- Electrical Equipment & Services

- Power Limited Tray Cable Market

Power Limited Tray Cable Market Size, Share, and Growth Forecast 2026 – 2033

Power Limited Tray Cable Market by Construction Type (Shielded and Unshielded), by Jacket Type (PVC, CPE, LSZH), by Insulation Type (THWN, XLPO, EPR, FREP/FR-EPR, XLPE/XHHW) and End-use Industry and Regional Analysis for 2026 - 2033

Power Limited Tray Cable Market Overview

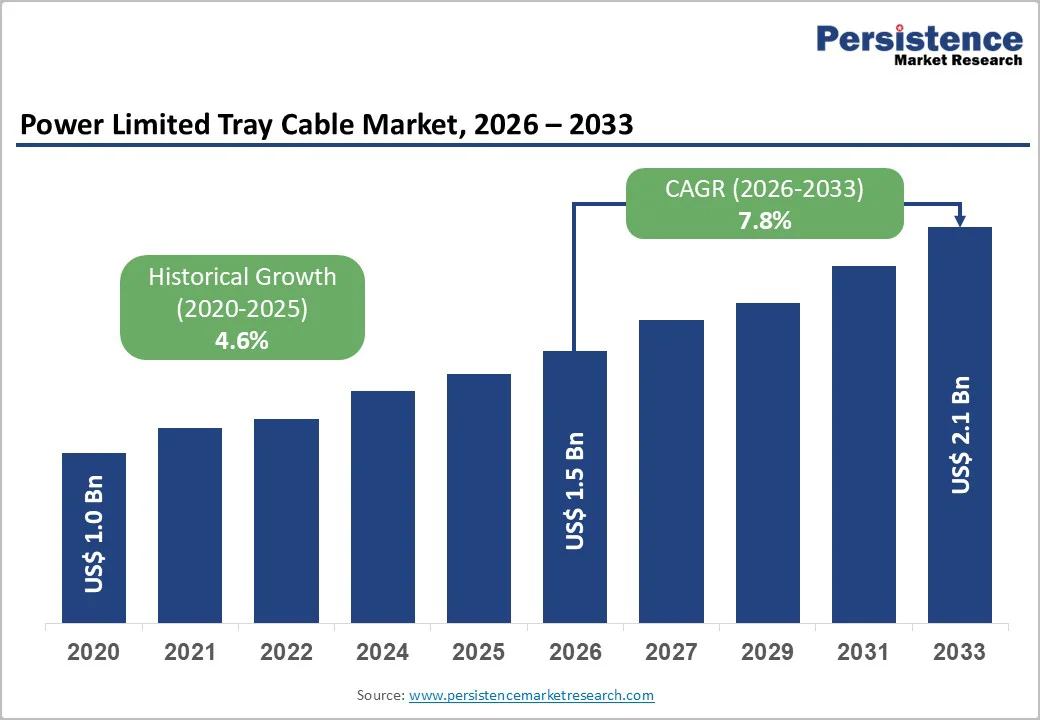

The global power limited tray cable market size was valued at US$ 1.5 Bn in 2026 and is projected to reach US$ 2.1 Bn by 2033, growing at a CAGR of 4.6% between 2026 and 2033.

The market is experiencing sustained growth driven by three interconnected factors: the unprecedented expansion of data center infrastructure powered by artificial intelligence and cloud computing, the global transition to renewable energy sources requiring sophisticated transmission systems, and massive government-backed infrastructure development initiatives. These factors collectively necessitate advanced power management and distribution solutions, making power-limited tray cables critical components of modern electrical infrastructure across industrial, commercial, and utility-scale installations.

Key Market Highlights

- Leading Region: North America maintains the largest market share at approximately 38% of global value, sustained by sophisticated infrastructure requirements, stringent safety standards, substantial capital investment in grid modernization (US$ 10.5 billion Grid Resilience Initiative), and premium specifications for EMI-protected cables in data center and industrial applications.

- Fastest Growing Region: Asia Pacific emerges as the fastest-expanding regional market driven by rapid industrialization, urbanization, and massive government-backed infrastructure initiatives, with India and China leading through renewable energy targets (India's 500 GW by 2030) and factory automation investments exceeding global peers by 20-25%.

- Dominant Segment: Shielded cable construction type commands approximately 55% market share, driven by critical requirements for EMI protection in high-density data centers, industrial automation facilities, and utility control systems where signal integrity directly impacts operational reliability and safety.

- Fastest Growing Segment: Renewable energy end-use applications demonstrate exceptional growth momentum at approximately 18% CAGR, emerging as the fastest-expanding market segment through the combined impact of ambitious government renewable targets, corporate carbon neutrality commitments, and technological maturation of wind and solar generation systems requiring robust transmission cable infrastructure.

- Key Market Opportunity: 5G and fiber-to-the-home (FTTH) network infrastructure expansion presents exceptional growth potential, with projected 10%+ annual growth in specialized cable management systems supporting dense network deployments, creating a sustained multi-year market opportunity as telecommunications operators execute capital-intensive buildout programs extending through 2033.

| Report Attribute | Details |

|---|---|

|

Power Limited Tray Cable Market Size (2026E) |

US$ 3.4 Bn |

|

Market Value Forecast (2033F) |

US$ 5.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7% |

|

Historical Market Growth (CAGR 2020 to 2024) |

3.8% |

Market Dynamics

Market Growth Drivers

Exponential Data Center Expansion and AI Infrastructure Acceleration

The global data center sector is experiencing unprecedented growth that fundamentally expands demand for power-limited tray cables. According to CRU analysis, cabling demand for data centers is projected to nearly triple from 264.8 kilotons in 2024 to 727 kilotons by 2029, representing one of the most dynamic growth vectors in the cable industry. Beyond the traditional colocation growth of 6.6% CAGR, artificial intelligence infrastructure deployment is expanding at a 33% CAGR, creating exponentially higher power-distribution requirements. Global data center power demand is forecasted to reach approximately 130 GW by 2028, reflecting a 16% CAGR from 2023 to 2028. In the United States specifically, data center power demand will account for up to 60% of total load growth through 2030. These AI-optimized facilities require sophisticated multi-tier cable distribution systems with higher current capacity, necessitating upgraded tray cable infrastructure capable of supporting 50 kW per rack configurations and three-phase power systems to minimize installation complexity and enhance efficiency.

Renewable Energy Transition and Grid Modernization Imperatives

Governments and utilities worldwide are executing transformational shifts toward renewable energy sources, fundamentally reshaping electrical infrastructure requirements and generating substantial tray cable demand. India has set an ambitious renewable energy target of 500 GW by 2030 (comprising 280 GW of solar and 140 GW of wind), supported by investments exceeding US$30 billion. Simultaneously, North America is experiencing rapid renewable capacity expansion, with major projects like Vineyard Wind and Roscoe Wind Farm requiring extensive specialized cabling infrastructure. Europe's €1 trillion Green Deal is accelerating the development of offshore wind and solar, with the region adding 17 GW of offshore wind capacity in 2022 alone. These renewable installations, particularly offshore wind farms and utility-scale solar arrays, require robust transmission systems connecting geographically dispersed generation sites to urban load centers, directly increasing demand for power limited tray cables designed to withstand harsh environmental conditions while delivering reliable long-distance power transmission. The Solar Cable Systems Market alone is expanding at 13% CAGR, driven by utility-scale solar projects accounting for over 60% of total solar capacity deployment.

Market Restraints

High Capital Expenditure and Supply Chain Vulnerabilities

The installation of comprehensive cable tray systems requires substantial capital investment, creating significant barriers to market adoption, particularly in price-sensitive markets and developing economies. The combined impact of raw material price volatility and supply chain disruptions has created persistent economic headwinds throughout the cable industry. Global copper and aluminum prices fluctuate based on macroeconomic cycles and geopolitical tensions, directly influencing production costs and project economics. Supply chain fragmentation, exacerbated by pandemic-related disruptions, has extended lead times and reduced manufacturing capacity utilization, constraining market growth momentum and delaying infrastructure projects that depend on timely cable delivery for scheduled completion.

Space Constraints and Installation Complexity in Densely Populated Urban Centers

Rapid urbanization is creating significant physical constraints that limit power-limited tray cable deployment in cities, where premium real estate and building codes restrict available installation pathways. Densely populated metropolitan areas require innovative, space-efficient cable management solutions rather than traditional tray systems, shifting demand toward compact conduit systems and alternative routing technologies. Retrofitting existing buildings with cable tray infrastructure presents substantial technical and regulatory challenges, including navigating historical preservation requirements, occupancy restrictions during construction, and coordinating with other building systems. These constraints reduce the addressable market in major urban centers, directly limiting the expansion potential of traditional power-limited tray cables in the most economically valuable geographic markets.

Market Opportunities

5G Network Deployment and Fiber-to-the-Home Infrastructure Expansion

The rollout of 5G technology and fiber-to-the-home (FTTH) networks across developed and emerging markets is creating significant new demand for power limited tray cables and associated management infrastructure. Europe is experiencing particularly robust growth in this sector, with projections indicating market expansion exceeding 10% annually for specialized conduits and protective cable systems. 5G base station deployment requires a densified network infrastructure with extensive underground and aerial cable routing, necessitating thousands of kilometers of new cable management systems across telecommunications operators' networks. Verizon alone has allocated US$10 billion to 5G expansion, underscoring the sector's capital intensity. The convergence of 5G technology with smart building initiatives (achieving 58% adoption in Europe) creates complementary demand for integrated power and data cable management solutions within commercial and residential properties, establishing a sustainable growth vector as operators’ complete capital deployment cycles through 2028-2033.

Industry 4.0 Adoption and Smart Manufacturing Cable Systems Development

The accelerating adoption of Industry 4.0 technologies and factory automation systems is generating exceptional opportunities for specialized power-limited tray cables engineered for industrial automation applications. The global industrial automation cable market is expanding at 7.12% CAGR, with Asia Pacific (particularly China, Japan, and India) driving the fastest regional growth through massive automation investments. China alone accounts for approximately 38% of global industrial automation cable consumption, with manufacturers investing 20-25% more in factory automation upgrades compared to global peers. Factory digitalization initiatives demand high-performance cables capable of supporting emerging IoT (Internet of Things) connectivity while delivering reliable power distribution through complex multi-level manufacturing facilities. The shift toward sensor-based production systems, robotic process automation, and real-time production monitoring creates distinct market opportunities for shielded power limited tray cables with enhanced electromagnetic interference (EMI) protection and superior mechanical durability, positioning manufacturers offering advanced cable solutions to capture significant value from this transformation.

Category-wise Insights

Construction Type Analysis

The power limited tray cable market demonstrates a clear bifurcation between shielded and unshielded construction types, with shielded cables commanding approximately 55% market share and experiencing faster growth momentum. Shielded cables, featuring foil or braid shielding layers around inner conductors, provide comprehensive electromagnetic interference (EMI) protection essential for high-density data center environments, industrial automation facilities, and utility control systems where signal integrity is mission-critical. These cables achieve near-complete isolation from external electromagnetic noise through complete cable coating or dual-layered protection (foil combined with braid), reducing crosstalk and ensuring reliable signal transmission in EMI-intensive industrial zones, recording studios, and security systems. However, shielding adds material cost (a 15-25% premium), increases cable diameter and weight, reduces installation flexibility, and requires specialized grounding procedures. Unshielded cables maintain market relevance through cost advantages (20-30% price reduction), superior installation flexibility, reduced weight, and proven performance in standard office LANs and low-EMI environments. The construction type selection depends fundamentally on end-use applications, with shielded dominance accelerating as industrial automation, data centers, and renewable energy control systems drive market composition toward high-EMI applications requiring robust interference protection.

Jacket Type Analysis

Polyvinyl chloride (PVC) jackets currently command approximately 48% market share, established by decades of widespread adoption, cost advantages, and proven performance across diverse industrial applications. PVC offers excellent flame propagation resistance (achieving UL 94 V-0 ratings), mechanical durability, and versatile performance across temperature ranges, making it the default specification for cost-sensitive applications in construction and standard industrial installations. However, regulatory and safety dynamics are fundamentally reshaping jacket type preferences across developed markets. Low Smoke Zero Halogen (LSZH) materials are experiencing the fastest growth trajectory, driven by stringent fire safety regulations, building codes emphasizing emergency safety, and corporate sustainability mandates. Europe is particularly aggressive in transitioning toward halogen-free materials, with regulatory frameworks increasingly prohibiting halogenated compounds in plenum spaces, enclosed building cavities, and confined industrial environments due to toxicity concerns when cables combust. LSZH formulations command 30-40% price premiums over PVC alternatives but eliminate toxic halogen gas emissions during fires, dramatically improving evacuation safety and reducing equipment damage from corrosive smoke. Chlorinated polyethylene (CPE) jackets occupy a narrowing market niche, offering modest cost reductions compared to PVC while delivering similar performance, positioning them for applications in emerging markets where cost considerations outweigh advanced safety specifications.

Insulation Type Analysis

Thermoplastic high heat-resistant nylon (THHN) insulation dominates the power-limited tray cable market with approximately 38% market share, sustained by cost efficiency (lowest material expense among viable alternatives), ease of installation, and established code acceptance across North American jurisdictions. THHN operates reliably at 90°C in dry conditions, serving standard industrial and commercial applications where temperature extremes and moisture resistance are not primary design constraints. However, THHN's limitation to 75°C in wet conditions and moderate chemical resistance restrict applicability in demanding industrial environments. Cross-linked polyethylene (XLPE/XHHW) insulation demonstrates the fastest expansion trajectory, projected to capture approximately 32% market share by 2033. XLPE delivers superior thermal stability (maintaining 90°C ratings in both wet and dry conditions), exceptional dielectric strength, enhanced chemical resistance, and extended service life (30-40 years versus 20-25 years for THHN). The synthetic cross-linking process enhances mechanical strength and environmental durability, positioning XLPE as the preferred specification for renewable energy transmission systems, offshore installations, and harsh industrial environments. Ethylene propylene rubber (EPR) insulation captures approximately 18% market share, particularly valued in applications requiring extreme flexibility, superior chemical resistance to oils and solvents, and low-temperature performance down to -40°C to -50°C.

Flame-retardant ethylene propylene (FREP/FR-EPR) formulations are emerging in specialized hazardous-location applications that require the combined advantages of EPR flexibility and enhanced fire-safety characteristics. THWN/THWN-2 water-resistant nylon insulation maintains steady relevance at approximately 12% market share, specifically for wet installations where superior water resistance exceeds THHN capabilities while maintaining cost-effectiveness below XLPE alternatives.

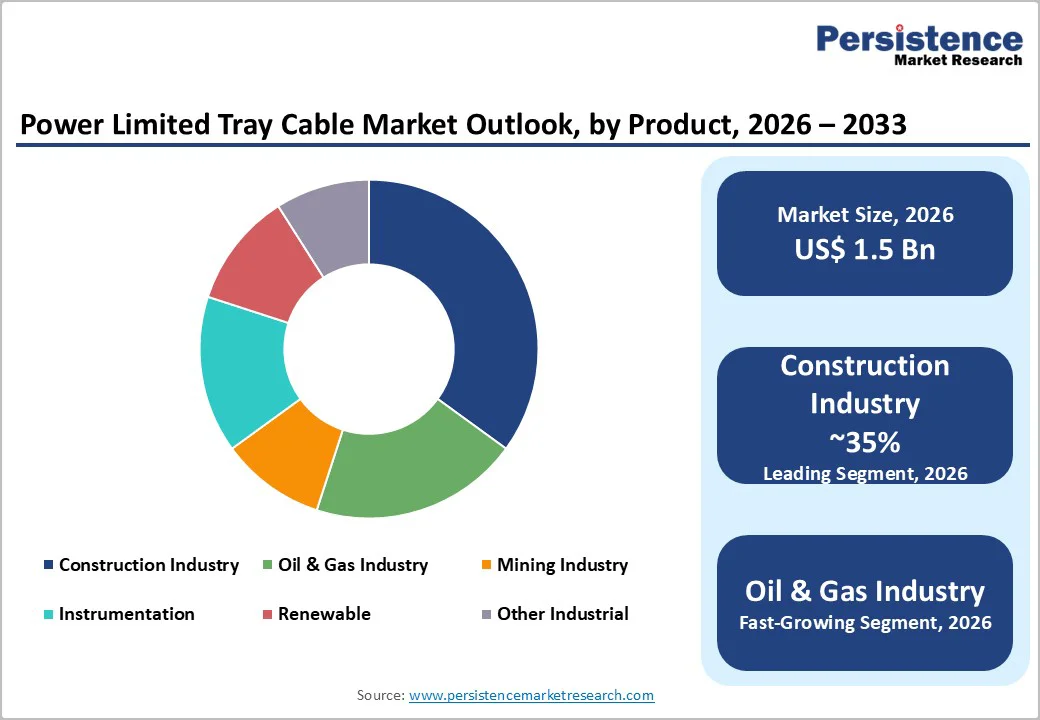

End-use Industry Analysis

The construction industry emerges as the dominant end-use sector, commanding approximately 32% of total power-limited tray cable demand, sustained by persistent residential and commercial building expansion, particularly across emerging markets like China, India, and Brazil. Infrastructure development initiatives—including the Indian government's Pradhan Mantri Awas Yojana (PMAY) scheme allocating US$ 9.5 billion for housing development and the PM Gati Shakti National Master Plan targeting expanded grid capacity by 28,700 circuit kilometers—are generating substantial electrical infrastructure demand. However, the renewable energy sector is experiencing the fastest growth, with an approximately 18% CAGR, emerging as the dominant future driver through the convergence of government renewable energy targets and corporate carbon neutrality commitments. Oil and gas operations capture approximately 19% market share, with specialized cable requirements for hazardous location classifications (Class I/II Division 1&2) creating distinct technical specifications and regulatory compliance demands. Mining industry applications command approximately 15% market share, characterized by extreme environmental demands requiring superior abrasion resistance, heat tolerance (up to 90°C continuous operation), and mechanical durability under crushing and impact conditions. Instrumentation applications capture approximately 10% market share in process control, measurement, and automation systems. Instrumentation cables operate at 300/500V ratings, require low-noise characteristics, and demand superior reliability in critical process-monitoring applications across petrochemical facilities and power generation plants.

Regional Insights

North America Power Limited Tray Cable Trends

North America, particularly the United States, maintains its position as the largest regional market for power-limited tray cables, representing approximately 38% of the global market value, sustained by sophisticated infrastructure, stringent safety standards, and continued capital investment in grid modernization. The U.S. Grid Resilience and Innovation Partnership has allocated US$ 10.5 billion specifically for transmission line modernization, directly benefiting power cable manufacturers and supporting sustained infrastructure investment cycles. Data center concentration in major metropolitan areas (particularly California, Virginia, and Texas) is driving unprecedented demand for cable infrastructure, with AI-powered facilities requiring three-phase power systems and high-capacity distribution networks.

The renewable energy transition is fundamentally reshaping North American cable demand, with accelerating wind and solar deployment requiring specialized transmission infrastructure. Offshore wind projects, including Vineyard Wind off Massachusetts and extensive development programs along the Atlantic Coast, demand specialized submarine cables with XLPE insulation capable of ±320 kV transmission across salt-corrosion environments. Texas's Roscoe Wind Farm and similar utility-scale renewable projects across the Great Plains require medium-voltage collection systems and ultra-high-voltage transmission cables connecting dispersed generation sites to population centers.

Europe Power Limited Tray Cable Trends

Europe's power-limited tray cable market is valued at approximately US$ 3.4 billion in 2024, with projections reaching US$ 4.8 billion by 2030, representing 5.8% CAGR expansion driven by sustainability commitments and digital transformation initiatives. Germany dominates the European market with approximately 32% regional share, leveraging its substantial industrial base in automotive and manufacturing sectors that depend on advanced automation cable systems. Germany accounts for over 30% of European industrial automation investments, directly driving demand for shielded power-limited tray cables designed for Industry 4.0 applications. Federal Ministry for Economic Affairs commitments of €17 billion toward wind and solar projects in 2022 further accelerate cable infrastructure requirements across renewable installations.

Europe's distinctive regulatory environment is fundamentally transforming product specifications, with the EU Energy Performance of Buildings Directive and comparable regulatory frameworks driving 40% of new construction projects to incorporate halogen-free, low-smoke cable systems. France's €14 billion investment in sustainable building projects and €10 billion allocation to solar and wind power under the Multiannual Energy Plan are generating robust demand for specialized renewable energy transmission cables. United Kingdom, post-Brexit, maintains a distinctive advanced market characterized by aggressive adoption of 5G infrastructure, data center development, and stringent fire safety standards, with notable projects including HS2 high-speed rail and extensive offshore wind farm development. European utilities are implementing sophisticated smart grid technologies, requiring control cables capable of supporting IoT connectivity alongside traditional power distribution, creating hybrid cable solutions combining electrical and data transmission functions.

Asia Pacific Power Limited Tray Cable Trends

Asia Pacific emerges as the fastest-growing regional market for power-limited tray cables, driven by rapid industrialization, accelerating urbanization, and massive infrastructure development initiatives across the region's most populous nations. China's dominance within Asia Pacific is sustained through its extraordinary manufacturing capacity, accounting for approximately 38% of global industrial automation cable consumption, combined with government-mandated automation investments totaling 20% higher than global peers. China's industrial cables market was valued at approximately US$ 68.52 billion in 2024, with projections reaching US$ 123 billion by 2033, reflecting infrastructure investment in factories, renewable energy installations, and smart city development across Shenzhen, Shanghai, and emerging industrial zones. India, positioned as the third-largest global cable market, consumed approximately 1,266 kilotonnes of insulated metallic cable in 2023, representing 6% of global consumption, and maintained robust 7.8% year-over-year growth in 2024.

India's 500 GW renewable energy target by 2030 necessitates massive transmission infrastructure investment, particularly for solar projects requiring 50 kilometers of solar cable per 1 MW installation and offshore wind systems requiring specialized submarine array and export cables (rated 33-400 kV). The Green Energy Corridor Project, targeting 50 GW of renewable energy supply to national grids, is fundamentally reshaping cable demand toward specialized high-voltage transmission systems. Japan and South Korea contribute substantial market value through advanced manufacturing, sophisticated industrial automation applications, and aggressive corporate renewable energy procurement programs.

Market Structure Analysis

The global power limited tray cable market exhibits a consolidated competitive structure, dominated by 8-10 major multinational corporations commanding approximately 60-65% aggregate market share, complemented by numerous regional and specialized manufacturers addressing niche applications and geographies. Market consolidation reflects substantial capital requirements for R&D infrastructure, global supply chain operations, and technical certification capabilities, creating significant barriers to competitive entry.

Leading competitors including Prysmian Group, Nexans, Belden, and HELUKABE maintain competitive advantages through vertically integrated manufacturing, extensive distribution networks across developed and emerging markets, and proprietary technology platforms for specialized applications. Prysmian Group, positioning itself as the world's largest industrial and energy cables manufacturer, maintains superior competitive standing through advanced R&D capabilities, comprehensive product portfolios spanning power transmission, telecommunications, industrial automation, and renewable energy systems, and geographic diversification across North America, Europe, and Asia Pacific regions.

Key Market Developments

- In May 2026, Prysmian Group expanded industrial cable production capacity to support accelerating demand from renewable power projects and smart grid infrastructure upgrades across international markets, signaling confidence in sustained long-term growth in specialized cable systems for energy transition applications.

- In January 2026, Nexans launched new industrial cable solutions specifically engineered to improve sustainability and energy efficiency metrics, aligning with client requirements for carbon reduction initiatives and supporting increasing regulatory mandates for eco-friendly cable formulations in construction and industrial applications.

Companies Covered in Power Limited Tray Cable Market

- Multicable Corporation

- Belden Inc

- Sycor International Inc

- HELUKABEL Canada

- Nexans Deutschland GmbH

- Houston Wire & Cable Co.

- SAB Bröckskes GmbH & Co. KG

- Prysmian Group

- Anixter Inc

- Turck Inc.

- Others Key Players

Frequently Asked Questions

The global Power Limited Tray Cable Market is projected to reach US$ 2.1 billion by 2033, expanding from US$ 1.5 billion in 2026 to a 4.6% CAGR, driven by sustained demand from data center infrastructure, renewable energy transmission systems, and industrial automation applications across developed and emerging markets.

The primary demand drivers are exponential data center expansion (cabling demand nearly tripling from 264.8 kt in 2024 to 727 kt by 2029), the renewable energy transition with massive government targets (India's 500 GW by 2030, Europe's € 1 trillion Green Deal), and infrastructure modernization initiatives including grid upgrades and 5G deployment requiring sophisticated cable distribution systems supporting high-density installations.

Thermoplastic high heat-resistant nylon (THHN) currently dominates with approximately 38% market share due to cost-efficiency and established code acceptance, but Cross-linked polyethylene (XLPE) is the fastest-growing segment due to superior thermal stability (90°C in wet and dry conditions), extended service life (30-40 years), and enhanced chemical resistance essential for renewable energy and harsh industrial applications.

North America maintains market leadership at approximately 38% of global value, sustained by infrastructure investment (US$ 10.5 billion Grid Resilience Initiative), data center concentration, and stringent safety requirements.

Leading market players include Prysmian Group (world's largest industrial cables manufacturer), Nexans S.A. (global sustainable electrification specialist), Belden Inc. (industrial automation cable leader), HELUKABEL Canada, Sycor International Inc., Multicable Corporation, Houston Wire & Cable Co.