- Industrial Machinery

- Pressure Relief Valves for Water and Wastewater Treatment Market

Pressure Relief Valves for Water and Wastewater Treatment Market Size, Share, Trends, Growth, Regional Forecasts from 2026 to 2033

Pressure Relief Valves for Water and Wastewater Treatment Market by Product (Spring Loaded, Pilot-operated, Dead Weight, P&T Actuated), Set Pressure (Low, Medium, High), End-user (Municipal Water Treatment Plants, Municipal Wastewater Treatment Plants, Industrial Wastewater Treatment Facilities, Others), and Regional Analysis 2026 - 2033

Pressure Relief Valves for Water and Wastewater Treatment Market Share and Trends Analysis

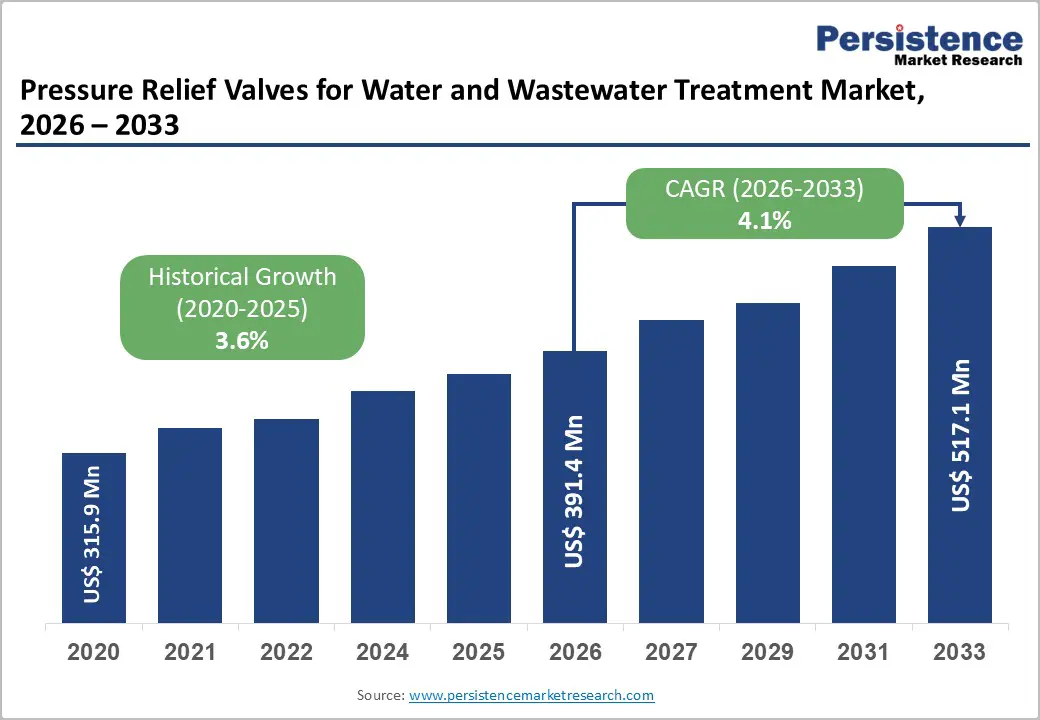

The global pressure relief valves for water and wastewater treatment market size is projected to grow from US$391.4 million in 2026 to US$517.1 million by 2033, growing at a CAGR of 4.6% during the forecast period from 2026 to 2033.

The market growth is driven by rising investments in municipal and industrial wastewater infrastructure. Increasingly stringent environmental regulations across major economies continue to accelerate market adoption. Advancements in IoT-enabled smart valve systems are improving efficiency, monitoring accuracy, and operational safety. Urbanization, water scarcity, and the shift toward circular water management further strengthen demand for reliable pressure protection solutions.

Key Industry Highlights:

- Product Segment Leadership and Growth Dynamics: Spring-loaded valves lead with a 38% share, while pilot-operated systems grow fastest, at a 5.2% CAGR, driven by their precision and suitability for complex industrial applications.

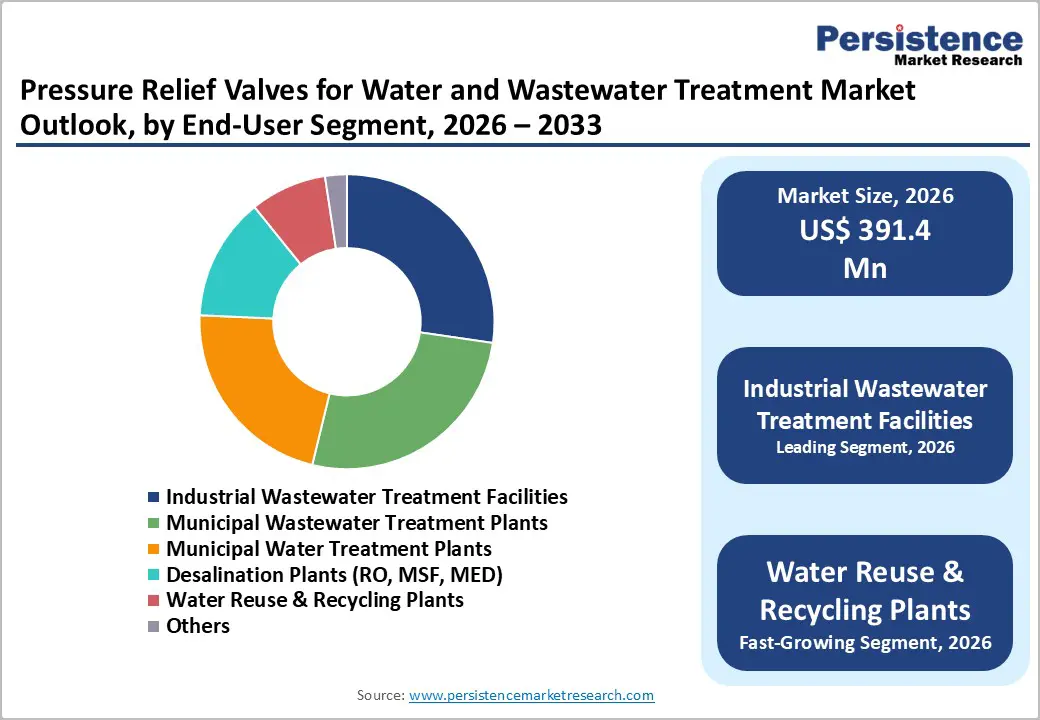

- End-user Demand Drivers: Industrial wastewater facilities hold 27% share, while water reuse and recycling plants grow at 2.4% CAGR, driven by circular water economy priorities.

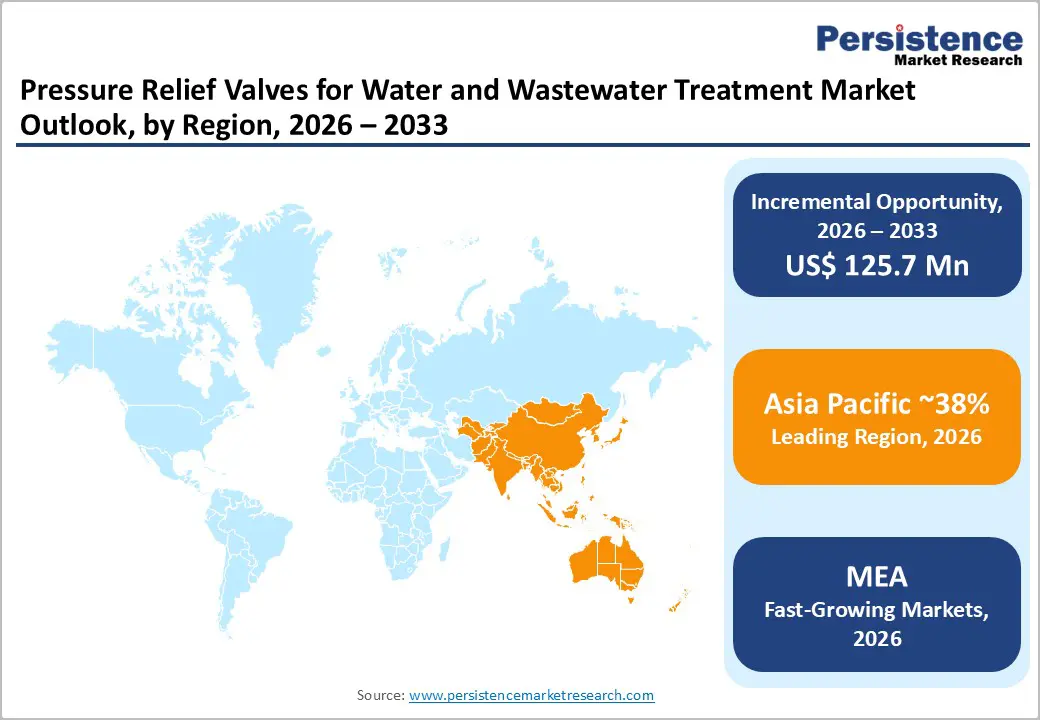

- Regional Market Leadership: Asia Pacific leads with a 38% share and a 4.6% CAGR, driven by China’s large-scale water treatment expansion and growing desalination infrastructure.

- Technology and Innovation Drivers: IoT-enabled smart valves and predictive maintenance technologies are key drivers of innovation, improving efficiency, uptime, and compliance in treatment facilities.

- Strategic Market Evolution: The market is evolving toward value-added service models, with manufacturers increasingly offering integrated monitoring and predictive maintenance solutions over standalone components.

| Key Insights | Details |

|---|---|

| Pressure Relief Valves for Water and Wastewater Treatment Market Size (2026E) | US$ 391.4 million |

| Market Value Forecast (2033F) | US$ 517.1 million |

| Projected Growth CAGR (2026 - 2033) | 4.1% |

| Historical Market Growth (2020 - 2025) | 3.6% |

Market Dynamics Analysis

Drivers - Accelerating Urbanization and Water Infrastructure Investment

Global urbanization rates are intensifying demand for robust water and wastewater infrastructure, particularly in the Asia Pacific and Latin American regions experiencing rapid population growth. China's water treatment sector expanded to RMB 1.1 trillion (approximately US$150 billion) in 2024, growing at ~17.7% annually, with the government allocating RMB 26 billion to water pollution control initiatives. The European Investment Bank committed US$191 million for water infrastructure upgrades in India's Uttarakhand state, targeting benefits for approximately 900,000 people through enhanced distribution networks and automated treatment systems. U.S. municipal capital expenditure projections indicate US$515.4 billion in cumulative infrastructure investment through 2035, with wastewater representing 58% of total spend, growing at 4.18% annually. These substantial infrastructure commitments necessitate reliable pressure management solutions, positioning pressure relief valves as essential components in new treatment facility construction and legacy system modernization projects.

Technological Innovation in Smart Water Systems and IoT Integration

The integration of Internet of Things (IoT) technology and artificial intelligence into water treatment infrastructure is fundamentally transforming operational paradigms and creating differentiated demand for advanced pressure relief valves. Smart valve systems enable real-time monitoring of pressure fluctuations, predictive maintenance algorithms that identify component failure risks before occurrence, and remote operational control capabilities across distributed treatment networks. IoT-enabled pressure relief valves reduce system downtime through automated leak detection and pressure optimization, yielding quantified benefits, including a 30-50% reduction in combined water-sewer service costs and a 15% reduction in energy consumption in optimized desalination operations.

Chinese water treatment operators and municipal authorities are increasingly partnering with global technology providers to co-develop IoT-integrated water networks and automated monitoring systems, while facilities worldwide adopt sensor-based pressure management to comply with emerging energy efficiency standards, particularly the EU's 2045 energy neutrality requirement for treatment plants.

Restraints - High Capital Investment Requirements and Operational Complexity

Pressure relief valve systems represent significant capital expenditures for municipal and industrial operators, particularly in resource-constrained developing regions where treatment facility budgets compete with complementary infrastructure priorities. Advanced pilot-operated relief valves, required for complex pressure scenarios in large-scale industrial applications, command substantially higher price points than spring-loaded alternatives due to increased complexity, precision manufacturing tolerances, and specialized maintenance requirements. Smaller municipal utilities serving populations under 25,000 frequently lack internal technical capacity for advanced valve installation and maintenance, requiring external expertise and extending project timelines. This capital intensity creates implementation barriers for treatment facilities in lower-income jurisdictions, potentially constraining market penetration in price-sensitive emerging markets despite strong environmental compliance mandates.

Supply Chain Vulnerabilities and Manufacturing Concentration

The global pressure relief valve manufacturing sector exhibits substantial concentration risk, with the four largest operators accounting for approximately 20% of total industry revenue. Sourcing dependencies on specialized materials, precision machining capabilities, and electronic components exposes the supply chain to geopolitical disruptions and commodity price volatility. Regional manufacturing capacities remain unevenly distributed, with established facilities concentrated in developed economies, creating logistics constraints and lead-time risks for operators in remote or developing regions. Recent supply chain disruptions have extended project timelines for treatment facility upgrades, constraining near-term market growth and potentially incentivizing delays in capital allocation among cost-conscious municipal authorities.

Opportunities - Water Reuse and Recycling Infrastructure Expansion

The global water reuse and recycling infrastructure is experiencing substantial growth, expanding at 10.5% CAGR. This expansion is driven by acute water scarcity, regulatory mandates, including Saudi Arabia's Vision 2030, which targets 70% recycling and a 43% demand reduction, and industrial adoption of zero-liquid discharge strategies in manufacturing operations. Advanced pressure relief systems are critical enablers for water recycling facilities, managing pressure differentials across multiple treatment stages, including reverse osmosis (RO), ultrafiltration (UF), and membrane bioreactor (MBR) technologies. Building-scale reuse installations generate 30-50% savings on combined water-sewer utility costs, creating financial incentives for facility operators to implement comprehensive recycling infrastructure where pressure management components directly influence operational efficiency and system reliability.

Desalination Plant Development and Technology Integration

The global water desalination equipment market is witnessing significant growth, driven by rising water scarcity, industrial demand, and rapid adoption of reverse osmosis technology, which accounts for 68% of total installations. The Middle East and Africa Water Desalination Equipment Market alone is valued at US$5.1 billion in 2025, representing 45-50% of global demand owing to the region’s heavy dependence on non-conventional water sources. Desalination capacity additions in the Asia Pacific, particularly in China, India, Australia, and Southeast Asia, are accelerating due to intensifying water stress and government strategic initiatives. Pressure relief valves are integral to desalination operations, managing pressure differentials across membrane systems where reverse osmosis processes operate at 250-1000 PSI, requiring sophisticated pressure control to balance efficiency, membrane longevity, and system safety. The Hong Kong Tseung Kwan O desalination plant, which commenced operations in February 2024, utilizing advanced RO technology, exemplifies infrastructure expansion, creating sustained demand for precision pressure management components across the Asia Pacific region.

Category-wise Analysis

Product Type Insights

The pressure relief valve segment shows varied growth tied to operational needs and application complexity. Spring-loaded valves hold a dominant 38% share due to cost-efficiency, mechanical simplicity, and rapid response suited for municipal systems. They require minimal maintenance, operate without inlet-outlet pressure differentials, and respond about 100 milliseconds faster than alternatives, making them preferred where installation and lifecycle cost priorities drive selection. Pilot-operated valves, though smaller in share, are the fastest-growing, with a 5.2% CAGR, supported by industrial wastewater applications that require higher pressure accuracy and greater flow capability. With pressure offsets of only 1-5% versus 20-40% for spring-loaded types, they deliver precise control and efficiency essential for pharmaceutical, chemical, and petrochemical treatment facilities across diverse industrial and municipal applications worldwide today.

Set Pressure Insights

Low-pressure relief valves dominate with 47% share, serving municipal water treatment applications and low-pressure industrial processes where operational parameters typically range from 0-150 PSI. Municipal treatment facilities, reverse osmosis pretreatment systems, and general-purpose wastewater applications prefer low-pressure configurations for cost efficiency and mechanical simplicity. The high-pressure segment, despite a smaller current market share, emerges as the fastest-growing category, expanding at 5.1% CAGR, reflecting intensifying industrial adoption of advanced technologies, including reverse osmosis desalination, membrane bioreactors, and ultrafiltration systems operating at elevated pressure differentials of 250-1000 PSI. Industrial wastewater treatment facilities increasingly implement membrane filtration technologies that require high-pressure relief systems, particularly in the petrochemical, pharmaceutical, and textile manufacturing sectors, where wastewater complexity necessitates advanced treatment methods.

End-user Insights

Industrial wastewater treatment facilities command a dominant 27% share, encompassing food and beverage processing, chemical and petrochemical effluent management, pharmaceutical wastewater systems, pulp and paper operations, and textile dyeing industries. These facilities generate high-complexity waste streams that require sophisticated pressure management systems to protect membrane filtration, chemical treatment equipment, and conveyance infrastructure from overpressure. Water reuse and recycling plants represent the fastest-growing end-user segment, expanding at a 2.4% CAGR, reflecting global prioritization of circular water economy development and industrial adoption of zero-liquid discharge strategies. Desalination facilities, municipal water treatment plants, and municipal wastewater systems collectively represent the remaining market demand, with regulatory mandates driving sustained investment in both municipal infrastructure upgrades and emerging industrial reuse applications.

Regional Market Insights

North America Pressure Relief Valves for Water & Wastewater Treatment Market Trends

North America commands approximately 23% of global market share, with the United States representing the primary demand center driven by EPA regulatory enforcement and substantial municipal capital allocation for infrastructure modernization. U.S. municipal water and wastewater treatment capital expenditure is projected to reach US$57.3 billion annually by 2035 from current US$37.2 billion levels, with particular concentration in southern states, including Texas and Florida, experiencing rapid suburban expansion and intensifying water stress. The region benefits from established manufacturing infrastructure, sophisticated regulatory compliance frameworks, and substantial investment in digital transformation for utility operations, positioning North American treatment facilities at the forefront of smart water technology adoption and IoT-enabled pressure management system deployment.

The pressure relief valve segment shows distinct growth patterns. Spring-loaded valves lead with a 38% share, driven by cost-efficiency, simplicity, and rapid response, making them ideal for municipal systems. Pilot-operated valves grow at the fastest 5.2% CAGR, valued in industrial wastewater treatment for superior pressure accuracy, minimal offset, and higher flow capability, essential for chemical, pharmaceutical, and petrochemical applications across complex treatment plant operations.

Europe Pressure Relief Valves for Water & Wastewater Treatment Market Analysis

Europe maintains a considerable 22% global market share while expanding at 3.2% CAGR, driven by the implementation of the revised Urban Wastewater Directive and harmonized environmental standards across EU member states. Germany leads European demand through its engineering-intensive municipal infrastructure modernization programs and strong chemical manufacturing sector, requiring sophisticated pressure management in industrial wastewater applications. The United Kingdom, France, and Spain are advancing water recycling initiatives aligned with EU circular economy frameworks, creating demand for specialized pressure relief components compatible with advanced treatment technologies. The region's emphasis on sustainability and energy efficiency is accelerating the adoption of IoT-enabled valve systems that optimize pressure profiles across treatment sequences and enable predictive maintenance aligned with energy neutrality mandates.

European treatment facilities favor locally manufactured components from German, Swedish, and Swiss valve specialists due to technical expertise and strong regional support. EU-wide regulatory harmonization strengthens demand for suppliers with European manufacturing certification. Rising attention to PFAS and micropollutants accelerates the adoption of advanced membrane systems requiring precise pressure control, positioning Europe as a leader in next-generation valve technology deployment.

Asia Pacific Pressure Relief Valves for Water & Wastewater Treatment Market Analysis

Asia Pacific leads globally with a 38% market share and is expanding at a 4.6% CAGR, reflecting the region's rapid industrialization, accelerating urbanization, and intensifying water scarcity. China dominates Asia Pacific demand, with its water treatment sector expanding to RMB 1.1 trillion in 2024 and government policy prioritizing 95% wastewater treatment rates in county-level cities and 25% water reuse rates in water-scarce regions under the 14th Five-Year Plan. Large-scale desalination infrastructure expansion in coastal provinces, including Shandong, Tianjin, and Guangdong is driving sustained demand for pressure relief components compatible with reverse osmosis and hybrid desalination technologies. India's wastewater treatment market is expanding at a 10% CAGR, with EIB financing of US$191 million for Uttarakhand water infrastructure modernization exemplifying a broader South Asian infrastructure development trajectory that supports municipal and industrial treatment facility investment.

Japan and Australia leverage mature RO-based desalination supported by advanced pressure management, while Singapore and Southeast Asia expand desalination and recycling to strengthen water security. Strong regional manufacturing reduces logistics burdens and enhances supply resilience. Growing adoption of IoT-enabled smart water systems accelerates demand for high-precision, automation-ready pressure relief valves across Asian treatment facilities and ensures operational reliability overall consistently.

Competitive Landscape

The global pressure relief valve market for water and wastewater treatment is moderately fragmented, with global leaders Parker Hannifin, Emerson, and Flowserve holding strong share, while KSB and Alfa Laval dominate Europe, and CIRCOR, Danfoss, and Honeywell lead specialized niches. Consolidation is rising through acquisitions, with competition shifting toward IoT-enabled smart valves, advanced materials, and integrated monitoring capabilities.

Strategic Developments:

- In August 2025, CIRCOR agreed to acquire Swelore Engineering and Hiro Nisha Systems, strengthening its portfolio with advanced pressure control and relief technologies essential for wastewater dosing applications.

- In 2024, Yokogawa launched its OpreX Water Loss Management System featuring a Pressure Management Function that optimizes PRV settings to reduce non-revenue water by up to 50% while maintaining distribution network reliability.

- In October 2022, Flowserve introduced the FLEX® Isobaric Energy Recovery Device, a next-generation compact pressure exchanger delivering over 98% hydraulic energy recovery and up to 60% energy savings in RO desalination systems with integrated overpressure protection.

Companies Covered in Pressure Relief Valves for Water and Wastewater Treatment Market

- Parker Hannifin Corporation

- Emerson Electric Company

- Flowserve Corporation

- CIRCOR International

- KSB AG

- Alfa Laval Corporate AB

- Danfoss

- Honeywell International

- Crane Holdings Company

- Swagelok Company

- ASCO Numatics

- IMI Precision Engineering

- Yokogawa Electric Corporation

- LESER GmbH

- Schneider Electric

Frequently Asked Questions

The global pressure relief valves for water and wastewater treatment market is valued at US$391.4 million in 2026 and is expected to reach US$517.1 million by 2033.

Market growth is driven by stricter environmental regulations, expanding municipal and industrial wastewater infrastructure, rapid urbanization, and rising adoption of IoT-enabled smart valve technologies enhancing monitoring, efficiency, and compliance.

The pressure relief valves for water and wastewater treatment market is projected to grow at a CAGR of 4.06% from 2026 to 2033.

Key opportunities arise from water reuse expansion, desalination growth in APAC and the Middle East, renewable-integrated treatment facilities, and zero-liquid discharge initiatives requiring advanced pressure management solutions.

Key global players include Parker Hannifin, Emerson Electric, Flowserve, KSB Group, Alfa Laval, and Danfoss, supported by a mix of global leaders and regional specialists emphasizing IoT integration, durability, and automation compatibility.