- Home Appliances

- Hurricane Window Market

Hurricane Window Market Size, Share, and Growth Forecast, 2026-2033

Hurricane Window Market by Product Type (Single Hung, Sliding, Casement, Fixed, Custom), Frame Type (Aluminum, Vinyl, Wood, Fiberglass), End-User (Residential, Commercial, Institutional, Industrial), and Regional Analysis for 2026-2033

Hurricane Window Market Share and Trends Analysis

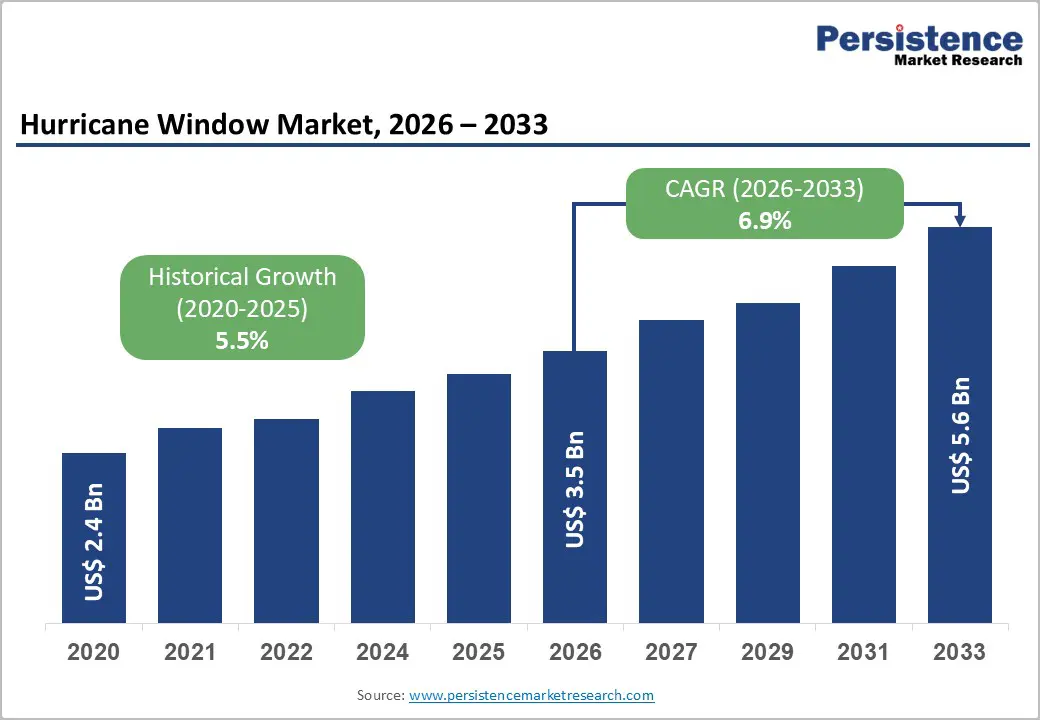

The global hurricane window market size is likely to be valued at US$ 3.5 billion in 2026, and is projected to reach US$ 5.6 billion by 2033, growing at a CAGR of 6.9% during the forecast period 2026 - 2033. The market is expanding steadily as governments enforce stricter coastal building codes and insurers integrate resilience metrics into underwriting models. Regulatory mandates in hurricane-prone regions require certified impact-resistant windows that meet wind-borne debris standards, directly increasing replacement and new construction demand.

Rising storm intensity and longer hurricane seasons are prompting homeowners, developers, and commercial property owners to prioritize structural fortification. Insurance carriers increasingly offer premium reductions for properties equipped with storm-resistant windows, strengthening the financial case for installation. Simultaneously, rapid residential construction in high-risk coastal corridors across North America and Asia-Pacific sustains consistent demand for compliant hurricane protection window systems.

Key Industry Highlights

- Dominant End-User: Residential applications are projected to account for approximately 62% of total revenue in 2026, while the commercial segment is expected to expand the fastest through 2033, supported by stricter compliance and asset protection mandates.

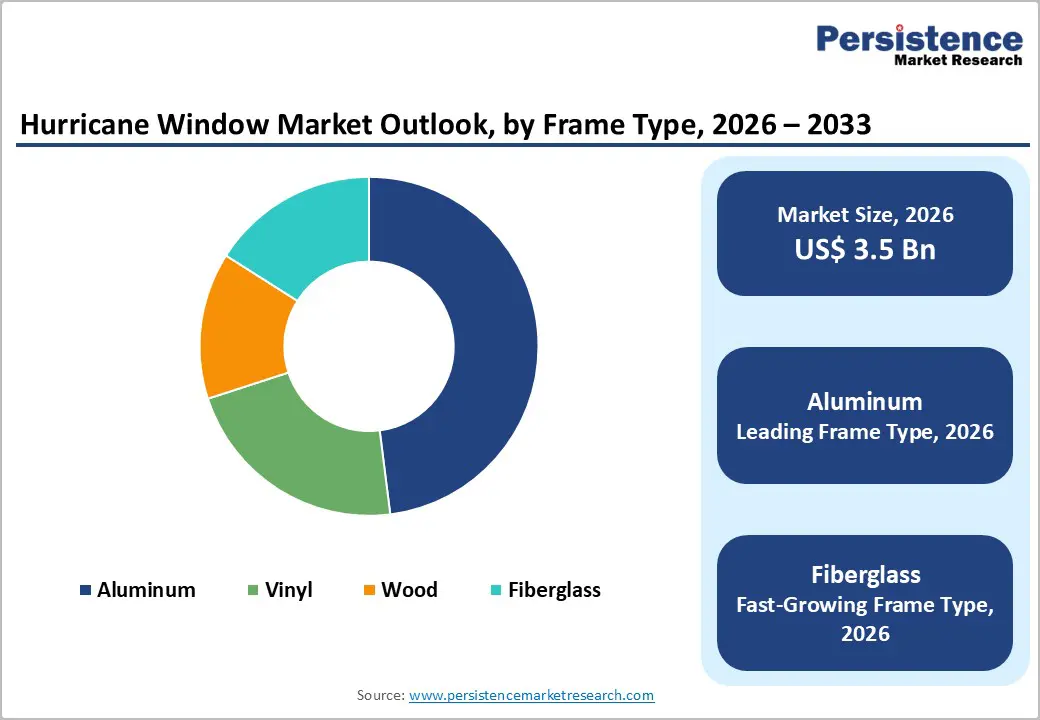

- Leading Frame Materials: Aluminum frames are anticipated to lead with about 48% share in 2026, while fiberglass frames are projected to register the strongest growth at nearly 8.1% CAGR during 2026–2033, supported by durability and thermal performance advantages.

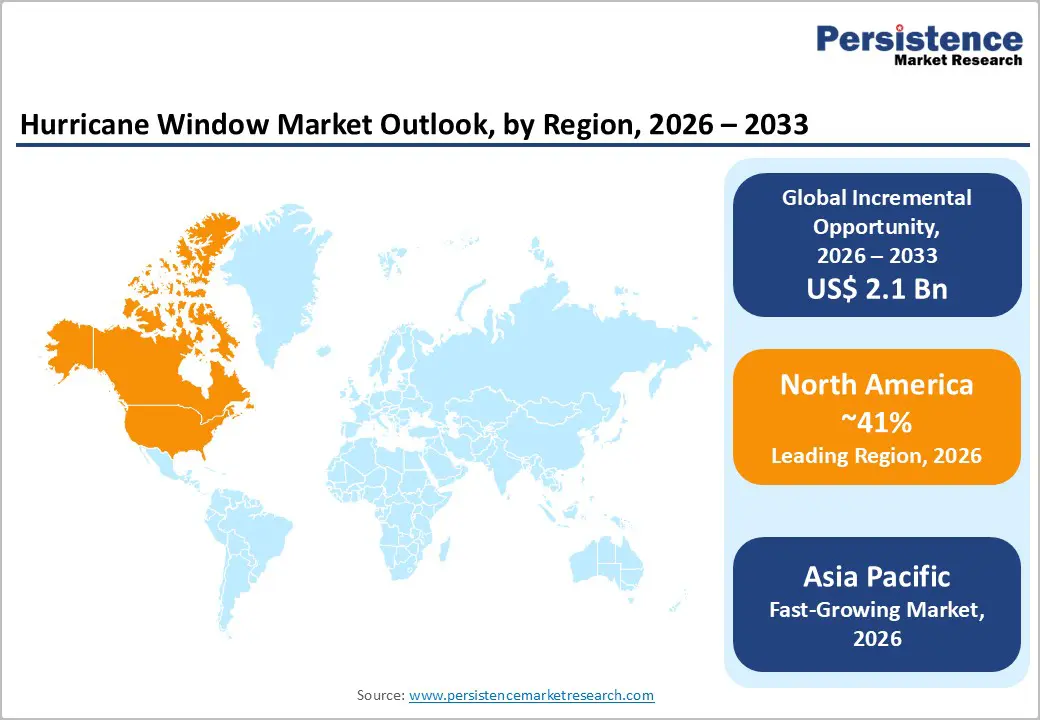

- Regional Leadership: North America is expected to hold close to 41% of the market share in 2026, while the Asia Pacific market is projected to expand the fastest at roughly 8.4% CAGR through 2033, fueled by disaster-resilient construction investments.

- Strategic Focus: Capacity expansions and launches of energy-efficient hurricane windows defined competitive activity, strengthening compliance positioning and product differentiation across residential and commercial segments.

| Key Insights | Details |

|---|---|

| Hurricane Window Market Size (2026E) | US$ 3.5 Bn |

| Market Value Forecast (2033F) | US$ 5.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Climate Risk and Insurance-Driven Resilience Investment

The frequency and severity of tropical cyclones and hurricanes have increased over the past two decades. According to the National Oceanic and Atmospheric Administration (NOAA), the U.S. recorded 28 separate billion-dollar weather disasters in 2023 alone. Rising insured losses have prompted carriers to tighten underwriting standards and link premiums to structural mitigation features. In 2025, Florida continued funding the My Safe Florida Home Program, allocating additional grants to support impact-rated window and door retrofits. Similarly, Louisiana maintained its Fortify Homes Program to incentivize resilient upgrades in hurricane-prone parishes. Insurers increasingly recognize certified hurricane impact windows as risk-reduction assets rather than discretionary improvements. These financial and climatic pressures are accelerating structural demand across high-exposure regions.

This directly supports the adoption of storm-resistant windows engineered to withstand high-velocity debris and extreme wind pressures. Homeowners in hurricane-prone states such as Florida and Texas are proactively upgrading glazing systems to secure premium discounts and protect long-term property value. Updated 2025 FORTIFIED Home standards strengthened requirements for opening protection, further institutionalizing impact-resistant solutions within resilience frameworks. As insurance underwriting models incorporate structural mitigation scoring, purchasing behavior is shifting from post-disaster replacement to preventive installation. Lenders and real estate stakeholders increasingly factor certified impact glazing into asset valuation metrics. These dynamics are structurally reinforcing the long-term trajectory of the hurricane protection windows market.

Regulatory Enforcement and Coastal Urbanization Expansion

Building code modernization continues to expand the addressable market for compliant glazing systems. The International Code Council (ICC) enforces the International Building Code (IBC) and International Residential Code (IRC), mandating impact-resistant glazing in designated wind-borne debris regions. Florida’s Building Code, among the strictest globally, requires certified impact-resistant glass windows for coastal properties. In 2025 and 2026, multiple state-level updates broadened enforcement scope and clarified compliance thresholds for opening protection systems. According to mitigation assessments by the U.S. Federal Emergency Management Agency (FEMA), buildings compliant with modern wind-resistant standards can experience up to 40% lower structural damage during major storms. Stronger enforcement mechanisms are reducing substitution risk from conventional glazing alternatives.

The United Nations Department of Economic and Social Affairs (UNDESA) reports that nearly 40% of the global population lives within 100 kilometers of a coastline. Rapid urbanization across the U.S., China, India, and Southeast Asia is expanding the structural base exposed to cyclone and hurricane risk. Coastal housing development and mixed-use infrastructure projects increasingly integrate certified energy-efficient hurricane windows at the design stage. Developers align resilience compliance with sustainability certifications to meet investor and municipal requirements. This convergence of regulatory enforcement and coastal population growth is embedding impact-resistant window systems as a foundational element of modern building practice.

High Upfront Installation Costs and Financing Barriers

Hurricane-resistant windows typically cost 2–3 times more than conventional glazing systems due to laminated glass, reinforced frames, and compliance testing requirements. For residential retrofit projects, total installed costs can exceed US$ 10,000 depending on property size and specifications. In coastal zones such as Miami-Dade and Broward Counties, stringent high-velocity wind design codes mandate engineered systems that further elevate base costs, making affordable alternatives less viable. Local contractors report that these code-driven requirements extend project planning and approval timelines, adding to soft costs. This cumulative cost structure slows adoption among budget-conscious homeowners and smaller developers.

While lifecycle savings through insurance discounts and reduced storm damage are recognized in industry discussions, upfront capital expenditure continues to constrain broader penetration. Financing mechanisms for resilience upgrades remain limited in many regions, with few low-interest retrofit programs available to offset high initial outlays. Federal and state incentives are inconsistent across markets, creating uneven demand even within hurricane-prone areas. Homeowners often prioritize immediate needs over structural upgrades, especially when costs compete with other essential investments. As a result, pricing sensitivity remains a persistent restraint on the hurricane window market’s expansion into mainstream segments.

Supply Chain Volatility in Aluminum and Glass Materials

The market relies heavily on aluminum frames and laminated glass components, exposing production costs to raw material volatility. Government data from the Associated General Contractors of America shows that producer prices for construction materials, especially aluminum mill shapes, rose sharply through early 2026, reflecting tariffs and supply constraints that inflated baseline input costs. Benchmark aluminum prices have recently reached multi-year highs, driven by structural supply tightness and elevated energy costs, which directly increase manufacturing expenses. These price dynamics compress margins for window producers and make customer pricing less predictable.

In parallel, global glass prices have experienced fluctuating production levels and supply interruptions, influencing delivery schedules for laminated and architectural glass suppliers. Extended lead times for high-performance glass and aluminum extrusion components are contributing to project delays and higher inventory carrying costs for manufacturers. Smaller regional players are especially vulnerable, as limited purchasing power reduces their ability to hedge against price swings. Because these raw materials constitute significant portions of total cost for impact-resistant window systems, supply chain volatility continues to challenge market stability and slows project execution timelines, restraining growth in both retrofit and new-build segments.

Federal Resilience Funding and Urban Retrofit Modernization

A large portion of housing stock in hurricane-prone regions was built before modern building code revisions. The retrofit opportunity in the U.S. Gulf Coast and Caribbean region alone represents a multibillion-dollar addressable segment. The FEMA expanded allocations under its Building Resilient Infrastructure and Communities (BRIC) program to prioritize structural mitigation projects, including fortified building envelope upgrades. Municipal governments are increasingly using these funds to modernize public housing and community infrastructure in wind-exposed zones. This shift supports broader adoption of certified impact-resistant window systems in both public and private properties. As local authorities aim to reduce long-term disaster recovery spending, retrofit investment is becoming a fiscal strategy rather than a reactive repair measure.

Insurance-linked incentives and federal resilience grants continue increasing homeowner awareness beyond traditional high-income coastal clusters. In 2026, the U.S. Department of Housing and Urban Development (HUD) incorporated resilience-focused rehabilitation criteria into select Community Development Block Grant disaster recovery frameworks. This policy alignment supports financing access for envelope hardening upgrades in vulnerable communities. Contractors are responding with modular storm-proof window systems designed for rapid installation and code compliance. As funding mechanisms mature, retrofit adoption is transitioning from isolated upgrades to coordinated urban resilience programs. This evolution creates a scalable and policy-backed growth channel within the hurricane window market.

Energy-Efficient Innovation and Asia-Pacific Resilience Investment

Dual-function products combining energy-efficient hurricane windows with low-emissivity coatings and smart sensors represent a high-value opportunity. ENERGY STAR-certified glazing reduces heating, ventilation, and air-conditioning (HVAC) costs, creating dual ROI drivers, storm protection and energy savings. The U.S. Department of Energy (DOE) strengthened incentives for high-performance building envelopes under federal energy efficiency initiatives, reinforcing demand for advanced glazing in coastal construction. Builders increasingly align resilient window installation with sustainability certifications to access tax credits and green financing instruments. This convergence improves product differentiation and supports premium pricing strategies. As energy codes tighten, advanced impact-rated glazing becomes part of mainstream compliance rather than a niche upgrade.

Asia-Pacific coastal infrastructure expansion, particularly in India and Southeast Asian economies, presents long-term structural growth potential. The Asian Development Bank approved expanded climate adaptation financing for cyclone-prone urban regions, supporting resilient housing and infrastructure upgrades. These investments are accelerating disaster-mitigation construction standards across emerging coastal cities. Localized manufacturing and cost-optimized vinyl and fiberglass frames can improve affordability while meeting performance requirements. Governments are strengthening national disaster preparedness frameworks, which will gradually formalize compliance expectations for structural openings. This combination of policy-backed infrastructure funding and urban expansion positions Asia-Pacific as a high-growth opportunity zone for certified impact-resistant window solutions.

Category-wise Analysis

Product Type Insights

Single hung windows re expected to represent the leading product types, accounting for approximately 34% of the hurricane window market revenue share in 2026. Their dominance stems from cost efficiency, standardized sizing, and compatibility with large-scale residential construction. Builders continue to favor this format for production housing in hurricane-prone states because it simplifies compliance with wind-borne debris regulations. In early 2026, regional housing authorities in coastal North Carolina referenced impact-rated single hung configurations in updated reconstruction guidance following severe storm damage, reinforcing their suitability for resilient rebuilding. The format supports efficient bulk procurement and predictable installation timelines. These operational advantages sustain its leading share across mainstream impact-resistant window deployments.

Custom windows are projected to be the fastest-growing segment, expanding at an estimated 8.3% CAGR through 2033. Demand is accelerating in architect-designed coastal properties and luxury multi-family developments requiring large-span or specialty glazing. The municipal planning approvals in high-end waterfront districts of Miami highlighted increased use of oversized impact-rated glazing panels in new condominium towers, reflecting a shift toward panoramic hurricane-compliant designs. Developers are integrating bespoke impact-resistant window systems that meet both structural and aesthetic criteria. Customization allows greater daylight optimization while maintaining certified storm performance. This premiumization trend continues to elevate average selling prices and segment growth momentum.

Frame Type Insights

Aluminum frames are likely to lead the market with an estimated 48% revenue share in 2026, reflecting their structural durability and high wind-load tolerance. Their corrosion resistance makes them particularly suitable for coastal and salt-exposed environments. The infrastructure rebuilding projects supported by the U.S. Army Corps of Engineers incorporated reinforced aluminum-framed glazing systems in public coastal facilities to meet enhanced resilience benchmarks. Commercial developers continue specifying aluminum for mid-rise hospitality and office buildings due to strength-to-weight advantages. The established extrusion supply base supports consistent manufacturing output. These factors collectively reinforce aluminum’s dominant role in certified hurricane window systems.

Fiberglass frames are poised to register the fastest growth, advancing at approximately 8.1% CAGR between 2026 and 2033. Builders increasingly recognize fiberglass for its thermal stability and resistance to expansion under fluctuating temperatures. In 2026, energy-focused retrofit programs aligned with guidance from the U.S. Department of Energy emphasized high-performance framing materials capable of improving overall building envelope efficiency in storm-prone regions. Fiberglass supports compliance with both wind-resistance and insulation performance requirements. Its durability reduces long-term maintenance cycles compared to traditional wood alternatives. As sustainability and lifecycle cost metrics gain influence in procurement decisions, fiberglass adoption continues to accelerate across residential and light-commercial projects.

Regional Insights

North America Hurricane Window Market Trends

North America is likely to lead, accounting for approximately 41% of the hurricane window market share in 2026. The United States continues to anchor demand, particularly in coastal and hurricane-prone states. In 2025, the FEMA expanded allocations under its BRIC program to support wind-hardening upgrades in vulnerable communities, indirectly strengthening demand for impact-resistant glazing systems. Updated wind-load enforcement cycles across southeastern states further reinforced compliance-based replacement activity. Insurance underwriting adjustments tied to storm exposure also influenced homeowner retrofit decisions. Commercial developers increasingly specify impact-rated systems to reduce long-term asset risk. These combined regulatory and financial mechanisms sustain the region’s dominant position.

In 2026, the coastal rebuilding and mitigation planning supported by the National Hurricane Center seasonal outlook updates continued to influence municipal preparedness strategies. Several Gulf Coast municipalities integrated enhanced façade protection requirements into public reconstruction tenders following recent storm damage assessments. Domestic manufacturers benefited from localized supply chains, reducing lead times for laminated glass production. Public school districts and healthcare facilities increasingly incorporated certified impact-resistant windows into capital improvement budgets. Retrofit financing support from state-backed resilience funds further widened the addressable base. These developments reinforce North America’s maturity, regulatory clarity, and revenue leadership.

Europe Hurricane Window Market Trends

Europe accounts for approximately 24% of global market share in 2026, demonstrating steady and standards-driven expansion. In 2025, the European Parliament advanced implementation measures under the revised Energy Performance of Buildings Directive (EPBD), encouraging deeper renovation of aging building envelopes. While primarily energy-focused, these upgrades supported the integration of reinforced and laminated glazing in storm-exposed zones. Southern European countries continued strengthening façade resilience requirements in response to intensifying Mediterranean storm systems. Cross-border harmonization of CE marking requirements simplified compliance pathways for impact-rated window manufacturers. Sustainability-linked procurement policies further promoted high-performance glazing systems. The region’s growth remains policy-driven and efficiency-oriented.

The infrastructure modernization programs in Spain and Italy incorporated façade reinforcement components within public coastal redevelopment frameworks. Climate adaptation funding coordinated through the European Commission supported structural upgrades in storm-vulnerable municipalities. Manufacturers responded by expanding thermally efficient, reinforced window lines aligned with green building certifications. Commercial property owners prioritized dual-performance systems combining energy efficiency and wind resistance. Retrofit incentives for residential buildings strengthened replacement demand in older housing stock. Collectively, these verified regulatory and funding movements underpin Europe’s stable market trajectory.

Asia Pacific Hurricane Window Market Trends

Asia Pacific is expected to be the fastest-growing regional market for hurricane windows, projected to expand at around 8.4% CAGR through 2033. In 2025, Japan’s Ministry of Land, Infrastructure, Transport and Tourism updated structural resilience guidance for typhoon-prone prefectures, reinforcing the role of impact-rated glazing in mid- and high-rise buildings. Rapid coastal urbanization across China and India further increased exposure-driven construction demand. Developers in major metropolitan corridors incorporated storm-certified façade systems into new residential towers. Public infrastructure investments also began emphasizing disaster-mitigation specifications. These macro drivers continue to accelerate regional adoption.

The disaster recovery planning following severe typhoon activity in parts of Southeast Asia prompted resilience-focused rebuilding programs supported by national public works agencies. The National Disaster Management Authority emphasized structural strengthening measures in updated mitigation advisories, indirectly supporting reinforced window deployment in cyclone-prone states. Local manufacturing expansion improved cost competitiveness for laminated and impact-rated systems. Public-private housing partnerships increasingly integrated storm-resistant glazing as a baseline safety feature. Regulatory tightening in coastal urban zones is gradually improving compliance uniformity. These policy and infrastructure movements firmly position Asia Pacific as the primary growth engine of the global market.

Competitive Landscape

The global hurricane window market structure is moderately consolidated, with PGT Innovations, Andersen Corporation, JELD-WEN, and MI Windows and Doors majority of the revenue generated. These companies leverage extensive contractor networks, strong brand recognition, and certified impact-resistant product lines. Their vertically integrated manufacturing models enhance quality control and cost efficiency. Continuous R&D investments focus on laminated glass durability, thermal efficiency, and code compliance. Established relationships with builders and distributors reinforce their leadership across hurricane-prone regions.

Regional and specialized players such as ES Windows and Weather Shield compete through architectural customization and niche market focus. High certification requirements and impact-testing standards create strong barriers to entry. However, retrofit demand and premium coastal housing projects open opportunities for agile manufacturers. Partnerships between glass suppliers and installation firms enhance execution capabilities. Gradual consolidation is expected as larger firms pursue acquisitions to strengthen geographic reach and product depth.

Key Industry Developments

- In February 2026, PGT Custom Windows and Doors expanded its portfolio with new Scout and Sparta aluminum window systems and two French door models, FD 450 Estate and FD 160. Offering hurricane protection, the additions offer builders and homeowners broader choices in durability, design flexibility, and impact-resistant performance.

- In January 2026, Hope’s Windows showcased its Old World Suite Impact hurricane-rated steel windows and doors at the 2026 National Association of Home Builders (NAHB) International Builders’ Show (IBS). The systems are engineered for coastal and high-wind regions, delivering verified resistance to wind loads, impact, air infiltration, and water penetration.

- In August 2025, Vytex Windows introduced the Potomac Coastal Series, an impact-rated window collection designed for Florida and other hurricane-prone regions. The system features reinforced frames and laminated glass for wind-borne debris protection while offering up to 40% more glass area for improved daylight and aesthetics.

Companies Covered in Hurricane Window Market

- PGT Innovations

- Andersen Corporation

- JELD-WEN Holding Inc.

- MI Windows and Doors

- Pella Corporation

- YKK AP Inc.

- Marvin

- CGI Windows & Doors

- Alside

- Simonton Windows & Doors

- WinDoor

- Weather Shield

- Harvey Building Products

Frequently Asked Questions

The global hurricane window market is projected to reach US$ 3.5 billion in 2026.

Surging hurricane intensity, stricter coastal building codes, insurance-linked compliance requirements, and growing retrofit demand are the primary market drivers.

The market is poised to witness a CAGR of 6.9% from 2026 to 2033.

Expansion of coastal residential construction, government-backed resilience programs, and demand for energy-efficient impact-resistant glazing are creating significant growth opportunities.

PGT Innovations, Andersen Corporation, JELD-WEN, and MI Windows and Doors are among the leading players in the market.