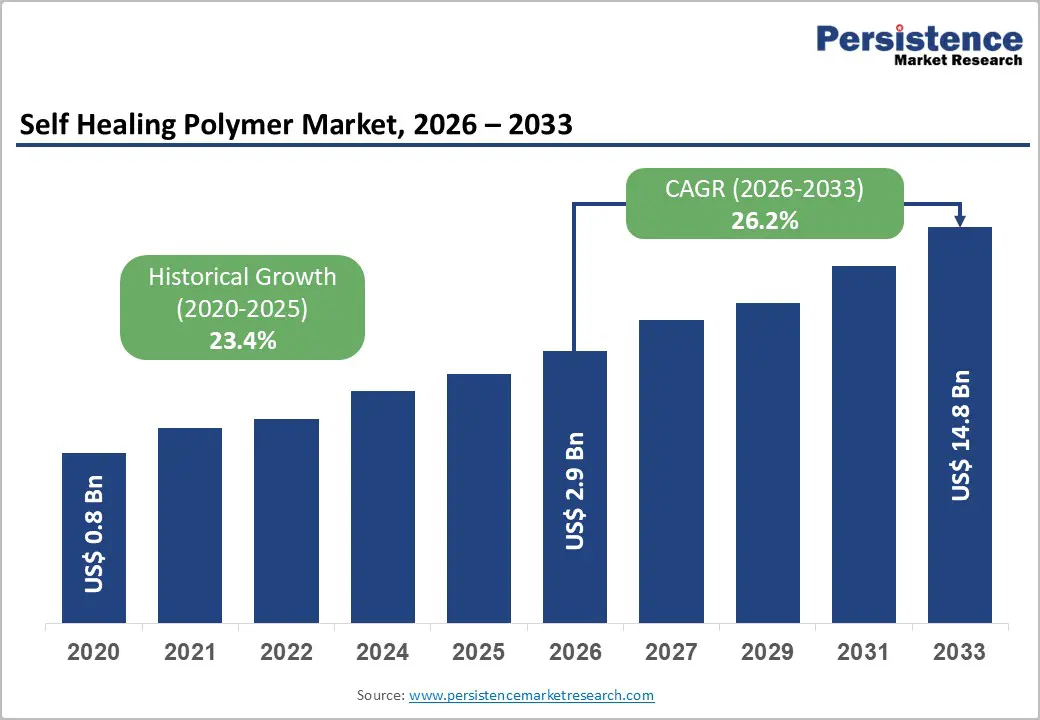

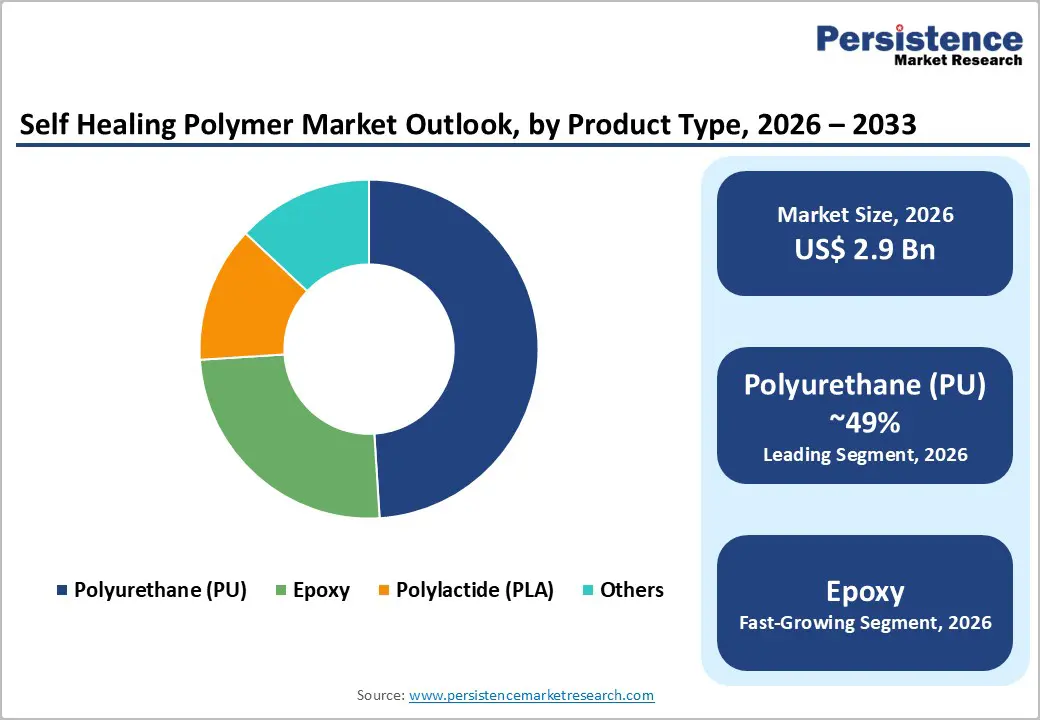

The global self-healing polymer market size is likely to be valued at US$ 2.9 billion in 2026 and is projected to reach US$ 14.8 billion by 2033, growing at a CAGR of 26.2% between 2026 and 2033.

The primary growth is anchored in the accelerating integration of self-healing polymer systems across automotive surface engineering, aerospace structural composites, electronics and EV battery platforms, and sustainable construction materials, where autonomous repair capability translates directly into quantifiable lifecycle and maintenance cost advantages. Landmark scientific breakthroughs in autonomous crack repair mechanisms without external stimuli, combined with intensifying regulatory mandates for durable and eco-efficient materials, are structurally reinforcing technology adoption.

Key Industry Highlights:

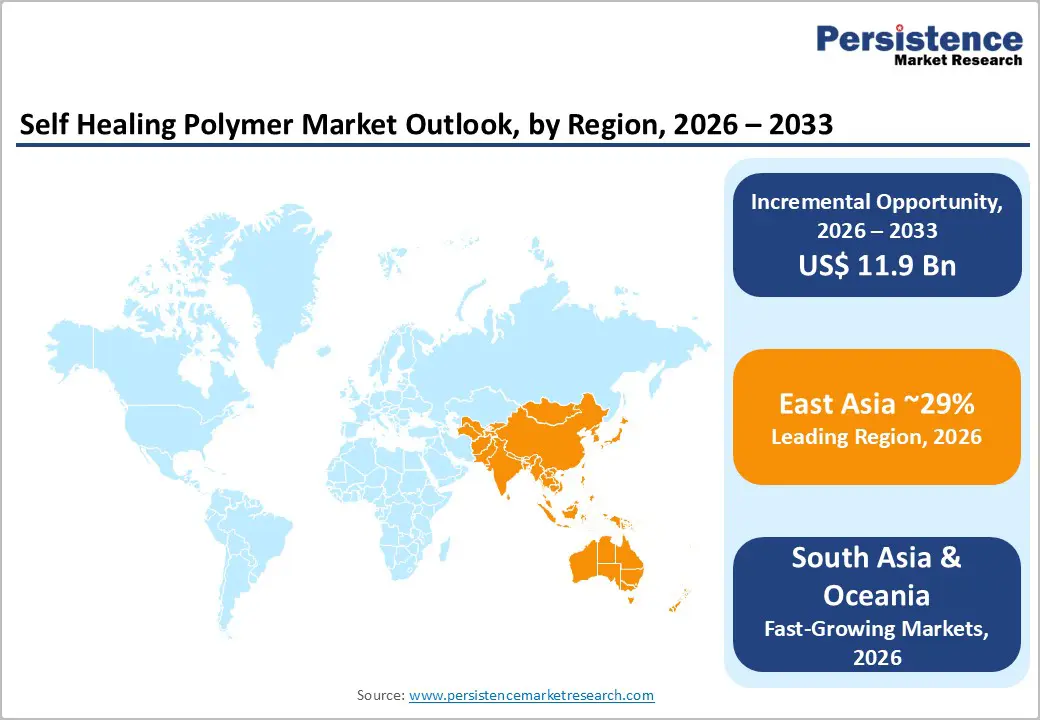

- East Asia Market Leadership: East Asia dominates the Self-Healing Polymer Market with approximately 29% share, driven by strong automotive manufacturing, electronics production, and rapid adoption of advanced material technologies in China, Japan, and South Korea.

- North America Innovation-Led Growth: North America accounts for around 24% of the market, supported by a robust aerospace & defence sector, expanding EV battery ecosystem, and early commercialisation of self-healing materials.

- Europe Sustainability-Driven Demand: Europe holds nearly 23% share, anchored by stringent environmental regulations, strong aerospace R&D, and increasing demand for durable and sustainable construction materials.

- Polyurethane Leading Product Segment: Polyurethane dominates with approximately 49% share, driven by its superior mechanical properties, versatility, and widespread use in coatings, automotive, and electronics applications.

- Automotive Leading Application Segment: Automotive leads with around 32% share, fueled by demand for scratch-resistant coatings, reduced maintenance costs, and growing EV adoption.

- Epoxy Fastest-Growing Segment: Epoxy-based self-healing polymers are the fastest-growing segment due to their high strength, chemical resistance, and suitability for construction and aerospace applications.

| Key Insights | Details |

|---|---|

| Market Self-Healing Polymer Size (2026E) | US$ 2.9 Bn |

| Market Value Forecast (2033F) | US$ 14.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 26.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 23.4% |

DRO Analysis

Drivers - Automotive Sector Demand for Durable, Low-Maintenance Surface Engineering Solutions

The automotive industry's focus on reducing total ownership costs, warranty liabilities, and surface maintenance expenditures has positioned self-healing polymer coatings as a technically and commercially strategic solution. OEMs and Tier-1 coating suppliers are deploying polyurethane-based self-healing systems that leverage intrinsic reflow mechanisms to autonomously repair superficial scratches without external intervention, preserving vehicle aesthetics and reducing post-sale service costs. These attributes are particularly critical in premium and electric vehicle platforms, where surface longevity is directly tied to resale value and consumer satisfaction. Within the Self-Healing Polymer Market, automotive applications represent the most commercially mature adoption channel

BASF's portfolio of advanced polyurethane composites and recycled-content materials, showcased at PU TECH 2025 for automotive applications, emphasised material durability and eco-efficient production processes, confirming tier-1 chemical suppliers' alignment with automotive procurement priorities. The Korea Research Institute of Chemical Technology developed a coating for car surfaces that scratches self-heals within 30 minutes using heat radiation from sunlight, reflecting the sustained pipeline of commercial-ready self-healing surface technologies advancing toward broader OEM integration.

Aerospace and Defence Industrial Expansion Accelerating Advanced Material Procurement

The aerospace and defence sector's structural reliance on materials that maintain integrity under extreme mechanical and environmental stress creates an inherently strong demand pathway for self-healing polymer composites and coatings. Self-healing polymer systems that autonomously repair abrasion damage, microcrack propagation, and surface degradation reduce maintenance intervals and enhance structural airworthiness, delivering both operational and economic value in aviation and defence platforms. The Self-Healing Polymer Market directly benefits from this sector's accelerating procurement of investment in advanced material systems

The European aerospace and defence industry delivered a total turnover of €325.7 billion, reflecting a 10.1% year-on-year increase, with R&D investment reaching €25.2 billion, a 9.4% annual increase, of which 61% was directed toward military technology initiatives. The defence segment alone achieved a turnover of €183.4 billion, a 13.8 % year-on-year increase across aeronautics, naval, and land systems, while the U.S. aerospace and defence industry generated nearly $995 billion in total business activity and recorded exports of $138.6 billion. India's defence production reached its highest-ever level at INR1.54 lakh crore in FY 2024 to 25, with exports surging to INR23,622 crore exported to over 100 countries, collectively amplifying global procurement demand for advanced polymer materials across military and civil aerospace programs.

Electronics Sector Modernisation and EV Battery Technology Integration: Opening New Application Channels

The structural transformation of the global electronics industry, particularly the rapid commercialisation of EV battery systems and flexible electronics, has established self-healing polymers as a technically critical material class for next-generation energy storage and component protection. Self-healing polymer binders and sealants address the fundamental limitation of conventional passive binders, which cannot restore electrode cohesion after crack formation during battery cycling, thereby causing irreversible capacity loss. The Self-Healing Polymer Market is directly positioned to capture the value created by the EV battery materials transition as automakers and battery manufacturers prioritise longevity and safety.

BASF highlighted OPPANOL polyisobutylene-based binders and sealants exhibiting inherent self-healing properties that reduce physical damage and enhance durability in lithium-ion battery systems, underscoring how leading chemical manufacturers are actively commercialising self-healing polymer functionalities for EV applications. India's electronics manufacturing sector expanded from US$ 29 billion in FY2015 to US$ 101 billion in FY2023, contributing 3.4% of GDP, with electronics exports reaching US$ 29.12 billion in FY2024, a 23.6% year-on-year increase. Europe's semiconductor sector contributed approximately €51 billion, representing 9.3% of the global market, with the EU27 region posting 12.3% growth, reflecting the scale of electronics sector demand that underpins polymer material procurement.

Restraint - Elevated Production Costs and Raw Material Complexity are Constraining Broad Adoption

The synthesis of self-healing polymers requires sophisticated chemical processes, specialised feedstocks, and precision formulation controls that generate production costs substantially above conventional polymer alternatives. For cost-sensitive industries, particularly construction commodity segments and mass-market consumer products, the price premium associated with self-healing materials acts as a meaningful procurement barrier. These cost pressures are further intensified by soaring energy and feedstock prices driven by geopolitical tensions, as documented in Plastics Europe's annual reporting, which also identified that chemical recycling demand for recyclates already exceeds supply. Supply chain constraints in specialty chemical inputs compound input cost volatility, limiting the ability of producers to achieve cost-competitive scale across all target applications.

Low Recycling Infrastructure Maturity and Regulatory Compliance Complexity

The commercialisation trajectory of self-healing polymers is structurally constrained by the nascent state of advanced polymer recycling infrastructure and evolving regulatory frameworks governing end-of-life material management. Plastics Europe's reporting documented that non-fossil-based plastics accounted for only 12.4% of European plastics production against an EU 2030 target of 20% non-fossil carbon in plastics, while Europe's share of global plastics production declined from 23% to 15% between 2006 and 2021. U.S. plastics recycling rates remain below 6%.

The complex molecular architecture of self-healing polymer systems, incorporating reversible crosslinks, encapsulated healing agents, and proprietary dynamic chemistries, further complicates end-of-life recyclability, creating compliance risk in regulatory environments where full lifecycle accountability is mandated.

Opportunities - Medical and Healthcare Applications: Biomedical Device Innovation and Autonomous Repair Material Platforms

The medical and healthcare sector represents one of the highest-value and most structurally differentiated growth frontiers for the self-healing polymer market, driven by unmet clinical demand for materials that maintain structural integrity under continuous physiological loading without requiring external intervention. Self-healing polymers with biocompatible chemistries are uniquely positioned for implantable devices, surgical repair substrates, drug delivery matrices, and wearable health monitoring platforms, where material degradation under cyclic mechanical stress remains a persistent technical limitation in current solutions.

Researchers from IIT Indore and IIT Hyderabad reported a breakthrough in autonomous self-healing in organic crystals, where micron-sized cracks are repaired within milliseconds through a novel symmetry-breaking mechanism without heat or light stimulation. This fundamental scientific advance provides a critical design framework for next-generation biomedical self-healing polymers with enhanced structural resilience and fully autonomous repair capability. India's government-backed initiatives, including iDEX funding for defence technology innovation and collaboration frameworks between academic institutions and industry, exemplify the ecosystem investment that is accelerating advanced materials research directly applicable to the self-healing polymer market medical segment.

Construction Sector Sustainability Mandates and Infrastructure Investment Generating Durable Materials Demand

Large-scale government-backed infrastructure investment programs and regulatory sustainability mandates across major construction markets are creating directly addressable procurement opportunities for self-healing polymer coatings, sealants, and structural materials in the Self-Healing Polymer Market. The ability of self-healing polymer systems to autonomously repair microcracks in concrete, roofing systems, and façade coatings substantially reduces maintenance expenditure and extends asset service life, aligning with both economic and environmental sustainability objectives central to modern infrastructure procurement criteria.

India's government increased capital expenditure by 11.1% to $133 billion in FY2025, equivalent to 3.4% of GDP, with the real estate market projected to reach $5.8 trillion, contributing 15.5% of total GDP. The U.S. recorded total annual construction spending of $2.2 trillion, representing 4.5% of GDP, with 1.6 million new homes constructed. In the EU, Spain posted 11.2% annual construction output growth, and Czechia recorded 9.7% growth. BASF and Sika's joint launch of Baxxodur EC 151, an advanced epoxy hardener enabling high-performance, low-VOC flooring coatings with enhanced mechanical and chemical resistance for construction applications, marks a concrete commercial pathway for self-healing-enabled epoxy polymer systems in this segment.

Category-wise Analysis

Product Type Insights

Polyurethane commands a dominant 49% share of the global self-healing polymer market by product type, driven by its exceptional versatility across automotive coating, aerospace protective film, electronics encapsulant, and construction sealant applications. Its tunable mechanical properties, compatibility with established commercial coating processes, including Direct Coating, and superior resistance to abrasion, UV radiation, and environmental exposure make it the formulation backbone of commercial self-healing polymer adoption.

Covestro's introduction of advanced polyurethane coating systems under the Direct Coating process, incorporating self-healing surface variants that autonomously repair superficial scratches through a controlled reflow mechanism, established a pivotal commercial benchmark for polyurethane self-healing systems in automotive and electronics manufacturing. Japan's self-healing polymer market identifies polyurethane as the largest revenue-generating material type, with automotive OEMs and coating formulators across Asia actively deploying intrinsic dynamic polyurethane chemistries for scratch and microcrack repair, further validating the material category's sustained volume leadership across international markets.

Epoxy-based self-healing polymers represent the fastest-growing product type segment within the Global Self-Healing Polymer Market, underpinned by their superior mechanical strength, chemical resistance, and compatibility with high-performance structural applications in aerospace composites, industrial flooring, and construction coatings. The chemistry of epoxy systems enables effective encapsulation of healing agents and the formation of dynamic covalent networks that deliver robust self-repair performance in demanding environments where surface degradation and structural microcracking are recurring operational challenges.

Application Insights

The automotive end-use segment is likely to hold a 32% share in 2026, reflecting the sector's advanced and early-stage commercialization of self-healing polymer coatings for exterior surface protection, interior aesthetics, and EV battery component durability. Automotive OEMs' procurement requirements for surface systems that autonomously repair scratches and minor abrasions, reducing warranty claims and enhancing long-term aesthetic quality, have made this segment the primary commercial proving ground for self-healing polymer technologies.

The Korea Research Institute of Chemical Technology's development of a commercial-comparable self-healing car coating that repairs scratches within 30 minutes using solar heat radiation reflects the depth of automotive-focused self-healing polymer R&D investment across leading manufacturing economies. The commercial integration of OPPANOL-based self-healing binders and sealants in lithium-ion battery systems further broadens automotive self-healing polymer demand beyond exterior coatings into critical powertrain components, establishing a dual application growth vector that reinforces the segment's market leadership position.

The medical and healthcare segment is the fastest-growing end-use category within the Global Self-Healing Polymer Market, propelled by the convergence of biomedical device innovation, breakthroughs in autonomous material repair mechanisms, and accelerating investment in regenerative medicine, surgical materials, and wearable health monitoring platforms. Conventional biomedical polymers cannot restore structural integrity after cyclic physiological loading, creating a critical unmet technical need that self-healing polymer systems are uniquely equipped to address across implantables, drug delivery matrices, and artificial tissue substrates.

Regional Insights and Trends

East Asia Self-healing Polymer Market Trends

East Asia holds the largest regional share of 35% in the global market, with the region's dominance anchored in China's position as the world's foremost manufacturing hub for automotive, electronics, and industrial polymer applications, complemented by Japan's advanced automotive OEM ecosystem and South Korea's leadership in semiconductor and display manufacturing. China's self-healing polymer sector is supported by a deeply integrated domestic supply chain spanning petrochemical feedstocks, speciality chemical formulation, and high-volume end-use manufacturing, enabling cost-competitive scaling across automotive coating and electronics applications

China accounts for the largest national self-healing polymer market within Asia Pacific, while Japan's market has polyurethane as the largest material segment and polylactide PLA as the fastest-growing formulation. South Korea's investment in polymer research for automotive components, exemplified by the Korea Research Institute of Chemical Technology's development of solar-activated self-healing car coatings repairing scratches within 30 minutes, reflects the region's technology pipeline depth. Japan's electronics sector is pioneering self-healing phone screen coatings and flexible electronics applications, while Asia Pacific automotive OEMs and coating formulators are actively piloting intrinsic dynamic chemistries for scratch and microcrack repair.

North America Self-healing Polymer Market Trends

North America accounts for 24% of the global self-healing polymer market, with the United States functioning as the primary demand engine, supported by its world-leading aerospace and defence industrial base, advanced automotive manufacturing sector, and rapidly expanding EV battery technology ecosystem. The U.S. aerospace and defence industry generated nearly $995 billion in total business activity, combining $556 billion in direct output with $439 billion from the supply chain, contributing 1.5% of U.S. nominal GDP and supporting exports of $138.6 billion, with employment of over 2.2 million workers across direct and indirect roles.

The U.S. construction sector recorded total annual spending of $2.2 trillion, representing 4.5% of GDP, with 1.6 million new homes built and over 8.2 million industry employees, including 6.4 million in construction-specific occupations, creating a substantial procurement base for advanced coating and sealant materials. BASF's demonstration of OPPANOL-based self-healing binders and sealants for lithium-ion battery systems at the North American Battery Show reflected North America's dual role as both a primary commercial launch market and an innovation testbed for self-healing polymer integration in EV battery systems. The U.S. construction industry's embrace of modernisation, combined with federal infrastructure investment programs and EV adoption incentives, collectively amplifies the region's addressable demand in the Global Self-Healing Polymer Market.

Europe Self-healing Polymer Market Trends

Europe commands a 20% share of the global self-healing polymer market, driven by its leadership in aerospace and defense materials innovation, sustainable construction policy frameworks, automotive engineering expertise, and a speciality chemicals production base that includes several of the world's leading self-healing polymer producers. The European aerospace and defense industry delivered a total turnover of €325.7 billion with a 10.1% year-on-year increase, while defence R&D investment reached €25.2 billion, with the defence sector alone achieving a turnover of €183.4 billion across aeronautics, naval, and land systems, generating demand for advanced protective polymer materials in structural and surface applications.

The European construction sector reported monthly output growth of 0.4% in the EU, with Spain posting 11.2% annual construction output growth and Czechia recording 9.7% growth, reflecting active market demand for durable and sustainable construction materials, including self-healing polymer coatings. Plastics Europe's documentation of a 20% improvement in recycled plastics usage, reaching nearly 10% recycled content, combined with the EU's 2030 target of 20% non-fossil carbon in plastics production, establishes a strong regulatory tailwind for advanced polymer systems with inherently superior lifecycle performance.

Competitive Landscape

The global self-healing polymer market exhibits a moderately fragmented to semi-consolidated structure, characterised by the presence of both large multinational chemical companies and specialised innovators. Leading players such as BASF SE, Covestro AG, Arkema S.A., Huntsman Corporation, Dow Inc., and Autonomic Materials Inc. dominate the landscape through strong R&D and global reach. The market is highly innovation-driven, with competition focused on enhancing healing efficiency, durability, and multi-cycle performance across applications.

Large companies benefit from economies of scale and integrated value chains, while niche players contribute advanced technologies such as microencapsulation and intrinsic healing chemistry. Strategic collaborations, product innovations, and sustainability initiatives are further intensifying competition.

Key Developments

- In March 2025, BASF and Sika jointly launched Baxxodur® EC 151, an advanced epoxy hardener designed for durable, low-VOC, and high-performance flooring coatings in construction applications. While primarily focused on sustainability and enhanced durability, the development supports longer material lifecycles and reduced maintenance, aligning with the broader industry shift toward advanced polymer systems, including self-healing-enabled coatings.

- In October 2024, BASF highlighted its advanced battery material solutions at the North American Battery Show 2024, including OPPANOL® polyisobutylene-based binders and sealants exhibiting inherent self-healing properties that reduce physical damage and enhance durability in lithium-ion battery systems. This development underscores the growing integration of self-healing polymer functionalities in EV battery components to improve safety, performance, and lifecycle efficiency.

Companies Covered in Self-Healing Polymer Market

- Huntsman International LLC

- BASF SE

- Covestro AG

- Dow

- Sika AG

- Wanhua Chemical Group Co., Ltd.

- Arkema S.A.

- NEI Corporation

- The Lubrizol Corporation

- The Goodyear Tire & Rubber Company

Frequently Asked Questions

The global Self-Healing Polymer Market is projected to be valued at US$ 2.9 Bn in 2026.

The Polyurethane (PU) segment is expected to account for approximately 49% of the Global Self-Healing Polymer Market by Product Type in 2026.

The market is expected to witness a CAGR of 26.2% from 2026 to 2033.

Growth of the Self-Healing Polymer Market is driven by rising demand from automotive, aerospace & defence, and electronics sectors for durable, low-maintenance materials, along with increasing adoption in EV batteries and advanced coatings that enhance performance, longevity, and cost efficiency.

Key opportunities in the Self-Healing Polymer Market lie in expanding biomedical and healthcare applications for autonomous repair materials and growing construction sector demand for durable, self-repairing infrastructure solutions driven by sustainability mandates and large-scale investments.

Key players in the Self-Healing Polymer Market include BASF SE, Covestro AG, Arkema S.A., Huntsman Corporation, Dow Inc., and Autonomic Materials Inc.