- Renewable Energy

- Wind Turbine Pitch System Market

Wind Turbine Pitch System Market Size, Share, and Growth Forecast, 2025 - 2032

Wind Turbine Pitch System Market By Product Type (Pitch Motors, Pitch Valves, Pitch Pumps, Remote Terminal Software, Pitch Servo Drives), Application (On-Shore Turbines, Off-Shore Turbines), and Regional Analysis for 2025 - 2032

Wind Turbine Pitch System Market Share and Trends Analysis

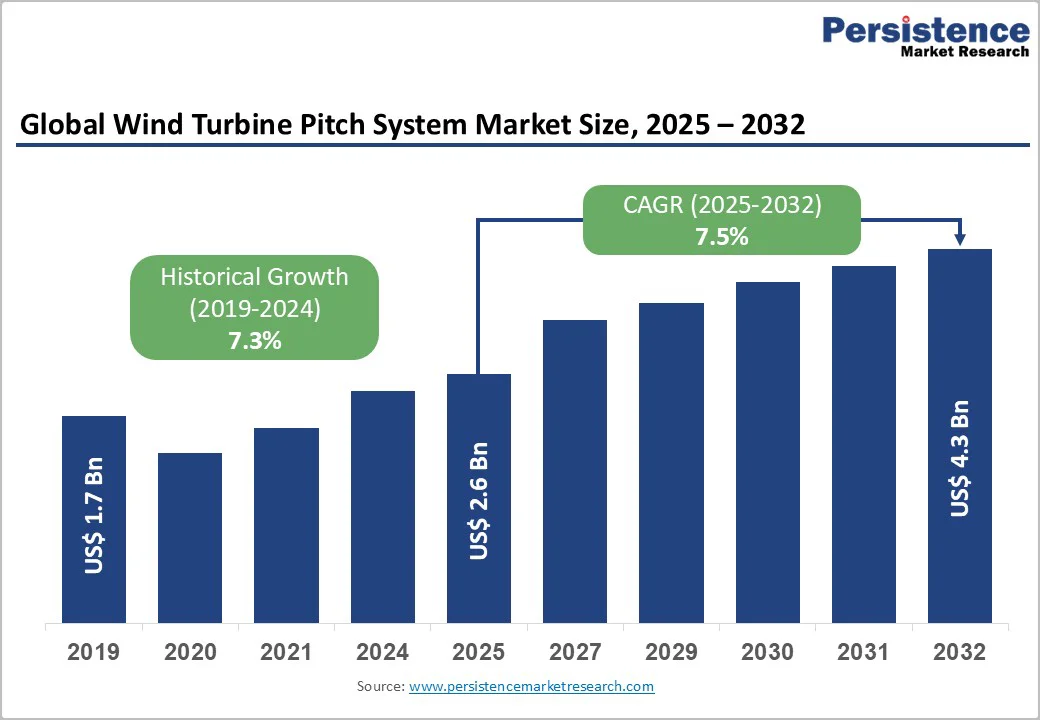

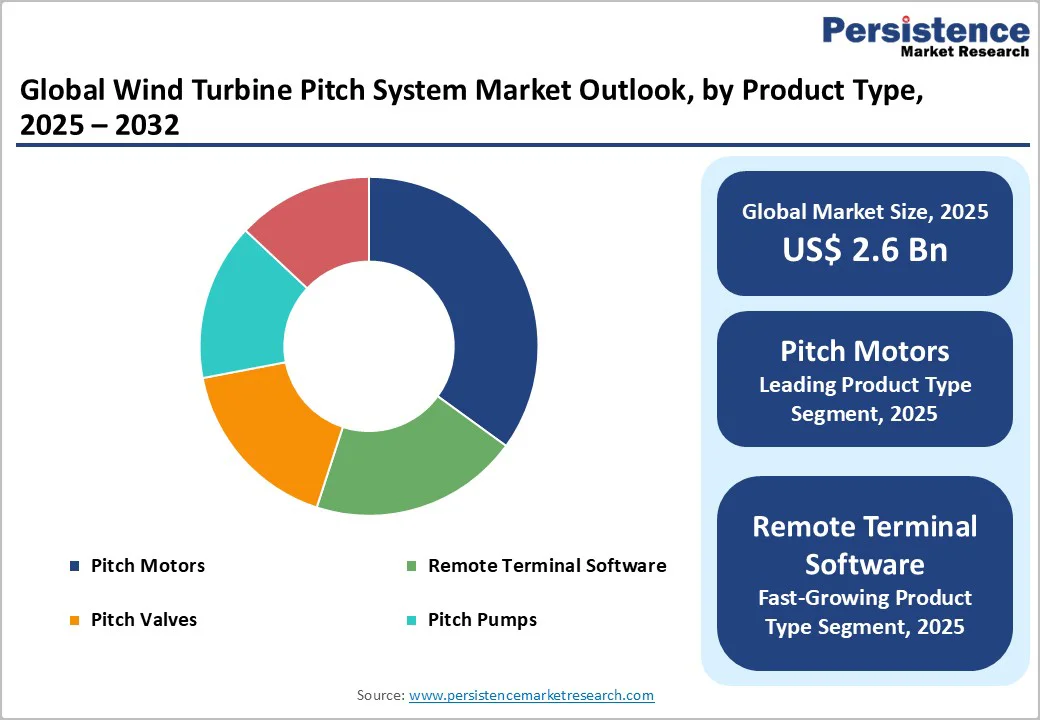

The global wind turbine pitch system market size is likely to be valued at US$2.6 billion in 2025, and is projected to reach US$4.3 billion by 2032, growing at a CAGR of 7.5% during the forecast period 2025-2032. Market growth is primarily driven by increasing investments in renewable energy, especially wind power, technological advancements in pitch-control systems that enhance turbine efficiency, and favorable government policies that promote clean energy adoption.

Key Industry Highlights

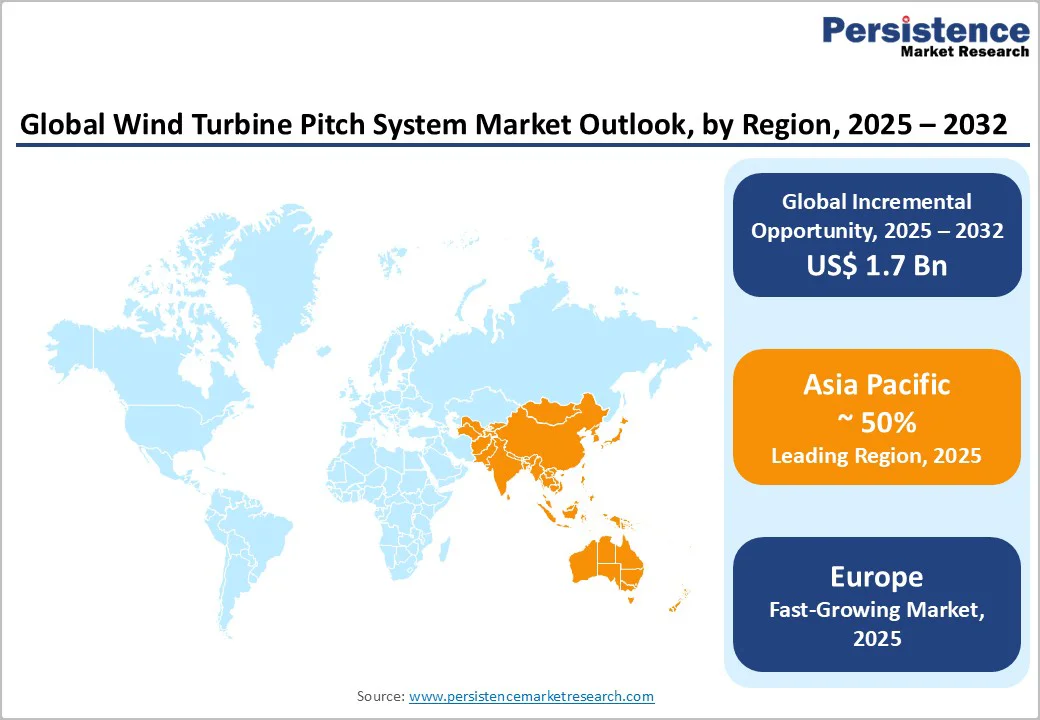

- Dominant Region: Asia Pacific leads the market with an estimated 50% share in 2025, driven by large-scale onshore and offshore installations and integrated manufacturing.

- Fastest-growing Regional Market: Europe holds about 34% of the market share, driven by large-scale turbine retrofits, advanced digital monitoring, and a strong, integrated manufacturing and service ecosystem.

- Leading Product Type: Pitch motors lead the product segment, accounting for over 35% of revenue in 2025, known for their precise blade control.

- Leading Application: Offshore turbines lead the application segment, with an estimated 55% revenue share, driven by their resilience in harsh conditions.

| Report Attribute | Details |

|---|---|

|

Wind Turbine Pitch System Market Size (2025E) |

US$2.6 Bn |

|

Market Value Forecast (2032F) |

US$4.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Advancements in Pitch Systems

Technological advancements in pitch systems are revolutionizing the efficiency and reliability of modern wind turbines. Innovative control algorithms now enable pitch mechanisms to respond more precisely to fluctuating wind speeds, reducing mechanical stress on blades and extending operational life. Smart sensors integrated into pitch systems monitor real-time blade conditions, enabling predictive maintenance and minimizing unplanned downtime. These developments also facilitate dynamic load management, optimizing energy capture during variable wind conditions while protecting turbine components from excessive wear. Advanced materials, such as lightweight composites and corrosion-resistant alloys, enhance the durability and responsiveness of pitch mechanisms, enabling faster adjustments and improved overall performance.

Emerging digitalization trends have led to more integrated pitch systems capable of seamless communication with turbine supervisory control systems. This connectivity enables adaptive adjustments based on wind forecasts, grid demand, and turbine health data, enhancing overall energy output. Remote monitoring and automated diagnostics have become standard features, lowering operational costs and improving safety during maintenance. Modular and compact designs further simplify installation and reduce maintenance complexity. As these technological improvements continue, wind energy operators can achieve higher efficiency, longer asset life, and more reliable performance under diverse environmental conditions, driving growth and adoption across onshore and offshore installations.

High Initial Capital Investment

High initial capital investment poses a significant challenge for adopting advanced pitch systems in wind turbines. The cost of precision components, such as high-performance sensors, actuators, and control units, remains substantial, often forming a large portion of the overall turbine setup. Installation of these systems requires specialized engineering expertise and advanced tools, which further increases upfront expenditure. For smaller operators or new entrants in the wind energy sector, these financial requirements can limit the ability to implement state-of-the-art pitch mechanisms. The need for custom designs in certain turbine models also increases the investment burden, as standardized solutions may not meet all operational requirements.

Maintenance and integration planning contribute to the financial burden during the initial phase. Advanced pitch systems often demand sophisticated monitoring software and calibration procedures, which must be factored into project budgets. Long lead times for procuring critical components can delay commissioning and add indirect costs. This high upfront expenditure can slow the adoption rate, particularly in emerging markets or regions with limited financing options. Investors and project developers may choose simpler or older technologies to manage costs, which restricts the deployment of highly efficient and responsive pitch systems.

Technological Convergence and Digitalization

Technological convergence and digitalization present a significant opportunity for enhancing the performance and efficiency of wind turbine pitch systems. Integration of advanced sensors, IoT devices, and real-time data analytics allows turbines to continuously monitor blade conditions, wind patterns, and mechanical stress. This real-time intelligence enables adaptive control of blade angles, optimizing energy capture while minimizing component wear. Machine learning (ML) algorithms can analyze historical and live data to predict optimal operational strategies, improving overall efficiency. The convergence of mechanical, electrical, and software systems ensures that turbines operate more smoothly, reducing downtime and extending the life of critical components.

Digitalization also facilitates remote monitoring and automated maintenance scheduling, reducing labor requirements and operational costs. Cloud-based platforms enable operators to manage multiple turbines or entire wind farms from a central location, enhancing coordination and performance tracking. Integration with energy management systems allows turbines to respond dynamically to grid demands, maximizing energy output during peak periods. Modular software updates and digital twins provide a platform for continuous improvement without requiring major hardware changes. These innovations open pathways for smarter, more reliable, and cost-effective wind energy production, while supporting scalability across onshore and offshore installations.

Category-wise Analysis

Product Type Insights

Pitch motors dominate the product segment, accounting for over 35% of the revenue share in 2025, due to their essential role in adjusting blade angles for optimal energy capture. Their precise torque control minimizes mechanical stress and enhances turbine efficiency across varying wind conditions. Continuous innovations in motor design, durability, and performance reinforce their reliability in onshore and offshore environments. Integration with smart turbine control systems ensures seamless operation, while their robustness under harsh conditions sustains their dominant market position, making them the preferred choice for modern wind energy projects.

Remote terminal software is the fastest-growing product segment, accounting for around 20% of revenue, driven by the rise of digital monitoring and control systems. It enables real-time pitch adjustments, predictive maintenance, and diagnostics from centralized locations, reducing operational costs and downtime. Cloud-based platforms allow efficient management of multiple turbines and wind farms, while automated updates and performance tracking improve reliability. Its adaptability to advanced turbine systems and focus on operational efficiency drive rapid adoption across both onshore and offshore installations.

Application Insights

Offshore turbines dominate the application segment, capturing an estimated 55% of the wind turbine pitch system market revenue share in 2025. Their placement in areas with stronger and more consistent wind requires highly reliable pitch systems that can endure harsh marine conditions, including saltwater corrosion, high winds, and storms. Advanced pitch mechanisms ensure optimal blade performance while maintaining turbine longevity. The demand for resilient, high-performance systems in offshore installations drives the segment’s leadership, making it a key focus area for turbine manufacturers and operators seeking to maximize energy output in challenging environments.

Onshore turbines are likely to be the fastest-growing application segment through 2032, supported by increasing installations in emerging economies. Their lower deployment and maintenance costs, combined with easier accessibility, make them an attractive option for expanding wind energy capacity. Onshore turbines benefit from advances in pitch system technology, enabling efficient energy capture and operational reliability in diverse terrains. Rapid development of wind infrastructure in regions with growing energy demand further accelerates adoption, positioning onshore turbines as a high-growth segment across both developed and developing markets.

Regional Insights

Asia Pacific Wind Turbine Pitch System Market Trends

As of 2025, the Asia Pacific accounts for an estimated 51% of the wind turbine pitch system market share. This dominant position is driven by the massive scale of wind energy installations in China, resulting in both onshore and offshore development. The region’s vertically integrated manufacturing ecosystem produces turbines alongside critical components, including pitch motors, servo drives, and control modules. This integration lowers component costs, accelerates delivery, and enables rapid deployment of advanced pitch systems. The proximity between manufacturing facilities and large wind farms enables faster feedback, technology upgrades, and operational efficiency, strengthening the region’s supply chain and competitiveness.

Strong policy support and strategic investment in offshore wind projects are major factors in the sector's dominance. Countries such as China, India, Taiwan, and Vietnam are increasingly deploying large turbines in deep-water sites where precise blade pitch control is essential for efficiency and reliability. The demand for advanced pitch systems in these high-load applications, combined with local manufacturing capacity and concentrated adoption, ensures that the Asia Pacific region remains the leading market for wind turbine pitch systems.

Europe Wind Turbine Pitch System Market Trends

Europe holds roughly 34% of the global market share in 2025. The region's strong position is deeply rooted in its retrofit wave of ageing wind assets. Large fleets of turbines installed over a decade earlier are now entering mid-life, prompting retrofit programs that upgrade traditional fixed-pitch systems to high-precision electric or hybrid pitch drives. This dual demand, from new offshore mega-turbines and multiple retrofit cycles, has generated a sustained and broad opportunity for pitch-system manufacturers. Since most European turbines exceed 3-MW and operate offshore, manufacturers must supply robust pitch drives capable of high torque, corrosion resistance, and digital connectivity, creating a high-barrier niche that favors existing suppliers.

The European market also benefits from its highly integrated supply chain and policy-backed ecosystem. Germany, Denmark, and the UK lead in turbine manufacturing, component production, and system services. A growing number of European wind power installations have been incorporating digital monitoring of pitch systems over the past couple of years. This reflects the region’s mature industrialization in wind technology, where blade pitch functions are combined with condition monitoring, servicing contracts, and lifecycle optimization. The combination of heavy offshore investment, large-scale retrofit needs, and a robust industrial base ensures Europe remains the global center for advanced pitch-system adoption.

Competitive Landscape

The global wind turbine pitch system market structure is moderately consolidated, with major players such as Siemens Gamesa Renewable Energy, Vestas, and General Electric together holding more than half of the global market share. These leading companies leverage their extensive product portfolios, global manufacturing capabilities, and established service networks to maintain dominance in both onshore and offshore wind projects. Their broad range of solutions covers different turbine sizes, pitch drive technologies, and digital control systems, allowing them to serve diverse applications while meeting the increasing demand for precision, reliability, and efficiency.

Several mid-tier players are actively competing by targeting specialized segments such as offshore turbines, lightweight pitch drives, or digital-enhanced monitoring systems. This competitive landscape features a mix of large, well-resourced incumbents and innovative companies pushing technological boundaries. The presence of both types of players fosters ongoing advancement in pitch system efficiency, durability, and integration with turbine controls, ultimately driving growth and improving performance across the global wind energy sector.

Key Industry Developments

- In August 2025, India’s Ministry of New and Renewable Energy (MNRE) renamed the Revised List of Models and Manufacturers (RLMM) as the Approved List of Models and Manufacturers (ALMM) for wind, mandating the use of approved major wind turbine components such as pitches, blades, towers, gearboxes, generators, and special bearings in manufacturing. Exemptions apply for new manufacturers and models, allowing up to 800 MW capacity over two years to encourage innovation and efficiency.

- In June 2025, Water2Energy increased the power output of its 1.2 MW tidal turbine by 20% by implementing a new blade pitch control system. This advanced system optimizes the blade angle in real-time to maximize energy capture and efficiency from tidal flows, enhancing the turbine’s performance and reliability in challenging marine environments.

- In April 2025, Richardson Electronics expanded its partnership with TransAlta Corporation to supply patented ultracapacitor-based pitch energy modules for GE wind turbines across Canada and the U.S., replacing lead acid batteries with more reliable, maintenance-free solutions. This upgrade has significantly reduced turbine downtime, improved operational efficiency, and boosted long-term revenue for TransAlta.

Companies Covered in Wind Turbine Pitch System Market

- Siemens Gamesa Renewable Energy

- Vestas Wind Systems

- General Electric Renewable Energy

- Windurance

- Parker Hannifin Corporation

- Mita-Teknik

- KK Wind Solutions

- Dongfang Electronic Corporation

- Eaton

- Bosch Rexroth AG

- KEB Automation

- Hydratech Industries

Frequently Asked Questions

The global wind turbine pitch system market is projected to reach US$ 2.6 billion in 2025.

The growing need for precise blade control to optimize energy output, enhance turbine efficiency, and ensure operational reliability in both onshore and offshore wind farms is driving the market.

The market is poised to witness a CAGR of 7.5% from 2025 to 2032.

Rising demand for offshore wind farms, turbine retrofits, and digitalized pitch control systems presents key growth opportunities in the market.

Key players in the market include Siemens Gamesa Renewable Energy, Vestas Wind Systems, General Electric Renewable Energy, Windurance, Parker Hannifin Corporation, and Mita-Teknik.