- Renewable Energy

- Wind Turbine Rotor Blades Market

Wind Turbine Rotor Blades Market Size, Share, and Growth Forecast, 2025 - 2032

Wind Turbine Rotor Blades Market by Location (Onshore, Offshore), Blade Length (Less than 27 Meters, 27 Meters to 37 Meters, 38 Meters to 50 Meters, Greater than 50 Meters), Material (Carbon Fiber, Glass Fiber, Others), and Regional Analysis for 2025 - 2032

Wind Turbine Rotor Blades Market Share and Trends Analysis

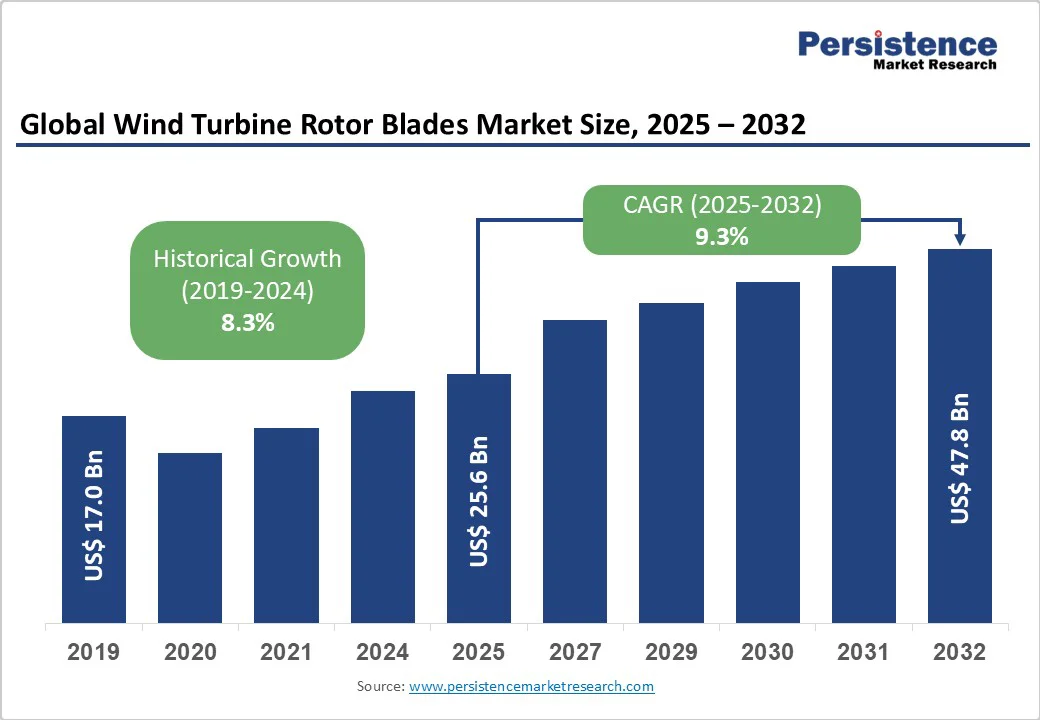

The global wind turbine rotor blades market size is likely to be valued at US$25.6 Billion in 2025 and is estimated to reach US$47.8 Billion by 2032, growing at a CAGR of 9.3% during the forecast period 2025 - 2032, driven by the expansion of renewable energy initiatives worldwide, increasing wind power installation capacities, and innovations in blade materials and design.

Key growth factors include government policies favoring clean energy, advancements in carbon and glass fiber composites reducing blade weight while enhancing strength, and the rising adoption of larger blades for enhanced efficiency.

Key Industry Highlights

- Fastest-growing Material: The carbon fiber segment is growing fastest, driven by increasing offshore installations requiring larger, lighter blades.

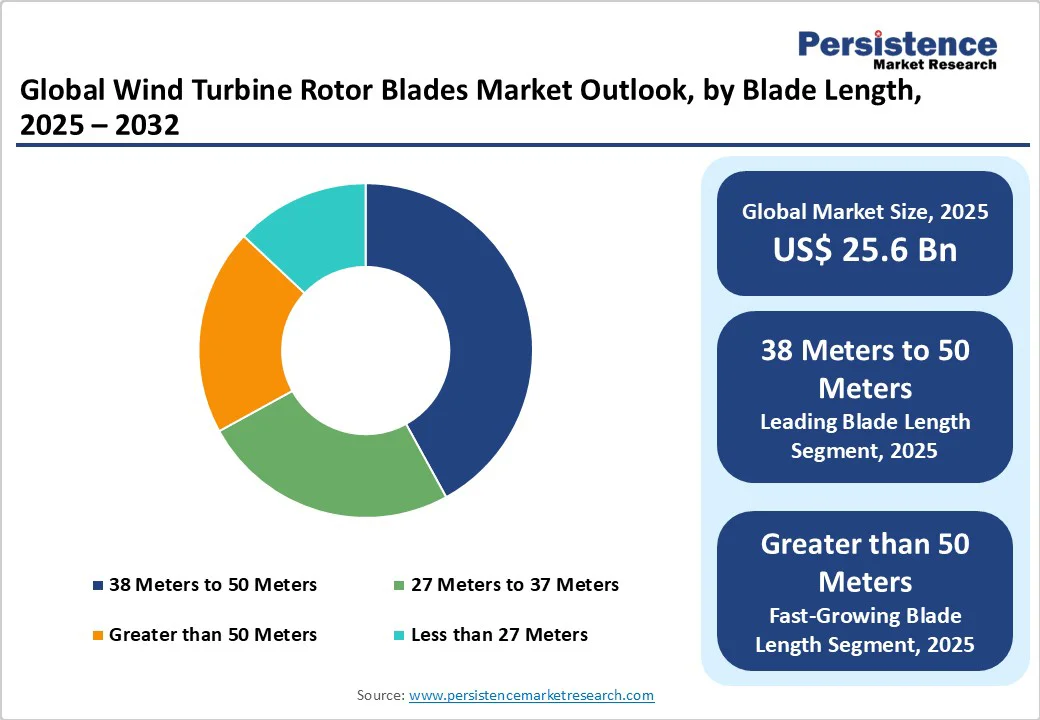

- Dominant & Fastest-growing Blade Length Segments: Blades in the 38-50-meter range dominate the market with over 40% share, while blades longer than 50 meters are the fastest growing.

- Leading & Fastest-growing Locations: Onshore applications hold 60% of the market share, with offshore growing rapidly, driven by government incentives and technological advancements.

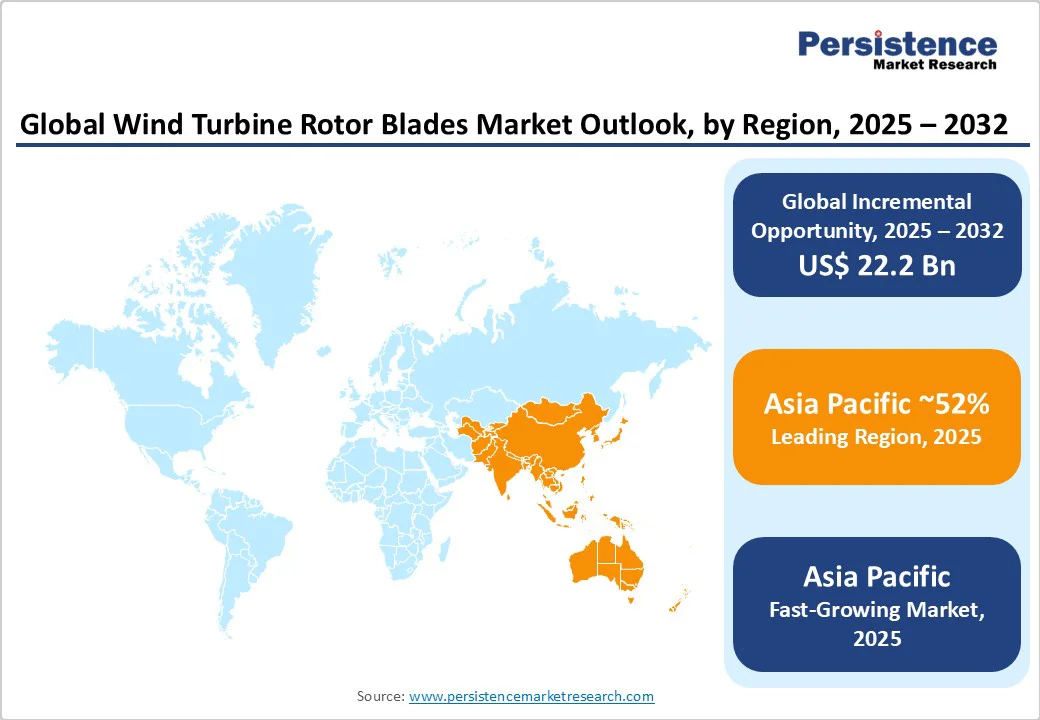

- Dominant & Fastest-growing Regions: Asia Pacific leads the global market with over 52% share by 2025 and a projected high CAGR through 2032, backed by China and India’s ambitious renewable capacity targets.

| Key Insights | Details |

|---|---|

| Wind Turbine Rotor Blades Market Size (2025E) | US$25.6 Bn |

| Market Value Forecast (2032F) | US$47.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 9.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Favorable Environmental Policies and Government Support

Governments worldwide are ramping up wind energy adoption to meet climate targets, cut emissions, and diversify energy sources. India’s investment of US$890 million in 1 GW offshore wind projects in Gujarat and Tamil Nadu highlights this transition, alongside Europe’s stringent carbon regulations and state-level mandates in the U.S. Such policies, offering subsidies, tax incentives, and regulatory clarity, are fueling rotor blade demand and attracting public-private investment. The IEA projects global wind capacity to double by 2030, supporting a forecast CAGR of 9.3% from 2025 to 2032.

On the technology front, innovations in carbon and glass fiber composites are driving performance gains. Carbon fiber’s high strength-to-weight ratio and fatigue resistance support longer blades for offshore turbines, enhancing energy capture.

Advances such as modular blade designs and improved aerodynamics are reducing manufacturing and transport costs. As economies of scale lower composite material costs, these innovations are making high-efficiency blades more accessible, helping reduce the levelized cost of energy (LCOE) and fueling global market expansion.

Expansion of Offshore Wind Projects

Offshore wind farms, characterized by stronger and more consistent wind speeds, are becoming focal points for renewable capacity additions. Market data indicates that the offshore segment revenue accounted for over 68% of the total rotor blade market in 2023. Offshore turbines require specially engineered, larger, and more durable rotor blades to withstand harsh marine conditions, presenting opportunities for higher-margin and technologically sophisticated products.

Government initiatives such as the European Investment Bank (EIB)’s US$650 Million loan to EnBW for North Sea projects underscore increasing financial commitments. Offshore wind capacity in Asia Pacific and Europe is forecasted to expand rapidly, leveraging floating turbine technologies and economies of scale, which will intensify demand for advanced rotor blades in the coming decade.

High Capital Investment and Operational Costs

Despite falling wind power generation costs, turbine and rotor blade manufacturing still demands high initial capital, largely due to expensive materials such as carbon fiber and the precision required in advanced blade designs. Offshore installations further inflate costs with complex logistics and maintenance in harsh environments.

Transportation and installation alone account for a significant portion of turbine CAPEX, often limiting feasibility in regions lacking infrastructure or financing. Additionally, the repair and upkeep of large blades raise OPEX, particularly impacting smaller developers and slowing market growth.

Structurally, the rotor blade market grapples with supply chain constraints. Sourcing specialized raw materials such as carbon fiber precursors and resins is challenging due to limited global production capacity and price volatility. The supplier base remains highly concentrated, exposing manufacturers to supply risks and delivery delays. Long lead times for blade production and shipping further hinder scalability. Addressing these issues requires supply chain diversification and strategic planning, potentially raising costs and complicating rapid market expansion.

Renewable Energy Expansion in Emerging Economies

Rapid industrialization and urbanization in key Asia Pacific economies, China, India, and ASEAN countries, are fueling rising energy demand and renewable capacity growth. Favorable government policies, increased investments, and expanding manufacturing capabilities position the region for significant market opportunities.

For example, India’s ambitious wind capacity targets and offshore wind projects represent multi-billion-dollar prospects by 2030. With ongoing electrification and decarbonization efforts, Asia Pacific is projected to hold the largest market share, surpassing 50% by 2030.

Repowering aging wind farms is emerging as a vital growth driver, as many turbines installed in the early 2000s near retrofit windows. Upgrading blades with advanced composite materials and longer designs boosts efficiency, reliability, and lifespan, creating substantial revenue potential, especially in Europe and North America.

Technological advancements, such as recyclable blade materials, smart sensors for predictive maintenance, and additive manufacturing of blade components, are enhancing performance and cutting lifecycle costs. Sustainable practices, including closed-loop recycling, are gaining traction, aligning with regulatory demands and attracting ESG-focused investors. These innovations are moving from pilot phases to mainstream adoption, steadily expanding their market impact and unlocking new investment and partnership opportunities.

Category-wise Analysis

Location Insights

Onshore wind turbine rotor blades are expected to capture approximately 60% of the market share in 2025, largely due to their lower capital and operational costs compared to offshore alternatives. The presence of well-established infrastructure for manufacturing, transport, and installation in key markets such as China, the U.S., Germany, and Spain reinforces the dominance of onshore wind.

Additionally, onshore projects offer easier accessibility for maintenance, which reduces lifecycle costs and minimizes operational downtime. Favorable regulatory environments in these regions, such as tax credits, streamlined permitting, and grid integration support, continue to encourage sustained investment in onshore installations, helping maintain their cost competitiveness despite growing interest in offshore development.

In contrast, the offshore wind segment is projected to grow at a robust CAGR from 2025 to 2032. This growth is fueled by strong policy support, falling technology costs, and the increasing adoption of high-capacity turbines designed for deeper waters and more consistent wind conditions.

Offshore projects, while more capital-intensive, contribute over 68% of market revenue due to their higher energy output and scalability. Significant investments in coastal infrastructure, especially across Europe and Asia Pacific, are accelerating offshore deployment, making it a key pillar in meeting global renewable energy and decarbonization goals.

Material Insights

Glass fiber composites are projected to remain the dominant material in the wind turbine rotor blade market, accounting for approximately 65% of revenue share in 2025. This dominance stems from their cost-efficiency and balanced mechanical properties, such as high tensile strength and flexibility, making them particularly suited for onshore blades ranging between 27 and 37 meters in length.

The widespread availability of raw materials, coupled with a well-established global supply chain and mature manufacturing processes, enhances the scalability of glass fiber composites. Their proven reliability under varied environmental conditions also supports sustained demand, particularly across Europe and Asia Pacific, where robust onshore wind infrastructure and manufacturing ecosystems exist. Continued deployment of mid-sized turbines in mature markets and blade replacements in aging wind farms further reinforce the segment’s resilience.

The carbon fiber segment is poised for rapid growth through 2032. As offshore wind projects scale up, the need for longer, lighter blades, often exceeding 50 meters, is driving adoption of carbon fiber, valued for its superior strength-to-weight ratio.

Advancements in manufacturing technologies and reductions in raw material costs are making carbon fiber more commercially viable. Additionally, rising demand for repowering existing turbines with high-performance blades is accelerating its global uptake.

Blade Length Insights

Blades measuring between 38 meters and 50 meters are likely to account for the largest market share in 2025, representing over 40% of rotor blade sales by volume. This segment strikes a practical balance between aerodynamic performance and logistical feasibility, offering optimized energy capture without prohibitive transportation or installation costs.

Most turbines within the 1.5 to 3 MW class employ blades of this length, making the segment highly relevant to onshore projects predominantly found in Europe and North America. Strong, well-established supply chains for these blade sizes ensure consistent availability and facilitate steady market growth. These blade sizes cater well to both new installations and blade replacement markets, underpinning their substantial share.

Blades exceeding 50 meters are forecast to be the fastest-growing segment through 2032, largely driven by the offshore wind sector and the development of turbines with power ratings exceeding 6 MW. The need to maximize energy yield and efficiency in challenging offshore environments compels the use of longer blades.

Innovations in blade design, including modular manufacturing and transport solutions, are enabling logistics improvements that support the deployment of these large blades globally. This segment is also benefiting from increased investment in offshore infrastructure supporting the assembly and installation of ultra-large rotor components, making it a critical growth driver for the industry’s future landscape.

Regional Insights

Asia Pacific Wind Turbine Rotor Blades Market Trends

Asia Pacific is slated to be the largest regional market, expected to hold around a 52% share in 2025, with a robust projected CAGR through 2032. China leads regional expansion, strongly supported by government policy frameworks fostering renewable energy capacity expansion and cost efficiencies in manufacturing. India and ASEAN countries contribute significantly, leveraging abundant wind resources and rising electrification demands.

The competitive advantage of Asia Pacific stems from its well-developed supply chains, low labor costs, and aggressive policy incentives, including large-scale auctions and viability gap funding mechanisms. Infrastructure advancements, coupled with expanding offshore wind tender programs, further support market acceleration. Collectively, these factors position Asia Pacific as the hub for both manufacturing scale and market demand growth in rotor blade technology.

Europe Wind Turbine Rotor Blades Market Trends

Europe is predicted to account for an estimated 25% of the rotor blade market globally in 2025, with Germany, the U.K., France, and Spain spearheading it, characterized by advanced wind power capacities and mature regulatory frameworks harmonized under the umbrella of the European Union (EU). The growth is propelled by aggressive offshore wind expansion underpinned by subsidies and ambitious carbon neutrality goals aiming for fulfillment between 2030 and 2050.

Europe’s skilled workforce and engineering prowess drive leadership in the manufacturing of high-capacity offshore turbines, bolstered by EU infrastructure investments and private sector participation in floating offshore blade projects. This robust ecosystem favors both technological development and strategic investments, enabling Europe to maintain a strong competitive position in the global wind blade market.

North America Wind Turbine Rotor Blades Market Trends

North America is expected to capture roughly 20% of the wind turbine rotor blades market share in 2025, with the United States as the dominant contributor. The market growth is anchored by state-level renewable portfolio standards, federal tax incentives, including the Inflation Reduction Act, and escalating investments in both onshore and offshore wind developments. The regulatory environment remains favorable, with continued emphasis on expanding clean energy capacity under initiatives led by the Biden administration.

The U.S. benefits from a vibrant innovation ecosystem encompassing blade design R&D and sustainable manufacturing processes, which, combined with strong industry partnerships, attract ongoing capital for production capacity expansion and recycling technology development. This dynamic environment positions North America as a competitive and innovation-driven wind blade manufacturing hub poised for sustained growth.

Competitive Landscape

The global wind turbine rotor blade market structure paints a moderately consolidated picture, with the top five players commanding approximately 58% of the market share in 2025. Leading firms such as Siemens AG, Vestas Wind Systems, Suzlon Energy, and Gamesa dominate through vertically integrated manufacturing operations, extensive R&D investment, and continuous technological innovation. While Tier-1 suppliers hold significant market influence, the sector also features a diverse range of regional and specialized manufacturers competing on factors such as cost efficiency, material innovation, and niche capabilities.

Competitive dynamics heavily emphasize innovation leadership, scale economies in global supply chains, and resilience through strategic alliances, joint ventures, and, in some cases backward integration, to secure raw materials and manufacturing inputs. This competitive structure offers both barriers and opportunities for newcomers, driven by high entry thresholds but also enabled by emerging technologies and regional market growth.

Key Industry Developments

- In September 2025, ORE Catapult and RWE launched a testing program revealing that wind turbine blades with ~20 years of use could last up to 50% longer. By simulating extreme ageing and evaluating various repair and maintenance strategies, the study highlighted effective ways to extend blade lifespan.

- In September 2025, Radia unveiled the WindRunner, a 108 m long cargo aircraft with an 80 m wingspan, built to airlift wind turbine blades up to ~100 m long, bypassing road and rail limits. Designed for direct delivery to wind farms via semi-prepared runways, it aims to ease turbine deployment. Potential uses extend to oversized cargo and military logistics, though challenges remain in engineering, regulation, and sustainability.

- In August 2025, RWE and Siemens Gamesa began installing 150 recyclable rotor blades at the 1.4 GW Sofia offshore wind farm off England’s northeast coast. Made with a special resin, the blades can be separated at end-of-life and repurposed into products such as helmets, suitcases, or auto parts. Over half are already in place, with the remainder to be installed in 2025 via the vessel *Wind Peak*. This marks the U.K.’s first large-scale use of fully recyclable blades, setting a new standard for sustainability in offshore wind.

Companies Covered in Wind Turbine Rotor Blades Market

- Siemens AG

- Vestas Wind Systems A/S

- Suzlon Energy Limited

- Gamesa Corporacion Tecnologica

- General Electric Company

- Acciona S.A.

- Enercon GmbH

- Nordex SE

- Powerblades GmbH

- SGL Rotec GmbH & Co. KG

- EnBW

- MHI Vestas Offshore Wind

- Hitachi Power Solutions

- Aeris Energy

- Sinoi GmbH

Frequently Asked Questions

The wind turbine rotor blades market is projected to reach US$25.6 Billion in 2025.

The expansion of renewable energy initiatives worldwide, increasing wind power installation capacities, and innovations in blade materials and design are driving the market.

The wind turbine rotor blades market is poised to witness a CAGR of 9.3% from 2025 to 2032.

Government policies favoring clean energy, advancements in carbon and glass fiber composites reducing blade weight while enhancing strength, and the rising adoption of larger blades for enhanced efficiency are key market opportunities.

Siemens AG, Vestas Wind Systems A/S, and Suzlon Energy Limited are some of the key players in the wind turbine rotor blades market.