- Medical Devices

- Pressure Ulcer Devices Market

Pressure Ulcer Devices Market Size, Share, and Growth Forecast, 2025 - 2032

Pressure Ulcer Devices Market By Device Type (Static Support Surfaces, Dynamic Support Surfaces, Others), Ulcer Stage (Stage I, Stage II, Stage III, Stage IV, Deep Tissue Injury), End-user (Hospitals, Clinics, Others), and Regional Analysis for 2025 - 2032

Pressure Ulcer Devices Market Share and Trends Analysis

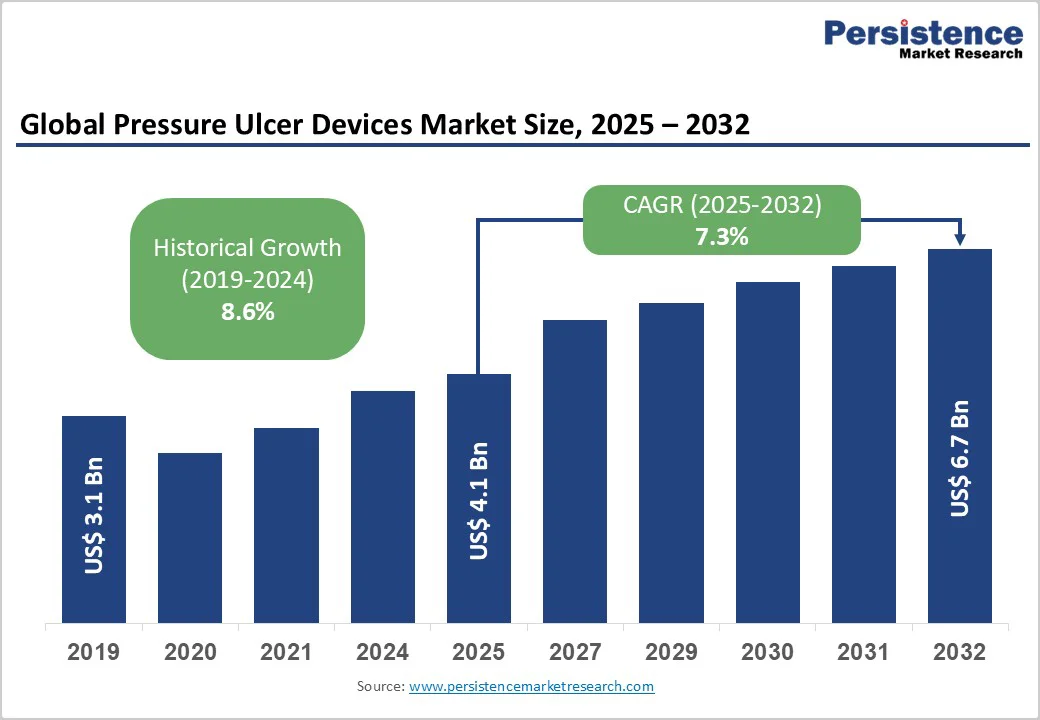

The global pressure ulcer devices market size is likely to be valued at US$4.1 Billion in 2025, and is estimated to reach US$6.7 Billion by 2032, growing at a CAGR of 7.3% during the forecast period 2025−2032, driven by demographic aging, rising chronic disease prevalence, and ongoing innovation in support surfaces and wound care technologies.

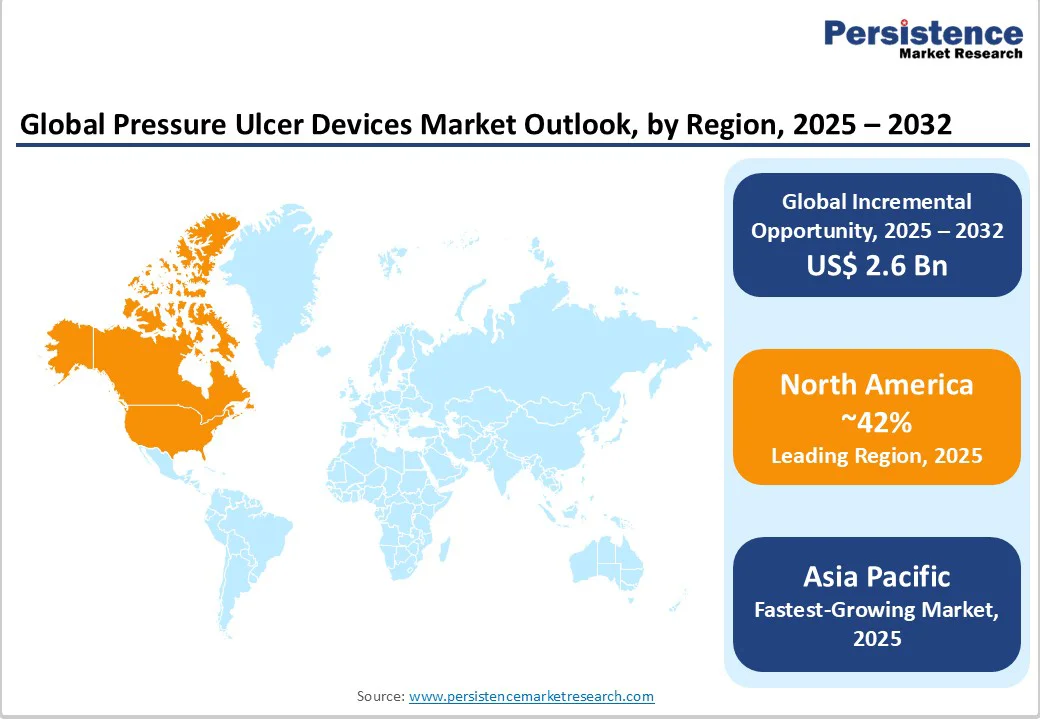

Key growth factors include increased healthcare expenditure, regulatory mandates for pressure ulcer prevention, and the expansion of home healthcare services. Asia Pacific is emerging as the fastest-growing regional market, while North America maintains market leadership due to advanced healthcare infrastructure and robust reimbursement policies.

Key Industry Highlights

- Leading Region: North America leads in 2025 with around 42% of the market share, powered by a strong regulatory environment that prioritizes patient safety and device innovation.

- Fastest-growing Regional Market: Asia Pacific is the fastest-growing regional market from 2025 to 2032, aided by China and India.

- Device Leadership: Smart support surfaces are transforming pressure ulcer prevention, and are expected to command approximately 38% of the market revenue share in 2025.

- Fastest-growing Device Type: Detection devices are set to be the fastest-growing segment through 2032, as a result of an increasing emphasis on early detection and prevention of ulcers and bed sores.

- End-user Dominance: Home healthcare is the fastest-growing end-user segment during 2025-2032 due to aging populations preferring remote health monitoring.

- Key Trend: The shift toward decentralized care and the expansion of home healthcare present significant growth opportunities in emerging markets.

| Key Insights | Details |

|---|---|

|

Pressure Ulcer Devices Market Size (2025E) |

US$4.1 Bn |

|

Market Value Forecast (2032F) |

US$6.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technological Innovation in Smart Support Surfaces

The integration of Internet of Things (IoT), artificial intelligence (AI), and real-time pressure monitoring into support surfaces is transforming pressure ulcer prevention strategies. Smart mattresses and cushions equipped with sensors can detect micro-movements, redistribute pressure automatically, and alert caregivers to potential tissue stress, reducing ulcer incidence in clinical trials.

For example, in December 2024, Lenexa Medical launched LenexaCARE, a smart monitoring system that uses real-time pressure sensors to prevent bedsores in hospitals and aged care facilities, with successful trials in Australia, Singapore, and global expansion plans. These advancements are particularly impactful in hospitals and long-term care settings, where staff shortages and high patient turnover increase the risk of missed preventive interventions. For manufacturers, investing in R&D for sensor-integrated devices offers a significant competitive advantage, with early adopters capturing premium pricing and market share.

Supply Chain Disruptions and Raw Material Price Fluctuations Challenge Market Stability

The pressure ulcer devices market growth faces significant challenges due to supply chain fragility and raw material price volatility. According to a 2025 industry report, over half of advanced pressure ulcer devices rely on specialized polymers, foams, and electronic components sourced from a limited number of suppliers, primarily in Asia and Europe.

The COVID-19 pandemic and recent geopolitical tensions have exposed vulnerabilities in these supply chains, leading to production delays and increased costs. These disruptions not only impact device availability but also erode profit margins, particularly for small and medium-sized enterprises. To mitigate these risks, manufacturers must diversify their supplier base, invest in local production, and develop contingency plans for raw material procurement. Strategic partnerships with logistics providers and the adoption of digital supply chain management tools can enhance resilience and ensure uninterrupted device supply.

Telemedicine and Remote Monitoring Offer Transformative Growth Potential

The integration of telemedicine and remote monitoring technologies into pressure ulcer care presents a transformative opportunity for market expansion. The global telemedicine market is projected to grow at a high CAGR from 2025 to 2032, with remote wound monitoring emerging as a key application. Telemedicine platforms enable real-time assessment of pressure ulcers, remote consultations with specialists, and continuous monitoring of patient progress, reducing the need for in-person visits and improving care outcomes.

For example, the U.S. Department of Health Resources and Services Administration (HRSA) hosted the National Telehealth Conference in July 2024 to devise a pathway for telemedicine-enabled products and services. Companies that develop telemedicine-compatible pressure ulcer devices can capture significant market share and establish a competitive edge in both developed and emerging markets. Strategic partnerships with telemedicine providers and investment in digital health platforms are essential for success in this rapidly evolving landscape.

Category-wise Analysis

Device Type Insights

Static support surfaces, including foam mattresses, gel cushions, and solid padding, are the leading segment in the pressure ulcer devices market, accounting for an estimated 38% of the revenue share in 2025. This segment’s dominance is driven by its affordability, ease of deployment, and proven efficacy in preventing pressure ulcers across diverse care settings. Static support surfaces are widely adopted in hospitals, long-term care facilities, and home healthcare environments, particularly in price-sensitive markets such as Asia Pacific and Latin America, where cost-effective solutions are prioritized over advanced technologies. Key drivers also include ongoing innovation in foam and gel formulations, ergonomic design improvements, and the integration of antimicrobial materials to reduce infection risk. Regulatory standards in North America and Europe mandate the use of pressure-relieving surfaces in acute care settings, further supporting market demand.

Detection devices, including in-shoe sensors, sub-epidermal moisture (SEM) scanners, and pressure mapping systems, are the fastest-growing segment in the market from 2025 to 2032. The segment’s rapid expansion is fueled by increasing emphasis on early detection and prevention, technological advancements, and rising healthcare expenditure. The integration of AI-driven analytics and wireless connectivity, which enhances device effectiveness and enables remote monitoring and telemedicine applications, is emerging as a major growth stimulant. Detection devices offer real-time monitoring of tissue stress, enabling timely interventions and reducing ulcer incidence. These devices are particularly impactful in hospitals and long-term care settings, where staff shortages and high patient turnover increase the risk of missed preventive interventions.

Ulcer Stage Insights

Stage II pressure ulcers, characterized by partial-thickness skin loss, are set to account for an estimated 30% of the pressure ulcer devices market revenue in 2025. This segment’s dominance is driven by the high prevalence of partial-thickness ulcers in both acute and chronic care settings, as well as the availability of advanced wound dressings and therapies specifically designed for this stage. The segment is primarily being propelled by the rising incidence of chronic diseases, such as diabetes and cardiovascular disease, which increase the risk of partial-thickness ulcers. Trends such as the development of advanced wound dressings, including hydrocolloid and hydrogel dressings, are further enhancing healing outcomes and patient comfort and aiding growth.

Deep tissue injury, including unstageable ulcers, is the fastest-growing segment between 2025 and 2032. The segment’s rapid expansion is fueled by the increasing complexity of wound care and the need for advanced diagnostic and therapeutic devices. Two major drivers fueling the growth of this segment are the rising prevalence of chronic diseases and a steadily increasing number of elderly individuals worldwide, as both these factors increase the risk of deep tissue injury. Technological advancements in diagnostic imaging and therapeutic devices are markedly improving the ability to detect and treat deep tissue injuries. The development of bioengineered tissue substitutes and advanced wound therapy devices is creating new and long-term high-value opportunities for manufacturers.

End-user Insights

Hospitals are the dominant end-user segment, likely to account for an estimated 40% of the market revenue in 2025. This segment’s dominance is driven by the high prevalence of pressure ulcers in acute care settings, stringent regulatory standards, and robust reimbursement policies. Hospitals benefit from advanced healthcare infrastructure, a well-established supply chain, and a broad distribution network, enabling rapid market penetration. The growing adoption of smart devices and AI-enabled monitoring solutions at these facilities for elevating patient outcomes is favoring the continued expansion of this segment. To maintain market leadership, manufacturers must focus on product innovation, such as enhanced durability, ease of application, and cost-effective solutions for hospitals, especially in developing economies.

Home healthcare is the fastest-growing end-user segment during 2025-2032, fueled by the shift toward decentralized care, rising disposable incomes, and government initiatives to improve home healthcare infrastructure. The development and acceptance of portable and user-friendly devices are proving critical in ensuring a high level of patient comfort and compliance in home care. The segment also benefits from government initiatives to subsidize advanced wound care devices and expand home healthcare services, creating significant opportunities for manufacturers. To capture market share, companies must focus on engineering easy-to-use devices tailored to home healthcare settings.

Regional Insights

North America Pressure Ulcer Devices Market Trends

North America maintains a leading position in 2025, holding approximately 42% of the pressure ulcer devices market share. The unmatched position of the region is founded on a combination of advanced healthcare infrastructure, high healthcare expenditure, and a strong regulatory environment that prioritizes patient safety and device innovation.

The prevalence of chronic diseases and an aging population are significant factors driving demand for both preventive and therapeutic devices. Strict regulatory standards, such as those enforced by the U.S. Food and Drug Administration (FDA), ensure rapid adoption of new technologies and facilitate the entry of innovative products into the market. The region’s leadership is further reinforced by the presence of major medical device manufacturers, such as 3M and Hill-Rom, and a robust ecosystem for research and development. Investment in digital health platforms and telemedicine is creating new opportunities for market expansion, particularly in home healthcare and remote monitoring.

Europe Pressure Ulcer Devices Market Trends

Europe represents about 28% of the market in 2025, supported by aggressive regulatory harmonization under the European Union (EU)’s Medical Device Regulation (MDR), which streamlines device approval and fosters innovation. Advanced healthcare systems, rising healthcare expenditure, and government initiatives to improve wound care standards are key drivers. A large elderly population and increasing prevalence of chronic diseases are fueling the demand for pressure ulcer prevention and treatment solutions.

The competitive landscape of the market here is moderately fragmented, with a mix of global and regional players. Investment is increasingly directed toward cost-effective devices and home healthcare solutions, with telemedicine and remote monitoring emerging as major growth areas. The European Commission’s funding for telemedicine and remote wound monitoring devices through programs such as Horizon Europe EU4Health is catalyzing market expansion and innovation, creating a favorable environment for both established and novice companies.

Asia Pacific Pressure Ulcer Devices Market Trends

Asia Pacific is the fastest-growing regional market for pressure ulcer devices from 2025 to 2032. The regional market growth is driven by manufacturing strengths, rising disposable incomes, and government initiatives to improve healthcare infrastructure in India, China, and ASEAN countries. An aging population and growing incidence of chronic diseases are the prime market movers, along with the expansion of home healthcare services.

The competitive landscape is highly fragmented, with a mix of global and local players. Investment is focused on developing affordable, user-friendly devices and telemedicine solutions, with notable opportunities in rural healthcare and underserved areas. Government programs aimed at expanding home healthcare and subsidizing advanced wound care devices are further supporting regional growth. The region’s manufacturing base and proximity to emerging markets enhance its competitive edge, making it a key area for market expansion and innovation.

Competitive Landscape

The global pressure ulcer devices market structure is moderately consolidated, with the top five players accounting for approximately 45% of the market share in 2025. Leading companies include 3M Company, Hill-Rom Holdings, Inc., ArjoHuntleigh, Medline Industries, LP, and Stryker Corporation. The market is characterized by intense competition, with a mix of global and regional players.

Competitive positioning is driven by technological innovation, product differentiation, and strategic partnerships. Companies that are investing in R&D for developing smart devices and AI-enabled solutions are well-positioned to capture premium pricing and market share. The market is also witnessing increased consolidation, with mergers and acquisitions driving innovation and cost synergies.

Key Industry Developments

- In November 2025, Orpyx Medical Technologies’ digital foot-monitoring platform was chosen for a US$5 Million NIH-funded trial at Johns Hopkins. The WIREDUP study, enrolling 400 participants, will assess whether digital monitoring reduces diabetic foot ulcers and amputation risk, highlighting the growing role of wearable sensors in proactive chronic disease care.

- In August 2025, UCLA engineers developed an alternating-pressure mattress that prevents bedsores by cyclically shifting pressure across the body. Using a lattice of sensors and compliant mechanisms, it redistributes pressure based on individual needs. Tests show it improves blood flow, minimizes prolonged pressure, and significantly reduces pressure ulcer risk.

- In May 2025, Tidewave Medical launched Tidewave, the first continuous movement system for pressure ulcer prevention. The mattress automatically repositions patients, easing pressure on care teams and enhancing comfort. Designed for hospitals and long-term care, it supports the prevention and healing of ulcers and is now available in the U.K. and globally recognized.

Companies Covered in Pressure Ulcer Devices Market

- 3M Company

- Hill-Rom Holdings, Inc.

- Arjo AB

- Medline Industries, LP

- Stryker Corporation

- Smith & Nephew plc

- Mölnlycke Health Care AB

- ConvaTec Group plc

- Paul Hartmann AG

- Essity AB

- BSN Medical GmbH

- Medtronic plc

- B. Braun Melsungen AG

- Cardinal Health, Inc.

- Baxter International Inc.

Frequently Asked Questions

The global pressure ulcer devices market is projected to reach US$4.1 Billion in 2025.

Aging populations, rising chronic disease prevalence globally, and ongoing innovation in support surfaces and wound care technologies are driving the market.

The pressure ulcer devices market is poised to witness a CAGR of 7.3% from 2025 to 2032.

Increased healthcare expenditure, regulatory mandates for pressure ulcer prevention, and the expansion of home healthcare services are key market opportunities.

3M Company, Hill-Rom Holdings, Inc., Arjo AB, and Medline Industries, LP are some of the top players in the pressure ulcer devices market.