- Smart Packaging

- Plastic Kegs Market

Plastic Kegs Market Size, Share, and Growth Forecast, 2026 - 2033

Plastic Kegs Market by Material (PET, HDPE, Others), Capacity (20-40 Liters, Up to 20 Liters, Others), Application, and Regional Analysis for 2026 - 2033

Plastic Kegs Market Size and Trends Analysis

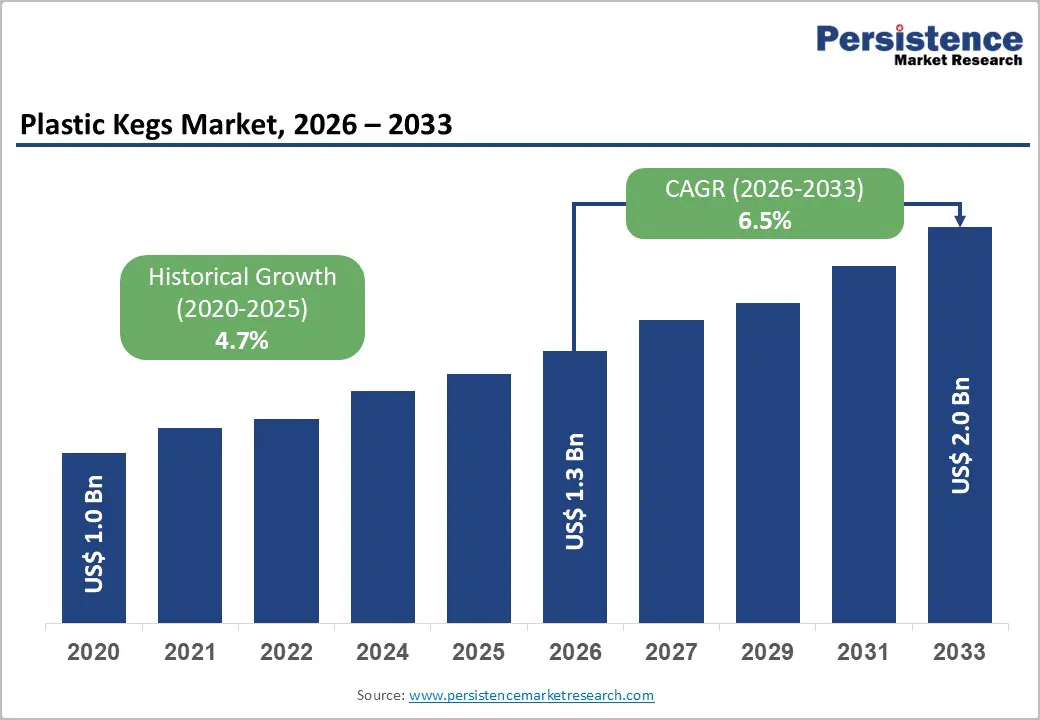

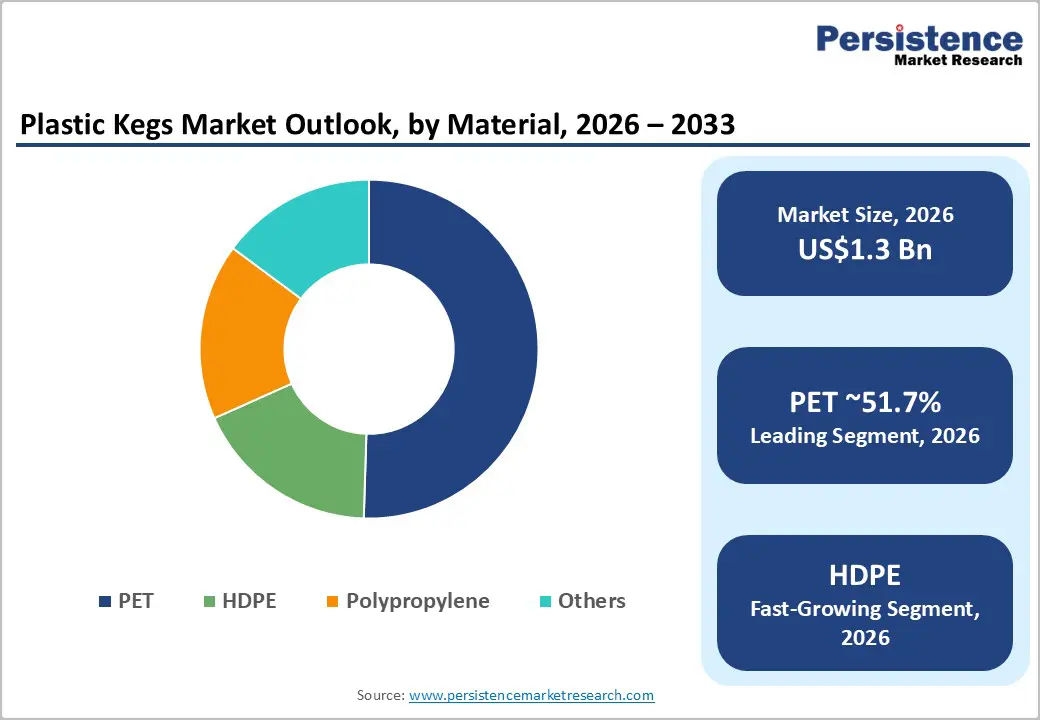

The global plastic kegs market size is likely to be valued at US$1.3 billion in 2026 and is expected to reach US$ 2.0 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033, driven by the rising draft beverage consumption across on-trade and off-trade channels, alongside accelerating adoption of lightweight and one-way plastic kegs that reduce logistics complexity and total cost of ownership.

Craft and small-batch beverage producers remain a structural demand base, particularly for 20-40 liter formats, while sustainability mandates and circular-economy initiatives are reshaping material selection and service models. Innovation in polymer materials, pooled keg systems, and digital asset-tracking solutions is steadily redefining competitive advantage across global value chains.

Key Industry Highlights

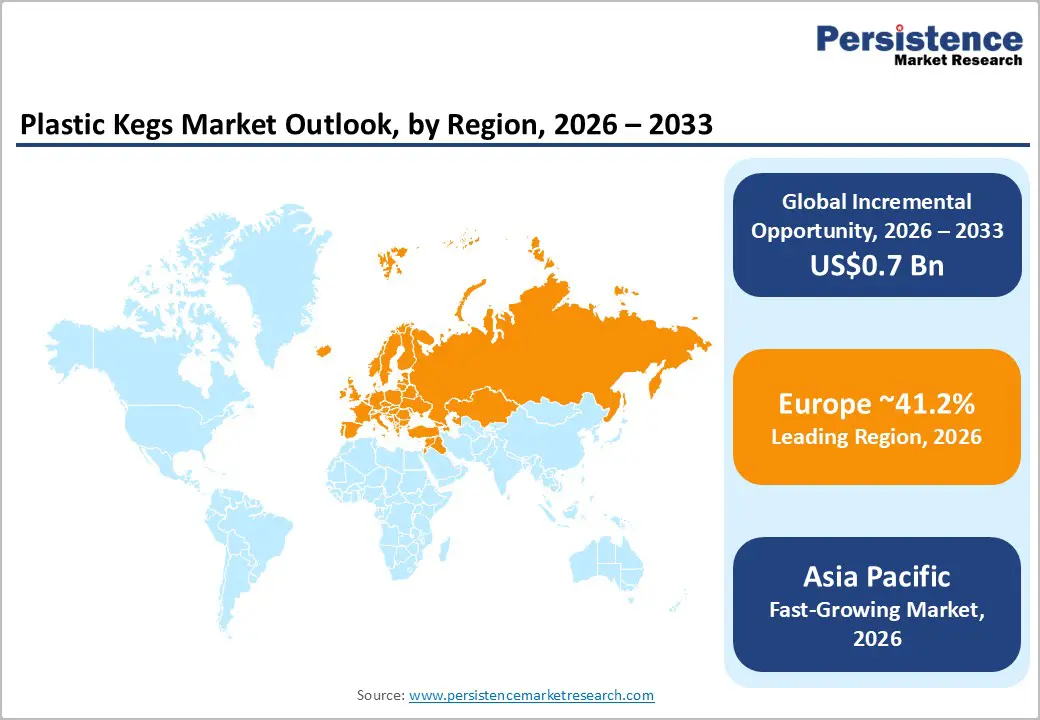

- Leading Region: Europe is projected to lead the market with 41.2% share in 2026, supported by strong circular-economy regulations, dense brewery networks, and widespread adoption of recyclable PET and reusable polymer kegs across on-trade and export channels.

- Fastest-growing Region: The Asia-Pacific region is the fastest-growing, driven by urbanization, rising disposable incomes, and expanding hospitality sectors, with rapid uptake of one-way PET kegs in China, India, Japan, and the ASEAN markets.

- Investment Plans: Investment is concentrated in pooled keg services, recycled-content PET production, and IoT-enabled asset tracking, with service platforms and localized manufacturing expansions targeting cost efficiency and lifecycle optimization across North America, Europe, and Asia Pacific.

- Dominant Material: PET kegs are expected to dominate the material segment, with up to 51.7% share, owing to their lightweight, recyclability, and suitability for one-way and export-oriented applications in craft beer, cider, and specialty beverages.

- Leading Application: Alcoholic beverages are estimated to account for over 64.8% of market share in 2026, anchored by beer and craft brewing, with sustained usage in on-trade, seasonal releases, and export distribution.

| Key Insights | Details |

|---|---|

| Plastic Kegs Market Size (2026E) | US$1.3 Bn |

| Market Value Forecast (2033F) | US$2.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Cost and Logistics Advantages of Lightweight Plastic Kegs

Lightweight plastic kegs, particularly PET-based one-way formats, offer clear economic benefits over traditional stainless-steel kegs by reducing transport weight, eliminating reverse logistics, and lowering handling costs. Freight weight reductions can materially improve export economics, especially for long-distance and intercontinental shipments. For small and mid-sized beverage producers, the ability to ship without recovering empty kegs reduces capital tied up in fleet assets and simplifies market entry for new SKUs. These advantages are especially pronounced in seasonal, event-based, and trial-market deployments. As beverage supply chains prioritize flexibility and speed to market, lightweight plastic kegs directly support market expansion.

Sustainability Mandates and Circular-Economy Alignment

Regulatory emphasis on recyclability, reuse, and eco-design across Europe and North America is accelerating the adoption of plastic kegs that align with circular-economy principles. Recyclable PET and reusable polymer kegs fit within evolving packaging regulations that penalize waste-intensive formats. Deposit-return schemes and extended producer responsibility policies raise the relative cost of single-use alternatives while favoring pooled or recyclable systems. This has created a dual-track market structure: one-way PET for export and temporary use, and multi-use polymer kegs for high-volume domestic circulation. Over time, increased recycled content and improved collection infrastructure are lowering lifecycle costs, reinforcing plastic kegs as a compliant and economically viable solution.

Technology Convergence in Keg Management and Asset Tracking

Digitalization is becoming integral to keg economics. IoT-enabled tracking, digital identification tags, and asset-management platforms improve visibility across keg fleets, reducing loss rates and improving fill-to-return cycles. These technologies allow operators to optimize fleet size, reduce idle assets, and lower empty-mile transport costs. When combined with durable polymer kegs or pooled PET systems, digital tracking improves return on assets and reduces working capital requirements for distributors and brewers. This convergence of physical containers and software platforms is strengthening the value proposition of plastic kegs for large distributors and multinational beverage companies seeking scalable, data-driven logistics models.

Barrier Analysis - Polymer Feedstock Price Volatility

Plastic keg production is sensitive to fluctuations in polymer feedstock prices, including PET, HDPE, and polypropylene. Volatility in crude-oil-linked inputs can compress manufacturer margins and force price pass-throughs to beverage customers. Historically, packaging markets have experienced 15-30% polymer price swings, which can materially impact profitability. When beverage producers operate under margin pressure, higher packaging costs may delay adoption or favor alternative formats. Manufacturers must therefore balance procurement strategies, pricing discipline, and material innovation to mitigate exposure to input-cost volatility.

End-Of-Life and Recycling Infrastructure Gaps

The sustainability performance of plastic kegs depends on reliable collection and recycling pathways. In regions with limited recycling infrastructure or low sorting rates, the environmental advantage of PET and polymer kegs is weakened, increasing reputational and regulatory risk. Where recovery systems are underdeveloped, authorities may restrict single-use formats or impose additional compliance costs. To sustain growth, suppliers increasingly need to invest in take-back programs, partnerships with recyclers, or pooled systems that ensure closed-loop circulation.

Opportunity Analysis - Export-Oriented One-Way PET Kegs

One-way PET kegs enable brewers to access distant markets without the burden of reverse logistics. Export-focused craft and contract brewers can ship draft beverages more efficiently, opening new geographic revenue streams. If export-oriented PET kegs capture 10-15% of incremental volume growth between 2026 and 2033, this represents a substantial revenue opportunity for suppliers. The convergence of global draft demand and rising logistics costs makes export-friendly PET formats a near-term growth lever.

Expansion of Pooled Keg and Pay-Per-Fill Models

Pooling and pay-per-fill services reduce capital barriers for small brewers, hospitality operators, and event organizers. By outsourcing fleet ownership and maintenance, users improve cash flow and operational focus. If pooled services penetrate 5-8% of addressable small-batch and event-based beverage operations by 2030, recurring service revenues could scale significantly. This model aligns with broader trends toward asset-light operations and logistics outsourcing.

Growth in Small-Format and Non-Alcoholic Draught Products

Smaller kegs support SKU proliferation, product trials, and premium draught experiences in both alcoholic and non-alcoholic beverages. Up to 20-liter formats are well-suited for RTD cocktails, cold brew coffee, kombucha, and functional beverages. If small-format kegs account for 40-50% of new draught product launches by 2030, suppliers positioned in this segment can capture outsized unit growth and pricing premiums.

Category-wise Analysis

Material Insights

PET is the dominant material in the market and is projected to account for up to 51.7% of the market share in 2026, supported by its lightweight structure, high recyclability, and compatibility with one-way and hybrid keg designs. PET kegs significantly reduce transportation weight and handling complexity, which is particularly valuable for export-oriented breweries, mobile beverage vendors, and event-based distribution models. Craft beer producers, cider makers, and specialty beverage brands increasingly prefer PET kegs for international shipments where return logistics are impractical. PET’s strong gas-barrier performance, transparency for quality inspection, and compliance with food-contact regulations also make it suitable for both carbonated products, such as beer, and non-carbonated beverages, including cold brew coffee and functional drinks.

HDPE-based and polyethylene/polypropylene polymer blends are likely to be the fastest-growing material segment, driven by rising demand for reusable and pooled keg systems. These materials offer superior durability, impact resistance, and structural stability, enabling multi-trip circulation across extended distribution cycles. More than 70% of durable polymer kegs are manufactured using HDPE-dominant blends, reflecting industry preference for long service life, ease of refurbishment, and resistance to rough handling in high-volume logistics networks. Growth is strongest in pooled-fleet applications used by regional breweries, beverage distributors, and hospitality chains, where lifecycle cost-efficiency, reduced keg loss, and operational reliability outweigh the higher upfront material costs.

Application Insights

Alcoholic beverages are expected to be the largest application segment and are anticipated to account for over 64.8% of market share in 2026, primarily driven by beer and the expanding craft brewing ecosystem. Draft beer continues to dominate usage due to well-established dispensing infrastructure across bars, restaurants, taprooms, and event venues. Seasonal product launches, limited-edition brews, and export-focused offerings further reinforce demand for plastic kegs, particularly PET and reusable polymer formats. Plastic kegs are increasingly used for international shipments of craft beer and cider, where reduced weight, lower breakage risk, and simplified logistics provide clear advantages over traditional stainless-steel kegs.

Non-alcoholic beverages are likely to be the fastest-growing application segment, supported by rising consumption of cold brew coffee, kombucha, RTD mocktails, and functional beverages. Health-conscious consumer behavior and premiumization trends are expanding draught-format adoption beyond alcoholic drinks, particularly in cafés, co-working spaces, fitness centers, and specialty retail outlets. Plastic kegs, especially small-format PET variants, are well suited to these applications due to their ease of handling, preservation of freshness, and flexibility for trial launches. Producers increasingly use plastic kegs to test new formulations and regional demand before committing to large-scale investments in bottling or canning.

Regional Insights

North America Plastic Kegs Market Trends - Craft Brewery-Driven Adoption and Pooled Keg Expansion

North America remains a major revenue contributor to the plastic kegs market, supported by a dense craft brewing ecosystem, strong on-trade consumption culture, and highly developed beverage logistics infrastructure. The U.S. leads regional demand, driven by high per-capita draft beer consumption and a large base of independent craft breweries that prioritize flexibility and cost control. American craft brewers increasingly use PET and reusable polymer kegs for limited-release beers, seasonal SKUs, and interstate distribution, where reduced freight weight and lower loss risk materially improve margins. One-way plastic kegs are also widely used for exports to Latin America and Asia, where return logistics are uneconomical.

Pooled keg systems have gained traction across the U.S. and Canada as breweries seek to reduce capital tied up in stainless-steel fleets. Large beverage service operators and logistics providers have expanded shared keg pool models, enabling smaller brewers to scale distribution without owning container assets. The adoption of RFID- and QR-based asset-tracking technologies has improved fleet visibility, reduced keg shrinkage, and optimized rotation cycles. These developments align with broader digitization trends across North American beverage supply chains.

From a regulatory standpoint, food-contact safety standards are well established, providing a stable framework for the adoption of polymer kegs. Environmental policies at the state and provincial levels increasingly favor recyclable and reusable packaging, indirectly supporting PET and HDPE-based keg formats. Investment activity in the region is concentrated around service platforms, digital tracking solutions, and hybrid packaging strategies that combine reusable polymer kegs for domestic circulation with PET kegs for export and event-based use.

Europe Plastic Kegs Market Trends - Regulation-Led Circular Economy and Reusable Keg Leadership

Europe is expected to lead the market, with an estimated 41.2% share in 2026, reflecting the region’s advanced circular-economy regulations, dense brewery networks, and highly efficient beverage distribution systems. Germany, the U.K., France, and Spain form the core of regional demand, each combining strong traditional brewing cultures with rapidly expanding craft and specialty beer segments. European brewers have been early adopters of reusable polymer kegs, particularly in domestic and intra-EU distribution, where return logistics are efficient and cost-effective. EU-level packaging and waste directives strongly favor recyclable materials, reusable systems, and reduced lifecycle emissions.

These policies have accelerated the shift toward PET one-way kegs for export and HDPE-based reusable kegs for local circulation. Pooled keg services are well established across Western Europe, allowing breweries to outsource fleet management while complying with sustainability and reporting requirements. Many hospitality chains and beverage distributors actively prefer pooled plastic kegs due to consistent quality, standardized handling, and lower operational risk.

Investment trends in Europe include expansion of domestic plastic keg manufacturing capacity, increased use of recycled PET content, and development of closed-loop recovery systems. Several European beverage packaging suppliers have strengthened partnerships with recyclers and logistics providers to ensure end-of-life compliance and traceability. These developments reinforce Europe’s leadership position and make the region a reference market for regulatory-driven adoption of plastic kegs globally.

Asia Pacific Plastic Kegs Market Trends - One-Way PET Kegs and Urban Draft Growth Across

Asia Pacific is expected to be the fastest-growing regional market for plastic kegs, driven by rapid urbanization, rising disposable incomes, and expanding hospitality and food-service sectors. China, Japan, India, and key ASEAN markets are experiencing increased demand for draft beverages in urban centers, including beer, cider, cold brew coffee, and emerging non-alcoholic formats. In many of these markets, one-way PET kegs are favored because return logistics are fragmented, cross-border distribution is common, and infrastructure for keg recovery remains uneven.

Japan and Australia have demonstrated early adoption of plastic kegs for both alcoholic and non-alcoholic beverages, supported by quality-focused beverage cultures and strong convenience retail networks. In China and Southeast Asia, international and regional brewers increasingly use PET kegs for event-based sales, tap takeovers, and export-oriented distribution to reduce freight costs and handling complexity. India’s growing craft beer scene, concentrated in major metropolitan areas, is also contributing to demand for small-format plastic kegs suited for taprooms and pilot batches.

Asia-Pacific’s manufacturing cost advantages strengthen its position as both a consumption and a production hub for plastic kegs. Several global and regional suppliers source or assemble polymer kegs in the region to support export markets. Growth opportunities increasingly center on localized production partnerships, urban pooled services for hospitality clusters, and small-format kegs aligned with premium and experimental beverage launches. As regulatory frameworks evolve and recycling infrastructure improves, the adoption of plastic kegs in the Asia Pacific is expected to accelerate further.

Competitive Landscape

The global plastic kegs market exhibits moderate concentration, with specialized polymer manufacturers competing alongside service-oriented pooling operators. Competition is defined by material innovation, sustainability credentials, and service integration. Partnerships between container producers and fleet managers are increasingly common, reflecting demand for end-to-end solutions rather than standalone products.

Leading players focus on lightweight design, durable polymer blends, pooled services, and digital asset management. Differentiation centers on lifecycle economics, sustainability performance, and logistics efficiency.

Key Industry Developments

- In March 2025, OneCircle introduced a pre-flushed version of its sustainable KeyKeg format that arrives pre-vented and nitrogen-flushed to streamline the filling process for beverage producers, improving operational efficiency for craft brewers and reducing pre-fill preparation time.

Companies Covered in Plastic Kegs Market

- Petainer

- MicroStar

- Kegstar

- THIELMANN

- OneCircle

- PolyKeg

- i-Keg

- KegPlast

- Konvoy

- BevPak

- Blefa

- NDL Keg

- Kegco

- KegLand

- Pet Technologies

- Schäfer Container Systems

- Ardagh Group

- Mauser Packaging Solutions

Frequently Asked Questions

The global plastic kegsmarket size is likely to be valued at US$1.3 billion in 2026.

By 2033, the plastic kegs market is expected to reach US$2.0 billion.

Key trends include the shift toward lightweight and one-way PET kegs, expansion of pooled and pay-per-fill service models, increasing use of IoT-enabled keg tracking, and growing demand for small-format kegs driven by craft beverages, RTD drinks, and event-based consumption.

By material, PET is the leading segment, accounting for up to 51.7% share, driven by recyclability, ease of handling, and strong suitability for export and single-use applications. By application, alcoholic beverages dominate with over 64.8% share, anchored by beer and craft brewing.

The plastic kegs market is projected to grow at a CAGR of 6.5% between 2026 and 2033.

Major players with strong product portfolios and market presence include Petainer, MicroStar / Kegstar, i-Keg, KegPlast, and Konvoy.