- Industrial Machinery

- Bead Winding Machine Market

Bead Winding Machine Market Size, Share, and Growth Forecast, 2026 – 2033

Bead Winding Machine Market by Machine Type (Manual, Electric, Others), Configuration (Single Bead Machine, Multi Spindle Bead Machine, Automatic Bead Machine, CNC Bead Machine, High Speed Bead Machine), End-User (Passenger Cars, Commercial Vehicles, Off Road Vehicles (OTR), Industrial Machinery, Agriculture Machinery), and Regional Analysis for 2026-2033

Bead Winding Machine Market Share and Trends Analysis

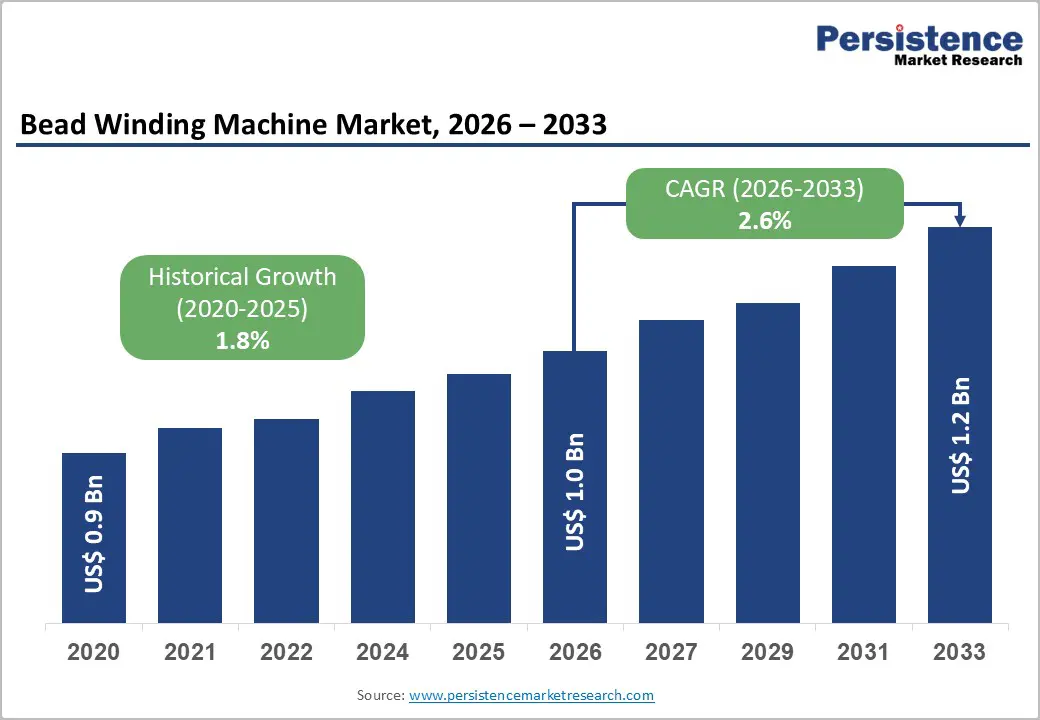

The global bead winding machine market size is likely to be valued at US$ 1.0 billion in 2026, and is projected to reach US$ 1.2 billion by 2033, growing at a CAGR of 2.6% during the forecast period 2026−2033. Growth is primarily driven by rising automotive production, increased demand for specialized tire construction, and integration of automated manufacturing technologies. Technological innovations in winding precision and enhanced material handling contribute to operational efficiency, improving adoption among tire manufacturers. Expansion of industrial infrastructure in emerging economies facilitates procurement and deployment of advanced machines. Regulatory support for quality assurance and safety standards enhances confidence in machine adoption, particularly among commercial tire producers. Demographic trends influencing vehicle ownership and transportation networks indirectly elevate demand for efficient tire assembly solutions.

Key Industry Highlights

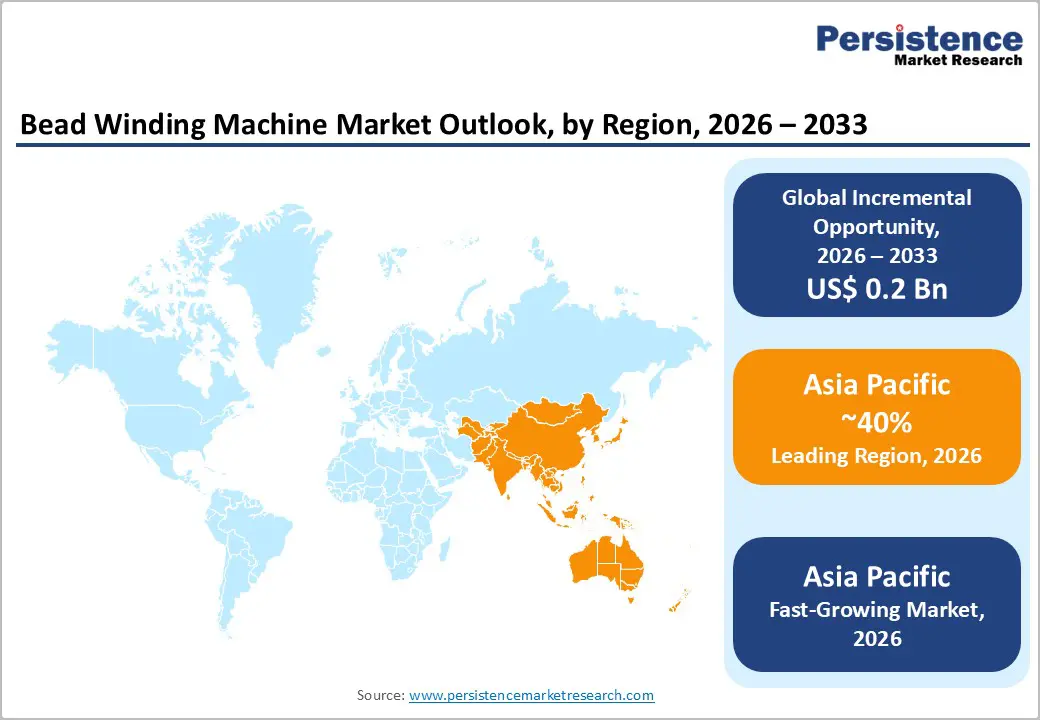

- Dominant Region: Asia Pacific is projected to dominate with around 40% market share in 2026, driven by tire manufacturing and vehicle production in China, India, Japan, and South Korea.

- Fastest-growing Market: Asia Pacific is expected to be the fastest-growing market between 2026 and 2033, stimulated by progressive industrial policy, capacity expansion, and automation in China.

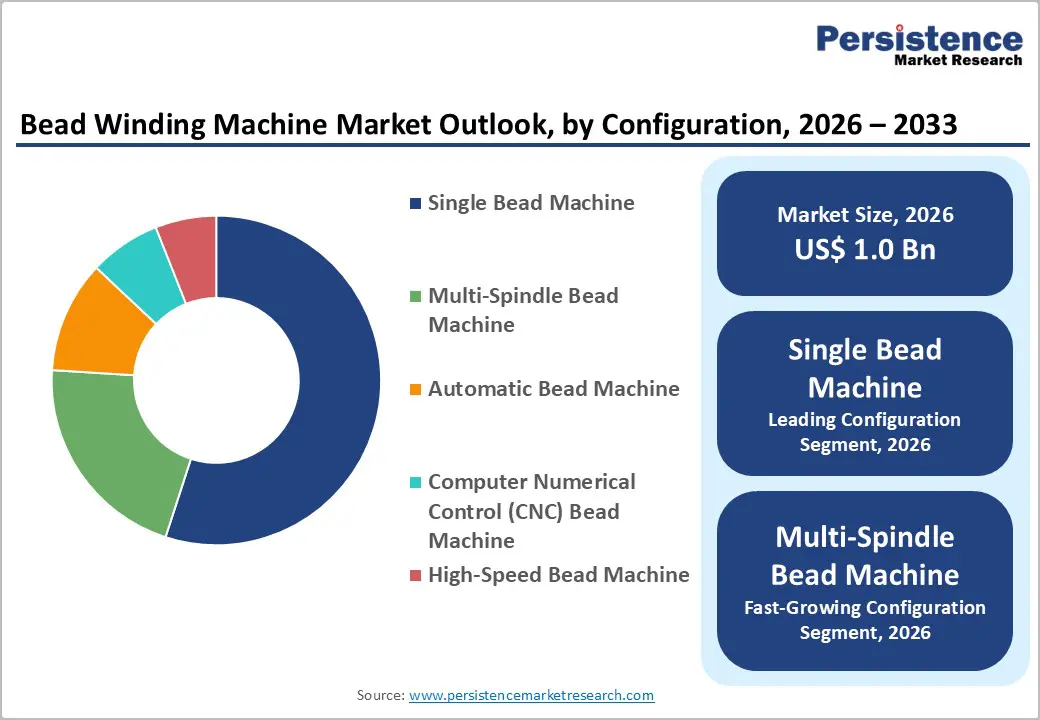

- Leading Configuration: Single bead machines are projected to lead the market with over 55% share in 2026, propelled by reliability and low-cost operations.

- Fastest-growing Configuration: Multi-spindle bead machines are projected to be the fastest-growing segment from 2026 to 2033, owing to their high throughput, automation, and versatility.

| Key Insights | Details |

|---|---|

|

Bead Winding Machine Market Size (2026E) |

US$ 1.0 Bn |

|

Market Value Forecast (2033F) |

US$ 1.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

2.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

1.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Surging Expansion of Automotive Production

Rising vehicle production translates into stronger demand for precision manufacturing technologies tied to reinforcement and quality processes since larger output drives the need for highly efficient, repeatable production systems. According to data from the Government of India, the total production of passenger vehicles, commercial vehicles, three wheelers, two wheelers and quadricycles reached 3,10,34,174 units in FY25, marking a substantial scale of manufacturing activity supported by policy and industry growth efforts. With such high volumes being produced, original equipment manufacturers (OEMs) prioritize equipment that supports consistent quality, reduced cycle times and stable throughput to meet both domestic and international delivery schedules while managing labor costs and production risks.

Industrial capacity expansion associated with surging vehicle output also influences supplier strategies as plants streamline capacity utilization and pursue technology upgrades to reduce bottlenecks in production workflows. Government manufacturing incentive programs aimed at increasing local production and exports create an environment where investment in advanced machinery delivers tangible returns through improved operational performance. As production targets rise and manufacturers scale operations, there is a direct correlation between output volumes and the adoption of sophisticated equipment designed to uphold quality standards, support higher speeds and maintain precision under increased load conditions.

Technological Advancement in Tire Manufacturing Equipment

Integration of advanced manufacturing technologies in tire production significantly improves operational efficiency and product quality. Automated systems and computer-controlled equipment enable precise alignment and uniform reinforcement in tire components, reducing defects and material waste. Real-time monitoring, predictive maintenance, and digital process controls allow manufacturers to maintain strict tolerances while scaling production. Robotics and AI-driven quality inspection further support consistent output across large production volumes, strengthening competitiveness in global markets. The ability to integrate sensors, data analytics, and smart controls also ensures timely identification of operational inefficiencies, lowering operational risk and increasing throughput.

Advanced equipment improves adaptability to evolving industry standards and regulatory requirements. Modular and programmable systems permit rapid adjustments in production parameters for different tire types, including passenger, commercial, and off-road applications. Enhanced precision in bead and reinforcement placement contributes to improved product performance and longevity. Process automation reduces labor dependency, accelerates cycle times, and enables cost-efficient scaling of operations. Investment in these technologies aligns with strategic initiatives for industrial modernization and digital transformation, offering measurable gains in reliability, efficiency, and production capacity without compromising safety or quality standards.

Limited Skilled Workforce Availability

Industrial operations are increasingly dependent on specialized skills such as computer numerical control (CNC) programming, precision assembly, and advanced machine maintenance, yet the supply of such talent remains constrained. Many potential workers enter the market without hands on training or formal credentials that match employer requirements, resulting in significant challenges for firms trying to hire capable technicians and operators.

A further structural issue stems from the mismatch between traditional education outputs and practical industrial needs. Government schemes and training institutions often struggle to align curricula with the rapid technological evolution in production environments, leaving a large pool of graduates underprepared for roles involving automation, robotics, or machine diagnostics. This dynamic suppresses operational efficiency and drives up recruitment costs, as employers invest extra resources in retraining. Employers also report high attrition in blue collar roles and difficulties retaining trained staff, which intensifies shortages of competent personnel on the shop floor.

High Capital Investment Requirements

Capital intensive automated equipment demands significant upfront expenditure for acquisition of advanced control systems, robotics, customized tooling, and integration into existing production lines. Such expenditures extend beyond purchase price to include site preparation, power infrastructure, workforce training, and long term maintenance, which elevate the total cost of ownership and restrict smaller firms from adopting cutting edge machinery. Large capital outlays can strain cash flow and limit resources available for other strategic initiatives, affecting the pace of technology adoption and operational expansion.

Investment requirements limit participation and slow uptake of automation when internal funds or affordable financing are unavailable. High thresholds create barriers to entry as firms must commit substantial capital before achieving efficiency gains or productivity improvements. Organizations in regions without access to low cost capital often defer automation, prioritizing operational stability and short term financial management. These dynamics reinforce slower modernization of production assets, reduce competitive agility, and restrict expansion potential in a market driven by precision and high-performance standards.

Opportunity Analysis- Integration with Industry 4.0 and Smart Manufacturing

Adoption of digitalized, connected production systems enables real time monitoring of operations and sensor led predictive insights that improve asset utilization and reduce unplanned downtime, driving productivity gains across manufacturing units. Firms deploying embedded digital sensors and data analytics capture machine-level performance data and transform it into actionable insights that reduce cycle times and quality defects, delivering consistent output quality with minimal manual intervention. This capability supports rapid adjustment of production parameters and optimization of workflows, which helps maintain throughput even under fluctuating demand scenarios, leading to measurable operational improvements.^

Government policy emphasis on digital transformation reinforces the economic case for smart technology adoption. A sector adoption benchmark shows more than two thirds of Indian manufacturers are embracing digital transformation by 2025, underscoring a broad shift towards connected factory systems that enable interoperability and advanced process control across equipment fleets. Programs such as national initiatives to enhance digital integration, skills development in IoT and automation, and technology upskilling frameworks support the availability of talent and infrastructure needed for modern manufacturing environments.

Sustainable Technology Integration

Integrating sustainable technologies into industrial equipment drives operational efficiency, regulatory compliance, and cost control in a manufacturing environment. Government policy frameworks in 2025 are supporting energy efficient upgrades and lower emission technologies, creating a context where upgrading machinery to meet energy performance standards aligns with broader industrial goals. For example, India’s renewable energy capacity reached a record 44.5 GW in 2025, with non-fossil sources providing more than 50 % of installed electricity capacity, reflecting policy momentum toward cleaner energy and lower carbon intensity across sectors including manufacturing. Investments in technology that reduces energy use and emissions help lower operating costs over the long term, enhance access to incentives and tax schemes, and reduce vulnerability to future regulatory constraints on carbon and energy use.

A second driver is market differentiation and supplier competitiveness. Buyers and global supply chains increasingly prioritize products manufactured with lower environmental impact, and governments are calibrating standards to reflect sustainability metrics such as energy efficiency and emissions intensity. Programs such as India’s Zero Defect Zero Effect initiative encourage quality manufacturing with minimal environmental impact across micro, small, and medium enterprises, making sustainable technology upgrades a condition for inclusion in export and procurement value chains.

Category-wise Analysis

Configuration Insights

Single bead machine extracts are poised to dominate with a forecasted market share of over 55% in 2026, powered by consistent performance in standard tire production lines. Simplified operation and integration with existing assembly workflows enhance adoption across mid-sized and large tire manufacturing facilities, reducing the need for extensive operator training. Consistent performance ensures minimal downtime and uniform product quality, which supports predictable supply chain planning. Regulatory compliance for safety and quality is easier to maintain, lowering the risk of production delays or penalties. Industrial procurement strategies favor single bead machines for predictable maintenance costs, energy efficiency, and long-term operational stability, making them a reliable choice for manufacturers prioritizing steady output and controlled overheads.

Multi-spindle bead machine is estimated to be the fastest-growing segment from 2026 to 2033, fueled by higher throughput capabilities and suitability for large-scale tire production. Automation compatibility allows seamless integration with advanced manufacturing lines, reducing manual labor dependency and enabling continuous production cycles. Reduced cycle times contribute to higher efficiency and lower per-unit production costs, making it attractive for factories handling high-volume tire orders. Flexibility for diverse tire specifications enhances operational versatility, allowing rapid switching between product lines.

End-User Insights

Passenger cars are likely to be the leading segment with a projected 50% of the bead winding machine market revenue share in 2026 due to high global demand for personal vehicles and corresponding tire production. Standardized production requirements facilitate efficient machine utilization, allowing manufacturers to maintain consistent output with minimal downtime. Precision in bead winding ensures uniform tire performance, supporting quality assurance and compliance with safety standards. Regulatory emphasis on quality and safety encourages adoption of precise equipment, reducing risk of defects or recalls. OEM partnerships provide predictable procurement cycles, technical support, and service infrastructure, ensuring smooth integration into existing production lines and long-term operational efficiency.

Commercial vehicles are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by expanding logistics and transportation sectors. Growing fleet sizes and specialized tire designs for heavy-duty and long-haul applications increase the need for advanced bead winding machinery. Automation adoption supports reduced labor requirements and consistent output quality, lowering operational costs and improving reliability. Industrial trends toward regional and long-distance transportation expansion drive sustained investment in production equipment.

Regional Insights

North America Bead Winding Machine Market Trends

In North America, the demand for advanced bead winding machinery is robust, owing to established automotive and tire manufacturing hubs in the United States, Canada, and Mexico. High vehicle production volumes and rising adoption of electric and premium vehicles require precision equipment capable of meeting stringent quality and performance standards. Integration of automated and digitally controlled bead winding lines enhances throughput while reducing labor dependency and operational errors. Industrial strategies prioritize energy-efficient operations and predictive maintenance systems, allowing manufacturers to optimize uptime and production cycles. Established aftermarket and replacement tire markets create steady demand for consistent output, prompting manufacturers to invest in high-speed, flexible machinery that accommodates diverse tire specifications.

Sustained growth is supported by cross-border industrial activity and nearshoring trends, which enable seamless supply chain integration and faster response to fluctuating demand in commercial and specialty tire production. Mexico’s tire manufacturing for commercial vehicles, combined with Canada’s component production capabilities, strengthens manufacturing throughput and supports capital-intensive upgrades. Regulatory standards emphasizing energy efficiency, safety, and emission reductions drive adoption of automated, high-precision bead winding machinery. Investment in workforce training and technical upskilling ensures efficient operation of advanced systems, enhancing productivity and reducing operational risks.

Europe Bead Winding Machine Market Trends

Europe is projected to hold a significant position in the bead winding machine market due to established automotive and tire manufacturing industries concentrated in countries such as Germany, Italy, France, and Spain. High vehicle production standards and stringent safety regulations drive demand for precision bead winding equipment that ensures consistent tire quality and compliance with international norms. Advanced manufacturing ecosystems, including robust supply chains and extensive technical expertise, support adoption of automated and CNC-based bead winding systems. Major automotive clusters in Germany, particularly around Stuttgart and Munich, integrate state-of-the-art tire production technologies into assembly lines, enabling high-volume output with minimal variability.

Automation integration and smart manufacturing initiatives allow rapid scaling of production capacity while maintaining quality standards, particularly for high-performance and electric vehicle (EV) tires. Government initiatives promoting industrial digitization, such as Germany’s Industrie 4.0 program, encourage adoption of connected bead winding systems with real-time monitoring and process optimization. Investments from global and regional players into retrofitting older plants with high-speed and multi-spindle machines improve throughput and energy efficiency. Rising demand for eco-friendly tires and adherence to EU emissions regulations further drive procurement of advanced equipment, supporting consistent growth in high-value manufacturing segments and reinforcing competitiveness in international tire markets.

Asia Pacific Bead Winding Machine Market Trends

Asia Pacific is expected to dominate with an estimated around 40% of the bead winding machine market share in 2026, reflecting the largest concentration of tire manufacturing and associated production technologies globally. Countries such as China, India, Japan, and South Korea lead vehicle and tire production, supported by integrated automotive value chains linking major assembly hubs, tier 1 manufacturers, and component fabricators within a contiguous industrial ecosystem. High production volumes of passenger and commercial vehicles in these countries directly stimulate demand for bead winding equipment calibrated for diverse tire specifications, amplifying economies of scale. Local supply networks, abundant material inputs, and competitive manufacturing costs further enhance operational throughput, enabling suppliers and OEMs to achieve lower unit costs relative to other regions.

Asia Pacific is forecasted to be the fastest-growing market for the bead winding machine market between 2026 and 2033, propelled by strategic industrial policies and capacity expansion initiatives that incentivize automation and advanced production technologies. Rapid urbanization and increasing vehicle ownership in countries such as China and India underpin long-term tire demand fundamentals, supporting reinvestment into manufacturing infrastructure prioritizing precision and throughput enhancements. Domestic and foreign capital investments target new tire plants and retrofitting existing facilities with high-speed and digitally integrated bead winding systems.

Competitive Landscape

The global bead winding machine market exhibits a moderately consolidated structure, with several key players maintaining a strong presence and influencing market dynamics. Leading companies such as Cimcorp, Bharaj Machineries Pvt Ltd, Strongman Group, Herbert Maschinenbau GmbH & Coo. KG, and Tianjin Saixiang Technology Co, Ltd hold substantial shares, collectively accounting for approximately 45% of the market. These players leverage advanced automation, precision engineering, and integration with digital manufacturing systems to meet the growing demand for high-quality tire production and industrial reinforcement applications. Smaller regional and specialized suppliers focus on niche segments, offering customized solutions, flexible configurations, and localized support, which creates opportunities for differentiation through technology, service, and process innovation.

Investment in research and development allows key players to introduce high-speed, multi-spindle, and CNC-enabled bead winding machines, enhancing productivity and operational efficiency for large-scale and specialty tire manufacturers. Market competition emphasizes the ability to provide end-to-end service support, including installation, maintenance, and operator training, which strengthens customer relationships and reduces operational risks. Technological innovation, including smart monitoring systems and energy-efficient designs, has become a central differentiator, allowing firms to optimize resource consumption and minimize downtime. Strategic collaborations with automotive OEMs and tire manufacturers further enhance positioning, enabling players to align machinery capabilities with evolving industry standards.

Key Industry Developments

- In October 2025, VIPO established VIPO India Private Limited in New Delhi to support tire manufacturing customers in India with local technical service, spare parts supply and digital assistance for bead winding and related machinery.

- In September 2025, machinery and equipment at Goodyear’s closed Fulda tire plant in Germany, including complete 17–22-inch passenger and SUV tire production lines and bead winding machines, were put up for sale through a private treaty and online auction following the facility’s shutdown amid declining demand and rising competition.

- In March 2025, VIPO unveiled the LIHEXAL 8, an octuple head bead winding innovation capable of producing eight beads per cycle to significantly boost efficiency and quality in tire manufacturing.

Companies Covered in Bead Winding Machine Market

- Cimcorp

- Bharaj Machineries Pvt Ltd

- Strongman Group

- Herbert Maschinenbau GmbH & Coo. KG

- Tianjin Saixiang Technology Co, Ltd

- Lorenz Pan AG

- MEC A/S

- Kobe Steel, Ltd

- VMI Group

Frequently Asked Questions

The global bead winding machine market is projected to reach US$ 1.0 billion in 2026.

Rising global automotive production and increasing adoption of automation and Industry 4.0 technologies in tire manufacturing primarily are driving the market.

The market is poised to witness a CAGR of 2.6% from 2026 to 2033.

Expansion of EV production and growth in high-performance tire demand are creating key opportunities in the market.

Some of the key market players include Cimcorp, Bharaj Machineries Pvt Ltd, Strongman Group, and Herbert Maschinenbau GmbH & Coo. KG.