- Sensors & Controls

- Piezoresistive Pressure Sensor Market

Piezoresistive Pressure Sensor Market Size, Share, and Growth Forecast, 2026 – 2033

Piezoresistive Pressure Sensor Market by Sensor Type (Absolute, Gauge, Differential, Sealed), Pressure Range (Low Pressure (<10 kPa), Medium Pressure (10 kPa – 1000 kPa), High Pressure (>1000 kPa)), End-Use Industry (Automotive & Transportation, Industrial Manufacturing, Healthcare, Aerospace & Defense, Electronics) and Regional Analysis for 2026-2033

Piezoresistive Pressure Sensor Market Share and Trends Analysis

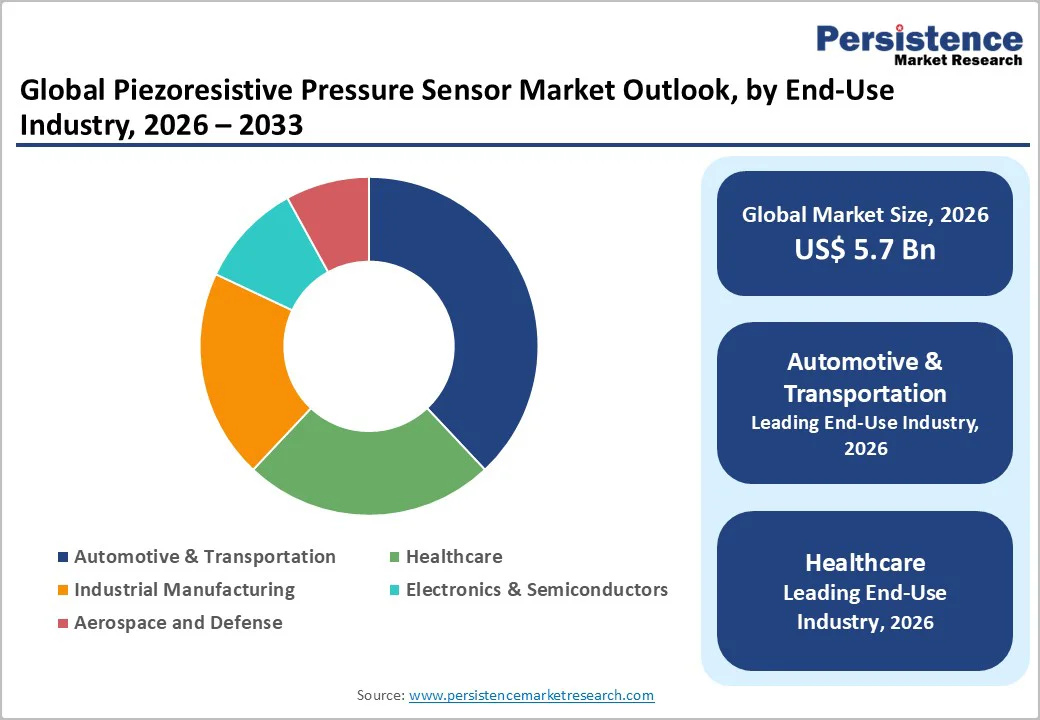

The global piezoresistive pressure sensor market size is likely to be valued at US$ 5.7 billion in 2026, and is projected to reach US$ 7.7 billion by 2033, growing at a CAGR of 4.4% during the forecast period 2026-2033. This growth is supported by the steadily rising integration of pressure-sensing components in automotive safety systems, industrial process monitoring, and medical instrumentation. Increasing regulatory emphasis on emissions measurement, workplace safety, and healthcare device precision further drives adoption. The expansion of semiconductor-based micro-electro-mechanical system (MEMS) manufacturing capacity further enhances supply stability and lowers unit costs, reinforcing broader end-use penetration.

Key Industry Highlights

- Leading Sensor Type: Absolute pressure sensors are expected to hold around 48% of the market in 2026, driven by their broad industrial and automotive use.

- Dominant Pressure Range: Medium-pressure sensors are projected to account for approximately 52% revenue share in 2026, supported by their widespread use in automotive and industrial equipment.

- Leading End-Use Industry: The automotive sector is expected to capture about 38% of the market revenue in 2026, reflecting its reliance on manifold, fuel, and tire pressure sensing.

- Fastest-growing End-Use Industry: Healthcare is forecasted to grow the fastest at about 10% CAGR through 2033, owing to the digitalization of medical devices.

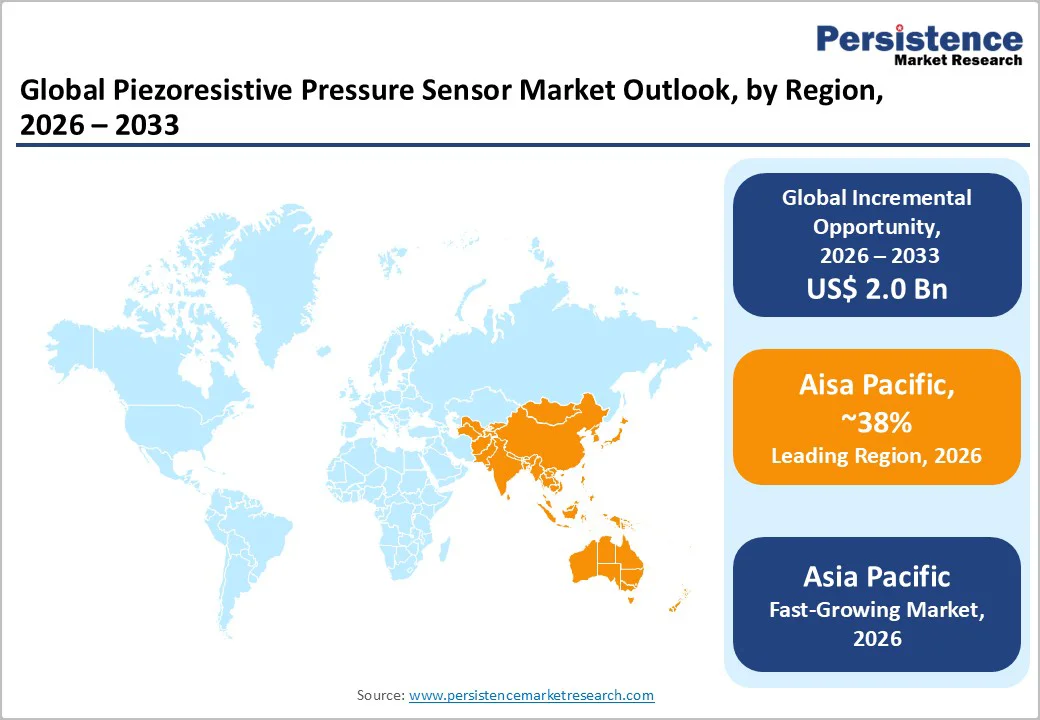

- Regional Dominance: Asia Pacific is anticipated to dominate with approximately 38% market share in 2026, supported by large-scale electronics and automotive production.

- Key Driver: Growing demand for advanced pressure monitoring technologies across automotive, medical, aerospace, and industrial applications is driving overall market growth.

| Key Insights | Details |

|---|---|

| Piezoelectric Pressure Sensor Market Size (2026E) | US$ 5.7 Bn |

| Market Value Forecast (2033F) | US$ 7.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Use of Advanced Pressure Monitoring across Sectors

The piezoresistive sensor market benefits from converging demand across three critical application domains. Automotive powertrains, industrial automation systems, and emerging mobility platforms increasingly require accurate pressure monitoring to satisfy stringent safety regulations, operational efficiency targets, and emissions compliance standards. Simultaneously, healthcare infrastructure modernization is driving sensor deployment across clinical environments, where ventilators, infusion pumps, and patient monitoring devices demand reliable pressure measurement capabilities. This dual-sector momentum reflects a fundamental shift toward precision engineering across both established and emerging industries.

Piezoresistive MEMS technology addresses these market imperatives through its distinctive technical advantages. The combination of high measurement accuracy, exceptional signal stability, and miniaturized form factor enables seamless integration into next-generation automotive systems, industrial machinery, and portable medical devices. By delivering consistent performance across diverse operating conditions, piezoresistive MEMS sensors have become essential components for manufacturers seeking to balance performance requirements with design constraints. This technological foundation positions piezoresistive sensors as foundational enablers in the ongoing evolution of connected, efficient, and intelligent systems across transportation, manufacturing, and healthcare sectors.

Supply Chain Vulnerabilities and Performance Maintenance Requirements

Supply chain volatility continues to challenge the piezoresistive sensor market growth, with semiconductor shortages and regional manufacturing bottlenecks affecting component availability. Disruptions in material supply and logistics often result in increased production costs and unpredictable delivery timelines. These constraints are particularly pronounced in regions with limited fabrication capacity, where manufacturers struggle to maintain consistent output and meet growing demand. As a result, both producers and customers face higher expenses and operational uncertainty, which can hinder the broader adoption of piezoresistive sensors.

In addition to supply chain issues, piezoresistive sensors require regular calibration to ensure measurement accuracy in varying environmental conditions. Exposure to temperature shifts, humidity, or chemically aggressive settings can degrade sensor performance over time, necessitating ongoing maintenance. This need for periodic recalibration adds to the total cost of ownership, making piezoresistive sensors less competitive in cost-sensitive markets. In such applications, simpler or lower-maintenance sensing technologies may offer a more economical solution, limiting the market reach of piezoresistive devices despite their technical advantages.

Expansion of Pressure Sensor Applications in Smart Industries and Healthcare

Smart manufacturing, advanced mobility solutions, and healthcare innovation are converging to generate substantial growth opportunities for piezoresistive pressure sensors. Industrial facilities are rapidly deploying automation technologies, real-time monitoring systems, and energy management solutions that depend on precise pressure measurement for operational efficiency and predictive maintenance capabilities. Concurrently, the transition to electric and hydrogen vehicles introduces new sensor requirements, including battery thermal management, fuel-cell performance monitoring, and brake-by-wire system integration. These technological shifts demand sensors capable of delivering reliable data under demanding conditions.

Healthcare applications are similarly driving sensor adoption through the proliferation of compact medical devices, distributed care models, and remote diagnostic platforms. Miniaturized, energy-efficient sensors with high measurement accuracy are essential for respiratory monitors, infusion delivery systems, and wearable health tracking devices. The intersection of industrial automation, advanced transportation, and healthcare delivery has created a robust demand foundation that spans high-value applications requiring both technical sophistication and operational reliability. This multi-sector expansion establishes piezoresistive sensors as critical infrastructure components supporting the next generation of connected, autonomous, and patient-centric systems.

Category-wise Analysis

Sensor Type Insights

Absolute sensors are set to control about 48% of the piezoresistive pressure sensor market revenue share in 2026, reflecting their ability to measure pressure relative to a perfect vacuum for dependable performance across demanding use cases. Their role in automotive engine control, industrial vacuum systems, and environmental monitoring remains central, as these applications prioritize high precision and stability to protect assets and ensure compliance. Precision, reliability, and compatibility with MEMS fabrication enable scalable, high-volume production while maintaining tight tolerances. To capture sustained demand, suppliers should emphasize calibrated modules, contamination?resistant packaging, and reference designs that speed qualification in automotive, semiconductor, and instrumentation programs.

Differential sensors are likely to expand the fastest from 2026 to 2033, as heating, ventilation, and air conditioning (HVAC) systems, filtration equipment, medical devices, and smart infrastructure increasingly require granular pressure data to improve diagnostics and control. By measuring the difference between two pressure points, these devices enable early fault detection, energy optimization, and safer operation across facilities and clinical workflows. The 2025 launch of customized differential sensors for Triatek’s EcoAir Valve highlights adoption in smart building deployments that target indoor air quality (IAQ) improvements and predictive maintenance in industrial and commercial environments. Vendors can accelerate penetration by offering configurable ranges, digital interfaces, and application?specific calibration profiles that integrate seamlessly with building automation platforms and medical device architectures.

Pressure Range Insights

Medium-pressure sensors, operating between 10 and 1,000 kilopascals (kPa), are projected to lead the market, capturing an estimated 52% revenue share in 2026. This dominance reflects their versatility across core automotive, industrial, and healthcare applications, including systems such as fuel injection, hydraulic controls, industrial pumps, and medical monitoring equipment. Original equipment manufacturers (OEMs) prefer these sensors for their stable and reliable performance within moderate pressure ranges. The broad, established deployment of these components in conventional machinery and industrial equipment ensures sustained demand, underscoring the importance of supply chain resilience and strong OEM partnerships for market leaders.

High-pressure sensors, designed for applications exceeding 1,000 kPa, are anticipated to register the highest CAGR during the 2026-2033 forecast period, driven by advancements in the aerospace, energy, and hydrogen mobility sectors. These sensors are essential for safely and efficiently monitoring turbines, fuel cells, and industrial reactors that operate under extreme environmental conditions. The introduction of hydrogen-rated pressure sensors by companies such as Baker Hughes for electrolysis and refueling stations exemplifies this trend. This expanding adoption in alternative energy and other high-stakes industrial environments signals a critical opportunity for specialized manufacturers to innovate and capture value.

End-Use Industry Insights

The automotive sector is predicted to command over 38% market share in 2026, fueled by widespread deployment of powertrain sensors in engine management, braking systems, and exhaust after-treatment processes. Strict emissions and safety standards compel manufacturers to integrate these components for regulatory compliance and performance optimization. Innovations such as Bosch’s SMP290 tire pressure monitoring system (TPMS) sensor, which incorporates Bluetooth low energy (BLE) connectivity, demonstrate progress toward greater precision, energy savings, and data integration. Electric and autonomous vehicle architectures amplify this momentum, creating opportunities for suppliers to prioritize scalable, connected solutions that enhance vehicle reliability and efficiency.

Healthcare is poised to emerge as the fastest-growing end-use vertical between 2026 and 2033, powered by the surging demand for pressure sensors for operating ventilators, infusion pumps, and wearable monitors. Engineers emphasize miniaturization, low power consumption, and biocompatibility to meet device requirements. Advances in flexible pressure sensors enable home care and remote monitoring, responding to aging populations and chronic conditions. Manufacturers can leverage this trajectory by developing customizable, biocompatible modules that streamline integration into portable diagnostics, ultimately reducing healthcare delivery costs while improving patient outcomes.

Regional Insights

North America Piezoresistive Pressure Sensor Market Trends

North America is anticipated to capture approximately 32% of the piezoresistive pressure sensor market share in 2026, with the United States anchoring regional demand through automotive electrification, industrial automation, and advanced medical device manufacturing. Aerospace applications continue to require high-pressure and differential sensors for engine monitoring, turbine performance assessment, and altitude control systems. Regulatory frameworks, including the Federal Motor Vehicle Safety Standards (FMVSS), Environmental Protection Agency (EPA) emissions mandates, and Food and Drug Administration (FDA) medical device standards, sustain demand for sensors that deliver high precision and proven reliability through 2033. This regulatory environment creates barriers to entry while rewarding manufacturers that invest in compliance-ready platforms and validated reference designs.

Growth momentum also stems from multiple converging trends that deepen sensor penetration across key industries. Connected mobility and electric vehicle (EV) adoption drive requirements for high-accuracy components in battery thermal management, brake-by-wire architectures, and TPMS. Industrial digitalization, characterized by predictive maintenance programs and smart factory deployment, expands medium-pressure and high-pressure sensor integration into automated production lines and process control systems. Healthcare infrastructure modernization, encompassing advanced patient monitoring and next-generation ventilator platforms, further amplifies regional consumption. These drivers collectively position North America as an innovation-focused market with steady, multi-sector expansion, offering vendors opportunities to differentiate through connectivity features, edge analytics integration, and sector-specific calibration protocols that reduce total cost of ownership for end users.

Europe Piezoresistive Pressure Sensor Market Trends

Europe is forecasted to secure around 28% of the piezoresistive pressure sensor market revenues in 2026. Germany, the United Kingdom, France, and Spain are best positioned economically to lead regional consumption. Harmonized regulatory frameworks, including the European Union Medical Device Regulation (EU MDR), Euro 6/7 emissions standards, and International Electrotechnical Commission (IEC) standards, will accelerate advanced sensing adoption across sectors such as automotive, industrial, aerospace, and healthcare. Germany's automotive and aerospace supply chains will remain major consumers of medium-pressure and high-pressure sensors. Investments in hydrogen mobility and renewable energy infrastructure will sustain specialized high-pressure applications through 2033.

Regional expansion will originate primarily from hydrogen fuel-cell vehicle adoption and refueling infrastructure expansion, which will increase demand for high-pressure devices. Industrial digitalization and smart factory upgrades will raise the deployment of differential and absolute sensors for process optimization and predictive maintenance. MEMS miniaturization and healthcare modernization will enable sensor integration into medical equipment. These combined trends indicate steady growth in Europe's high-precision pressure sensor sector throughout the forecast period.

Asia Pacific Piezoresistive Pressure Sensor Market Trends

Asia Pacific is likely to secure approximately 38% of the global market sales in 2026, solidifying its status as the dominant region. China will spearhead adoption across automotive production, industrial automation platforms, and consumer electronics assembly. Cost-effective semiconductor fabrication facilities and resilient supply chains bolster this leadership. India and ASEAN countries will contribute through precision automotive components, medical electronics manufacturing, and industrial upgrades. Rapid demand for medium-pressure and high-pressure sensors in manufacturing hubs and EV supply chains will persist through 2033.

Government initiatives are expected to further propel regional market expansion via industrial modernization efforts, EV and hydrogen mobility programs, and healthcare growth featuring wearable diagnostics and home monitoring tools. Regulators are prioritizing emission controls, workplace safety protocols, and smart factory implementations to drive sensor integration. Expanding MEMS fabrication capabilities and large-scale production further accelerate this trajectory. Suppliers can maximize opportunities by forging local partnerships, customizing high-volume modules for EV platforms, and aligning with national incentives to streamline market entry and reduce logistics costs.

Competitive Landscape

The global piezoresistive pressure sensor market landscape in 2026 is expected to be led by major players such as Bosch, Honeywell, TE Connectivity, STMicroelectronics, NXP, Omron, and BD Sensors. These companies retain strong market positions through extensive sensor portfolios, advanced MEMS production capabilities, and deep OEM partnerships. Their leadership is supported by high reliability, precision engineering, and strong adoption across automotive, industrial, medical, and mobility applications.

Competition is increasingly driven by emerging MEMS-focused manufacturers and regional suppliers offering compact, affordable, and application-specific sensing solutions. Companies differentiate through innovations in miniaturization, long-life performance, and integration of digital communication interfaces. Expanding production in Asia, growing demand in medical electronics, and rising EV system integration encourage continuous R&D. This enables vendors to scale globally and meet rapidly evolving multi-industry sensing requirements in 2026.

Key Industry Developments

- In September 2025, TE Connectivity introduced the 85UHP series, leveraging a MEMS piezoresistive chip housed in 316L stainless steel or alloy C276 for enhanced corrosion resistance. This design supports high durability in harsh media environments, expanding TE’s offerings for demanding industrial and process applications.

- In July 2025, Kistler launched the 4012A piezoresistive absolute pressure sensor for hydrogen applications in combustion engines and fuel cells, providing reliable measurements up to 20 or 50 bar despite hydrogen embrittlement challenges. The sensor supports gas exchange analysis, low-pressure fuel rail monitoring, and fuel cell pressure tracking to enable emission-free, decarbonized mobility solutions.

- In June 2025, Omron launched the E8Y-L micropressure sensor series featuring an integrated digital display for real-time monitoring. The sensors target precise low-differential pressure measurement in clean industrial environments, supporting applications involving air and non-corrosive gases.

Companies Covered in Piezoresistive Pressure Sensor Market

- Honeywell International Inc.

- Bosch Sensortec GmbH

- TE Connectivity

- NXP Semiconductors

- Infineon Technologies AG

- STMicroelectronics

- Omron Corporation

- TDK Corporation

- Sensata Technologies

- Amphenol Advanced Sensors

- Melexis NV

- Keller AG für Druckmesstechnik

- MicroSensor Co., Ltd.

- WIKA Alexander Wiegand SE & Co. KG

Frequently Asked Questions

The global piezoresistive pressure sensor market is projected to reach US$ 5.7 billion in 2026.

Increased demand for high-precision MEMS sensors, strong adoption in EVs and ADAS systems, advancements in medical monitoring equipment, industrial digitalization, and the expansion of wireless and IoT-enabled sensing platforms are driving the market.

The market is poised to witness a CAGR of 4.4% from 2026 to 2033.

Engineering miniaturized and flexible sensors for wearables, high-pressure sensors for hydrogen mobility, digital/IoT-integrated sensor platforms, medical-grade MEMS sensors, and ruggedized sensors for harsh industrial and energy environments will open new market opportunities.

Bosch, Honeywell, TE Connectivity, STMicroelectronics, NXP Semiconductors, and Omron are some of the key players in the market.