- Power Generation, Transmission, & Distribution

- Power System Simulator Market

Power System Simulator Market Size, Share, and Growth Forecast 2026 - 2033

Power System Simulator Market by Component (Hardware, Software, Services), Analysis (Load Flow, Short Circuit, Harmonic, Transient, Others), End-user (Power Generation, Transmission & Distribution, Industrial, Others), and Regional Analysis, 2026 - 2033

Power System Simulator Market Size and Trend Analysis

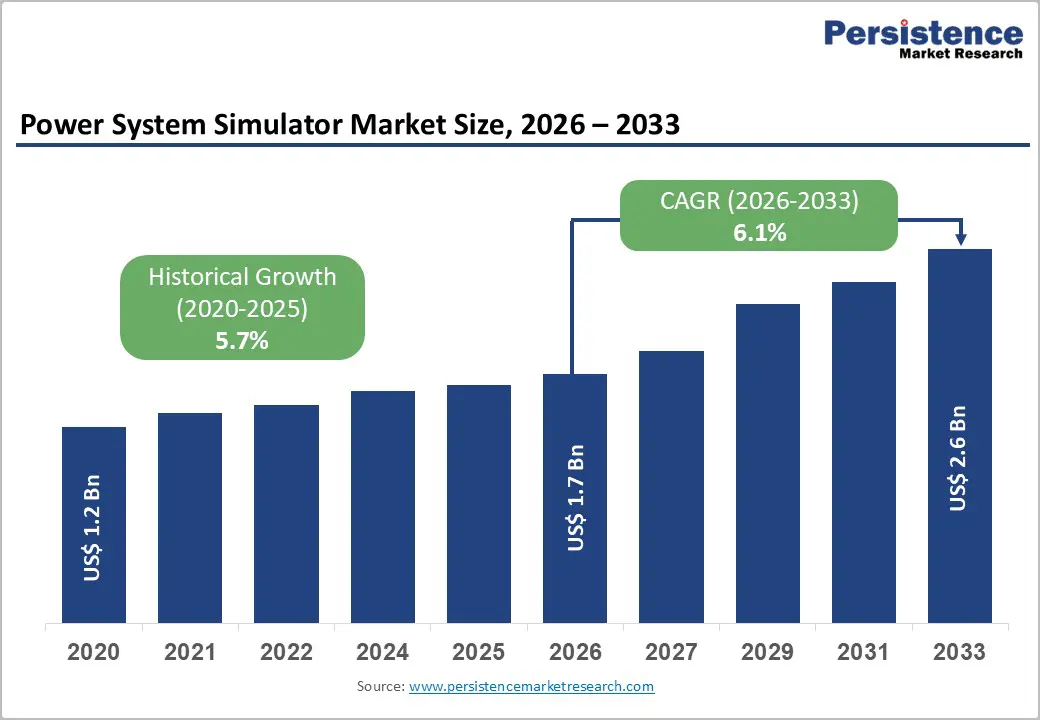

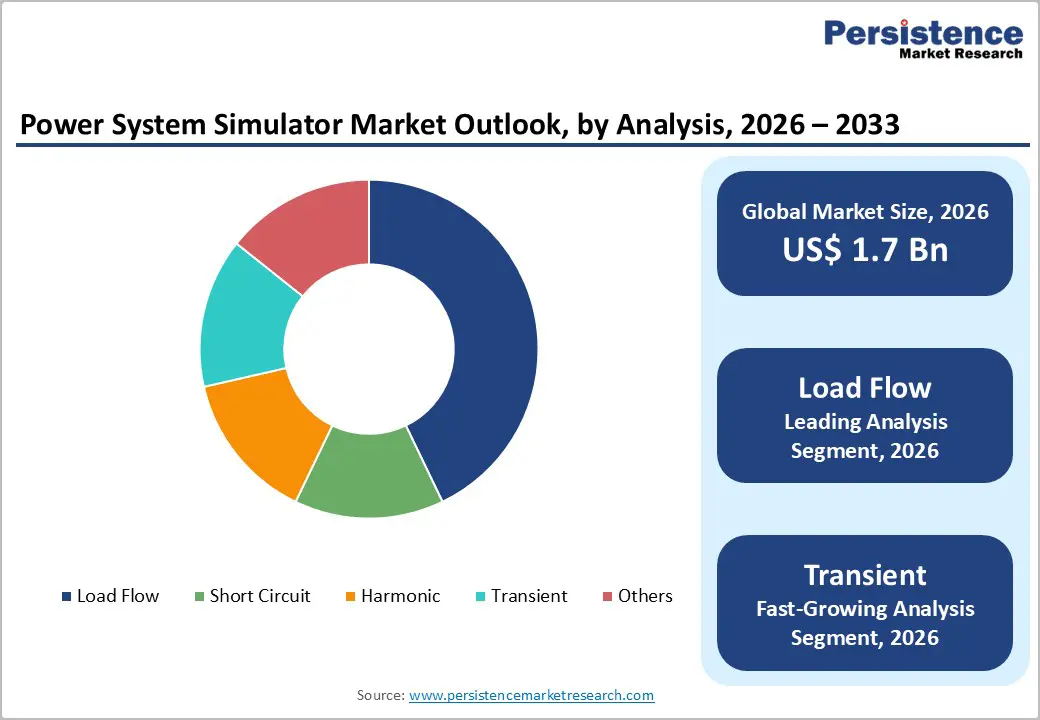

The global power system simulator market size is expected to be valued at US$ 1.7 billion in 2026 and projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

The market growth is driven by rising global electricity demand, increased grid complexity from renewable energy integration, and rising investment in smart grid infrastructure across developed and emerging economies. Power system simulators enable utilities to optimize grid operations, enhance system reliability, and accelerate the transition to renewable energy sources by providing real-time analysis, testing, and training capabilities essential to modern power system management.

Key Market Highlights

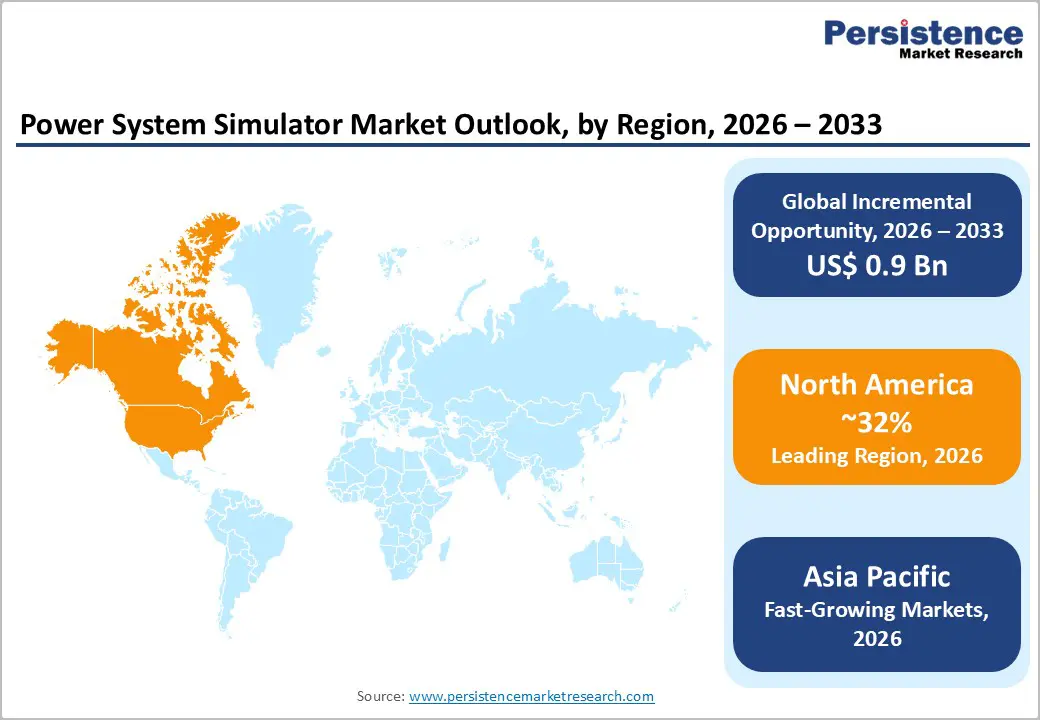

- Leading Region: North America leads global power system simulator adoption with 32% market share in 2025, driven by aging grid infrastructure modernization, substantial utility investment, and strong engineering expertise supporting advanced grid analysis and operator training requirements.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region with 7.1% CAGR through 2033, driven by rapid electricity demand, aggressive renewable energy deployment, and grid expansion across China, India, and ASEAN, supporting the world’s largest infrastructure development initiatives.

- Dominant Segment: Software solutions command a dominant 54% component segment share, reflecting specialized simulation platform requirements for comprehensive power system analysis across all application types globally.

- Fastest-Growing Segment: Transient stability analysis and electromagnetic transient simulation are the fastest-growing analysis segments, with a 7.9% CAGR through 2033, driven by challenges in integrating renewable energy that require sophisticated time-domain evaluation of grid dynamics.

- Key Opportunity: Hardware-in-the-loop and digital twin technologies represent a key market opportunity with a 7.8% CAGR through 2033, enabling real-time equipment testing, operator training, and grid optimization, supporting the renewable energy transition and smart grid development initiatives.

| Key Insights | Details |

|---|---|

|

Power System Simulator Market Size (2026E) |

US$ 1.7 billion |

|

Market Value Forecast (2033F) |

US$ 2.6 billion |

|

Projected Growth CAGR(2026-2033) |

6.1% |

|

Historical Market Growth (2020-2025) |

5.7% |

Market Dynamics

Drivers - Renewable Energy Integration and Grid Modernization Requirements

The exponential growth in renewable energy deployment globally creates a critical need for advanced power system simulators capable of managing grid complexity and instability risks. Global renewable electricity capacity reached 3,700 GW in 2022, according to international energy data, with solar and wind generation continuing to expand rapidly. Renewable energy sources introduce variable generation patterns, frequency regulation challenges, and voltage stability concerns requiring sophisticated simulation and analysis capabilities.

Utilities worldwide are investing heavily in grid modernization initiatives to accommodate distributed renewable generation, enhance system resilience, and enable seamless integration of electric vehicles and energy storage systems. Europe, China, and the United States are leading renewable energy deployment, driving substantial investments in simulators for grid planning, protection scheme validation, and operator training. Advanced simulators enable utilities to conduct comprehensive load flow, short-circuit, harmonic, and transient analyses, which are essential for ensuring reliable operation in renewable-dominant grids and directly supporting the accelerating energy transition.

Smart Grid Development and Digital Transformation of Utilities

Smart grid initiatives across developed and emerging economies are driving substantial adoption of power system simulators as utilities transition toward digitalized, automated, and increasingly autonomous grid operations. Smart grid concepts require real-time monitoring, advanced control systems, and sophisticated operator training platforms that power system simulators provide. Governments globally are investing in smart grid infrastructure, with the U.S. Department of Energy allocating over US$ 65 billion for grid modernization, while Europe and the Asia-Pacific regions are implementing comparable programs.

Digital transformation of utility operations requires simulator capabilities for operator training, system design validation, cybersecurity testing, and emergency response planning. Major utilities, including Duke Energy, EDF, and State Grid of China, are deploying advanced simulator systems supporting real-time hardware-in-the-loop testing, digital twin applications, and artificial intelligence-driven grid optimization. These investments underscore the critical role that power system simulators play in enabling utility digital transformation and supporting the global transition toward smart, resilient, and sustainable power systems.

Restraint - High Initial Capital Investment and Operational Complexity

Implementing comprehensive power system simulator solutions requires substantial upfront capital investment in specialized hardware, software licenses, and integration services that can exceed US$ 5-10 million for large-scale implementations. Smaller utilities and developing-nation power companies face significant financial barriers to acquiring and maintaining advanced simulator systems. Beyond capital requirements, operating sophisticated simulators demands highly trained personnel with specialized expertise in power systems, software platforms, and real-time simulation technologies.

The scarcity of qualified simulator technicians and engineers limits adoption in regions with less developed technical talent pools. Maintenance, updates, and licensing fees create ongoing operational costs that strain budgets at utilities with limited financial resources. Legacy grid infrastructure in many developing nations requires substantial upgrades before advanced simulators can deliver meaningful value, further limiting the addressable market size.

Integration Challenges with Legacy Systems and Cybersecurity Concerns

Integrating modern power system simulators with existing SCADA systems, EMS platforms, and legacy infrastructure presents substantial technical and operational challenges. Many utilities operate aging grid infrastructure developed decades ago with incompatible communication protocols, data formats, and control architectures. The increasing connectivity of simulator systems with operational grids creates cybersecurity vulnerabilities that utilities must carefully manage. Interconnecting simulators to real-time grid operations introduces cyber-attack risks that could compromise grid reliability and security. Regulatory requirements for grid security compliance add to implementation complexity and costs. Many utilities prioritize immediate grid reliability concerns over simulator investments, deferring modernization in financially constrained environments.

Opportunity - Hardware-in-the-Loop and Digital Twin Technologies in Renewable Integration

Hardware-in-the-Loop (HIL) simulation and digital twin technologies represent rapidly growing opportunity segments, with a projected 7.8% CAGR through 2033, significantly exceeding overall market growth. HIL simulation enables real-time testing of protective relays, control systems, and renewable energy inverters in virtualized grid environments before deployment in operational systems. Digital twin applications create virtual replicas of physical power systems, enabling operators to conduct training, test emergency response procedures, and optimize grid operations without impacting live systems. Transient stability analysis and electromagnetic transient simulation using HIL platforms are becoming essential for validating grid-forming inverters and advanced power electronics deployed in renewable-heavy grids.

Major equipment manufacturers, including Siemens, ABB, and General Electric, are integrating HIL capabilities into simulator platforms to support equipment manufacturers and utilities. The IEEE and international standards bodies are establishing guidelines for HIL testing in renewable grids, creating regulatory drivers for adoption. This rapidly expanding technology segment offers substantial revenue opportunities for simulator vendors offering integrated HIL and digital twin capabilities.

Emerging Market Grid Development and Energy Access Initiatives

Developing economies across Africa, South Asia, and Latin America are investing substantially in expanding electricity infrastructure and modernizing grids to support economic growth and universal energy access objectives. These nations face particular challenges in managing distributed generation, limited technical expertise, and aging transmission systems that power system simulators can address cost-effectively. Regional development banks, including the World Bank and the Asian Development Bank, are financing grid modernization projects that require simulator capabilities for planning, design validation, and operator training.

Countries including India, Nigeria, and Indonesia are deploying advanced simulators to support national renewable energy targets and improve grid reliability. Training and education applications represent particularly attractive opportunities, as emerging-market utilities often lack local expertise for grid analysis and require simulator-based training platforms. Vendors offering cost-effective simulator solutions, localized support, and training services are well positioned to capture the growing demand in developing regions. The combination of rising electricity demand, renewable energy deployment targets, and limited existing simulator infrastructure creates substantial growth opportunities in emerging markets.

Category-wise Analysis

Component Insights

Software solutions represent the leading component segment, commanding approximately 54% market share in 2025, reflecting the dominant role software plays in power system simulation. Specialized simulation software platforms, including PSSE, ETAP, Neplan, and DIgSILENT PowerFactory, provide comprehensive capabilities for load flow, short circuit, harmonic, and transient analyses essential for grid planning and operation. Software flexibility, continuous updates supporting new grid technologies, and scalability across different utility sizes and grid complexities support market dominance.

Cloud-based and software-as-a-service SaaS simulator platforms are expanding accessibility for smaller utilities and consultants. Software modularity enables utilities to adopt solutions incrementally, reducing implementation barriers compared to comprehensive hardware systems. Ongoing licensing revenues and subscription-based models create stable streams of revenue, supporting vendor investments in continuous product development and innovation.

Analysis Insights

Load flow analysis represents the leading analysis type segment, accounting for approximately 41% market share in 2025, reflecting its fundamental importance in power system planning and operation. Load flow analysis enables utilities to determine voltage magnitudes, phase angles, and power flows throughout transmission and distribution networks under various operating conditions. Load flow studies are essential for transmission planning, generation dispatch optimization, and transmission congestion management in competitive electricity markets.

Every major utility conducts routine load flow analysis to validate system designs, evaluate network reinforcements, and ensure compliance with stability standards. The established nature of load flow analysis, standardized methodologies, and widespread utility adoption support sustained market share leadership. However, transient stability analysis and electromagnetic transient simulation are the fastest-growing analysis types, with a projected 7.9% CAGR through 2033, driven by renewable energy integration challenges requiring sophisticated time-domain analysis of fast-acting power electronics and grid dynamics.

End-user Insights

Power generation applications represent the leading end-use segment, commanding approximately 48% market share in 2025, reflecting utilities’ foundational requirement for simulator capabilities in generation planning and operation. Power generation simulators support generator protection coordination, excitation system tuning, governor response optimization, and black-start procedure validation, all of which are essential for system reliability.

Hydroelectric, thermal, and nuclear generating stations use simulators for operator training, validation of startup procedures, and emergency response planning. Renewable energy generating facilities, including wind farms and solar installations, increasingly utilize simulators for power plant control system testing and grid code compliance validation. Independent power producers and generation companies deploy simulators for equipment procurement decisions and operational planning.

Regional Insights

North America Power System Simulator Market Trends and Insights

North America represents the largest power system simulator market with approximately 32% global market share in 2025, driven by advanced grid infrastructure, substantial utility investment in modernization, and strong engineering expertise. The United States dominates regional adoption, with major utilities such as Duke Energy, American Electric Power, and Southern Company deploying comprehensive simulation systems to support grid planning and operations. Federal initiatives, including the Department of Energy’s Grid Modernization Lab Consortium, are accelerating simulator adoption and technology innovation across the region.

The region’s aging transmission infrastructure, combined with rapid growth in renewable energy, creates substantial demand for simulators to plan grid upgrades and validate new protection schemes. North American utilities are increasingly adopting real-time digital simulation platforms supporting operator training for complex grid scenarios, including widespread renewable generation. Cybersecurity requirements for critical infrastructure protection are driving the adoption of hardware-in-the-loop testing capabilities for validating control system resilience.

Europe Power System Simulator Market Trends and Insights

Europe is the second-largest power system simulator market with particularly strong demand in Germany, France, and the United Kingdom. European utilities face particularly challenging grid integration requirements as renewable energy sources exceed 50% of electricity generation in countries including Denmark, Germany, and Portugal. The European Union’s ambitious climate targets and renewable energy deployment requirements are driving substantial utility investment in simulation capabilities to manage increasingly complex grid operations.

European grid operators, including Tennet, RTE, and National Grid, are deploying advanced simulators supporting real-time training and grid analysis. The region’s stringent reliability standards, interconnected multinational grids, and aggressive renewable energy targets create strong incentives for investment in simulators. Germany’s Energiewende and France’s nuclear transition policies are driving specific simulator requirements for managing grid stability with high renewable penetration.

Europe is projected to see continued integration of renewable energy and smart grid development, supporting sustained market expansion. The region’s technological leadership and established utility modernization budgets ensure continued robust adoption of simulators.

Asia Pacific Power System Simulator Market Trends and Insights

Asia Pacific is the fastest-growing power system simulator market with a projected 7.1% CAGR through 2033. China represents the dominant regional market, with State Grid of China deploying massive simulator capabilities supporting world’s largest power system operations. Rapid electricity demand growth, aggressive renewable energy deployment, and extensive grid expansion create substantial simulator demand across the region.

India’s rapidly modernizing power system, combined with government targets to exceed 500 GW of renewable energy capacity by 2030, is driving accelerated adoption of simulators across utilities and system operators. Japan’s renewable energy integration, following nuclear power reductions, and ASEAN countries’ development of regional power markets, create growing simulator demand.

Regional power equipment manufacturers are increasingly investing in simulator capabilities for control system testing and export market support. The region’s rapid industrialization, urbanization, and electrification requirements, combined with enormous renewable energy deployment, are driving the fastest-growing simulator market globally, as utilities require capabilities to manage unprecedented grid complexity and modernization challenges.

Competitive Landscape

The global power system simulator market features a moderately consolidated structure shaped by high technical entry barriers, long sales cycles, and strong customer reliance on proven simulation accuracy. Market leadership is held by established technology providers offering comprehensive software platforms supported by decades of grid modeling expertise and deep integration with utility workflows. Competitive differentiation is increasingly driven by advanced real-time simulation, hardware-in-the-loop capabilities, and digital twin functionality that support renewable integration, grid resilience, and operator training.

Vendors are expanding cloud-based and subscription deployment models to improve scalability and reduce upfront investment for utilities and research institutions. Strategic alliances with grid equipment manufacturers, system integrators, and utilities are strengthening end-to-end solution offerings and embedding simulators within broader smart grid ecosystems. Continuous investment in artificial intelligence, automation, and cybersecurity features is enhancing analytical depth and operational relevance. Meanwhile, emerging open-source and modular solutions are introducing price competition, encouraging established players to focus on value-added services, customization, and long-term support contracts.

Key Market Developments:

- March 2025: ETAP and NVIDIA ETAP introduces the world’s first Electrical Digital Twin to simulate AI Factory power from grid to chip level using NVIDIA Omniverse, enabling advanced energy efficiency, predictive maintenance, and reduced costs through precise power management and dynamic scenario analysis.

- July 2025: ABB and SimGenics signed an MoU to develop simulator-based solutions for training, testing, and verification of nuclear plant operations in North America, covering conventional large plants, SMRs, and AMRs. The collaboration supports greenfield power generation, enhances safety, efficiency, and operational skills through realistic simulations, aligning with US and Canadian policies for next-generation nuclear technology deployment.

- October 2025: Vicor and Silvaco Vicor adopts Silvaco’s Victory TCAD 3D simulation solution for accurate power device modeling and simulation, transitioning from 2D to 3D to better capture complex effects, accelerate development, and improve reliability in high-density power modules.

- October 2025: OPAL-RT TECHNOLOGIES launches SPS Software, a new platform ensuring 100% compatibility with previous SimPowerSystems versions, synchronized with MATLAB releases, and supporting Windows initially, with Linux and MATLAB Online to follow, strengthening commitment to SPS users in power systems simulation.

Companies Covered in Power System Simulator Market

- Siemens

- ABB

- Eaton

- The MathWorks, Inc.

- RTDS Technologies Inc

- Fuji Electric Co., Ltd.

- General Electric Company

- ETAP (Operation Technology, Inc.)

- OPAL-RT TECHNOLOGIES, Inc.

- PSI Neplan AG

- DIgSILENT GmbH

- CEPEL (Centro de Pesquisas de Energia Elétrica)

- Powertech Technology Inc.

- Typhoon HIL Inc.

- Silvaco Group, Inc.

- Powersim Software AS

- PowerWorld Corporation

- PSCAD

- SKM System Analysis, Inc.

Frequently Asked Questions

The power system simulator market is projected to reach US$ 1.7 billion in 2026, growing from US$ 1.2 billion in 2020.

Rising renewable energy integration, smart grid modernization, aging grid infrastructure, and increasing operator training needs are the key drivers.

North America leads the market, while Asia Pacific is the fastest-growing region.

Hardware-in-the-loop and digital twin simulation technologies represent the strongest growth opportunity.

Key market players include Siemens, ABB, General Electric Company, The MathWorks, Inc., RTDS Technologies Inc, ETAP, and OPAL-RT TECHNOLOGIES, Inc.,