- Home Appliances

- Ultra-Portable Speaker Market

Ultra-Portable Speaker Market Size, Share, and Growth Forecast 2025 - 2032

Ultra-Portable Speaker Market by Technology (Bluetooth, Wi-fi, Other), Distribution Channel (Retail, Online, Other), End User (Residential, Commercial), and Regional Analysis for 2025-2032

Ultra-Portable Speaker Market Size and Trend Analysis

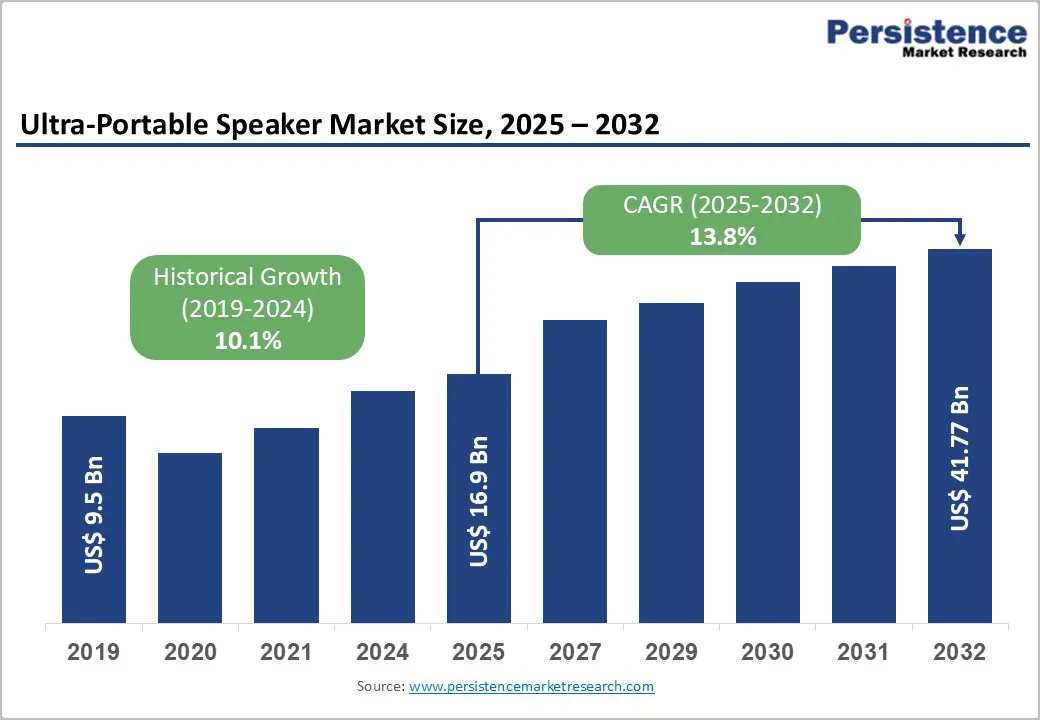

The global Ultra-Portable Speaker Market size is supposed to be valued at US$16.9 Bn in 2025 and is projected to reach US$41.8 Bn by 2032, growing at a CAGR of 13.8% between 2025 and 2032. The primary drivers include surging demand for wireless audio solutions and integration with smart devices, fueled by rising smartphone penetration and the adoption of streaming services worldwide. The integration of advanced technologies, including Bluetooth 5.3, voice assistant compatibility with Amazon Alexa and Google Assistant, and enhanced battery life exceeding 16-30 hours, has transformed ultra-portable speakers from simple audio devices into multifunctional smart companions.

According to the Recording Industry Association of America, more than 100 million paid music-streaming subscribers were in the U.S. alone in 2024, representing a significant increase from 75.5 million in 2020.

Key Market Highlights

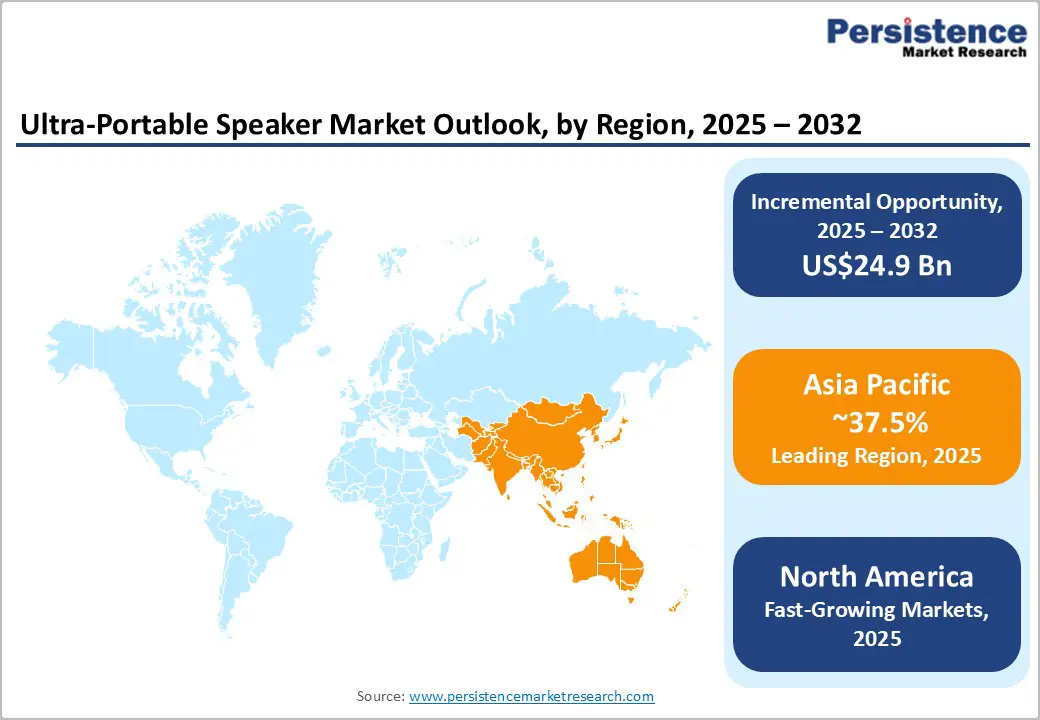

- Regional Leader: Asia Pacific dominates the market, with a market share of 37.5%, fueled by manufacturing in China and rising demand in India for affordable portable devices.

- Fastest Growing Region: North America emerges as the fastest growing region in the Ultra-Portable Speaker Market due to high innovation and consumer spending on wireless audio for outdoor and home use.

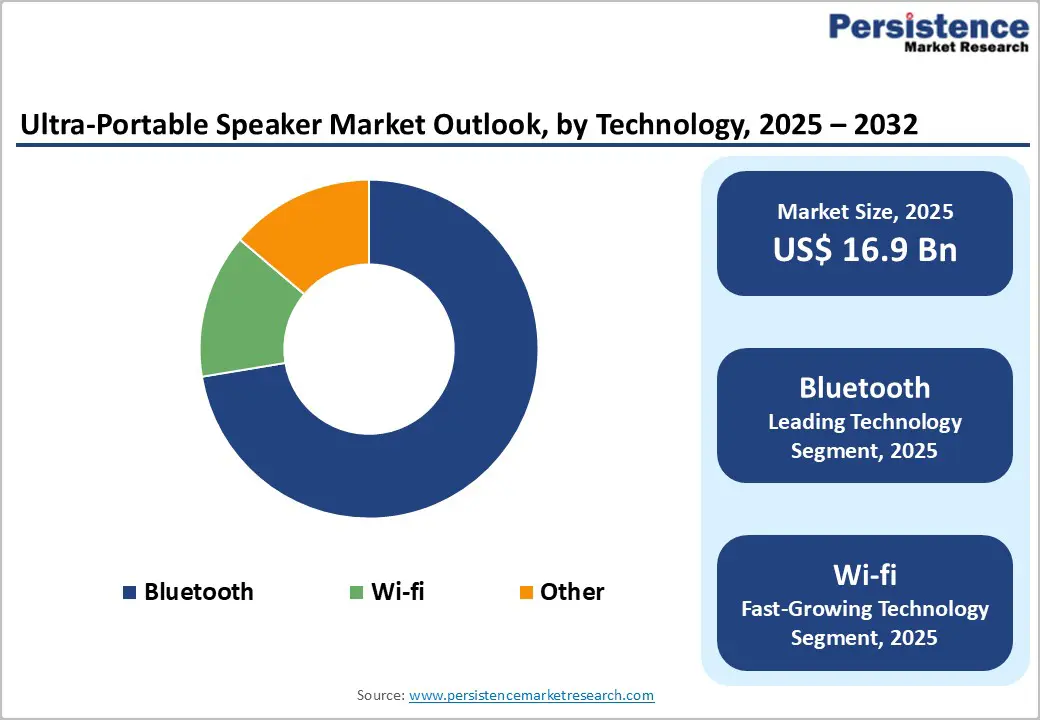

- Leading Segment: Bluetooth technology leads segments with 72.4% share, offering seamless connectivity for mobile entertainment needs.

- Fastest Growing Segment: Online distribution grows rapidly at 22% CAGR, driven by e-commerce accessibility and product variety.

- Growth Opportunities: Smart home integration presents key opportunities, enabling AI-enhanced audio across emerging ecosystems to drive sustained demand.

| Key Insights | Details |

|---|---|

| Ultra-Portable Speaker Market Size (2025E) | US$16.9 Bn |

| Market Value Forecast (2032F) | US$41.8 Bn |

| Projected Growth CAGR (2025-2032) | 13.8% |

| Historical Market Growth (2019-2024) | 10.1% |

Market Dynamics

Market Growth Drivers

Exponential Rise in Smartphone Adoption and Music Streaming Ecosystem Expansion

The unprecedented surge in global smartphone penetration is a cornerstone driver of the ultra-portable speaker market, with smartphone users projected to reach 5.28 billion by 2025 and 6.38 billion by 2029. Smartphones today serve as the primary hub for music, podcasts, and digital entertainment, driving strong demand for compact, high-fidelity bluetooth speakers that enhance the audio experience.

The proliferation of music streaming platforms has revolutionized audio accessibility, with global streaming subscribers reaching 818 million in 2024, a 12% year-over-year increase, according to the IMS Business Report 2025. Spotify alone accounted for a dominant 32% market share, with over 250 million subscribers. This streaming revolution, combined with platforms such as Amazon Music (11.1%) and YouTube Music (9.7%) holding 11.1% and 9.7% of global subscribers, motivates consumers to seek enhanced portable sound experiences through advanced Bluetooth speakers that deliver superior clarity, seamless connectivity, and multi-device compatibility across their digital ecosystems.

Accelerating Outdoor Recreation Culture and Adventure Tourism Fueling Demand for Rugged Audio Solutions

The growing popularity of outdoor activities and mobile entertainment lifestyles is propelling the Ultra-Portable Speaker Market, as consumers seek durable, weather-resistant audio solutions for camping, hiking, and events. The 2024 Outdoor Participation Trends Report shows that the outdoor recreation participation base grew 4.1% in 2023, to a record 175.8 million participants, representing 57.3% of the U.S. population. Europe saw approximately 1.1 billion tourism trips in 2022, a 23% increase from the prior year, driving regional demand for compact, battery-powered audio solutions.

Leading manufacturers, including JBL, Bose, and Sony, have responded by introducing IP67-rated speakers such as the Boombox 3, SoundLink Flex, and SRS-XB100, which withstand dust, water submersion up to 1 meter for 30 minutes. Growing participation in outdoor activities further amplifies demand, with innovations extending battery life to 16-32 hours.

Market Restraints

Intense Price Competition and Market Saturation Pressuring Manufacturer Profit Margins

The ultra-portable speaker market faces significant challenges from intense price competition and growing market saturation, particularly in mature regions where more than 50 active global players compete for market share. The influx of cost-effective alternatives from Chinese and regional manufacturers has intensified pricing pressures, forcing premium brands such as Bose, JBL, Sony, and Apple to continuously balance affordability with quality innovation while maintaining brand differentiation.

Raw material prices for lithium-ion batteries have surged 25% over the past year due to supply chain disruptions, according to the International Energy Agency (IEA), raising overall device pricing by 10-15%. This pricing barrier discourages mass adoption, particularly in price-sensitive markets, and intensifies competition from low-cost alternatives, potentially capping growth at 10% in emerging economies.

Battery Technology Limitations and Extended Usage Constraints

Consumer expectations for extended battery life present substantive technical and economic barriers to market expansion. While premium brands, such as JBL and Marshall, promise playback times between 16 to 32 hours, real-world performance frequently falls short of manufacturer specifications due to variable volume levels, ambient temperature conditions, and utilization of power-intensive features. For instance, the Bose SoundLink Max offers approximately 20 hours of playback, while Sony's SRS-XB100 provides around 16 hours; however, both experience reduced runtime when using high-volume playback, RGB lighting effects, or multi-speaker wireless pairing.

The integration of voice assistants, wireless connectivity features, and high-fidelity audio processing accelerates battery drain, creating user frustration during extended outdoor activities. Frequent recharging requirements undermine the primary value proposition of portable audio devices and may deter consumers considering premium-priced options.

Market Opportunities

Integration of Advanced Technologies and Smart Home Ecosystem Connectivity

The accelerating integration of AI-driven voice assistants into ultra-portable speakers represents a transformative growth opportunity that will revolutionize user interaction and expand market potential across smart home ecosystems. With over 87 million smart speakers shipped and 320 million voice-enabled devices in use, demand for seamless voice control is surging, pushing brands to offer multi-assistant compatibility.

This technological convergence is exemplified by products like JBL Authentics 300 and 500, which enable the concurrent operation of Alexa and Google Assistant simultaneously, providing unprecedented flexibility in voice command execution. The Wireless Audio Device Market, valued at US$ 65.8 Bn in 2025 with a projected CAGR of 13.7%, demonstrates the broader smart audio ecosystem's expansion potential. As ecosystems evolve, integrating AI assistants and IoT helps manufacturers capture premium segments, build long-term engagement, and stand out in a competitive market.

Expansion in Emerging Markets and Sustainability

Rapid economic growth across emerging Asia-Pacific economies, particularly India and other Southeast Asian regions, where rising urbanization and 5G adoption are boosting demand for affordable, eco-friendly ultra-portable speakers, is unlocking substantial market opportunities for portable speaker manufacturers. ASEAN consumer electronics spending is expected to grow 18% annually, according to the Economic Research Institute for ASEAN and East Asia (ERIA), aligning with sustainable initiatives that use recyclable materials.

Local manufacturers, including Xiaomi, BoAt, and Noise, are capturing market share through aggressively priced, feature-rich product portfolios that appeal to first-time buyers and budget-conscious consumers. The expansion trajectory presents manufacturers with opportunities to establish brand presence, develop manufacturing capabilities, and cultivate customer loyalty in markets with demographic and economic fundamentals that support sustained growth over extended forecast periods.

Category-wise Insights

Technology Analysis

Bluetooth dominates the technology segment in the Ultra-Portable Speaker Market with an approximate 72.4% market share, owing to its widespread compatibility, low energy consumption, and ease of pairing with consumer devices. The widespread adoption of Bluetooth 5.3 and emerging Bluetooth LE Audio with Auracast™ technology has significantly enhanced connection stability, extended transmission range up to 10 meters, and enabled superior audio quality with lower power consumption.

The technology's dominance is further reinforced by growing smartphone penetration that reached 4.88 billion users globally in 2024, with 77% penetration in the U.S. alone translating to 251.7 million active smartphone users demanding wireless audio solutions. Bluetooth speaker demand is particularly strong among millennials and Gen Z consumers who prioritize wireless convenience for outdoor activities, social gatherings, fitness routines, and commuting scenarios where cable-free operation provides essential mobility advantages.

Distribution Channel Analysis

Online channels dominate the ultra-portable speaker market, accounting for about 55% of distribution. This leadership is driven by the convenience and accessibility offered by e-commerce platforms and direct-to-consumer strategies. Marketplaces such as Amazon, Flipkart, and Alibaba provide extensive product choices, transparent pricing, and reliable delivery services, making them highly attractive to consumers.

Furthermore, these platforms offer customer reviews and detailed specifications, which help buyers make informed decisions. The growing preference for frictionless shopping experiences, combined with the rapid expansion of digital retail, reinforces the dominance of online channels in this segment. This trend reflects a broader shift toward digital purchasing in consumer electronics globally.

End User Analysis

Residential users command the end-user segment in the Ultra-Portable Speaker Market, holding about 71% market share, fueled by home entertainment needs and integration with streaming services. Consumers increasingly position compact speakers in kitchens, bathrooms, bedrooms, and outdoor spaces, transforming voice control into a default household interface for media consumption and home automation.

Residential consumers seek ultra-portable speakers that seamlessly sync with home entertainment systems, deliver superior sound quality for music streaming services like Spotify and Apple Music, and enhance interior aesthetics through sleek, minimalist designs that complement modern home decor. The segment benefits from continuous smart-home upgrades that maintain replacement cycles of fewer than four years, significantly shorter than historical averages for legacy components, thereby creating recurring revenue opportunities for manufacturers.

Regional Insights

North America Ultra-Portable Speaker Trends

North America drives the Ultra-Portable Speaker Market with robust innovation and high consumer spending on audio tech, particularly in the U.S., where outdoor lifestyles drive demand. The region's regulatory framework, including FCC standards for wireless emissions, ensures product safety and accelerates market entry for new devices. An innovation ecosystem bolstered by CES exhibitions has introduced features like IP68-rated waterproofing, with U.S. sales comprising 25% of global volume. Key developments include JBL's 2025 Boombox series, which enhances bass for recreational use.

Canada demonstrates parallel growth dynamics driven by similar outdoor recreational cultures and technology adoption patterns. Major brands maintain extensive distribution networks across organized retail channels, specialty electronics retailers, and dominant e-commerce platforms, ensuring widespread market availability.

Europe Ultra-Portable Speaker Trends

Europe's Ultra-Portable Speaker Market exhibits steady performance across Germany, the U.K., France, and Spain, supported by harmonized EU RoHS regulations promoting sustainable electronics. European consumers increasingly prioritize waterproof and water-resistant models for outdoor activities, with approximately 30% of buyers emphasizing waterproof features as critical purchase criteria. Germany leads with an engineering focus, where 25% of households own portable audio, per GfK data, emphasizing quality and energy efficiency. U.K. and France see growth from music festivals, with 15% rise in event-related sales.

EU regulatory frameworks governing electronic waste and energy efficiency drive manufacturer investment in durable, repairable speaker designs featuring sustainable materials and extended product lifecycles. Regulatory alignment facilitates cross-border trade, boosting 10% CAGR in eco-friendly models. Recent trends include Sony's ULT Field launches in 2025, targeting urban commuters in Spain.

Asia Pacific Ultra-Portable Speaker Trends

Asia Pacific is leading the Ultra-Portable Speaker Market, with 37.5% market share, propelled by manufacturing hubs in China, Japan, and India, alongside ASEAN dynamics. China's production advantages yield cost-effective devices, with exports rising 18% annually, according to China Customs. India's youth demographic drives a 20% surge in demand through affordable models, supported by Make in India policies.

Japan and South Korea sustain steady demand for high-end speakers emphasizing audio quality, technological sophistication, and premium brand positioning, while Southeast Asian countries, including Indonesia, Vietnam, Thailand, the Philippines, and Singapore, contribute dynamic growth driven by growing urbanization rates.

Competitive Landscape

Market Structure Analysis

The Ultra-Portable Speaker Market is moderately fragmented, with numerous players holding around 40% share, amid numerous mid-tier entrants fostering innovation. Companies pursue expansion through R&D in battery tech and partnerships, like audio-streaming integrations, to capture niches. Key differentiators include brand heritage and features such as 360-degree sound. Emerging models emphasize subscription ecosystems and sustainability, driving 15% efficiency gains.

Key Market Developments

- February 2025: Xiaomi Introduces Smart Speaker Pro with Advanced AI Processing (Xiaomi) expanded its smart speaker portfolio with the Smart Speaker Pro, featuring upgraded AI processing capabilities, balanced-armature drivers, and enhanced smart-home ecosystem integration.

- October 2024: Bose Corporation introduced the SoundLink Home portable Bluetooth speaker featuring crisp audio with room-filling bass, 9 hours of battery life, Bluetooth 5.3 connectivity, and USB-C audio input, available in Light Silver, Cool Grey, and Warm Wood finishes

- August 2024: Marshall Group AB unveiled exciting generational updates with Emberton III and Willen II portable speakers, offering powerful 360° sound with extended battery life of 32+ hours and 17+ hours, respectively.

Top Companies in the Ultra-Portable Speaker Market

Sony Corporation (Tokyo, Japan): A leader with diverse portfolios, Sony excels in sound innovation, generating significant revenue from the ULT series. Its influence stems from R&D investments exceeding US$5 Bn annually, ensuring premium quality and market maturity.

Harman International (JBL) (Stamford, USA): JBL dominates portability with rugged designs, boasting a strong portfolio in bass-heavy models.

Bose Corporation (Framingham, USA): Renowned for audio fidelity, Bose drives growth via noise-cancellation tech. Its maturity reflects portfolio strength in residential applications.

Companies Covered in Ultra-Portable Speaker Market

- Apple, Inc.

- Marshall Group AB

- Samsung Electronics

- Sony Corporation

- Harman International (JBL)

- Xiaomi

- Sennheiser Electronic SE & Co. KG

- BoAt

- Bose Corporation

- Koninklijke Philips N.V.

- LG Electronics

- Panasonic Corporation

- Anker Soundcore

- Bang & Olufsen

- Logitech

- Ultimate Ears

Frequently Asked Questions

The market is valued at US$16.9 Bn in 2025 and expected to reach US$41.8 Bn by 2032, growing at a 13.8% CAGR.

Key drivers include wireless connectivity advancements and rising outdoor entertainment, with smartphone integration boosting adoption by 20% annually.

Bluetooth leads with 72.4% share due to its compatibility and low latency for portable use.

Asia Pacific commands the largest market share at 37.5% in 2024, driven by China's 782.8 million smartphone users and sophisticated e-commerce ecosystems, and India’s growing middle-class consumer base.

Smart home integration offers growth via the integration of AI-driven voice assistants within ultra-portable speakers.

Leading players include Sony Corporation, Harman International (JBL), and Bose Corporation, focusing on innovation and durability.