- Non-food Packaging

- Plastic Caulk Tube Market

Plastic Caulk Tube Market Size, Share, and Growth Forecast, 2026 - 2033

Plastic Caulk Tube Market by Material Type (PE, PP, Others), Application (Construction & Carpentry, DIY/Home Improvement, Others), Capacity, and Regional Analysis for 2026 - 2033

Plastic Caulk Tube Market Size and Trends Analysis

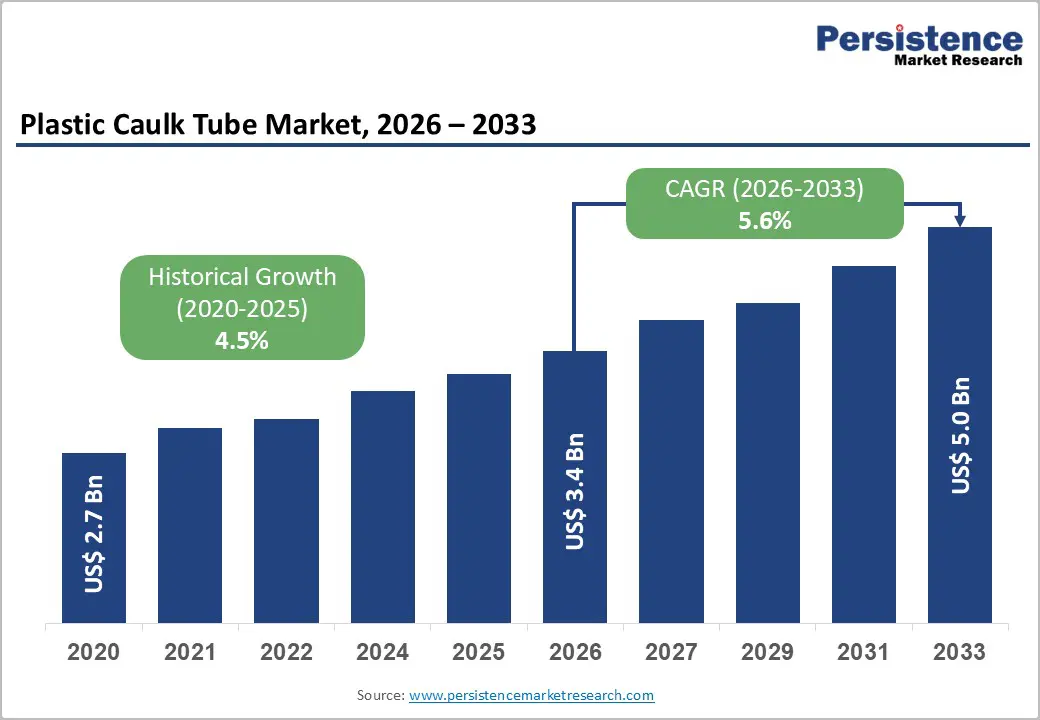

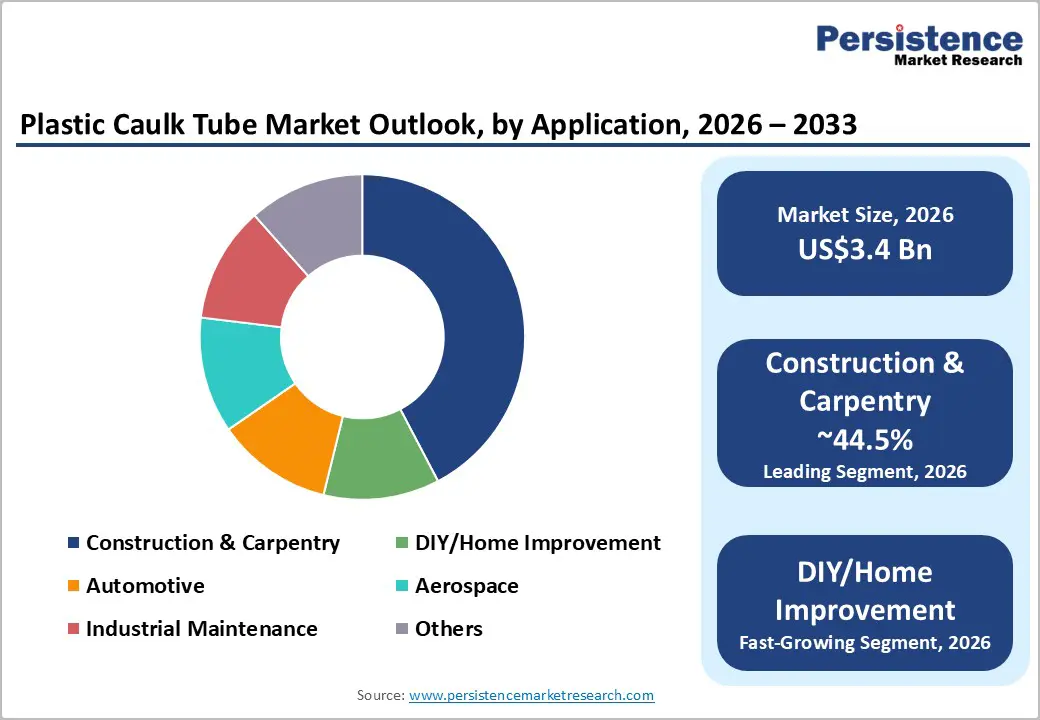

The global plastic caulk tube market size is likely to be valued at US$3.4 billion in 2026 and is expected to reach US$5.0 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033, driven by sustained construction activity, renovation cycles, and increased DIY participation.

Demand remains concentrated in construction and carpentry applications, while polyethylene (PE) continues to dominate the material landscape. Growth is further reinforced by stricter building codes emphasizing energy efficiency, as well as manufacturers’ investments in recyclable materials and ergonomically enhanced tube designs.

Key Industry Highlights:

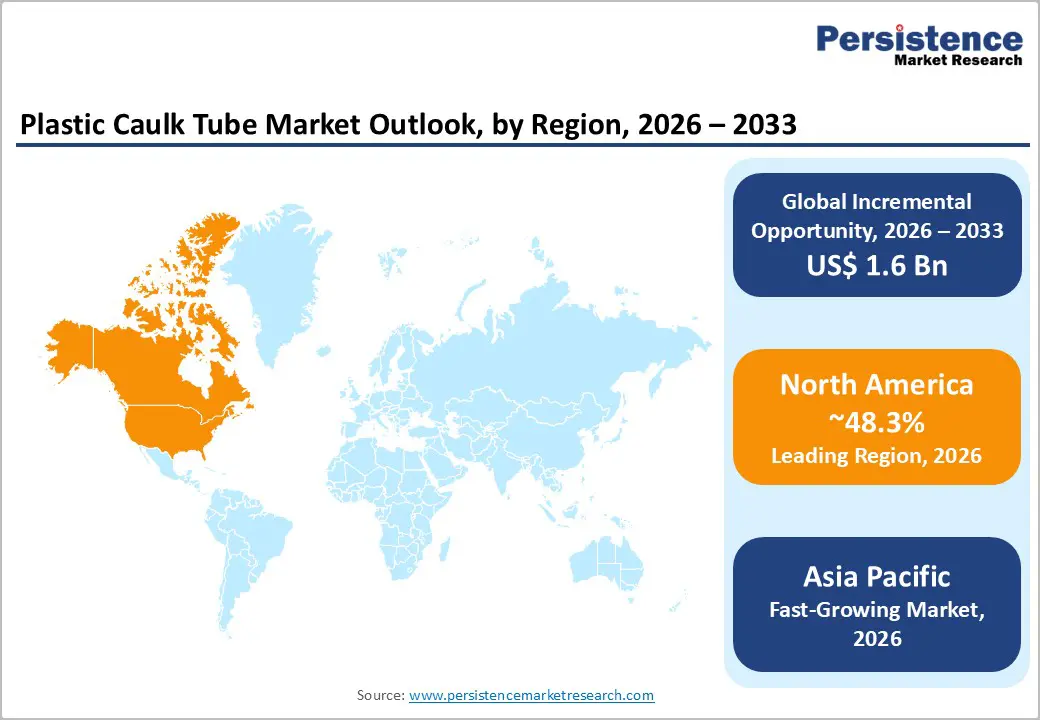

- Leading Region: North America is projected to dominate the market, accounting for nearly 48.3% of market share, supported by strong residential remodeling activity, stringent energy-efficiency codes, and advanced retail distribution networks across the U.S. and Canada.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization, infrastructure expansion, and manufacturing localization in China, India, and the ASEAN countries.

- Investment Plans: Manufacturers are investing in automation, lightweight tube designs, and integration of post-consumer recycled (PCR) materials, with sustainability-focused tube platforms targeting 15-25% recyclable adoption in mature markets by 2030.

- Dominant Material Type: Polyethylene (PE) is expected to remain the leading material segment, accounting for 37.8% of total material usage due to cost-effectiveness, flexibility, and compatibility with silicone and acrylic sealants.

- Leading Application: Construction and carpentry is estimated to account for the largest application share at approximately 44.5% of market share, supported by renovation cycles, infrastructure upgrades, and regulatory-driven building envelope sealing requirements.

| Key Insights | Details |

|---|---|

| Plastic Caulk Tube Market Size (2026E) | US$3.4 Bn |

| Market Value Forecast (2033F) | US$5.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Construction and Renovation Activity

Global construction pipelines, including both new builds and retrofit projects, directly drive demand for sealants and caulking products. Residential remodeling, commercial façade upgrades, infrastructure expansion, and energy-efficiency retrofits all require sealing materials, thereby increasing tube consumption in proportion. Energy-performance regulations in developed economies emphasize airtight building envelopes to reduce thermal leakage, directly increasing sealant usage in windows, doors, façades, and insulation joints. Construction and carpentry applications account for approximately 44.5% of total demand for plastic caulk tubes, reflecting the sector’s structural importance. Renovation cycles in mature economies and infrastructure investments in emerging markets collectively sustain long-term growth momentum. As governments prioritize energy-efficient building upgrades, sealant-intensive applications are expanding, reinforcing steady demand for professional-grade cartridges.

Product and Material Innovation (PE and PP Advancements)

Material innovation plays a central role in shaping the plastic caulk tube market. Polyethylene (PE) accounts for approximately 37.8% of the material mix, owing to its cost-effectiveness, flexibility, and compatibility with silicone and acrylic sealants. Advancements in polymer engineering have enabled thinner-walled designs with higher burst strength, thereby reducing raw material consumption while maintaining durability. Polypropylene (PP) is gaining traction due to enhanced stiffness, improved heat resistance, and greater recyclability. Manufacturers are increasingly developing mono-material tube systems that facilitate recycling and reduce environmental impact. Lightweighting initiatives also lower transportation costs and improve operational efficiency across supply chains. These technological improvements reduce the total cost of ownership for sealant manufacturers while supporting sustainability objectives, driving broader adoption across industrial and retail channels.

DIY and Retail Channel Expansion

The expansion of DIY culture and organized retail channels significantly contributes to market growth. Rising home improvement activity, influenced by renovation trends and increased consumer awareness, has boosted sales of packaged sealant products. Retail distribution through large home improvement chains and e-commerce platforms increases accessibility and product visibility. Smaller-format packaging, ergonomic nozzle designs, and convenience-oriented packaging solutions align with retail consumer preferences. Sales data across adhesives and sealants segments show year-over-year growth in DIY consumption, particularly for smaller-capacity tubes under 200 ml. The democratization of home-improvement solutions and digital retail access continues to broaden the addressable consumer base, thereby accelerating demand growth in this segment.

Barrier Analysis - Raw Material Price Volatility and Supply Risks

Plastic caulk tube production depends heavily on commodity resins such as PE, PP, and PVC. These materials are subject to feedstock price fluctuations driven by crude oil dynamics, geopolitical disruptions, seasonal demand shifts, and supply chain bottlenecks. Resin price volatility between 2023 and 2025 created margin pressure for converters, particularly small- and mid-sized manufacturers operating under tight cost structures. Price-sensitive applications, including industrial maintenance and low-cost sealants, are particularly vulnerable. Manufacturers may absorb cost increases or pass them downstream, potentially reducing competitiveness and slowing investment in innovation initiatives, such as the development of recyclable tubes.

Regulatory and Recycling Compliance Complexity

Evolving packaging regulations, including recycled-content mandates and plastic waste reduction policies, introduce compliance challenges. Certain jurisdictions impose restrictions on specific plastic types or require certification for recyclability. Existing tube designs may require re-engineering to meet updated standards. Compliance costs include polymer reformulation, testing, and third-party certification processes. For smaller converters, these expenditures can represent mid-single-digit percentages of annual revenue during early implementation phases. Regulatory fragmentation across regions also complicates cross-border trade and export operations, adding operational complexity.

Opportunity Analysis - Recyclable and PCR-Integrated Tube Platforms

Sustainability-driven procurement policies create significant growth opportunities. Recyclable mono-material PE and PP tube systems, along with the integration of post-consumer recycled (PCR) resin, can command premium pricing in regulated markets. If recyclable variants achieve 15-25% adoption in mature markets by 2030, the incremental addressable opportunity could represent several hundred million dollars within the overall market trajectory. Manufacturers investing in certified PCR supply chains, traceability systems, and validated recyclability claims are well-positioned to secure long-term contracts with multinational sealant brands and large retail chains. Sustainability compliance is transitioning from a marketing differentiator to a procurement requirement.

Small-Format and Precision Dispensing Solutions

The fastest-growing capacity segment is up to 200 ml, reflecting consumer demand for convenience and reduced waste. Smaller cartridges are particularly suited for precision applications such as bathroom repairs, trim work, and small renovation projects. Converters can enhance margins by developing refillable cartridge systems, concentrated formulations, and bundled tool-and-tube offerings. Integration of advanced nozzle technology improves application accuracy and reduces product waste. Targeted expansion through e-commerce platforms and retail partnerships strengthens brand penetration while capturing incremental value in the DIY channel.

Category-wise Analysis

Material Type Insights

Polyethylene (PE) is expected to account for approximately 37.8% of the market during the forecast period, maintaining its leadership in plastic caulk tube manufacturing. Its flexibility, chemical resistance, cost-effectiveness, and ease of extrusion make it well-suited for high-volume cartridge production. PE supports thin-wall designs without compromising burst strength, enabling material optimization and reduced per-unit production costs. The polymer demonstrates excellent compatibility with silicone, acrylic, latex, and hybrid sealant formulations, ensuring stable shelf life and dispensing performance. For example, many standard 300 ml construction-grade cartridges used for window glazing and bathroom sealing are made of high-density polyethylene (HDPE) for durability and leak resistance. Large converters benefit from standardized PE resin grades sourced in bulk, which improve supply chain consistency and reduce procurement volatility. The growing development of recyclable mono-material PE tube systems further reinforces its sustained dominance across North America and Europe.

Polypropylene (PP) is projected to be the fastest-growing material segment, driven by rising demand for higher rigidity, improved thermal resistance, and enhanced recyclability. PP cartridges offer greater structural stiffness than PE, making them suitable for heavy-duty sealants in industrial construction, automotive assembly, and infrastructure applications. For instance, high-performance polyurethane and epoxy-based sealants used in automotive windshield bonding or industrial flooring applications increasingly utilize PP cartridges to withstand pressure and transport stress. PP also enables impact-resistant designs that reduce deformation during logistics and storage. Manufacturers are investing in mono-material PP systems to align with circular economy objectives, particularly in Europe, where packaging recyclability standards are tightening. These attributes position PP as a strategic growth material for converters targeting premium and sustainability-focused segments.

Application Insights

Construction and carpentry applications are anticipated to account for approximately 44.5% of the market share in 2026, making them the largest end-use segment. Professional contractors rely heavily on standardized 280-310 ml cartridges for glazing, insulation sealing, façade expansion joints, drywall finishing, and flooring installations. Demand remains stable, driven by ongoing residential renovation cycles, commercial retrofits, and infrastructure development projects. For example, energy-efficiency upgrades involving window resealing and air-gap insulation directly increase consumption of silicone and acrylic sealants packaged in plastic cartridges. Government-driven infrastructure investments and building code requirements emphasizing airtight construction further reinforce sealant usage, as sealant consumption correlates closely with square footage constructed or renovated. Tube demand follows predictable volume patterns, providing stable order pipelines for manufacturers.

DIY and home improvement applications represent the fastest-growing segment, driven by increasing homeowner participation in minor repair and renovation activities. Growth in this segment is supported by urban housing upgrades, rental property maintenance, and rising consumer awareness of preventive sealing solutions. Retail-oriented packaging innovations such as compact 150-200 ml cartridges, easy-cut nozzles, resealable caps, and ergonomic dispensing designs enhance usability for non-professional consumers. For example, bathroom re-caulking kits and kitchen sealing solutions sold through large home improvement chains and online platforms frequently use small-format PE or PP cartridges designed for one-time projects. Private-label collaborations between packaging converters and retailers further expand distribution, while e-commerce growth supports compact, lightweight packaging formats that reduce shipping costs. This shift toward convenience-based consumption is expected to accelerate demand for smaller-capacity cartridges over the forecast period.

Regional Insights

North America Plastic Caulk Tube Market Trends - Renovation-Driven Demand, Retail Scale, and Energy-Code Alignment

North America is poised to dominate the sealant market, capturing nearly 48.3% of the share, with the U.S. being the largest contributor. This growth is driven by robust residential remodeling activity, as highlighted by the U.S. Census Bureau and the Joint Center for Housing Studies, which report high home improvement expenditures post-2020. Sealant demand correlates with remodeling trends, particularly in window replacement, roofing repairs, and bathroom renovations, where 280-310 ml cartridges are commonly used.

Canada's demand is bolstered by cold-climate sealing needs, particularly in provinces such as Ontario and Alberta, where thermal insulation retrofits are prevalent. Mexico contributes to the market through industrial construction growth, particularly in automotive and manufacturing sectors, driven by nearshoring.

U.S. building codes, aligned with the International Energy Conservation Code (IECC), emphasize air sealing and energy efficiency, further boosting demand for silicone and acrylic sealants in compliant plastic cartridges. Major brands such as DAP, Sika, Henkel, and 3M maintain a strong retail presence, with sustainability initiatives pushing manufacturers to increase post-consumer recycled (PCR) content in packaging.

RPM International’s investments in automation are improving efficiency and margin resilience by streamlining packaging and reducing material usage. Innovations such as ergonomic dispensing systems and anti-drip nozzles enhance competitive advantage in both professional and DIY markets. Regulatory support, strong retail infrastructure, and continued investment in automation ensure North America's continued leadership in the sealant market.

Europe Plastic Caulk Tube Market Trends - Regulation-Led Sustainability and High-Performance Industrial Sealing

Europe's sealant market is shaped by stringent sustainability mandates and regulatory frameworks, with Germany leading in industrial sealing due to its strong automotive, machinery, and construction sectors. The country’s focus on engineering standards and certification drives demand for high-performance PP and PE cartridges compatible with polyurethane and hybrid sealants. The U.K., France, and Spain benefit from national retrofit programs and aging housing stock, which fuel demand for sealants in renovation projects, including window glazing, façade joint sealing, and roofing insulation.

EU directives, such as the Energy Performance of Buildings Directive (EPBD), promote energy-efficient retrofits that require significant sealing and insulation work. Harmonized regulations across the EU ensure compliance with packaging recyclability, chemical safety under REACH, and VOC disclosure, driving demand for mono-material, recyclable systems.

Belgium's Soudal Group and Bostik (Arkema Group) lead in sustainable product innovations, focusing on recyclable cartridge designs and environmental product declarations (EPDs) for public infrastructure tenders. Investments prioritize certifications for recyclable tubes, lifecycle transparency, and localized production to minimize transportation-related emissions. Germany’s advanced recycling systems foster mono-material PP adoption. Suppliers that meet EU packaging and carbon reporting standards gain competitive advantages, particularly in government-funded projects. Europe's regulatory maturity is reshaping product development, supply chains, and capital strategies within the sealant market.

Asia Pacific Plastic Caulk Tube Market Trends - Urbanization, Infrastructure Expansion, and Export-Oriented Manufacturing

Asia-Pacific is the fastest-growing region in the sealant market, driven by rapid urbanization, expanding industrial bases, and rising domestic consumption of construction materials. China dominates both production and consumption, supported by extensive infrastructure programs and a robust manufacturing ecosystem, which includes numerous extrusion and injection-molding facilities supplying both domestic brands and export markets. Japan, meanwhile, focuses on high-performance specialty sealants for precision construction and automotive applications, which require advanced cartridge designs.

India and ASEAN countries such asVietnam, Indonesia, and Thailand are experiencing significant growth due to ongoing infrastructure development and rising demand for middle-class housing. Urban expansion and industrial localization are key growth drivers in these regions. According to World Bank data, urban population growth in India and Southeast Asia is supporting increased residential construction, thereby driving sealant demand in high-density housing projects. Additionally, the expanding DIY culture, particularly in urban China and India, has led to higher demand for compact cartridges available through e-commerce platforms such as JD.com and Flipkart.

Major players in India, such as Asian Paints and Pidilite Industries, are expanding their sealant and adhesive portfolios, further boosting demand for standardized cartridge packaging. In China, packaging manufacturers have invested in automated extrusion lines to enhance cost efficiency and export competitiveness, positioning the region as a global supply hub. Regulatory enforcement varies across countries: Japan has stringent material standards, while emerging ASEAN markets have evolving compliance frameworks, creating both opportunities and operational risks for multinational suppliers. Investment is increasingly focused on high-volume production facilities, competitive resin sourcing, and localized supply chains to strengthen the Asia Pacific’s role in the global market.

Competitive Landscape

The global plastic caulk tube market is moderately concentrated at the global level but fragmented regionally. Large packaging corporations control approximately 25-35% of the market collectively, while numerous mid-sized and regional converters serve localized demand.

Competitive positioning emphasizes scale, cost efficiency, sustainability compliance, and technical collaboration with sealant formulators. Large buyers negotiate long-term supply agreements, while smaller distributors rely on regional partnerships.

Leading companies prioritize recyclable mono-material designs, PCR integration, production automation, and retail channel expansion. Strategic partnerships with sealant manufacturers strengthen long-term supply agreements, while product differentiation focuses on ergonomic dispensing systems and sustainability certification.

Key Industry Developments

- In July 2025, UFlex’s FlexiTubes announced plans to showcase its USFDA-approved sustainable PCR-based tube solutions, including the Greenika line, at CMPL Expo 2025 in Mumbai, reinforcing its focus on circular economy packaging and extended producer responsibility goals.

Companies Covered in Plastic Caulk Tube Market

- Berry Global Inc.

- Sonoco Products Company

- Silgan Holdings Inc.

- Huhtamaki Oyj

- Montebello Packaging Inc.

- Alltub Group

- Albea Group

- Amcor plc

- Constantia Flexibles

- Essel Propack Ltd.

- CTL Packaging

- Intrapac International Corporation

- Linhardt Group

- Pirlo Group

- Antilla Propack

- Tectubes Group

- C-Pack Packaging Technologies

- Shanghai Xianrong Packaging Co., Ltd.

Frequently Asked Questions

The global plastic caulk tube market is likely to be valued at US$3.4 billion in 2026.

The plastic caulk tube market is expected to reach US$5.0 billion by 2033.

Key trends include rising adoption of recyclable and PCR-based tube materials to align with sustainability mandates and increased demand for lightweight and mono-material tube designs for easier recycling.

By material type, polyethylene (PE) leads with an anticipated share of 37.8%, driven by cost-efficiency and compatibility with silicone and acrylic sealants. By application, construction and carpentry dominate with approximately 44.5% of market share, supported by renovation cycles and energy-efficiency retrofits.

The plastic caulk tube market is projected to grow at a CAGR of 5.6% between 2026 and 2033.

Major players include Berry Global Inc., Sonoco Products Company, Silgan Holdings Inc., Huhtamaki Oyj, and Montebello Packaging Inc.