- Power Generation, Transmission, & Distribution

- Power Quality Instruments Market

Power Quality Instruments Market Size, Share, and Growth Forecast 2026 - 2033

Power Quality Instruments Market by Product Type (Analyzers (Fixed Power Quality Analyzers, Portable Power Quality Analyzers, Handheld Power Quality Analyzers), Meters, Recorders, Loggers, Others), Phase Type (Single Phase, Three Phase), Industry (Industrial & Manufacturing, Utilities, Commercial, Residential, Others), and Regional Analysis, 2026 - 2033

Power Quality Instruments Market Size and Trend Analysis

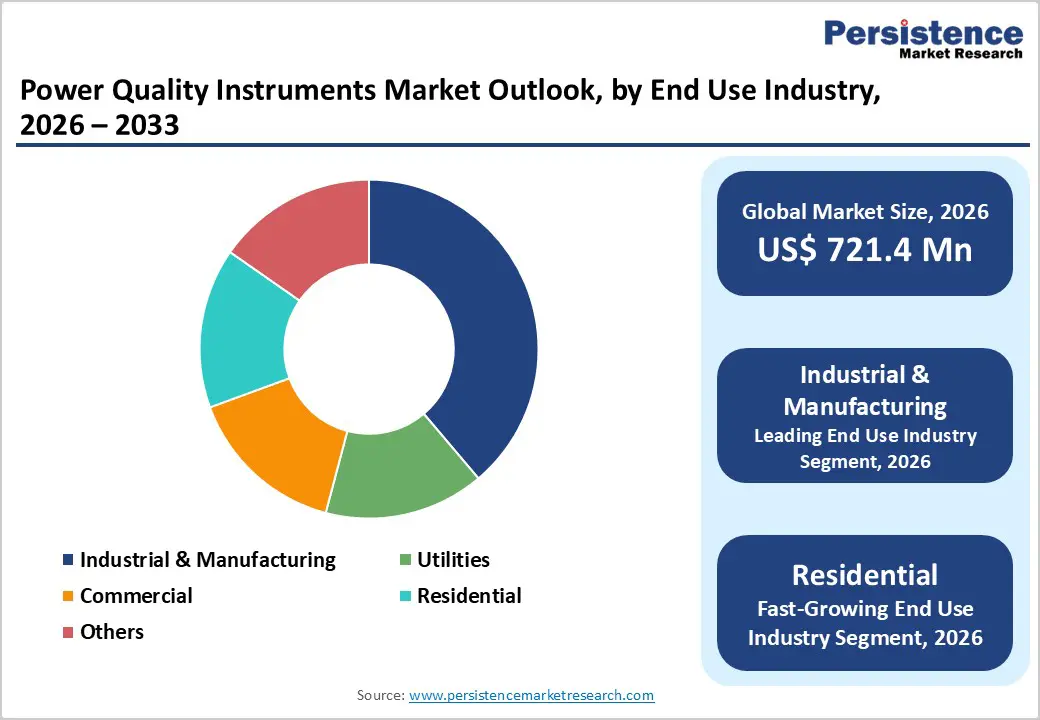

The global Power Quality Instruments market size is expected to be valued at US$ 721.4 million in 2026 and projected to reach US$ 1,166.0 million by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

The power quality instruments market is entering an accelerated growth phase, driven by the rapid global integration of renewable energy sources into utility grids, the proliferation of sensitive electronic loads across industrial and commercial facilities, and intensifying regulatory requirements for grid power quality compliance. As variable renewable generation, particularly solar photovoltaic and wind, introduces voltage fluctuations, harmonics, and frequency deviations into distribution networks, the deployment of advanced power quality analyzers, meters, and recorders has become operationally critical for utilities, industrial operators, and data center managers.

Key Industry Highlights

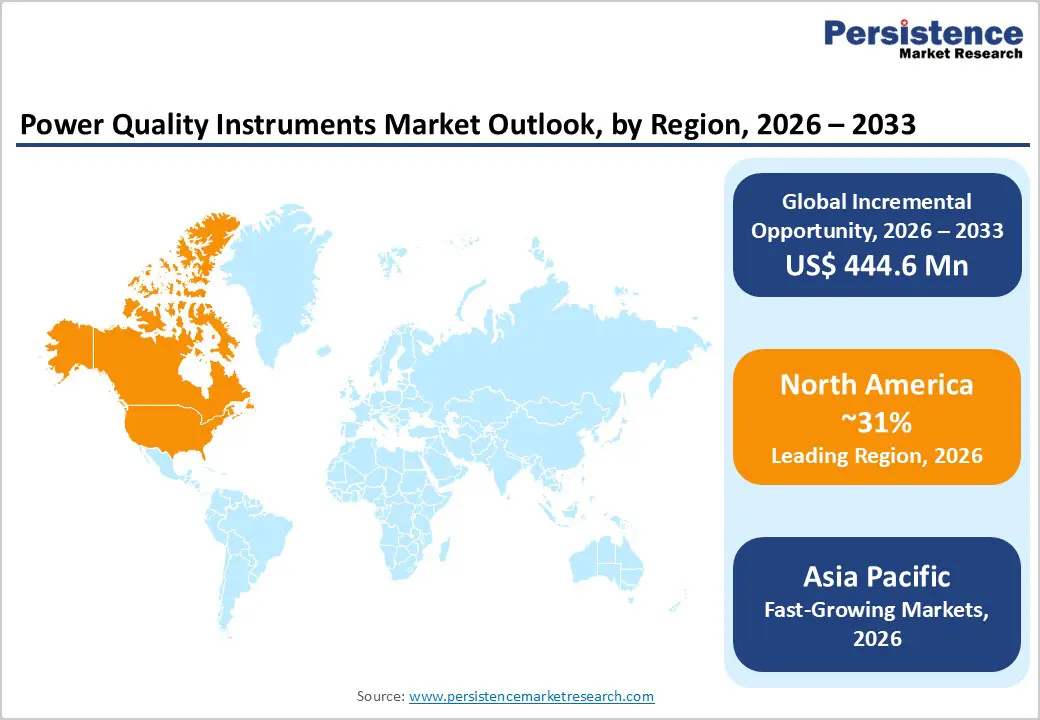

- Leading Region: North America leads the global Power Quality Instruments market with ~31% revenue share in 2025, supported by the U.S. DOE’s Grid Modernization Initiative, NERC reliability compliance mandates, growing demand for hyperscale data center power quality monitoring, and dominant market players including Eaton Corporation and Emerson Electric Co.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market over 2026–2033, driven by China’s massive grid modernization investments under the State Grid Corporation, India’s RDSS distribution upgrade scheme, Japan’s precision industrial power management requirements, and rapid industrial capacity expansion across ASEAN economies.

- Dominant Segment: Analyzers dominate the Product Type segment with approximately ~44% market share in 2025, underpinned by their comprehensive multi-parameter measurement capability, IEC 61000-4-30 Class A compliance for regulatory and contractual power quality verification, and growing adoption by utilities deploying renewable energy integration monitoring infrastructure.

- Fastest Growing Segment: IoT-enabled cloud-connected power quality instruments represent the fastest growing product innovation category, with DOE Grid Modernization Initiative programs and EU Horizon Europe research investments driving deployment of networked, AI-analytics-integrated monitoring solutions that generate recurring software and service revenue beyond traditional hardware sales.

- Key Opportunity: Data center power quality monitoring is the key market opportunity, with global hyperscale data center expansion, driven by AI and cloud computing demand, creating critical need for precision power quality instruments, given that a single voltage sag event can cost enterprises up to US$ 9,000 per minute of unplanned downtime.

| Key Insights | Details |

|---|---|

|

Power Quality Instruments Market Size (2026E) |

US$ 721.4 Million |

|

Market Value Forecast (2033F) |

US$ 1,166.0 Million |

|

Projected Growth CAGR (2026–2033) |

7.1% |

|

Historical Market Growth (2020–2025) |

5.8% |

Market Dynamics

Drivers - Rapid Renewable Energy Integration Amplifying Grid Power Quality Challenges

The global energy transition toward renewable electricity generation is a primary structural catalyst for the power quality instruments market. Solar photovoltaic and wind generation, unlike conventional synchronous generation, introduce inherent variability in voltage magnitude, harmonic distortion, and frequency stability into distribution and transmission grids, requiring continuous real-time power quality monitoring to maintain within regulatory thresholds. The International Energy Agency (IEA) reported that global renewable electricity capacity additions reached a record 295 gigawatts (GW) in 2022, with solar PV alone accounting for over 191 GW of new installations. By 2030, the IEA projects renewables will account for nearly 60% of global electricity generation under stated policy scenarios. Each new renewable installation, particularly grid-tied inverter-based resources, generates power quality events, including voltage swells, sags, harmonics, and interharmonics, that mandate monitoring with certified power quality analyzers compliant with standards such as IEC 61000-4-30 and EN 50160.

Smart Grid Modernization and Advanced Metering Infrastructure Investments

Government-led smart grid modernization programs across major economies are generating sustained, large-scale demand for power quality monitoring instruments as integral components of next-generation grid management infrastructure. The U.S. Department of Energy (DOE) has allocated substantial funding under the Infrastructure Investment and Jobs Act (IIJA), which includes over US$ 20 billion for grid resilience and modernization, toward the deployment of advanced sensing, metering, and monitoring systems that include power quality instrumentation at substation, feeder, and customer connection levels. In the European Union, the European Commission’s Electricity Market Reform and the Smart Grid Task Force are mandating interoperable, real-time power-quality data acquisition capabilities across member-state distribution system operators. This public investment-backed demand is compelling utilities to procure large volumes of fixed and portable power quality analyzers and data loggers from established manufacturers, including Eaton Corporation, ABB Ltd., and Schneider Electric S.E.

Restraints - High Instrument Cost and Complex Calibration Requirements

Advanced three-phase power quality analyzers, particularly those compliant with IEC 61000-4-30 Class A measurement standards required for formal utility and regulatory compliance testing, represent significant capital expenditures that can limit adoption among smaller industrial end users and distribution utilities in cost-constrained markets. High-specification portable power quality analyzers from leading manufacturers such as Siemens and Eaton Corporation can carry price tags of US$5,000 to over US$25,000 per unit, while comprehensive fixed monitoring systems for industrial substations can cost substantially more when installation, communication infrastructure, and software licensing are included. Additionally, maintaining measurement accuracy over time requires periodic professional calibration traceable to national standards bodies such as NIST (U.S.) or PTB (Germany), adding ongoing operational cost burdens that can deter procurement, especially among SME industrial operators in developing markets.

Lack of Standardization and Interoperability Across Measurement Protocols

Despite international power quality measurement standards, including IEC 61000-4-30, IEEE 1159, and EN 50160, significant interoperability gaps persist between instruments from different manufacturers and between legacy grid monitoring infrastructure and newer IoT-connected power quality logging systems. Different utilities and industrial operators may specify different measurement parameters, aggregation intervals, and communication protocols, creating integration complexity when deploying multi-vendor power quality monitoring networks. This fragmentation increases system integration costs and slows procurement decision cycles, particularly in large utility and industrial deployments, where interoperability with existing SCADA, energy management systems (EMS), and IEC 61850-compliant substation automation infrastructure is mandatory. Until comprehensive standardization matures, these interoperability barriers will continue to moderate the pace of large-scale deployment in complex grid environments.

Opportunity - Data Center and Critical Facility Power Quality Monitoring Expansion

The unprecedented global expansion of data center capacity, driven by cloud computing, artificial intelligence workload growth, and digital transformation, is creating a high-value and rapidly growing demand segment for precision power quality instruments. Data centers are among the most power quality-sensitive facilities in existence: voltage sags as brief as 16.7 milliseconds or harmonic distortion levels exceeding 5% THD (Total Harmonic Distortion) can cause server crashes, storage corruption, and unplanned downtime that costs enterprises an average of US$ 9,000 per minute of outage, according to Ponemon Institute research. The International Data Corporation (IDC) projects that global data center spending will grow significantly through 2026, with power quality management representing a mandatory operational investment. Manufacturers, including Emerson Electric Co., Eaton Corporation, and Schneider Electric S.E., are actively developing integrated power quality monitoring solutions tailored to data center power distribution architectures (including UPS monitoring, PDU harmonic analysis, and real-time alerting systems), positioning this segment as a premium, high-CAGR revenue opportunity through 2033.

IoT-Enabled Cloud-Connected Power Quality Instruments for Predictive Grid Analytics

The convergence of IoT connectivity, cloud computing, and machine learning analytics is transforming power quality instruments from standalone measurement devices into networked, data-generating nodes within intelligent grid and facility energy management platforms, creating a transformative product innovation and market expansion opportunity. Next-generation power quality instruments equipped with embedded cellular or Wi-Fi connectivity, on-board edge computing, and cloud-dashboard integration enable continuous remote monitoring, automated anomaly detection, and AI-driven predictive maintenance workflows that were previously impossible with conventional standalone instruments. The U.S. Department of Energy (DOE)’s Grid Modernization Initiative and the European Commission’s Horizon Europe research programs have both identified connected power quality monitoring as a priority technology for resilient grid operation. Companies including ABB Ltd. and Honeywell International, Inc. are actively developing cloud-platform-integrated power quality management ecosystems, representing a structurally differentiated and higher-margin recurring revenue model that goes well beyond traditional instrument hardware sales.

Category-wise Analysis

Product Type Insights

The Analyzers segment, encompassing Fixed, Portable, and Handheld Power Quality Analyzers, holds the dominant position in the power quality instruments market, commanding approximately ~44% of total global revenue in 2025. Power quality analyzers are the most technically comprehensive instruments in the market, capable of simultaneously measuring and recording voltage, current, frequency, harmonics up to the 50th order, flicker, transients, dips, swells, and unbalance parameters in compliance with IEC 61000-4-30 and IEEE 1159 standards. Portable power quality analyzers are particularly valued for troubleshooting and commissioning applications across industrial, utility, and commercial facilities, where site-specific measurements are required without permanent installation. The adoption of Class A-compliant analyzers, which provide the highest measurement accuracy for regulatory compliance, dispute resolution, and contractual power quality verification, is accelerating among utilities and large industrial energy managers, sustaining the analyzer segment’s market leadership and premium unit pricing throughout the forecast period.

Phase Type Insights

Three-phase power quality instruments dominate the phase-type segment, accounting for ~67% of total market revenue in 2025. The prevalence of three-phase power distribution systems across industrial, commercial, and utility environments, which represent the highest-value and highest-volume power quality monitoring application categories, underpins the overwhelming market leadership of three-phase instruments. Industrial manufacturing facilities, commercial buildings with large HVAC and elevator systems, data centers, and utility distribution feeders all operate on three-phase systems that require simultaneous multi-phase power-quality monitoring to identify phase imbalance, neutral-conductor overloading, and asymmetric harmonic injection. Standards including IEC 61000-4-30 explicitly define three-phase measurement methodologies as the framework for Class A and Class S compliance measurements, further cementing three-phase instrument specifications in formal utility and industrial procurement requirements managed by leading OEMs, including ABB Ltd., Siemens, and Legrand.

Industry Insights

The Industrial & Manufacturing segment holds the largest share of the power quality instruments market, representing approximately ~38% of total global revenue in 2025. Manufacturing facilities are both major consumers of electrical power and operators of equipment, including variable frequency drives (VFDs), arc furnaces, large motor loads, and switching power supplies, that both generate and are critically sensitive to power quality disturbances. According to the Electric Power Research Institute (EPRI), power quality problems cost the U.S. industry alone an estimated US$ 80–188 billion annually in equipment damage, production losses, and downtime, providing a compelling financial case for investment in continuous power quality monitoring. The deployment of advanced power quality analyzers and data loggers across industrial substations, motor control centers, and production line power distribution points enables proactive identification of harmonic pollution sources, grounding faults, and supply voltage deviations before they cause costly equipment failures or process shutdowns.

Regional Insights

North America Power Quality Instruments Market Trends and Insights

North America holds the leading position in the global power quality instruments market, accounting for an estimated ~31% of global revenue share in 2025, anchored by the United States’ technologically advanced electric utility sector, large industrial manufacturing base, and active smart grid investment programs. The U.S. Department of Energy (DOE), through the Grid Modernization Initiative and the Infrastructure Investment and Jobs Act grid funding allocations, has been instrumental in accelerating the deployment of advanced monitoring, sensing, and power-quality instrumentation across U.S. transmission and distribution networks. North American Electric Reliability Corporation (NERC) reliability standards and IEEE power quality guidelines provide a robust regulatory framework that mandates measurable power-quality compliance across utilities and large industrial interconnections, thereby sustaining procurement of certified instruments from established domestic and multinational suppliers.

The growth of hyperscale data centers, with major investments by Amazon Web Services, Microsoft Azure, and Google Cloud in Virginia, Texas, and the Pacific Northwest, is further intensifying North American demand for precision power-quality monitoring systems. Canada’s aggressive renewable energy integration across its provincial grids, particularly wind integration in Ontario and Alberta, is also driving utility investment in grid-connected power quality measurement infrastructure. Manufacturers including Eaton Corporation, Emerson Electric Co., and Honeywell International, Inc., leverage their deep North American market presence, regional service networks, and compliance expertise to maintain strong competitive positions across both utility and industrial customer segments.

Europe Power Quality Instruments Market Trends and Insights

Europe is a mature yet dynamically evolving market for power quality instruments, characterized by stringent regulatory harmonization, aggressive renewable energy deployment, and a strong culture of industrial energy-efficiency management. The European Union’s power quality standard EN 50160, which defines voltage characteristics of electricity supplied by public distribution networks, and the broader IEC 61000 series provide the regulatory foundation for power quality instrument procurement and compliance measurement across all EU member states. Germany, France, the United Kingdom, and the Nordic nations are the primary national markets, reflecting their large industrial manufacturing sectors, extensive renewable energy integration programs, and utility modernization investments.

Germany’s Energiewende policy, which has driven renewable energy’s share of electricity generation to over 55% in 2023 according to the Federal Network Agency (Bundesnetzagentur), is creating significant grid power quality management challenges at the distribution level, directly driving demand for advanced power quality monitoring instruments across German DSOs (Distribution System Operators). Schneider Electric S.E., ABB Ltd., Siemens, and Legrand maintain strong European market positions through product compliance with EN 50160 and IEC 61000-4-30, and through well-established distribution and service networks. The UK’s ongoing offshore wind expansion and France’s nuclear refurbishment program, alongside growing solar penetration, are further driving investment in utility-grade power quality monitoring across the region.

Asia Pacific Power Quality Instruments Market Trends and Insights

Asia Pacific is the fastest-growing regional market for power quality instruments over the 2026–2033 forecast period, driven by the world’s most dynamic electricity demand growth, rapid renewable energy integration, and massive industrial expansion across China, India, Japan, and ASEAN economies. China, the world’s largest electricity consumer and renewable energy installer, is the dominant national market in the region. The National Energy Administration (NEA) of China reported total electricity consumption of approximately 9.22 trillion kWh in 2023, with grid power quality management becoming increasingly critical as high-penetration solar and wind generation is integrated into provincial and national grid infrastructure. China’s State Grid Corporation and China Southern Power Grid are investing substantially in smart grid technologies, including power quality monitoring systems, creating large procurement volumes for both domestic manufacturers and international suppliers with local partnerships.

India is among the highest-growth individual markets globally for power quality instruments. The Ministry of Power, Government of India, has set ambitious targets under the National Electricity Policy and the Revamped Distribution Sector Scheme (RDSS), with an outlay of approximately INR 3.03 trillion, to upgrade distribution infrastructure and reduce aggregate technical and commercial losses, both of which require advanced power-quality measurement infrastructure. Japan’s precision industrial sector and its sophisticated grid management culture sustain demand for high-specification power quality instruments, while ASEAN nations, particularly Vietnam, Indonesia, Thailand, and Malaysia, are experiencing rapid industrial capacity growth, generating new demand for industrial and utility-grade power quality monitoring solutions across their expanding manufacturing corridors.

Competitive Landscape

The global power quality instruments market is moderately consolidated in the premium and mid-range segments, where a limited number of multinational electrical and instrumentation companies hold strong market positions. Competition is primarily based on measurement accuracy, compliance with international standards such as IEC 61000-4-30 Class A, portfolio breadth across portable and fixed analyzers, and the ability to integrate seamlessly into broader energy management ecosystems. Established players leverage global service networks, calibration capabilities, and long-standing utility and industrial relationships to sustain competitive advantage.

Strategically, the market is transitioning from hardware-centric sales toward integrated digital solutions. Cloud connectivity, IoT-enabled monitoring, and AI-driven analytics are becoming core differentiators, enabling real-time diagnostics and predictive maintenance. Vendors are increasingly adopting software-as-a-service subscription models, bundled energy management platforms, and condition-based monitoring contracts to generate recurring revenue streams. This shift toward data-driven service ecosystems is strengthening customer retention while expanding lifetime value beyond initial instrument deployment.

Key Developments:

- February, 2026: Accuenergy launched its new ACUvim-3 Series power quality meters compliant with IEC 61000-4-30 Class A standards, designed to enhance grid monitoring accuracy and reliability for utilities and industrial end users.

- February, 2026: Power Monitors, Inc. launched Merlin™, an AI-powered power quality analysis system designed to help electric utilities rapidly interpret complex PQ data, classify disturbances, and support compliance and reporting workflows.

- November, 2025: Keysight Technologies, Inc. announced a new portfolio of high-power automated test equipment (ATE) supplies, including regenerative power supplies and electronic loads, to help engineers address complex power validation challenges with higher density and automation.

Companies Covered in Power Quality Instruments Market

- Eaton Corporation

- ABB Ltd.

- Siemens

- General Electric Company

- Honeywell International, Inc.

- Leviton Manufacturing Co., Inc.

- Emerson Electric Co.

- Schneider Electric S.E.

- Legrand

- Piller Power Systems

- Fluke Corporation

- Yokogawa Electric Corporation

- Dranetz Technologies

Frequently Asked Questions

The global Power Quality Instruments market is valued at US$ 721.4 million in 2026 and is projected to reach US$ 1,166.0 million by 2033 at a CAGR of 7.1%.

Demand is driven by rising renewable energy integration, grid disturbances, smart grid modernization investments, and increasing need for real-time monitoring solutions.

North America leads with around 31% revenue share in 2025, supported by grid modernization programs and strong utility and data center demand.

The key opportunity lies in IoT-enabled, cloud-connected instruments offering AI-based analytics and subscription-driven monitoring platforms.

Key players include Eaton Corporation, ABB Ltd., Schneider Electric S.E., Siemens, and Fluke Corporation, among others competing through certified measurement solutions and digital analytics platforms.