- Industrial Machinery

- Dye Package Winder Market

Dye Package Winder Market Size, Share, and Growth Forecast, 2026 - 2033

Dye Package Winder Market by Product Type (Automatic, Semi-Automatic, Manual), Winding Type (Random Winding, Precision Winding), Application (Textile Industry, Technical Textiles, Others), and Regional Analysis 2026 - 2033

Dye Package Winder Market Size and Trends Analysis

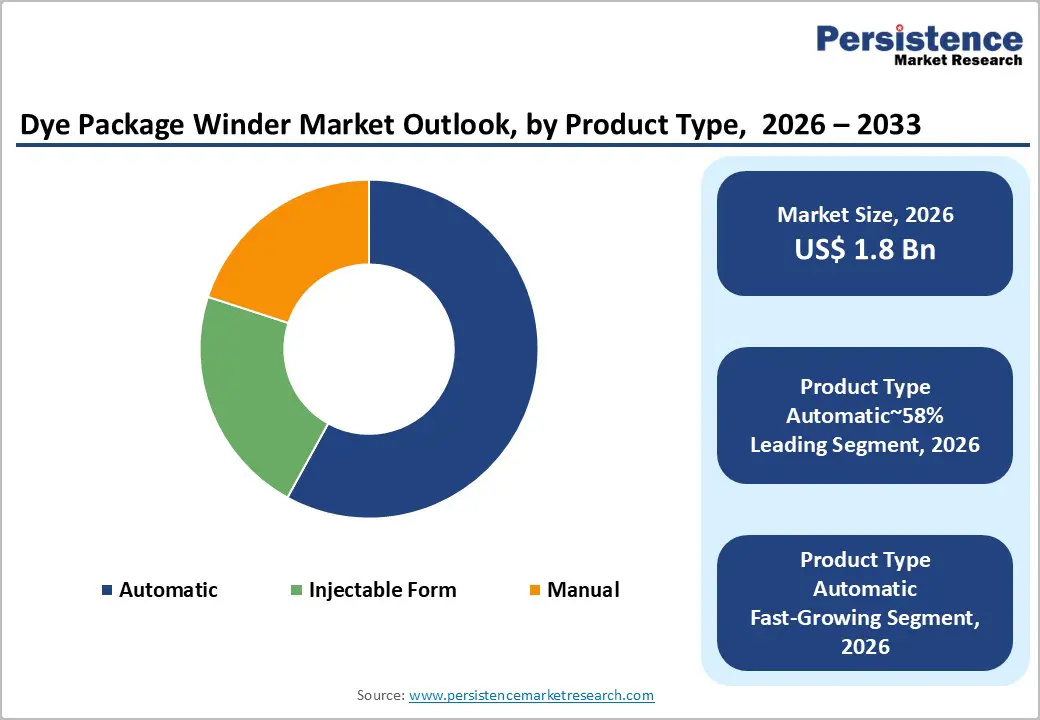

The global dye package winder market size is likely to be valued at US$1.8 billion in 2026 and is expected to reach US$2.6 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033, driven by the expansion of global textile production to meet increasing demand for high-quality fabrics. Manufacturers are increasingly adopting automated winding systems to improve yarn uniformity and dyeing consistency, supporting sustained market development. Additionally, modern winding technologies emphasize energy efficiency and precision, helping reduce operational costs while enhancing overall productivity.

Key Industry Highlights:

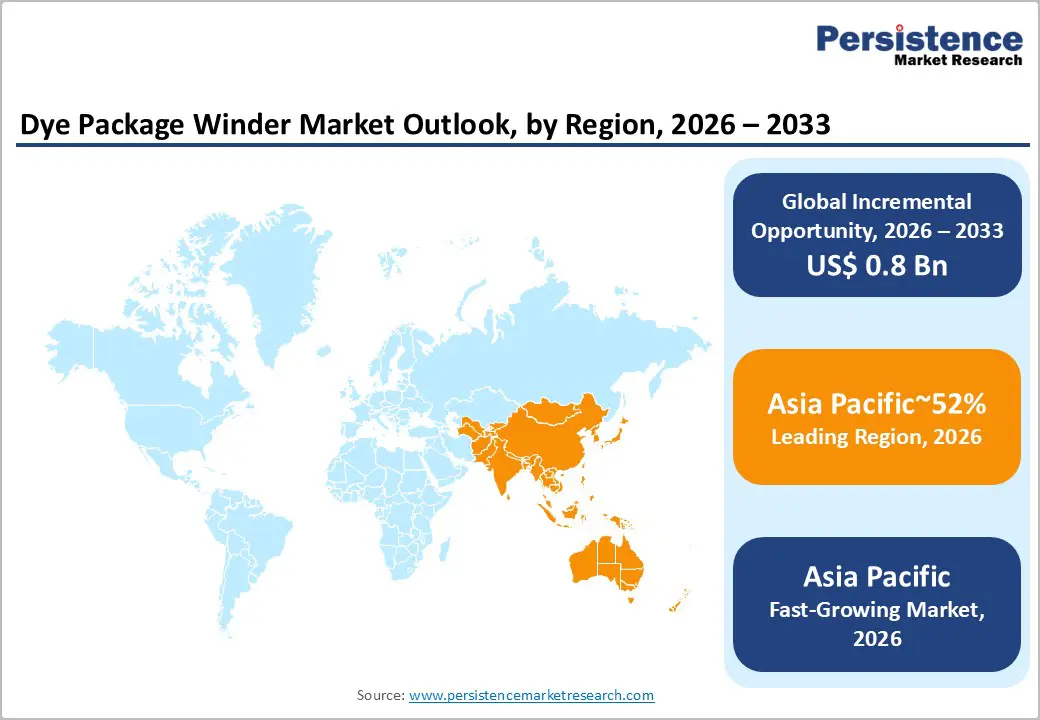

- Leading Region: Asia Pacific is projected to lead, accounting for approximately 52% share in 2026, supported by dense manufacturing clusters and supportive industrial policies.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest, driven by rapid urbanization and massive investments in textile parks.

- Leading Product Type: Automatic is anticipated to dominate, accounting for approximately 58% share in 2026, anchored by significant labor cost reductions.

- Leading Application: The textile industry is expected to lead, accounting for approximately 44% share in 2026, anchored by comprehensive material consumption.

| Key Insights | Details |

|---|---|

|

Dye Package Winder Market Size (2026E) |

US$1.8 Bn |

|

Market Value Forecast (2033F) |

US$2.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.0% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Automation Adoption in Winding Systems Driven by Labor Cost Pressures and Efficiency Gains

Global textile mills are increasingly adopting automated winding systems to mitigate escalating labor cost pressures. High-speed machinery minimizes manual intervention while ensuring consistent yarn quality across large production volumes. This transition enhances workflow efficiency, particularly within export-oriented manufacturing hubs requiring operational scalability. Enterprises prioritize equipment enabling continuous operations while maintaining uniform package density and structural consistency. Savio Macchine Tessili S.p.A., with Proxima Smartconer, reflects growing preference for advanced automated winding configurations. These dynamics integrate cost optimization with productivity enhancement across competitive textile production environments.

Modern winding platforms incorporate intelligent sensors enabling real-time yarn monitoring and defect detection capabilities. These systems reduce material waste by identifying inconsistencies during high-speed winding operations. Digital integration improves overall equipment effectiveness through synchronized control of multiple spindle units. Centralized management systems enhance operational coordination across complex textile manufacturing setups. Murata Machinery Ltd., with AIcone, demonstrates integration of automation with intelligent process control technologies. This convergence of automation and analytics strengthens production reliability and supports consistent quality output across industrial-scale operations.

Technical Textile Sector Expansion

The rapid expansion of technical textiles is generating new procurement requirements for advanced winding machinery globally. End-use industries such as medical, automotive, and protective equipment demand performance-specific yarn structures. These applications require controlled tension and precision winding to maintain structural integrity under demanding conditions. This diversification is increasing demand for versatile systems capable of handling high tenacity industrial yarns. SSM Schärer Schweiter Mettler AG, with DURO TW, supports heavy-duty winding requirements across technical textile processing environments. This shift embeds application-specific engineering into machinery design and procurement strategies.

Growing utilization of specialty fibers necessitates robust winding architectures capable of managing complex filament characteristics. Manufacturers are adapting equipment portfolios to address strength, elasticity, and abrasion resistance requirements. This alignment enables entry into high-margin segments associated with industrial and performance textiles. Increasing consumption of reinforced fabrics is driving innovation in handling heavy count yarn configurations. Savio Macchine Tessili S.p.A., with Phoenix Assembly Winder, reflects demand for specialized solutions within technical textile production ecosystems. These dynamics collectively expand revenue potential across niche, high-performance textile manufacturing segments.

Restraint Analysis - High Initial Capital Expenditure Limiting Automation Adoption in Winding Systems

Significant capital requirements for advanced automated winding machinery act as a primary adoption barrier. Small and medium textile units face constrained financing access for upgrading legacy equipment infrastructure. Elevated equipment pricing limits the penetration of Industry 4.0-enabled winding technologies across fragmented manufacturing clusters. High-interest-rate environments further restrict capital allocation toward premium machinery procurement decisions. Rieter Holding AG with Autoconer X6 represents high investment thresholds associated with technologically advanced winding platforms. These financial constraints structurally delay modernization cycles across cost-sensitive textile production ecosystems.

Extended payback periods discourage conservative manufacturers from transitioning toward fully automated winding configurations. Equipment pricing structures often misalign with limited capital reserves within decentralized textile mill networks. This economic imbalance sustains demand for refurbished machinery and manual winding systems with lower upfront costs. Budgetary limitations slow the replacement of legacy systems, preserving operational inefficiencies across production facilities. Savio Macchine Tessili S.p.A., with Proxima Smartconer, highlights the widening investment gap between manual and digitally integrated winding solutions. These conditions collectively constrain technology diffusion despite clear operational efficiency advantages.

Energy Consumption Volatility Impacting Cost Structures and Automation Adoption

High-throughput winding systems require substantial electrical input for suction motors and spindle operations. Rising industrial energy tariffs are compressing operating margins across textile manufacturing facilities globally. This cost pressure is influencing procurement strategies toward machines with optimized energy consumption profiles. Manufacturers must balance throughput efficiency with escalating electricity costs, impacting total production economics. Savio Macchine Tessili S.p.A., with Proxima Smartconer, emphasizes energy-optimized winding configurations under cost-sensitive operating environments. These dynamics structurally constrain the adoption of high-speed systems lacking integrated energy management capabilities.

Power supply instability in emerging markets introduces operational disruptions affecting production continuity and equipment reliability. Textile mills increasingly invest in backup infrastructure to safeguard electronically controlled winding machinery systems. This additional capital requirement elevates the total cost of ownership, reducing the attractiveness of advanced automated solutions. Regulatory scrutiny on energy-intensive processes is intensifying under evolving global sustainability compliance frameworks. SSM Schärer Schweiter Mettler AG with NEO YW reflects industry focus on minimizing energy consumption per spindle operation. These constraints collectively slow automation diffusion across regions with inconsistent energy infrastructure and regulatory pressures.

Opportunity Analysis - Industry 4.0 and IoT Integration Enhancing Operational Intelligence in Winding Systems

Integration of Internet of Things technologies is transforming maintenance frameworks within textile winding operations globally. Sensor-driven data acquisition enables predictive maintenance, reducing unplanned downtime and mechanical failure risks. Real-time analytics enhance spindle performance optimization, directly improving yarn consistency and process stability. Digital integration increases supply chain transparency, supporting traceability requirements across regulated textile production environments. Murata Machinery Ltd., with MSS Muratec Smart Support, enables data-centric maintenance and operational visibility. These capabilities embed intelligence into machinery, shifting operational models toward continuous performance monitoring systems.

Remote monitoring architectures enable centralized management of geographically distributed textile manufacturing facilities with improved coordination. Smart winding platforms facilitate efficient resource utilization, minimizing material waste and optimizing production throughput levels. Cloud-based data systems support structured audit trails, strengthening compliance with evolving quality assurance standards. Regulatory emphasis on traceability is reinforcing the adoption of connected machinery within industrial textile ecosystems. Savio Macchine Tessili S.p.A., with Savio Insight, delivers integrated digital platforms for connected winding operations. This technological shift is attracting investment from manufacturers prioritizing automation, scalability, and data-driven production control.

Sustainable Fiber Processing Driving Advanced Winding System Adoption

Rising demand for recycled and organic yarns is significantly reshaping winding system design requirements. Processing short staple recycled fibers necessitates controlled tension management and advanced splicing precision technologies. These material characteristics introduce structural variability, requiring adaptive winding architectures to maintain yarn integrity. Sustainable manufacturing mandates are accelerating replacement cycles for legacy winding equipment lacking process flexibility. Saurer AG with Autocoro 11 integrates optimized rotor spinning aligned with recycled fiber processing requirements. This transition embeds sustainability criteria directly into machinery procurement frameworks across textile production environments.

Eco-friendly dyeing processes impose stringent requirements on package density uniformity and permeability characteristics. Advanced winding systems enable optimized package geometry supporting low liquor ratio dyeing process efficiency. This alignment directly reduces water consumption and chemical usage within regulated textile processing operations. Regulatory pressure on effluent discharge is reinforcing the adoption of precision-controlled winding technologies. SSM Schärer Schweiter Mettler AG with NEO FW demonstrates adaptability for diverse sustainable yarn structures and compositions. Vendors integrating circular economy capabilities are strengthening competitive positioning within evolving textile manufacturing ecosystems.

Category-wise Analysis

Product Type Insights

The automatic segment is expected to lead, accounting for approximately 58% share in 2026, anchored by the critical requirement to reduce labor dependency in textile mills. Fully automated winding platforms minimize human intervention while maximizing the output of high-quality yarn packages. Enterprises are increasingly investing in link-winding systems that connect spinning frames directly to the winding unit. This integration eliminates manual handling and reduces the risk of yarn contamination during processing. Saurer with Autoconer X6 and Murata Machinery with QPRO EX exemplify the industry standard for high-speed automatic winding. Systems engineered for continuous operations ensure stable production cycles even in labor-scarce environments. Digital monitoring tools provide real-time data on spindle performance to maintain high efficiency levels. The convergence of labor cost pressures and technological maturity sustains the dominance of the automatic segment.

The automatic is also forecast to be the fastest-growing segment, driven by the aggressive transition toward Industry 4.0 and autonomous manufacturing. Modern mills are prioritizing software-driven equipment that integrates seamlessly into digital factory ecosystems. AI-powered features like adaptive tension control and intelligent bobbin flow management enhance production transparency. Savio Macchine Tessili with Proxima Smartconer and Rieter with Autoconer X6 lead this shift toward intelligent automation. These platforms offer significant energy savings through optimized suction motor control and individual spindle drives. As data connectivity becomes a standard requirement, the uptake of smart automatic winders is accelerating. The ongoing evolution of IoT-enabled maintenance further reinforces the growth trajectory of this technology-heavy segment.

Application Insights

The textile industry is expected to dominate, accounting for approximately 44.0% share in 2026, underpinned by the massive volume of apparel and home textile production globally. High-throughput winding systems are essential for preparing yarn packages that withstand intensive industrial dyeing cycles. Manufacturers prioritize equipment that can process various natural and synthetic fibers with consistent tension. This segment's dominance is reinforced by the continuous expansion of the global fashion retail market. Savio Macchine Tessili with Proxima Smartconer and Murata Machinery with AIcone support this large-scale production through automated winding. This structural alignment between high-volume demand and automation sustains the segment's market leadership.

Technical textiles are anticipated to be the fastest-growing segment, driven by the rising demand for specialized fibers in the automotive and medical sectors. Protective clothing and industrial filtration products require yarns with exceptional strength and precise package density. Advanced winding platforms enable the processing of high-performance filaments like aramid and carbon fibers. Integration of smart tension control supports the processing of delicate or abrasive technical yarns without damage. As global safety standards tighten, the procurement of specialized winding systems for protective gear is accelerating. This shift toward performance-oriented textiles is expanding the addressable market for versatile winding solutions.

Regional Insights

Asia Pacific Dye Package Winder Market Trends

Asia Pacific is expected to remain the leading regional market and is anticipated to be the fastest growing market, accounting for approximately 52% share in 2026, supported by massive textile production clusters. The region's dominance is anchored in large-scale spinning facilities that serve both domestic apparel markets and global export demands. High-throughput automated winders are essential for maintaining the competitive pricing and quality required by international retailers. Regional players are increasingly focusing on integrating Industry 4.0 technologies to mitigate rising operational costs. Energy efficiency remains a primary driver for machinery replacement cycles across dense industrial zones.

India is expected to anchor regional momentum through sustained investments in automated winding technologies aligned with export-driven textile strategies. Government-led initiatives like the Production Linked Incentive (PLI) scheme are anticipated to accelerate the adoption of advanced winding systems. Savio Macchine Tessili with Proxima Smartconer is expected to benefit from localization strategies that enhance service availability within textile hubs. Regulatory focus on improving yarn quality for global competitiveness is projected to increase procurement volumes among large spinning mills. The expansion of technical textile manufacturing in the country further reinforces the demand for specialized precision winders.

Europe Dye Package Winder Market Trends

Europe is expected to remain a structurally stable regional market, with demand primarily anchored in premiumization and replacement cycles. The region focuses on high-end textile production where precision and specialized yarn handling are critical for luxury fashion. Manufacturers prioritize winding systems that offer extreme flexibility for small-batch, high-variety production cycles. Strict environmental regulations are driving the adoption of energy-efficient machinery that reduces the carbon footprint of textile operations. Digitalization and IoT integration are standard requirements for maintaining high operational standards in the region.

Italy is expected to lead European demand through its world-renowned textile engineering sector and high-end fashion manufacturing base. Domestic manufacturers are investing in advanced precision winders to maintain their leadership in the luxury apparel segment. SSM with XENO-YW is positioned to meet the stringent quality requirements of Italian silk and fine wool processors. The focus on sustainable manufacturing is likely to drive the procurement of winders optimized for recycled natural fibers. Strategic partnerships between machinery vendors and premium textile brands are anticipated to foster localized technological innovation.

North America Dye Package Winder Market Trends

North America is expected to remain structurally stable, with demand primarily anchored in technical textile and medical applications. The market is characterized by a high concentration of technical fiber production for the aerospace and defense sectors. Manufacturers prioritize high-reliability winding platforms capable of handling specialty filaments with extreme precision. Labor scarcity in the region continues to drive the demand for fully autonomous and high-speed winding solutions. Compliance with strict safety and quality standards remains a key factor in machinery procurement decisions.

The U.S. is expected to anchor regional demand through its growing focus on domestic technical textile manufacturing and reshoring initiatives. Investments in advanced fiber research are projected to necessitate more sophisticated winding and yarn preparation equipment. Murata Machinery with QPRO EX is expected to serve the needs of high-capacity industrial yarn producers in the region. Growing demand for medical-grade textiles is anticipated to expand the utilization of specialized precision winding units. Regulatory support for sustainable and domestically produced textiles is likely to influence the adoption of next-generation winding technologies.

Competitive Landscape

The global dye package winder market is moderately consolidated, with leadership concentrated among global machinery manufacturers such as Murata Machinery, Saurer, and Savio Macchine Tessili. This structure reflects high engineering intensity and capital requirements for automated winding systems. Leading players matter because they establish performance benchmarks in precision winding, energy efficiency, and digital integration standards across textile production ecosystems. Procurement decisions are strongly influenced by their installed base, service reliability, and proprietary splicing and tension control technologies. Murata Machinery with QPRO EX, Saurer with Autoconer X6, and Savio Macchine Tessili with Proxima reinforce functional leadership through scalable automation architectures.

Competitive positioning is increasingly defined by integration depth across digital ecosystems and service-oriented machinery models. Premium players emphasize AI-driven monitoring and full mill integration to justify higher capital deployment thresholds. Mid-tier competitors focus on energy efficiency and operational reliability to address cost-sensitive textile clusters. Industry dynamics are shifting toward predictive maintenance adoption, IoT-enabled connectivity, and ecosystem partnerships with dyeing and spinning value chains. SSM with NEO-YW and Rieter with Autoconer X6 illustrate this transition toward data-rich, connected winding platforms. Market behavior indicates gradual consolidation within high-precision segments as software capability becomes a primary competitive lever.

Key Industry Developments:

- In March 2026, Ariser Engineering announced the unveiling of its Automatic Autodoffer Loading System for winding units at Texfair 2026. This development automates the final stages of the winding process, further reducing reliance on manual labor in textile spinning mills.

- In February 2026, Rieter completed the acquisition of the Barmag division from Oerlikon, integrating it as a new "Man-Made Fiber" division. This move significantly expands Rieter's reach into the synthetic fiber winding and processing sector, positioning it as a comprehensive system supplier for both natural and man-made yarns.

Companies Covered in Dye Package Winder Market

- Murata Machinery Ltd.

- Rieter Holding AG

- Saurer Group

- Savio Macchine Tessili S.p.A.

- Trützschler Group

- Lakshmi Machine Works

- Jingwei Textile Machinery Co., Ltd.

- Itema Group

- Uster Technologies AG

- SSM Schärer Schweiter Mettler AG

- Aikoku Alpha Corporation

- Hashima Co., Ltd.

- TMT Machinery, Inc.

- Toyota Industries Corporation

- Marzoli Machines Textiles S.r.l.

- Karl Mayer Group

Frequently Asked Questions

The global dye package winder market is estimated to be valued at approximately US$1.8 billion in 2026 and is projected to reach around US$2.6 billion by 2033, growing at a CAGR of 5.5% during the forecast period.

The primary driver of growth in the dye package winder market is the increasing adoption of automation, which reduces labor dependency while improving operational efficiency. Precision winding technologies enhance dyeing consistency and material utilization, making them essential for modern textile production. Additionally, rising demand for technical textiles and the need to meet stringent export quality standards are further accelerating market adoption.

The dye package winder market is expected to grow at a CAGR of 5.5% during the forecast period 2026 – 2033. Structural shifts sustain momentum.

Asia-Pacific leads with approximately 52% share in 2026. Manufacturing hubs and investments underpin this position. Growth continues fastest here.

Key players in the dye package winder market include Murata Machinery Ltd., Rieter Holding AG, Saurer Group, Savio Macchine Tessili S.p.A., SSM Schärer Schweiter Mettler AG, Trützschler Group, Lakshmi Machine Works, and Karl Mayer Group.