- Smart Packaging

- Injection Molded Plastic Market

Injection Molded Plastic Market Size, Share, and Growth Forecast, 2026 - 2033

Injection Molded Plastic Market by Raw Materials (Polyethylene, Polypropylene, Others), Applications (Packaging, Automotive & Transportation, Others), Processes, and Regional Analysis for 2026 - 2033

Injection Molded Plastic Market Size and Trends Analysis

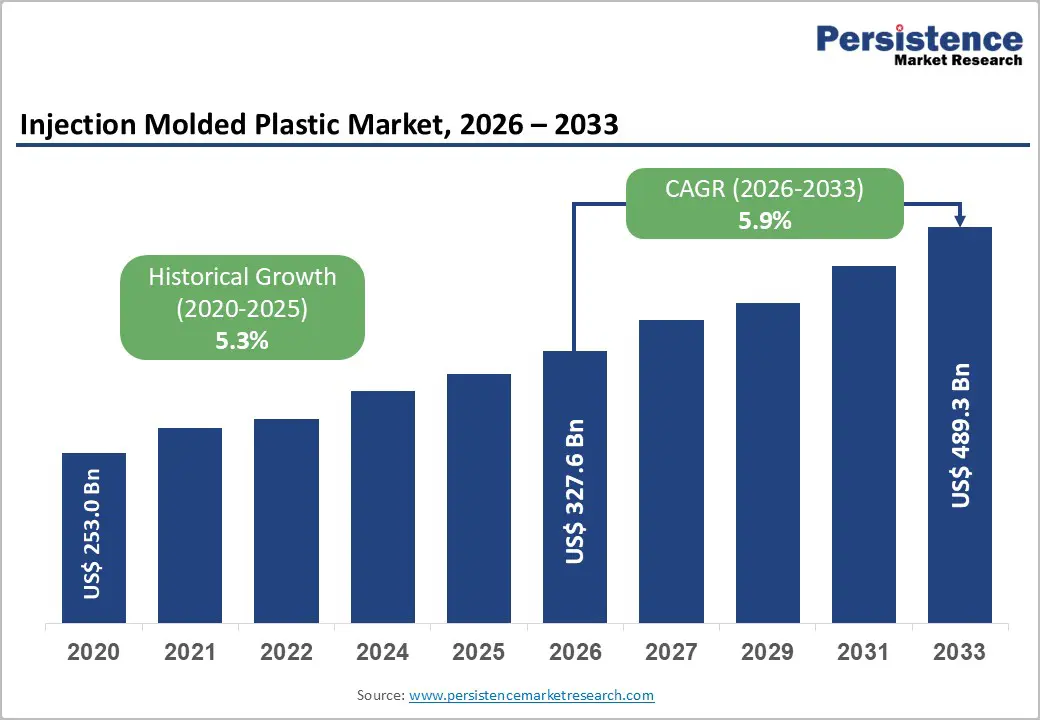

The global injection molded plastic market is likely to be valued at US$327.6 billion in 2026 and is expected to reach US$489.3 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033, driven by advancements in micro and two-shot molding, supply-chain regionalization, and polymer substitution toward higher-performance thermoplastics, which continue to accelerate value growth.

Feedstock price volatility and regulatory pressure on single-use plastics are reshaping product portfolios and driving investment into recycling, traceability, and process efficiency. OEMs and institutional buyers increasingly prioritize recyclability and material transparency in supplier selection.

Key Industry Highlights

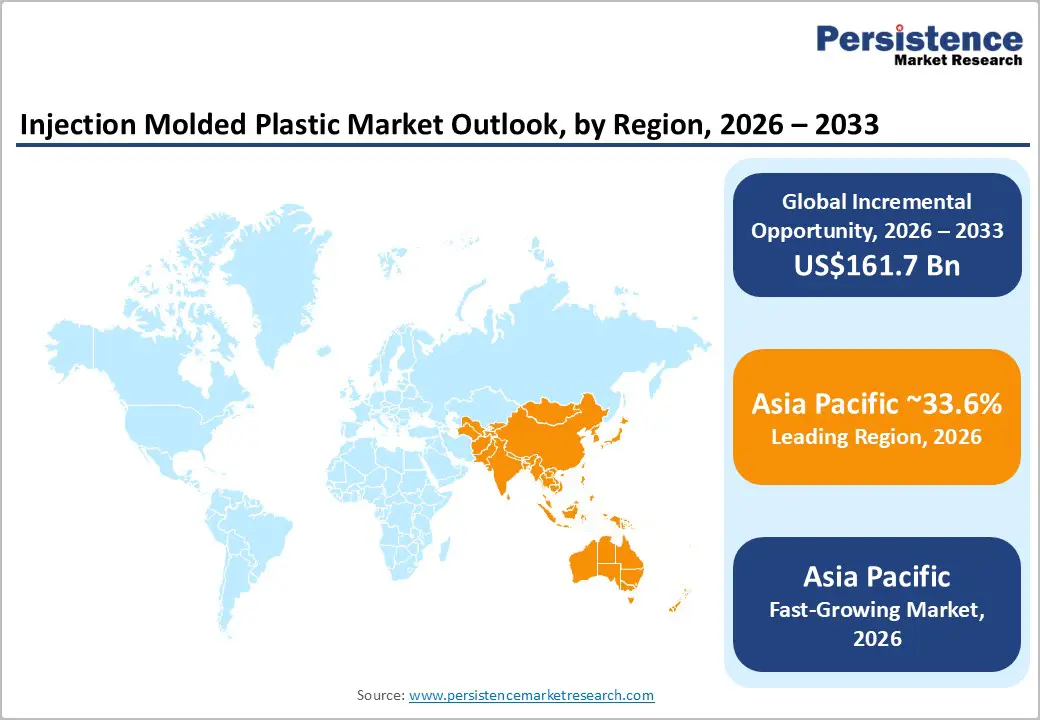

- Leading Region: Asia Pacific is projected to account for 33.6% of market share, driven by large-scale manufacturing capacity in China, strong automotive and electronics demand in Japan, and rapid growth in healthcare and consumer goods production across India and ASEAN economies.

- Fastest-growing Region: Asia Pacific, supported by expanding domestic consumption, cost-competitive production economics, and ongoing supply-chain diversification initiatives by global OEMs and brand owners.

- Investment Plans: Capital investments are focused on automation, electric and hybrid injection molding machines, cleanroom expansions for medical applications, and nearshoring capacity in North America, alongside closed-loop recycling and energy-efficient molding technologies in Europe to meet regulatory and sustainability requirements.

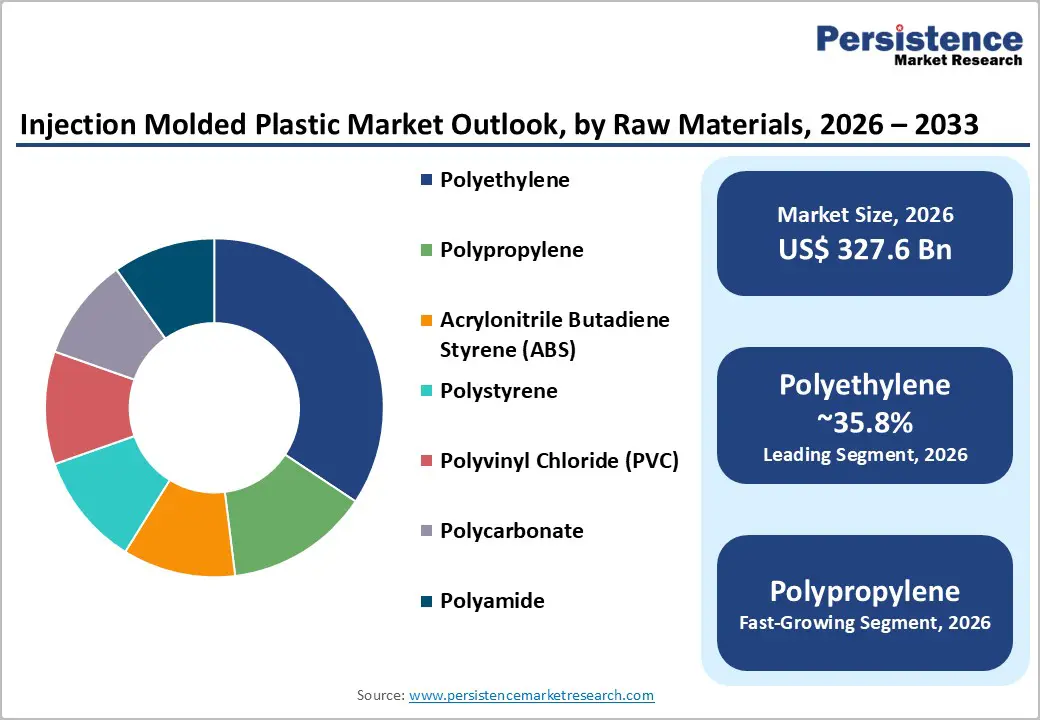

- Dominant Raw Materials: Polyethylene is anticipated to hold approximately 35.8% market share, due to its low cost, high processability, and extensive use in high-volume packaging, closures, and consumer goods applications.

- Leading Applications: Packaging is estimated to account for about 32.3% of market demand, driven by food and beverage, personal care, and e-commerce packaging requirements, supported by lightweighting and high-cavitation injection molding strategies.

| Key Insights | Details |

|---|---|

| Injection Molded Plastic Market Size (2026E) | US$327.6 Bn |

| Market Value Forecast (2033F) | US$489.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis -Packaging Demand and the Convenience Economy

Packaging remains the largest application segment by both value and volume through 2033. Global demand from the food, beverage, personal care, and e-commerce sectors continues to favor injection-molded components such as closures, caps, and rigid containers, thanks to high production speeds, low per-unit costs, and superior design flexibility. The packaging segment accounts for approximately 32.3% of market share, supporting sustained volume demand and scale efficiencies, particularly for commodity resins such as polyethylene. While upstream volatility in crude oil and monomer pricing creates short-term margin pressure, it does not materially alter mid-term structural demand. Ongoing lightweighting initiatives reduce material consumption per unit, enabling value capture through premium designs and multi-material closure systems.

Automotive Lightweighting and Electrification

Automotive and transportation represent the fastest-growing application segment, expanding at approximately 4.98% CAGR, driven by OEM priorities around lightweighting, modular design, and electrification. Injection molding enables the production of large, complex structural and interior components, fuel-system parts, and EV battery housings at lower weight than metal alternatives. The shift toward electric vehicles increases demand for high-performance polymers such as polyamide and polycarbonate blends, as well as advanced molding techniques, including two-shot and gas-assisted molding. These trends raise average selling prices per component and enable suppliers to capture greater system-level value through integrated assemblies and multi-material solutions.

Process Innovation and Automation

Advancements in micro injection molding, two-shot systems, and smart manufacturing platforms are significantly improving productivity and asset utilization. Automation reduces labor dependency and shortens ramp-up times for complex components, while sensor-based monitoring and predictive maintenance improve machine uptime and scrap reduction. These improvements expand the addressable market for injection molding into higher-value applications such as medical devices, optics, and precision electronics housings. Although capital intensity increases, the lifetime value of modernized facilities rises accordingly, encouraging consolidation among contract manufacturers and vertically integrated OEMs investing in advanced molding capabilities.

Barrier Analysis - Raw Material Price Volatility

Fluctuations in feedstock pricing across naphtha, ethylene, and polymer markets continue to compress margins for molded parts manufacturers, particularly those operating under fixed-price OEM contracts. Procurement volatility increases working capital requirements and complicates the pricing pass-through mechanisms, which are not always enforceable. For high-volume materials such as polyethylene, which holds approximately 35.8% of raw-material share, rapid cost movements can create a mismatch between input expenses and negotiated selling prices. When monomer prices rise by 20% within a quarter, typical contract structures recover only 50-70% of the increase in the same period, elevating credit and margin risk.

Regulatory and Sustainability Pressure

Stricter plastics regulations and extended producer responsibility (EPR) frameworks across Europe, North America, and parts of Asia-Pacific are increasing compliance costs and recycling obligations. These policies disproportionately affect single-use packaging and require manufacturers to invest in integrating recycled content, obtaining certification, and implementing takeback systems. Regulatory uncertainty around implementation timelines complicates capital planning, while constrained availability or price spikes in recycled resins can disrupt supply chains. Near-term compliance initiatives, including sorting infrastructure and material certification, typically add 0.5-2.0% to the cost of goods sold for mature packaging producers.

Opportunity Analysis - Recycled and Bio-Based Resins

The transition toward validated recycled and bio-based polymer content presents a material growth opportunity equivalent to a mid-single-digit percentage of global volume by 2030. Policy incentives and procurement mandates from large multinational buyers are accelerating demand for certified recycled polymers suitable for food-contact and technical applications. Suppliers that secure reliable feedstock through takeback programs or strategic partnerships and demonstrate consistent material performance can command pricing premiums and preferred supplier status. If packaging and consumer applications, which together account for more than half of total demand, adopt 5-10% post-consumer recycled content, this shift creates a multi-billion-dollar opportunity for qualified material and molding providers.

Regional Nearshoring and Contract Manufacturing

Supply-chain rebalancing toward nearshoring is generating new greenfield demand for injection molding capacity in North America, Eastern Europe, and Southeast Asia. OEMs increasingly prefer regional suppliers to reduce lead times, logistics risk, and tariff exposure for high-value components. Contract manufacturers offering integrated design-for-manufacturing capabilities, automation-first operations, and regional scale are well positioned to secure multi-year supply agreements. Capturing 3-5% of global production shifting to on-shore facilities implies multi-hundred-million-dollar investments in tooling and plant infrastructure per region through 2033.

Segmentation Analysis

Raw Materials Insights

Polyethylene is anticipated to account for approximately 35.8% of market share in 2026, making it the dominant resin category during the forecast period. Its leadership is driven by low material cost, excellent flow characteristics, chemical resistance, and broad applicability across packaging and consumer goods. Polyethylene is extensively used in high-volume closures, rigid containers, thin-wall packaging, household goods, and caps, where short cycle times and material efficiency are critical to profitability. Manufacturers with expertise in high-cavitation molds and thin-wall injection technologies achieve strong economies of scale and faster tooling amortization. Common commercial applications include food and beverage bottle caps, detergent closures, storage containers, and everyday consumer commodity products, predominantly utilizing HDPE and LLDPE grades.

Polypropylene is anticipated to be the fastest-growing raw material segment, supported by its favorable balance of stiffness, heat resistance, fatigue durability, and lower density compared with polyethylene. Rising demand from automotive interiors, under-hood components, EV battery housings, medical disposables, and durable consumer goods continues to accelerate PP adoption. Advanced PP compounds, including impact-modified, mineral-filled, and glass-filled grades, expand substitution opportunities against metals and heavier engineering plastics. These materials enable weight reduction, cost optimization, and enhanced performance, allowing compounders and converters to command higher average selling prices while improving margin profiles in technically demanding applications.

Applications Insights

Packaging is anticipated to remain the largest application segment, accounting for approximately 32.3% of market demand, driven by sustained growth in food and beverage, personal care, pharmaceutical packaging, and e-commerce distribution. Injection molding enables high-volume production of thin-wall containers, closures, caps, and rigid trays, primarily made from polyethylene and polypropylene. The process delivers low per-unit costs once tooling investments are amortized and enables consistent quality, tight tolerances, and enhanced aesthetic features such as textured surfaces and branding elements. Packaging manufacturers increasingly pursue lightweighting, downgauging, and material optimization strategies to reduce resin usage, lower transportation costs, and meet sustainability objectives without compromising product performance or shelf appeal.

Automotive and transportation applications are anticipated to register the highest growth rate, driven by electrification, vehicle lightweighting, and modular interior design. Injection-molded components, including battery enclosures, cable management systems, dashboards, door panels, air-intake manifolds, and underbody shields, are increasingly replacing traditional metal parts. The transition toward electric vehicles intensifies demand for fire-retardant, thermally stable, and structurally reinforced plastics, accelerating the adoption of engineering polymers and multi-shot injection molding processes. These trends increase part complexity and value density, enabling suppliers to improve margins while delivering integrated, weight-efficient automotive solutions.

Regional Insights

North America Injection Molded Plastic Market Trends - High-Complexity, Regulated Manufacturing Driven by Medical and EV Demand

North America represents a substantial share of high-value injection molded plastic demand, led overwhelmingly by the U.S., where technical complexity and regulatory rigor shape market structure. The region is a hub for advanced applications in medical devices, automotive systems, aerospace interiors, and electronics, where higher labor and compliance costs are offset by proximity to OEMs, shorter development cycles, and stronger pricing power. U.S.-based medical molders such as Phillips-Medisize, West Pharmaceutical Services, and Integer Holdings continue to expand cleanroom capacity to support demand for drug-delivery components, diagnostic consumables, and single-use medical devices.

Automotive and EV-driven demand is reinforced by OEMs such as Tesla, General Motors, and Ford, accelerating the adoption of injection-molded battery housings, thermal-management components, and lightweight interior modules. Tier-1 suppliers such as Magna International and Aptiv increasingly rely on highly automated molding cells to meet volume and precision requirements. Investment priorities across the region center on automation retrofits, robotics integration, digital quality control, and nearshoring initiatives, particularly along the U.S.-Mexico corridor, to strengthen supply-chain resilience. Regulatory requirements related to FDA compliance, product safety, and environmental standards raise entry barriers but structurally favor established, certified suppliers with long-term OEM relationships.

Europe Injection Molded Plastic Market Trends - Sustainability-Regulated Engineering Plastics and Automotive-Led Precision Molding

Europe combines strong demand for engineered injection-molded components with one of the world’s most advanced regulatory frameworks focused on sustainability, traceability, and circularity. Germany anchors regional performance through leadership in automotive manufacturing, industrial machinery, and polymer compounding, supported by companies such as BASF, Covestro, and Röchling Group, which supply high-performance materials and precision components. Automotive OEMs, including Volkswagen, BMW, and Mercedes-Benz, increasingly specify lightweight, recyclable plastic modules for interiors, structural reinforcements, and EV platforms.

The U.K. and France sustain demand for medical and precision molding, with suppliers supporting pharmaceutical packaging, diagnostic devices, and laboratory consumables. Spain and Italy maintain a strong base in rigid packaging and closures, supplying food, beverage, and personal-care brands. EU-wide regulatory harmonization, particularly under circular-economy and recycled-content mandates, raises compliance and certification requirements, increasing operational complexity for converters. These regulations also create structural demand for traceable recycled polymers, benefiting companies investing in closed-loop recycling, digitalized molding operations, and energy-efficient production technologies, including electric injection molding machines and smart factory systems.

Asia Pacific Injection Molded Plastic Market Trends - Scale-Driven Growth Anchored by China Manufacturing and Emerging Regional Hubs

Asia Pacific is anticipated to hold the largest global market share at 33.6% in 2026, and remains the fastest-growing regional market, supported by large-scale manufacturing capacity, expanding consumer demand, and cost-competitive production economics. China dominates regional output and export volumes, particularly in packaging, consumer goods, and electronic housings, supported by vertically integrated manufacturers and global suppliers such as Haitian International and Yizumi, which provide high-volume injection-molding machinery. Multinational brand sourcing for household goods and electronics continues to reinforce China’s scale advantage.

Japan focuses on high-precision injection molding, supplying automotive, electronics, and optical components for OEMs such as Toyota, Honda, Sony, and Panasonic, where tolerance control and material performance are critical. India demonstrates rapid growth in healthcare disposables, medical packaging, and consumer electronics enclosures, driven by rising domestic demand and government initiatives supporting local manufacturing. ASEAN economies, including Vietnam, Thailand, and Indonesia, attract increasing investments as cost-competitive manufacturing hubs, supporting regional supply-chain diversification. Environmental regulations remain uneven across Asia Pacific, creating short-term compliance challenges while opening long-term opportunities for local recycling infrastructure, sustainable resin adoption, and regional material sourcing strategies.

Competitive Landscape

The global injection molded plastic market exhibits moderate concentration upstream and fragmentation downstream. Large polymer producers dominate resin supply and influence pricing dynamics, while machine manufacturing and contract molding remain more fragmented with a mix of global leaders and regional specialists. Value capture is distributed across the chain, with material suppliers controlling upstream margins and system integrators and contract molders capturing downstream assembly and application-specific value. Leading players emphasize process innovation, automation-driven cost efficiency, and sustainability integration. Strategic differentiation increasingly relies on advanced molding techniques, recycled material sourcing, and end-to-end system solutions that secure long-term customer relationships.

Key Industry Developments

- In October 2025, machinery maker Tederic Machinery launched its INNOVA series of electro-hydraulic injection molding machines at the K 2025 exhibition, designed for high-efficiency packaging production and improved automation performance.

- In June 2025, BASF introduced Ultramid Advanced N3U42G6, a new halogen-free flame-retardant polyphthalamide grade designed for e-mobility high-voltage connectors, enhancing the durability and corrosion resistance of injection-molded electrical components in EV applications.

Companies Covered in Injection Molded Plastic Market

- BASF

- LyondellBasell

- SABIC

- Dow

- Covestro

- ExxonMobil Chemical

- Chevron Phillips Chemical

- DuPont

- Celanese

- Formosa Plastics

- Arburg

- Husky Injection Molding Systems

- ENGEL

- KraussMaffei

- Milacron

- Sumitomo (SHI) Demag

- Nissei Plastic Industrial

- Toshiba Machine/TOSHIBA MOLDED PRODUCTS

Frequently Asked Questions

The global injection molded plastic market is valued at US$327.6 billion in 2026.

By 2033, the injection molded plastic market is expected to reach US$489.3 billion.

Key trends include lightweighting and material substitution, increasing use of recyclable and bio-based polymers, growing adoption of automation and electric injection molding machines, and rising demand for high-precision and multi-shot molding in automotive, medical, and electronics applications.

By application, packaging is the leading segment, accounting for approximately 32.3% market share, driven by high-volume demand for closures, thin-wall containers, and rigid packaging used in food, beverage, and personal care industries.

The injection molded plastic market is projected to grow at a CAGR of 5.9% between 2026 and 2033.

Major players include BASF SE, LyondellBasell Industries, SABIC, Dow Inc., and Covestro AG.