- Medical Devices

- Portable Ultrasound Devices Market

Portable Ultrasound Devices Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Portable Ultrasound Devices Market by Product (Laptop-Based, Cart-Based, Tablet-Based, and Handheld), by Application (Gynecology, Urology, Musculoskeletal, Cardiovascular, and Others), by End-user (Hospitals, Diagnostics Centers, Specialty Clinics, Ambulatory Surgery Centers, and Others), and Regional Analysis from 2025 to 2032

Portable Ultrasound Devices Market Share and Trends Analysis

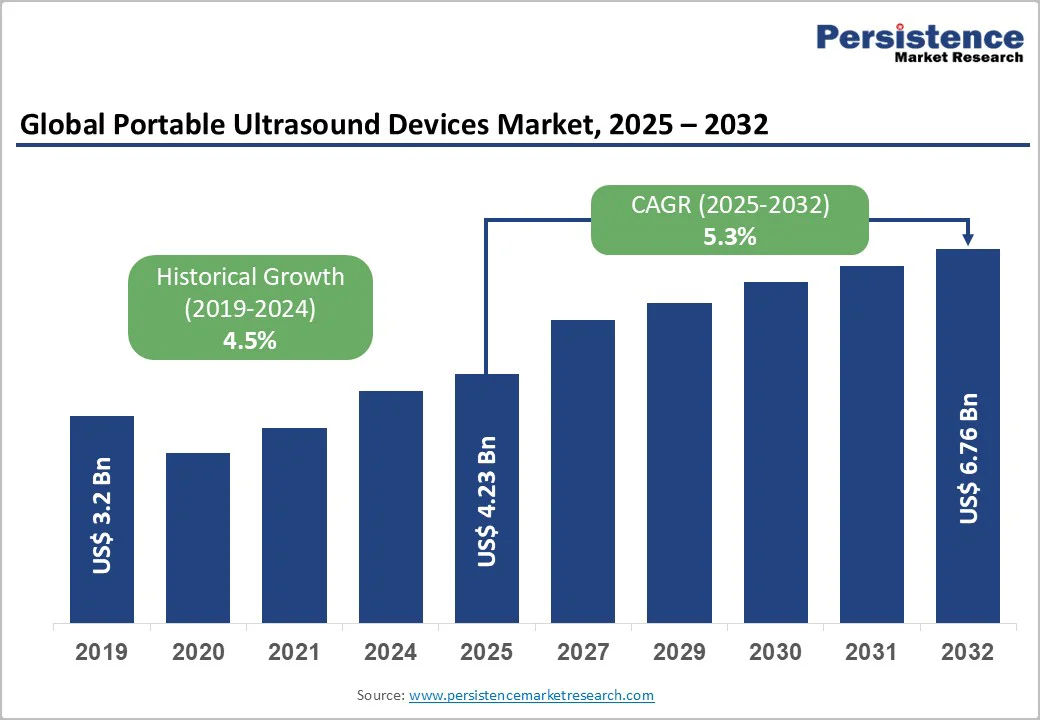

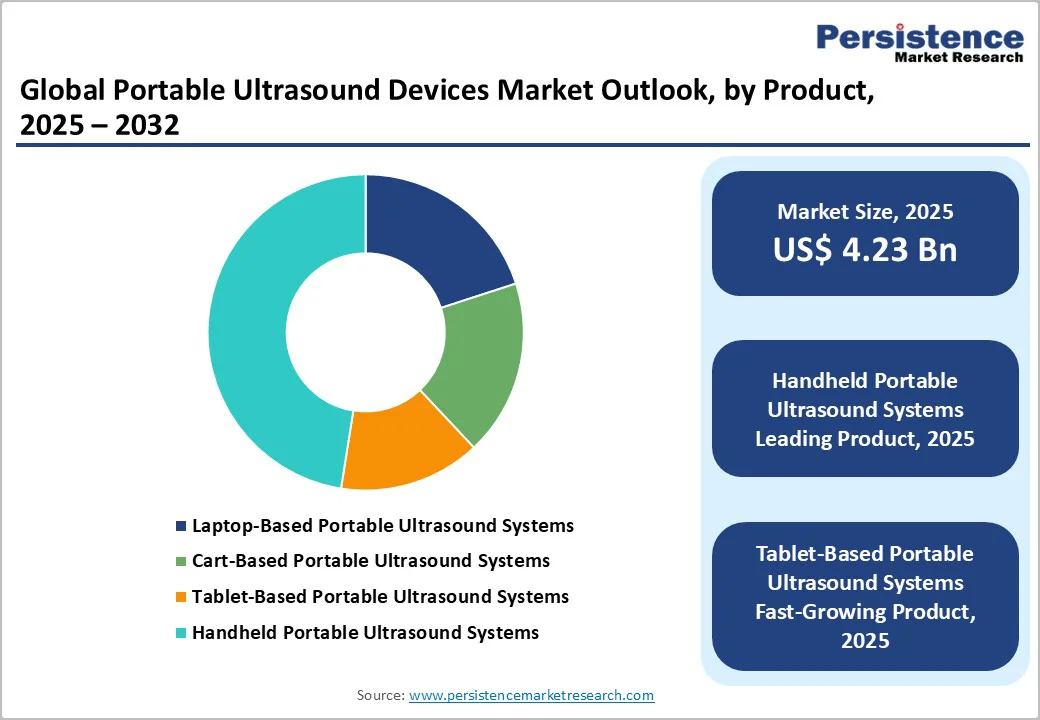

The global portable ultrasound devices market size is valued at US$ 4.23 billion in 2025 and projected to reach US$ 6.76 billion, growing a CAGR of 5.3% during the forecast period from 2025 to 2032.

Global demand for portable ultrasound devices is rising as the incidence of chronic and acute conditions, including cardiovascular diseases, maternal and fetal complications, abdominal disorders, and trauma-related injuries, continues to increase worldwide. The rise in the geriatric population, higher hospitalization rates, and the expanding use of point-of-care imaging in emergency and critical care settings are driving broader clinical adoption.

Key Industry Highlights

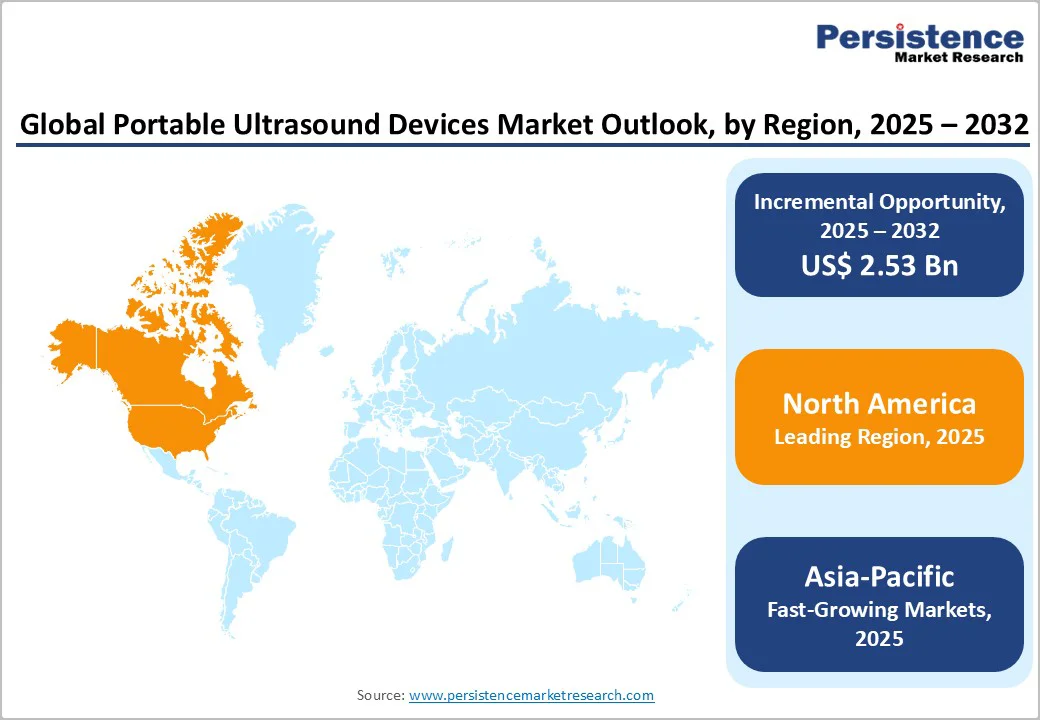

- Leading Region: North America dominates the global Portable Ultrasound Devices market with a share value of 40.2%, driven by advanced healthcare infrastructure, high adoption of point-of-care imaging, widespread use in emergency, cardiac, and prenatal care, and integration of AI-enabled and wireless imaging systems in hospitals and clinics.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, supported by rising incidence of chronic and maternal health conditions, rapid expansion of tertiary-care hospitals, increasing healthcare expenditure, and growing adoption of portable ultrasound systems in outpatient, home-care, and emergency services.

- Leading Product Segment: Handheld portable ultrasound systems lead the market due to their compact design, ease of use at point-of-care, high diagnostic reliability in ICUs and emergency settings, and strong hospital preference for rapid bedside imaging in trauma, prenatal, and surgical care.

- Fastest-Growing Product Segment: Tablet-based portable ultrasound systems are the fastest-growing segment, supported by lightweight and portable designs, wireless connectivity, integration with digital monitoring and AI-assisted imaging, and increasing use in ambulatory care, home diagnostics, and remote healthcare delivery.

- Leading Application Segment: Gynecology dominates the market, as hospitals, maternity centers, and outpatient clinics require portable imaging for prenatal, fertility, and diagnostic procedures, supporting efficient workflow, bedside monitoring, and improved maternal-fetal care.

- Fastest-Growing Application Segment: Musculoskeletal imaging represents the fastest-growing segment, driven by rising demand for early diagnosis of joint, tendon, and soft-tissue disorders, increasing adoption of portable ultrasound in rehabilitation and sports medicine, and growing use in outpatient and home-care settings.

| Key Insights | Details |

|---|---|

| Portable Ultrasound Devices Market Size (2025E) | US$ 4.23 Bn |

| Market Value Forecast (2032F) | US$ 6.76 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.5% |

Market Dynamics

Driver - Increasing Adoption of point-of-care ultrasound (POCUS) and Advancements in AI-Enabled Portable Ultrasound Technologies

Surging adoption of point-of-care ultrasound (POCUS) across emergency medicine, anesthesia, trauma care, and primary care is driving strong demand for handheld and tablet-based portable systems, as clinicians increasingly rely on them for rapid triage, bedside assessments, and guided procedures such as nerve blocks and central line insertions.

The rise in global burden of cardiovascular, pulmonary, and musculoskeletal diseases, where portable ultrasound enables quick, radiation-free evaluations in clinics, ambulatory centers, and underserved regions, accelerates and strengthens its role in decentralized diagnostics.

For instance, in July 2022, the World Health Organization reported that approximately 1.71 billion people worldwide suffer from musculoskeletal conditions, which drives portable ultrasound devices market growth.

Technological innovation in AI, wireless probes, and advanced battery systems is rapidly boosting portable ultrasound adoption. Clinicians now use AI-driven measurements, automated interpretation, and high-resolution micro-convex probes for faster, more accurate point-of-care diagnostics.

For instance, in April 2024, GE HealthCare launched Caption AI on the Vscan Air SL, enabling real-time guided imaging and automated ejection fraction analysis. Cloud-enabled PACS connectivity, rugged handheld designs, and multi-probe support are further enhancing use in emergency and ambulatory settings while reducing training barriers for non-radiology clinicians.

Restraints - Performance Limitations, High Ownership Costs, and Reimbursement Barriers

Handheld and compact portable ultrasound systems continue to face limitations in imaging depth and modality performance, particularly for deep abdominal, obese-patient, and advanced cardiac assessments.

Restricted Doppler functionality, limited elastography, and lower sensitivity in low-contrast scenarios reduce confidence in high-acuity settings, prompting hospitals to rely on cart-based or fixed consoles for detailed evaluations. This performance gap prevents portable systems from becoming primary imaging tools.

Moreover, in many regions, inconsistent reimbursement policies for point-of-care ultrasound (POCUS) exams, combined with the absence of standardized credentialing frameworks, create medico-legal and financial challenges for providers. These issues discourage large-scale POCUS deployment, especially in primary care and rural settings.

Additionally, the total cost of ownership remains high in resource-limited markets due to recurring expenses such as software subscriptions, probe replacements, maintenance contracts, and cloud storage. Mid-range compact models also remain expensive for low-income clinics, and shorter device lifecycles add to overall costs-constraining adoption despite strong clinical need.

Opportunity - Expansion of Home Healthcare Ecosystems and Advancements in Smart Cylinder Technologies

The rise of home healthcare, telemedicine, and remote monitoring is creating significant opportunities for portable ultrasound devices, driven by growing demand for wireless, smartphone-enabled systems that support pregnancy screening, chronic disease management, and rapid at-home evaluations.

Cloud-based image sharing and artificial intelligence (AI)-assisted interpretation enable specialists to guide frontline workers remotely, strengthening decentralized diagnostics in the post-COVID landscape. Additionally, portable ultrasound is becoming vital in rural and underserved regions, providing low-infrastructure imaging for maternal health, infectious disease assessment, and general care.

Government- and NGO-supported primary healthcare initiatives are further accelerating adoption across India, Africa, Southeast Asia, and Latin America.

Furthermore, portable ultrasound use is also expanding across emergency medical services (EMS), military forces, and disaster-response teams that depend on rugged, shock-resistant devices for trauma triage, focused assessment with sonography for trauma (FAST) exams, and on-site procedural guidance. Increased investments in emergency preparedness and battlefield medicine are boosting procurement momentum.

Beyond traditional medical settings, the technology is gaining traction in sports medicine, physiotherapy, fertility care, and veterinary practice due to minimal regulatory barriers and strong practitioner willingness to adopt compact imaging tools. Growing consumer interest in digital health solutions is also boosting uptake of home pregnancy and wellness-oriented ultrasound platforms.

Category-wise Analysis

By Product, Handheld Portable Ultrasound Systems Dominate Globally Due to Portability and Critical-Care Versatility

The handheld portable ultrasound systems segment is projected to dominate the global portable ultrasound devices market in 2025, accounting for a revenue share of more than 40%. The segment’s strong performance is primarily driven by their compact design, ease of use at point-of-care, and essential role in emergency, ICU, and perioperative settings.

Handheld systems allow rapid imaging in trauma care, bedside diagnostics, and outpatient clinics, supporting faster decision-making. Integration with digital platforms and wireless connectivity further enhances their adoption in hospitals, specialty clinics, and remote care units.

Additionally, ongoing technological advancements such as AI-assisted imaging and 3D/4D visualization are expanding clinical applications. Rising demand for telemedicine and mobile diagnostics in rural and resource-limited settings is also boosting segment growth.

By Application, Gynecology Leads the Market Globally Due to Consistent High Demand for Imaging across Critical and Outpatient Care

The gynecology segment is projected to dominate the global portable ultrasound devices market in 2025, accounting for a revenue share of 42.4%. This is driven by the high volume of prenatal, fertility, and diagnostic procedures requiring real-time imaging. Hospitals and specialty clinics prefer portable systems to improve workflow efficiency, support outpatient consultations, and reduce patient transfer needs.

The expansion of women’s health programs, increased access to maternal care, and rising awareness of early diagnostics. Moreover, advancements in high-resolution imaging and Doppler technology are enhancing diagnostic accuracy during surgeries. The growing adoption of minimally invasive procedures and intraoperative imaging.

By End-user, Hospitals Lead the Market Globally Due to Advanced Infrastructure and Higher Adoption of Point-of-Care Imaging

The hospitals segment is projected to dominate the global portable ultrasound devices market in 2025, accounting for a revenue share of around 50%. Hospitals utilize portable ultrasound for emergency care, ICUs, operating rooms, and general wards, enabling rapid bedside diagnostics and continuous monitoring.

Rising hospitalization rates, growing demand for minimally invasive procedures, and adoption of advanced imaging protocols strengthen the segment’s dominance. Investments in training, integration with electronic health records (EHRs), and point-of-care workflow optimization further drive hospital adoption.

Additionally, hospitals are increasingly investing in AI-enabled ultrasound systems to improve diagnostic efficiency and accuracy. The expansion of multi-specialty centers and emergency response capabilities is further boosting demand for portable imaging solutions.

Region-wise Insights

North America Portable Ultrasound Devices Market Trends

The North America market is expected to dominate globally with a value share of 44.6% in the 2025, with the U.S. leading the region due to its advanced healthcare infrastructure, high adoption of point-of-care imaging, and widespread use of portable ultrasound in emergency, cardiac, and prenatal care. Government initiatives supporting early diagnostics, high prevalence of chronic diseases, and rising geriatric population fuel demand.

The integration of AI-assisted imaging, wireless connectivity, and IoT-enabled monitoring further strengthens adoption across hospitals, surgical centers, and outpatient clinics. Moreover, increasing investments in telemedicine and mobile diagnostic services are expanding the reach of portable ultrasound devices. Growing collaborations between device manufacturers and healthcare providers are also facilitating faster deployment of advanced imaging solutions.

Europe Portable Ultrasound Devices Market Trends

The Europe market is expected to grow steadily, driven by investments in critical-care infrastructure, surgical facilities, and emergency services across Germany, France, and the UK. Increasing focus on maternal health, ICU imaging, and outpatient diagnostics supports demand for portable ultrasound devices.

Favorable reimbursement policies, technological advancements in compact imaging systems, and rising awareness of early disease detection among aging populations further drive market growth. Collaborations between healthcare providers and manufacturers enhance accessibility and operational efficiency.

Additionally, the adoption of AI-enabled and wireless ultrasound systems is improving diagnostic speed and accuracy across hospitals and clinics. Growing government initiatives to expand rural and home-based imaging services are further propelling market growth.

Asia Pacific Portable Ultrasound Devices Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 7.3% between 2025 and 2032, fueled by rising healthcare expenditure, urbanization, and increasing prevalence of chronic and maternal health conditions. Expansion of tertiary-care hospitals, government programs to improve rural diagnostics, and adoption of portable imaging in outpatient and home-care settings are key growth drivers.

The rise in medical tourism, advanced emergency services, and collaborations between local and global device manufacturers further enhance market penetration in countries like India, China, and Japan. Furthermore, increasing investments in AI-assisted portable ultrasound devices and telehealth solutions are enhancing diagnostic reach and efficiency.

Rising awareness of preventive healthcare and point-of-care imaging in semi-urban and rural regions is boosting market growth.

Competitive Landscape

The global portable ultrasound devices market is highly competitive, with major players such as GE HealthCare, Siemens, Koninklijke Philips N.V., SamsungHealthcare.com, FUJIFILM Holdings Corporation, and Shenzhen Mindray Bio-Medical Electronics Co., Ltd., leading through broad product portfolios, advanced imaging technologies, and strong distribution networks.

Manufacturers focus on compact, lightweight, and high-resolution devices, with innovations in AI-assisted imaging, wireless data transmission, and cloud-based diagnostics. Strategic initiatives include mergers and acquisitions, expansion of production capacities, partnerships with hospitals and specialty clinics, and development of portable systems for remote and point-of-care applications, strengthening competitive positioning globally.

Key Industry Developments:

- In November 2025, FUJIFILM Sonosite, Inc. introduced Sonosite MT, the newest addition to its range of portable ultrasound systems. Building on Sonosite’s dedication to providing durable, reliable, and user-friendly ultrasound technology with a strong focus on education, the Sonosite MT complements the acclaimed Sonosite PX, LX, and ST systems, further enhancing clinical imaging capabilities across diverse healthcare settings.

- In June 2025, Philips launched the Flash Ultrasound System 5100 POC, an advanced point-of-care (POC) ultrasound designed to meet the fast-paced demands of anesthesia, critical care, emergency medicine, and musculoskeletal imaging. Leveraging Philips’ expertise in cardiology and general imaging, the Flash 5100 POC offers outstanding image clarity, smart automation, and intuitive touchscreen controls in a compact, portable design.

- In July 2023, Konica Minolta Healthcare Americas, Inc. introduced the PocketPro H2, a wireless handheld ultrasound device designed for general imaging in point-of-care settings. In collaboration with Healcerion, Konica Minolta Healthcare renowned for its primary imaging solutions will distribute the PocketPro H2 in the U.S. for both human and veterinary applications, offering enhanced flexibility and cost-effective ultrasound solutions.

Companies Covered in Portable Ultrasound Devices Market

- GE HealthCare

- Siemens

- Koninklijke Philips N.V.

- SamsungHealthcare.com

- FUJIFILM Holdings Corporation

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- CANON MEDICAL SYSTEMS CORPORATION

- BenQ Medical Technology Corp.

- ALPINION MEDICAL SYSTEMS Co., Ltd.

- Hitachi Ltd.

- EDAN Instruments, Inc.

- Terason Division Teratech Corporation

- CHISON Medical Technologies Co., Ltd.

- Others

Frequently Asked Questions

The global portable ultrasound devices market is projected to be valued at US$ 4.23 Bn in 2025.

Rising demand for point-of-care imaging, increasing adoption of handheld and portable systems in hospitals, outpatient clinics, and emergency settings are driving the global portable ultrasound devices market.

The global portable ultrasound devices market is poised to witness a CAGR of 5.3% between 2025 and 2032.

Expanding use of portable ultrasound in telemedicine, home healthcare, and rural diagnostics are creating strong growth opportunities in the market.

GE HealthCare, Siemens, Koninklijke Philips N.V., SamsungHealthcare.com, FUJIFILM Holdings Corporation, and Shenzhen Mindray Bio-Medical Electronics Co., Ltd., are some of the key players in the portable ultrasound devices market.