- Food Ingredients & Additives

- Peanut Oil Market

Peanut Oil Market Size, Share, and Growth Forecast 2026 - 2033

Peanut Oil Market by Product Type (Refined Peanut Oil, Unrefined Peanut Oil, Cold-Pressed Peanut Oil, Roasted Peanut Oil), Nature (Organic, Conventional), End-user, Distribution Channel, and Regional Analysis, from 2026 - 2033

Peanut Oil Market Size and Trend Analysis

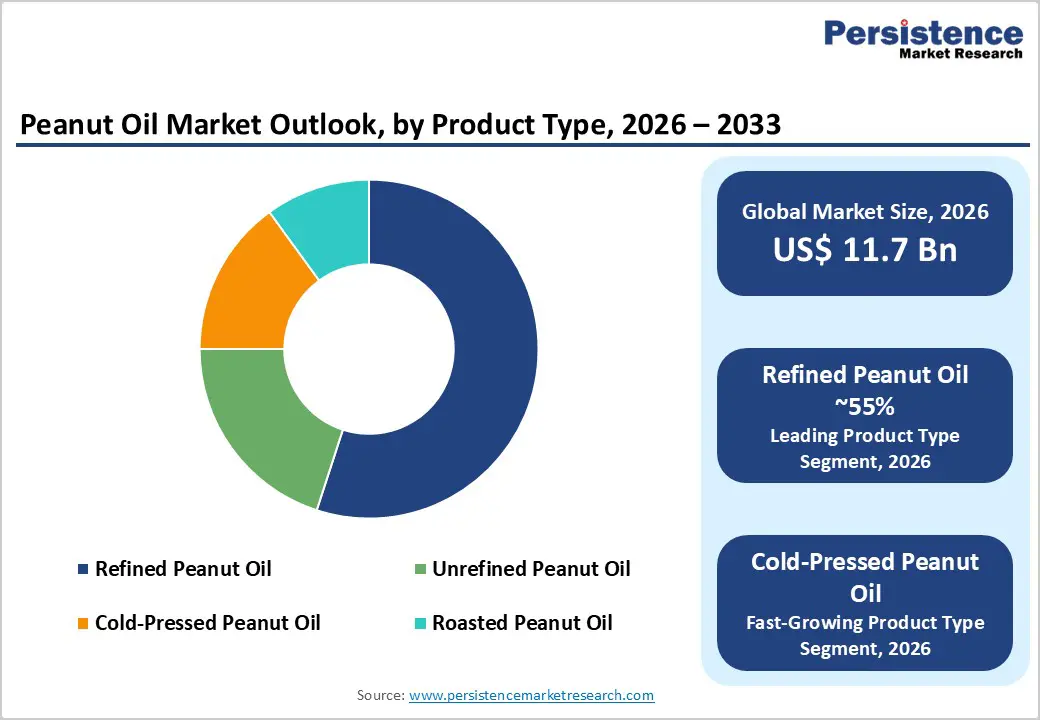

The global peanut oil market size is expected to be valued at US$ 11.7 billion in 2026 and projected to reach US$ 15.7 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

The market is expected to grow steadily with increasing awareness of the benefits of peanut oil applications. Peanut oil is considered one of the healthiest cooking oils as it is free from trans-fat and has low saturated fats. Due to the lower proportion of saturated fat, it is gaining traction among health-conscious consumers. Since consumer health consciousness is growing, the consumption pattern of edible oil is also witnessing a tectonic change. This has led the manufacturers to introduce healthy and fortified edible oils. Furthermore, with the rising emergence of modern trade channels across the developing regions, the outreach of edible oil is increasing in these regions.

Key Industry Highlights:

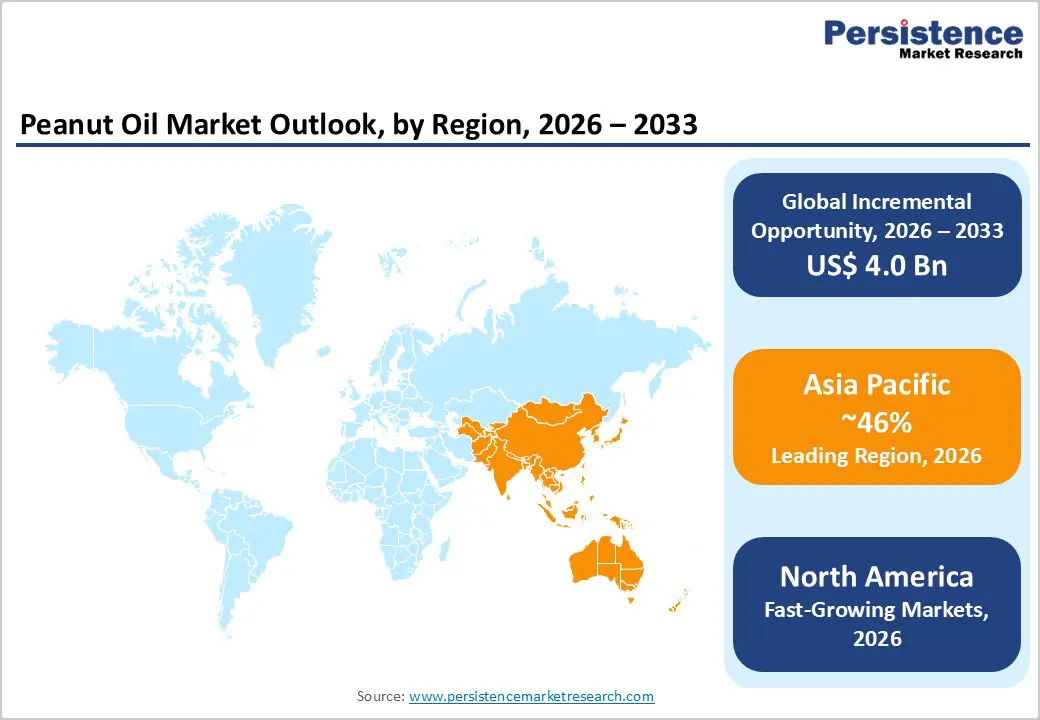

- Asia Pacific will remain the leading peanut oil market with about 46% share, driven by strong production in China and India and widespread culinary usage.

- North America is projected as the fastest-growing region, supported by allergen labeling clarity, health awareness, and increasing online grocery adoption among U.S. consumers.

- Refined peanut oil dominates with around 55% share due to high smoke point, neutral taste, and suitability for large-scale food processing and frying applications.

- Cold-pressed peanut oil is the fastest-growing segment, driven by clean-label trends, premium positioning, and rising consumer demand for minimally processed, nutrient-rich cooking oils.

- E-commerce expansion presents key opportunity, enabling brands to reach wider consumers, promote premium variants, and capitalize on growing online grocery and food product sales globally.

| Key Insights | Details |

|---|---|

|

Peanut Oil Market Size (2026E) |

US$ 11.7 billion |

|

Market Value Forecast (2033F) |

US$ 15.7 billion |

|

Projected Growth CAGR (2026–2033) |

4.3% |

|

Historical Market Growth (2020–2025) |

3.2% |

DRO Analysis

Drivers - Increased Demand for Cold-Pressed & Organic Variant Peanut Oil

Health-conscious consumers are increasingly shifting toward minimally processed edible oils, significantly driving demand for cold-pressed and organic peanut oil variants. Unlike refined peanut oil, cold-pressed oil is extracted without heat or chemical solvents, allowing it to retain essential nutrients such as vitamin E, antioxidants, and healthy fatty acids. This nutritional superiority makes it particularly attractive for consumers seeking heart-healthy cooking options and clean-label products. The growing awareness around lifestyle diseases, including cardiovascular conditions, has further encouraged consumers to replace conventional refined oils with healthier alternatives, boosting adoption across both developed and emerging markets.

In addition, the demand for organic peanut oil is gaining traction due to rising environmental and sustainability concerns. Consumers are increasingly avoiding products containing genetically modified organisms (GMOs) and chemical residues, favoring organic certifications and eco-friendly production practices. This trend is particularly prominent in North America and Europe, where regulatory frameworks and consumer awareness strongly support organic product consumption. The expansion of organic retail channels, along with the increasing availability of premium oil variants in supermarkets and online platforms, is further accelerating market growth. As a result, cold-pressed and organic peanut oils are emerging as high-value segments within the broader peanut oil market.

Restraints - Changing Agricultural Conditions Lead to Inconsistent Raw Material Costs

Changing agricultural conditions are a major challenge for the peanut oil market, directly impacting the availability and cost of raw materials. Climate change has led to increased frequency of extreme weather events such as droughts, irregular rainfall, and temperature fluctuations, which disrupt peanut cultivation cycles. For instance, in 2024, parts of Europe experienced abnormal rainfall patterns that significantly reduced crop yields by approximately 30–40%, demonstrating the vulnerability of agricultural production systems. Such fluctuations create supply shortages, leading to increased price volatility and uncertainty for manufacturers and suppliers in the peanut oil value chain.

Furthermore, peanut crops are highly susceptible to pests, diseases, and soil degradation, which can result in substantial yield losses. Farmers often rely on fertilizers, pesticides, and advanced farming techniques to mitigate these risks; however, the rising cost of agricultural inputs further increases overall production expenses. Additionally, government interventions such as export restrictions, subsidies, and land-use regulations can influence supply dynamics and pricing. These combined factors create instability in raw material procurement, making it difficult for manufacturers to maintain consistent pricing and profitability. As a result, fluctuating agricultural conditions remain a key restraint limiting the steady growth of the peanut oil market.

Opportunities - Introducing Fortified Peanut Oils with Added Nutrients

The growing demand for functional and health-enhancing foods presents a significant opportunity for the peanut oil market through the introduction of fortified peanut oils. Consumers today are not only seeking basic nutrition but also additional health benefits from their food products. By enriching peanut oil with nutrients such as omega-3 fatty acids, vitamin E, and plant sterols, manufacturers can position their offerings as premium, health-focused alternatives. These fortified oils appeal to a wide consumer base, including fitness enthusiasts, aging populations, and individuals managing lifestyle-related health conditions, thereby expanding market reach and value.

Moreover, supportive government initiatives and regulatory frameworks are encouraging innovation in the edible oil sector. For example, in October 2024, the Government of India launched the National Mission on Edible Oils – Oilseeds (NMEO-Oilseeds) with a financial outlay of INR10,103 crore, aimed at boosting domestic oilseed production and promoting self-reliance. Such initiatives create a favorable environment for the development of value-added products like fortified peanut oils. Increased investments in research and development, coupled with rising consumer awareness of functional nutrition, are expected to drive long-term growth opportunities for manufacturers focusing on product innovation in the peanut oil market.

Category-wise Analysis

Product Type Insights

Refined peanut oil is expected to remain the leading product segment, accounting for about 55% of the global peanut oil market in 2025, supported by its neutral flavor, high smoke point, and broad regulatory acceptance in packaged foods and foodservice. This dominance reflects the reality that most industrial and commercial frying applications require stable, standardized oils that withstand repeated high-temperature use while maintaining consistent taste and shelf life.

Clinical and regulatory assessments indicate that highly refined peanut oil contains negligible allergenic protein and is exempt from major allergen labeling in markets such as the U.S., making it more attractive to large food manufacturers and foodservice chains relative to unrefined variants. Together with robust availability of groundnuts in Asia and Africa, refined peanut oil’s favorable functionality ensures it stays the workhorse of the category even as cold-pressed and roasted oils grow faster from a smaller base.

Nature Insights

Conventional peanut oil is estimated to command roughly 85% of global volume in 2026, reflecting the still-nascent penetration of certified-organic oils in mass-market cooking and frying applications. This skew mirrors the broader edible oil landscape, where organic oils remain a small but growing niche relative to total vegetable oil consumption, particularly in price-sensitive emerging markets.

Conventional peanut oil benefits from well-established supply chains, including high-volume crushing operations in major producing countries such as China, India, and Nigeria, which together account for a significant share of global groundnut output and provide competitively priced raw material. While organic peanut oil is gaining traction among health-conscious and environmentally aware consumers, its higher price points and limited certified acreage mean that, in the forecast period, conventional formats will continue to dominate overall volumes while organic drives incremental premium value at the margin.

Distribution Channel Analysis

B2B channels are estimated to account for about 65% of global peanut oil sales in 2026, reflecting the predominance of industrial and institutional usage versus small-pack retail. Large-volume offtake from snack processors, quick-service restaurants, and commercial kitchens is typically supplied through bulk tankers, drums, or intermediate containers under long-term contracts, favoring B2B relationships with crushers and refiners. However, within B2C channels, supermarkets/hypermarkets and online retail are gaining share as urban consumers trade up to branded peanut oil for at-home cooking, supported by rising incomes and evolving retail infrastructure in regions such as Asia Pacific.

The rapid growth of online grocery documented by USDA ERS in the U.S. and by e-commerce statistics in China enhances visibility for branded and specialty peanut oils, helping to rebalance the channel mix in favor of retail over the forecast horizon.

Regional Insights

North America Peanut Oil Market Trends and Insights

In North America, peanut oil demand is shaped by health-driven consumption patterns, clear regulatory frameworks, and the rapid growth of online grocery channels. The U.S. market benefits from well-defined guidelines by the U.S. Food and Drug Administration (FDA), which exempts highly refined peanut oil from major allergen classification while still requiring ingredient transparency. This regulatory clarity supports its widespread use in packaged foods and foodservice applications where allergen management is critical.

Additionally, growing scientific evidence highlighting peanut oil’s role in improving lipid profiles and reducing triglycerides without negatively impacting HDL cholesterol has strengthened its positioning as a heart-friendly cooking oil, encouraging adoption among health-conscious consumers.

Simultaneously, the region is witnessing a structural shift toward digital retail. According to USDA Economic Research Service (ERS), approximately 19–20% of U.S. consumers purchased groceries online monthly during 2022–2023, while online grocery sales surged by nearly 55% between 2019 and 2020. This trend has significantly benefited premium and specialty peanut oils, which gain better visibility and consumer engagement online. Combined with advanced refining technologies, strong retail branding, and established edible oil processors, these factors position North America as a rapidly growing market despite its relatively smaller share compared to the Asia Pacific.

Asia Pacific Peanut Oil Market Trends and Insights

Asia Pacific dominates the global peanut oil market, accounting for approximately 46% of total market share in 2025, driven by strong production and consumption across countries such as China, India, and ASEAN nations. According to the Food and Agriculture Organization (FAO), Asia contributes nearly 70% of global groundnut production, with China producing around 15 million tonnes and India approximately 6 million tonnes, maintaining their positions as leading producers. This abundant raw material availability supports integrated processing industries and ensures consistent supply. Peanut oil is deeply embedded in regional cuisines due to its high smoke point and distinct flavor, making it a staple cooking medium in both households and foodservice sectors.

On the demand side, consumption patterns continue to strengthen due to rising incomes and urbanization. Projections by the OECD–FAO indicate that per capita vegetable oil consumption in India is expected to grow at around 3.1% annually, reaching nearly 24 kg per capita by 2027. Additionally, the expansion of e-commerce platforms is accelerating market growth; in China, online retail sales of physical goods reached approximately CNY 15.4 trillion ($2.2 trillion) in 2024, with food-related categories growing by about 16%. These combined supply and demand dynamics firmly establish Asia Pacific as both the largest and a structurally resilient growth hub for the peanut oil market.

Competitive Landscape

The global peanut oil market is witnessing intense competition among key players as they focus on advanced processing techniques, product innovation, and strategic investments to strengthen their market presence. Several manufacturers are adding premium, minimally processed varieties to their portfolios in response to the rising demand for cold-pressed peanut oil. Cold-pressed peanut oil meets the growing demand for clean-label and organic products by retaining more nutrients, natural flavors, and antioxidants. To increase productivity and satisfy customer demand for chemical-free oils, companies are investing in automation and state-of-the-art extraction facilities.

The market expansion is driven by strategic alliances and acquisitions, as companies enter rising areas including Asia-Pacific and Latin America. The worldwide peanut oil industry's competitive environment is being further shaped by ethical production, sustainable sourcing, and innovative branding.

Key Market Developments

- In December 2025, Fishfa Agri World introduced PeanutJi Vedic, India’s first high-oleic groundnut oil.

- In November 2023, Bharat Botanics proudly announces the grand opening of its cutting-edge wood-pressed cold oil processing facility in Gujarat, India. Spanning 16,000 square feet, this advanced and automated facility is designed to uphold the highest standards of hygiene and transparency.

- In August 2023, Tata Consumer Products (TCP), the consumer products arm of the Tata Group, has announced its entry into the premium and fast-growing cold-pressed oils segment under its brand ‘Tata Simply Better.’

Companies Covered in Peanut Oil Market

- ADM

- Cargill, Inc

- Olam Group

- Wilmar International Ltd

- Bunge Limited

- Marico

- Hain Celestial Group, Inc.

- Patanjali Ayurved Limited

- AAK

- Tata Consumer Products Limited

- Ventura Foods®

- Liberty Group

- Saraswathi Mills

- Mother Dairy Fruits & Vegetable Pvt Ltd

- Others

Frequently Asked Questions

The global peanut oil market size is expected to reach approximately US$ 11.7 billion in 2026.

The global peanut oil market is driven by increasing consumer demand for healthier cooking oils, growing awareness of its nutritional benefits, and expanding applications in the food industry.

East Asia region dominates the global peanut oil market.

A key opportunity lies in premium cold-pressed and specialty peanut oils sold via online and specialty retail channels, targeting health-conscious consumers seeking quality and traceability.

ADM, Cargill, Inc., Olam Group, Wilmar International Ltd, Bunge Limited, Marico, and Hain Celestial Group, Inc. are the leading players in the Global Peanut Oil market.