- Inks, Coatings, Adhesives & Sealants (ICAS)

- Paint Mixing Market

Paint Mixing Market Size, Share, and Growth Forecast 2025 - 2032

Paint Mixing Market By Paint Type (Water-Based Paints, Others), Equipment Type (Automatic Paint Mixers, Others), Application (Paint Manufacturers, Paint Users, Commercial Applications, Food & Equipment Machinery, Manufacturing Industry), and Regional Analysis for 2025 - 2032

Paint Mixing Market Size and Trends Analysis

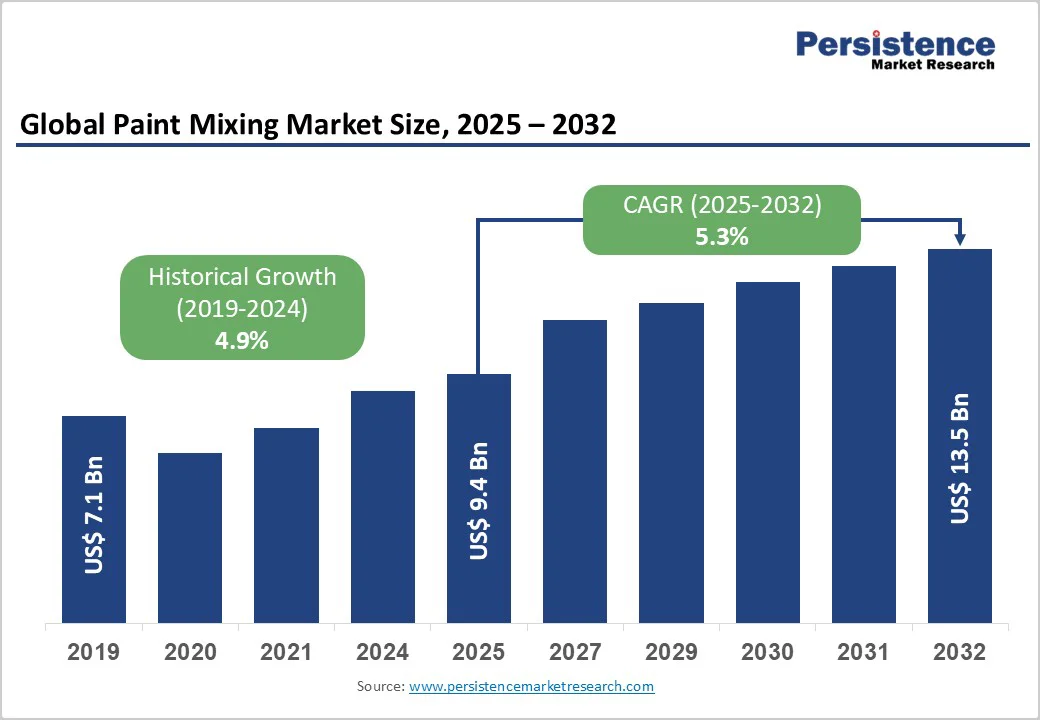

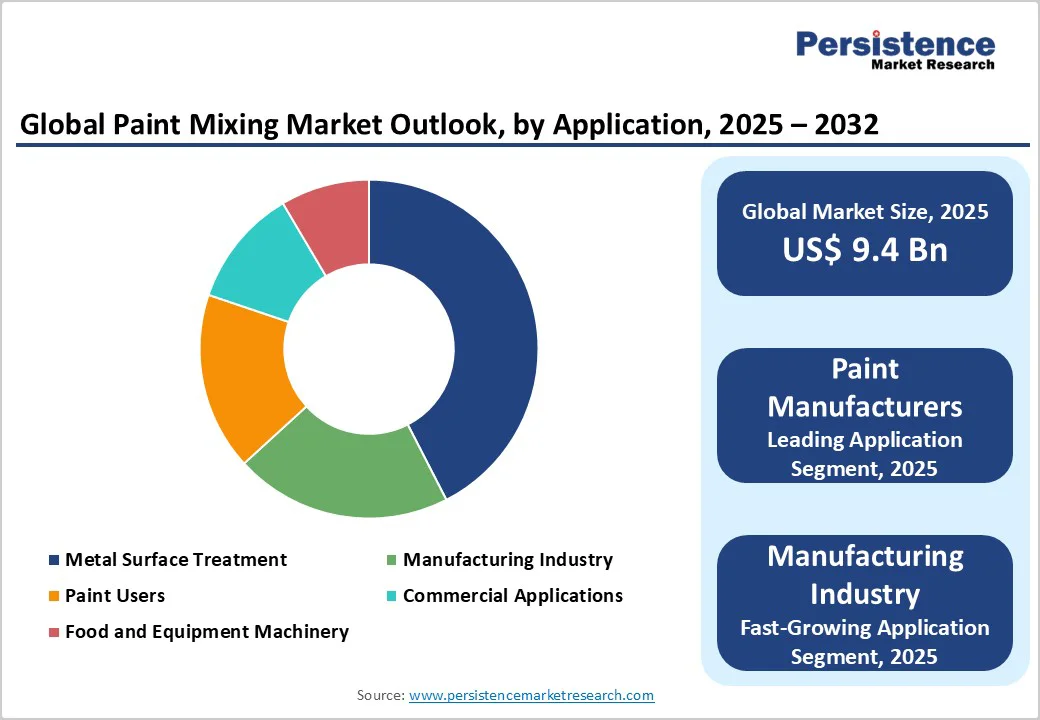

The global paint mixing market size is likely to be valued at US$9.4 Billion in 2025 and is expected to reach US$13.5 Billion by 2032, growing at a CAGR of 5.3% during the forecast period from 2025 to 2032, driven by increasing automation in industrial processes and rising demand for customized paint solutions across various sectors.

The expansion of construction activities globally and the automotive industry's need for precision color matching are the key factors propelling market advancement.

Key Industry Highlights

- Leading Region: North America dominates the paint mixing market with a 35% market share, driven by advanced manufacturing capabilities, strict regulatory frameworks, and robust automotive and construction sectors requiring precision mixing solutions.

- Fastest-Growing Region: Asia Pacific represents the fastest-growing region with a 6.5% CAGR, fueled by rapid industrialization in China and India, massive infrastructure development projects, and expanding automotive manufacturing capacity.

- Leading Paint Type Segment: The water-based paints segment leads with 65% market share due to environmental regulations limiting VOC emissions and growing consumer preference for eco-friendly formulations across residential and commercial applications.

- Fastest-Growing Equipment Type Segment: Automatic paint mixers are the fastest-growing segment with a 6.0% CAGR, driven by industrial automation trends, labor cost reduction needs, and demands for consistent quality in high-volume production operations.

- Key Market Opportunity: Smart manufacturing integration presents an opportunity through IoT-enabled systems, AI-driven color-matching platforms, and predictive maintenance technologies that can reduce waste by 15% while improving operational efficiency.

| Key Insights | Details |

|---|---|

| Paint Mixing Market Size (2025E) | US$9.4 Bn |

| Market Value Forecast (2032F) | US$13.5 Bn |

| Projected Growth CAGR (2025-2032) | 5.3% |

| Historical Market Growth (2019-2024) | 4.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Industrial Automation and Efficiency Demand

The paint mixing market is witnessing substantial growth due to the widespread adoption of automation technologies across manufacturing industries. Modern automatic paint mixers have transformed production processes by ensuring consistent color formulations and significantly reducing human error, often reducing error rates to below 2%. These advanced systems are capable of processing up to 25,000 liters per batch while maintaining precise temperature and viscosity levels through automated controls.

The integration of PLC-based control systems has further enhanced operational efficiency, enabling manufacturers to achieve high customer satisfaction rates of up to 93% and reduce processing time by as much as 60%. High-speed dispersing equipment, capable of peripheral speeds of 5,200 feet per minute, has improved particle size reduction and deagglomeration efficiency, reinforcing the market’s growth momentum driven by automation and precision demands.

Growing Demand from Construction and Automotive Industries

The expansion of global construction activities and the rise in automotive production are driving significant demand for precision paint mixing equipment. In Asia Pacific, where infrastructure projects exceed US$180 Billion annually, large-scale mixing operations are essential for architectural and protective coatings. This rapid development in the construction sector is boosting demand for advanced paint mixing solutions that ensure uniformity and high-quality finishes.

Similarly, automotive manufacturers, particularly electric vehicle producers, require specialized systems capable of handling waterborne basecoats and primers with annual capacities reaching 2,000 tonnes per facility. The growth of the automotive paint spraying equipment market further complements this trend, as precisely mixed formulations are crucial for optimal coating performance, collectively propelling the overall expansion of the paint mixing market across these key industrial sectors.

Barrier Analysis - High Initial Capital Investment and Maintenance Costs

The paint mixing equipment market is constrained by the high upfront costs associated with advanced industrial-grade systems. Automatic paint mixers can range from US$50,000 to US$250,000, depending on capacity and automation features, creating significant barriers for small and medium-sized enterprises.

Beyond initial purchase, additional expenses such as specialized installation, staff training, and ongoing maintenance can increase total investment by 30-40%. The complexity of modern mixing systems demands skilled technicians and regular calibration, leading to continuous operational costs that are difficult for many manufacturers to justify, particularly in price-sensitive regions, thereby limiting market adoption and growth among smaller players.

Environmental Regulations and Compliance Challenges

Stringent environmental regulations on volatile organic compound (VOC) emissions are creating compliance challenges for paint mixing equipment manufacturers and users. Many countries now limit VOC content to below 50 grams per liter for architectural paints, necessitating specialized equipment capable of handling water-based formulations.

Transitioning from solvent-based to eco-friendly alternatives often requires substantial modifications or complete overhauls of existing systems, with costs reaching hundreds of thousands of dollars. Smaller manufacturers with limited resources face difficulties in upgrading equipment and implementing compliance monitoring systems, restricting their ability to meet regulatory standards and thereby posing a significant restraint on market growth.

Opportunity Analysis - Expansion in Emerging Markets and Smart Manufacturing

The paint mixing market offers significant growth potential in emerging economies, where rapid industrialization and urbanization are boosting demand for advanced manufacturing equipment. Asia Pacific markets, led by China and India, are witnessing strong growth due to large-scale infrastructure projects that require efficient and consistent paint mixing operations.

The integration of Industry 4.0 technologies, such as IoT-enabled mixing systems and AI-driven color-matching platforms, is opening new revenue streams for equipment manufacturers. These smart systems optimize mixing parameters in real-time, predict maintenance needs, reduce waste by up to 15%, and ensure batch consistency. The development of mobile and modular mixing units provides flexible solutions for temporary construction sites and smaller-scale operations, further expanding market reach in these regions.

Growth in Specialized Applications and Eco-Friendly Solutions

Emerging applications in specialized sectors, including marine coatings, aerospace, and renewable energy infrastructure, are creating niche opportunities for precision paint mixing equipment. The wind turbine installation boom, particularly in North Sea coastal regions, requires advanced mixing systems capable of producing durable protective coatings under extreme environmental conditions.

The rising demand for water-resistant and acrylic paints, incorporating nano-additives and functional ingredients, is driving the adoption of sophisticated mixing technologies. Growing emphasis on sustainability has led manufacturers to invest in systems compatible with bio-based resins and recycled materials, with some reporting a 25% increase in orders for eco-friendly equipment. Precision mixing for self-healing and smart paint formulations also enables premium pricing opportunities, positioning equipment suppliers to capitalize on high-value niche segments.

Category-wise Analysis

Paint Type Insights

Water-based paints dominate the paint mixing market, accounting for approximately 65% of the total share, driven by environmental regulations and consumer preference for low-VOC formulations. Regulatory compliance in Europe and North America, where over 85% of new homes use water-based interior paints, further supports this leadership. In 2024, global consumption of water-based paints exceeded 21 million metric tons, with Asia Pacific leading at 9.5 million metric tons.

Mixing equipment for these formulations requires specialized technology to handle viscosity variations and ensure uniform pigment dispersion. High-shear mixing is particularly important when incorporating titanium dioxide and other inorganic pigments, making the development of advanced mixing systems crucial for consistent quality and optimal performance in large-scale production environments.

Equipment Type Insights

Automatic paint mixers are the fastest-growing equipment segment, holding 47% market share and projected to grow at a 6.0% CAGR through 2032. These systems meet industrial demands for consistency, labor efficiency, and precise mixing, with capabilities to handle batch sizes from 3 liters to 25,000 liters at speeds up to 6,000 RPM. Leading companies such as DynaMix and Charles Ross & Son Company offer features such as 360-degree rotation and hydraulic lifting for operational flexibility.

Semi-automatic mixers retain 35% market share due to cost-effectiveness for medium-scale operations. Manual mixers continue to serve niche applications requiring operator control and precision, particularly for specialty coatings and customized color formulations. Together, these equipment types address varying operational scales and industry needs.

Application Insights

Paint manufacturers form the largest application segment, representing 38% of market share, as they require high-capacity mixing systems for continuous production. Major producers, including Benjamin Moore, Dulux, and Behr Paint, invest heavily in modern mixing technologies to reduce waste and achieve up to 95% material utilization efficiency.

The manufacturing industry accounts for 28% of market demand, driven by specialized coatings for automotive, aerospace, and marine applications. Commercial applications, such as retail paint shops and automotive paint facilities, hold a 22% share, requiring smaller-capacity but highly precise mixers for custom color matching. These segments collectively define the operational requirements for the paint mixing market across scales and industries.

Regional Insights

North America Paint Mixing Market Trends

North America maintains market leadership with a 35% share, primarily driven by U.S. dominance in advanced manufacturing and strict regulatory frameworks favoring automated solutions.

The region's commercial construction sector reached US$180 Billion in 2024, directly translating to increased demand for premium architectural coatings and mixing equipment. California and Northeast states lead the adoption of low-VOC water-borne technologies, with regulatory compliance driving 60% of new equipment installations.

The U.S. automotive manufacturing, particularly in the Rust Belt and Southeast corridors, has accelerated demand for anti-corrosion coating systems requiring specialized mixing capabilities.

The implementation of AI-driven color-matching platforms in major metropolitan areas has reduced repaint cycle times by 40%, creating new equipment replacement opportunities. Mexico's maquiladora zones contribute significantly to regional growth through OEM demand for high-performance powder coating systems, with manufacturing output increasing 25% year-over-year.

Europe Paint Mixing Market Trends

Europe represents 30% of global market share, with Germany, the U.K., France, and Spain driving regional performance through regulatory harmonization and technological innovation.

The European Green Deal has stimulated renovation programs targeting 35 million buildings by 2030, significantly boosting specialty coatings consumption and mixing equipment demand. Water-borne systems captured 66.81% revenue share in 2024 and are expected to grow at 3.76% CAGR through 2030.

Germany's automotive manufacturing hubs require advanced mixing systems for electric vehicle coating applications, while North Sea coastal regions benefit from accelerating wind-turbine installations, driving protective coating demand.

PPG Industries established a 2,000-tonne capacity facility in Southeast Asia to serve both European export markets and regional automotive demand, demonstrating the interconnected nature of global mixing equipment supply chains. The Netherlands and Ireland’s tech clusters are increasingly adopting semiconductor and electronics coatings, requiring ultra-precise mixing capabilities.

Asia Pacific Paint Mixing Market Trends

Asia Pacific leads global growth with a 6.5% CAGR and a 42% market share projection by 2030, driven by China, Japan, India, and ASEAN manufacturing advantages.

China maintains a 56.42% regional share through unmatched construction scale and automotive assembly capacity, with Tier-1 and Tier-2 cities shifting toward premium water-borne, low-odor interior paints. India projects a 5.58% CAGR as the fastest regional growth, supported by smart-city programs and highway expansion projects requiring specialized coating applications.

Thailand's coatings industry, valued at US$1.34 Billion, benefits from international carmaker expansion, particularly electric vehicle manufacturers requiring specialized mixing systems. Indonesia has implemented sensor-based dosing systems and automated mixing lines to reduce waste and improve consistency in industrial applications.

Vietnam's electronics hubs sustain demand for clean-room-qualified epoxies, while Malaysia's palm-oil facilities specify heavy-duty anti-corrosive formulations requiring specialized mixing capabilities. Japan and South Korea remain innovation centers with strict VOC regulations and subsidy programs for green-ship retrofits.

Competitive Landscape

The global paint mixing market exhibits a fragmented competitive structure, with no single player holding a dominant position. This fragmentation allows specialized manufacturers to compete effectively through technological innovation, regional expertise, and tailored solutions for diverse customer needs. Companies differentiate themselves by offering advanced automation, energy-efficient designs, and modular systems that provide flexibility for different production scales.

Market leaders are focusing on strategies such as strategic acquisitions, substantial R&D investments, and expansion into high-growth regions. Emerging business models, including equipment-as-a-service and predictive maintenance contracts, are creating recurring revenue streams while helping customers reduce capital expenditure, further driving market competitiveness and innovation.

Key Market Developments

- In March 2025, PPG Industries inaugurated a new facility in Samut Prakan, Thailand, with an annual capacity to produce 2,000 tonnes of waterborne automotive basecoats and primers, featuring automated spray application technology.

- In November 2025, PPG Industries' MOONWALK automated paint mixing system achieved deployment across body shops in all 50 USA states, delivering productivity gains exceeding 10% and establishing new industry efficiency benchmarks.

Companies Covered in Paint Mixing Market

- DynaMix

- Farfly Machinery

- Hua Yun

- Charles Ross & Son Company

- Hockmeyer Equipment Corporation

- NDCO

- Netzsch Premier Technologies

- Xtrutech Ltd.

- Brillux

- Sartorius

- Ginhong

- Accio

- Dedoes Industries

- Mixer Direct

- Eastwood

- Graco Inc.

- J. Wagner GmbH

- Nordson Corporation

Frequently Asked Questions

The paint mixing market was valued at US$9.4 Billion in 2025 and is projected to reach US$13.5 Billion by 2032, growing at a CAGR of 5.3% during the forecast period.

The paint mixing market is driven by increasing industrial automation, rising demand for customized paint solutions, expansion of construction and automotive industries, and the need for precision color matching in manufacturing processes.

Water-based paints dominate the market with approximately 65% market share, driven by environmental regulations limiting VOC emissions and growing consumer preference for eco-friendly formulations.

North America leads the market with a 35% share, driven by advanced manufacturing capabilities, strict regulatory frameworks, and robust automotive and construction sectors requiring precision mixing solutions.

Key opportunities include expansion in emerging Asia Pacific markets with 6.5% CAGR growth, smart manufacturing integration through IoT-enabled systems, and specialized applications in marine coatings and renewable energy infrastructure.

Major players include DynaMix, Charles Ross & Son Company, Hockmeyer Equipment Corporation, Graco Inc., J. Wagner GmbH, Nordson Corporation, Farfly Machinery, Netzsch Premier Technologies, and Brillux.