- Inks, Coatings, Adhesives & Sealants (ICAS)

- Specialty Paints and Coatings Market

Specialty Paints and Coatings Market: Size, Share, Trends, Growth, and Forecast 2025 - 2032

Specialty Paints and Coatings Market by Resin Type (Epoxy, Acrylic, Polyester, Polyurethane (PU), Others), Product Type (Radiation-cured Coatings, Powder Coatings, Waterborne Coatings, Solvent-borne Coatings, Others), Application, and Regional Analysis for 2025 - 2032

Specialty Paints and Coatings Market Size and Trends Analysis

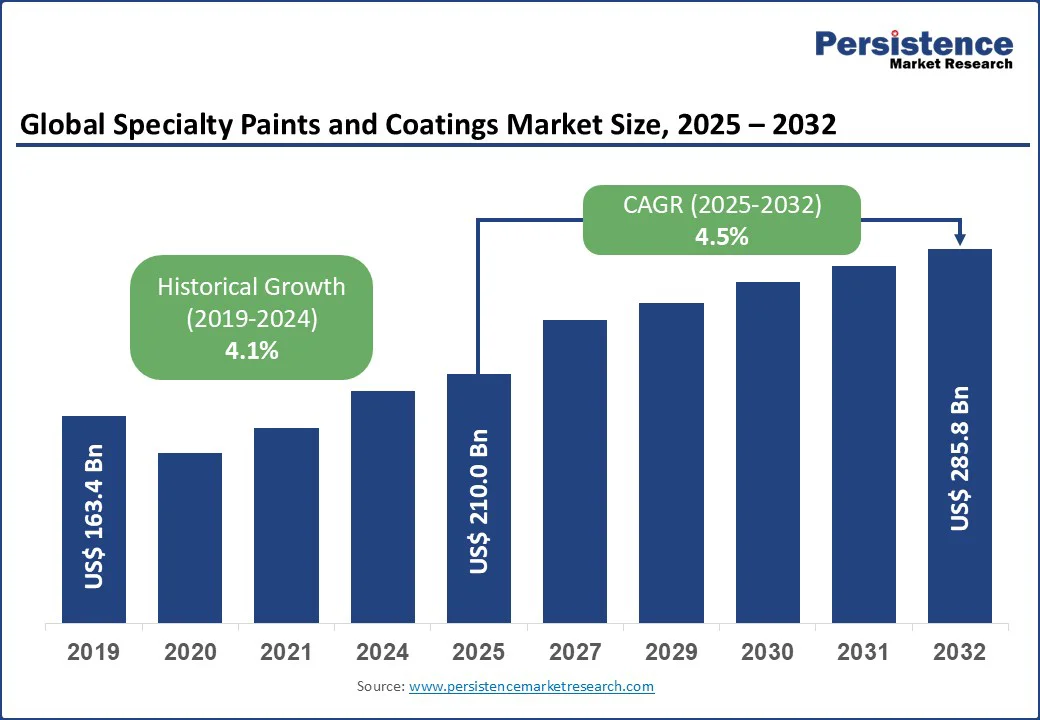

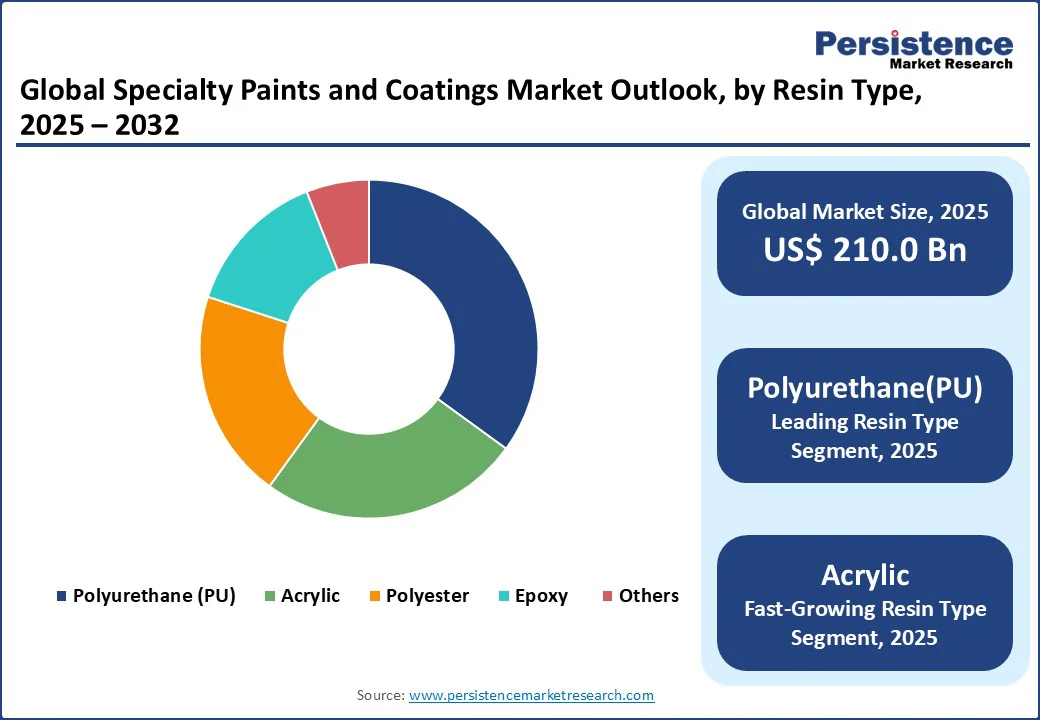

The global specialty paints and coatings market size is likely to be valued at US$ 210 Bn in 2025, and is expected to reach US$ 285.8 Bn by 2032, growing at a CAGR of 4.5% during the forecast period from 2025 to 2032.

This growth is fueled by rapid urbanization and infrastructure development, technological innovations such as nano and self-healing coatings, stringent environmental regulations promoting eco-friendly products, expanding automotive production including electric vehicles, and increasing demand from industries such as aerospace and marine for advanced protective coatings.

Key Industry Highlights:

- Consumer Trends: Demand for high-performance, eco-friendly coatings rises by 20%, fueled by regulatory pressures and preference for low-VOC products in architecture and automotive sectors.

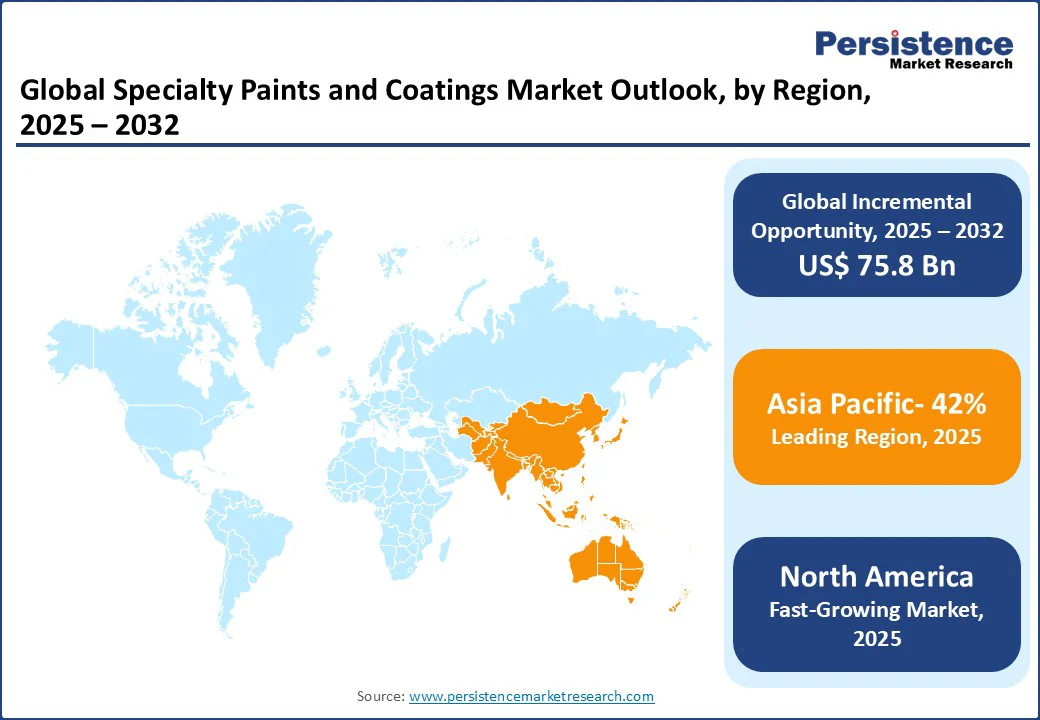

- Leading Region: Asia Pacific dominates with a 42% market share in 2025, driven by rapid industrialization, urbanization, and government infrastructure investments in China and India.

- Fastest-Growing Region: North America experiences strong growth due to sustainable building trends and the adoption of eco-friendly coatings, with the U.S. market valued at over US$630 million.

- Leading Resin Type: Polyurethane (PU) holds a 35% market share, widely used for its durability and corrosion resistance, especially in protective coatings and automotive refinish applications.

- Leading Application: Architectural coatings account for 38% of the specialty paints and coatings market, supported by increasing residential and commercial construction worldwide.

- Fastest-Growing Application: Protective coatings are growing rapidly, driven by infrastructure upgrades and a rising demand for corrosion-resistant solutions.

|

Global Market Attribute |

Key Insights |

|

Specialty Paints and Coatings Market Size (2019) |

US$163.4 Bn |

|

Specialty Paints and Coatings Market Size (2025E) |

US$210.0 Bn |

|

Market Value Forecast (2032F) |

US$285.8 Bn |

|

Projected Growth (CAGR 2025-2032) |

4.5% |

|

Historical Market Growth (CAGR 2019-2024) |

4.1% |

Market Dynamics

Driver: High Demand in End-user Industries

Growth in end-user industries is a major driver of the specialty paints and coatings market. Expanding sectors such as construction, automotive, aerospace, and marine increase the demand for advanced coatings with superior durability, corrosion resistance, and aesthetic properties.

For instance, the U.S. Department of Transportation’s Infrastructure Investment and Jobs Act allocates over $1 trillion towards upgrading roads, bridges, and public infrastructure, significantly boosting demand for protective and decorative coatings in construction projects. This government-backed infrastructure development fuels market growth by increasing demand for specialty coatings.

For instance, the automotive sector’s transition to electric vehicles (EVs), supported by incentives in the U.S. Inflation Reduction Act, is creating a surge in demand for innovative, sustainable coatings that enhance battery protection and vehicle lifespan.

Additionally, aerospace growth, backed by Federal Aviation Administration (FAA) data showing increased aircraft manufacturing, drives demand for lightweight, high-performance coatings. These examples from government initiatives highlight how growth in end-user industries propels the specialty paints and coatings market forward.

Restraint: Volatility in Raw Material Prices

Challenges such as raw material price volatility and stringent environmental regulations are pertinent. In 2025, prices for key resins such as epoxy and polyurethane fluctuated by 15% due to supply chain disruptions, increasing production costs and impacting profitability for manufacturers, particularly in price-sensitive regions. Compliance with VOC emission regulations, such as those enforced by the EU and the U.S. EPA, has increased production costs by 12%, limiting adoption among small-scale producers.

Competition from conventional paints and alternative materials, used in 35% of architectural applications, restricts market penetration in budget-driven projects. High energy costs in powder coating production, up by 10% due to volatile energy markets, pose operational challenges. Supply chain constraints, including a 12% shortage in titanium dioxide and other pigments, further hinder production capacity, particularly for waterborne and powder coatings, limiting growth in developing regions.

Opportunity: Sustainability and Use of Organic Compounds

The shift toward sustainable and high-performance coatings presents significant opportunities. The global green building materials market drives demand for eco-friendly coatings, with low-VOC waterborne coatings gaining 25% market share. Innovations in bio-based coatings, supported by US$ 6 billion in R&D investments, target protective and packaging applications, growing by 18% in 2025.

The rise of smart cities, with 120 projects planned globally by 2030, is expected to increase demand for specialty coatings in commercial and industrial applications by 20%. E-commerce for construction chemicals, growing at 15%, enhances accessibility for powder and waterborne coatings.

Emerging markets, with 2.5 billion urban consumers by 2030, offer untapped potential, particularly for acrylic coatings in high-performance architectural applications. These opportunities position specialty coatings as critical components in sustainable and durable construction solutions.

Segmental Insights

Resin Type Insights

In 2025, Polyurethane (PU) dominates with a 35% market share, driven by its superior durability, corrosion resistance, and versatility across industrial applications. PU coatings are extensively used in protective coatings and automotive refinish segments, accounting for nearly 65% of total PU resin demand.

Known for excellent adhesion, abrasion resistance, and long-lasting performance, polyurethane coatings are ideal for infrastructure, marine, and heavy machinery sectors. Their ability to withstand extreme environments makes PU the top choice among high-performance coating materials, solidifying its position as the leading resin type in the global market.

Acrylic coatings emerge as the fastest-growing segment, with demand rising by 18% in 2025, particularly in architectural and decorative applications. Acrylic resins are favored for their weather resistance, UV stability, and low-VOC formulations, aligning with increasing environmental regulations and sustainability goals. Their widespread adoption in residential and commercial construction supports strong growth across North America, Europe, and Asia Pacific.

Product Type Insights

Waterborne coatings lead in 2025 with a dominant 40% market share, driven by stringent environmental regulations and growing demand for low-VOC, eco-friendly coatings. These formulations are widely adopted across architectural and industrial applications, accounting for nearly 70% of total waterborne coatings usage.

Their ease of application, lower toxicity, and compliance with green building standards have made them the preferred choice in residential and commercial construction. As sustainability becomes a central focus in coatings technology, waterborne solutions continue to gain traction in developed markets such as North America and Europe.

Powder coatings are the fastest-growing product type in 2025, with market demand rising by approximately 20%, particularly in automotive and general industrial applications. These coatings offer superior durability, chemical resistance, and environmental benefits, such as zero solvent emissions. With increasing adoption in appliances, furniture, and metal fabrication, powder coatings are becoming a key solution for industries seeking performance and sustainability.

Application Insights

Architectural coatings dominate in 2025, capturing a 38% market share, driven by rising global demand in construction and renovation. With nearly 60% adoption across residential and commercial projects, architectural applications benefit from rapid urbanization, energy-efficient building initiatives, and government-funded infrastructure programs.

The growing focus on aesthetics, weather resistance, and sustainability has accelerated the shift toward low-VOC and waterborne solutions, especially in developed markets such as North America and Europe. This segment continues to lead due to its wide application scope and steady market demand.

Protective coatings stand out as the fastest-growing application segment, driven by increasing requirements for infrastructure durability and asset protection. These coatings are critical in extending the lifespan of bridges, highways, pipelines, and marine structures.

The rising focus on corrosion resistance and high-performance finishes is supported by government infrastructure spending, particularly in emerging markets. This demand surge positions protective coatings as a key growth area in the specialty coatings landscape.

Regional Insights

North America Specialty Paints and Coatings Market Trends

North America is the fastest-growing region in 2025, driven by a strong surge in sustainable construction and rising demand for eco-friendly solutions. The U.S. alone contributes over US$630 million, with 65% of consumers prioritizing low-VOC products.

Waterborne coatings for architectural use have increased by 15%, while protective coatings gain traction due to infrastructure upgrades. Backed by US$ 60 billion in green building investments, the region sees growing adoption of high-performance, low-emission coatings. Leading players such as The Sherwin-Williams Company and PPG Industries Inc. are innovating to meet this sustainable market demand.

Europe Specialty Paints and Coatings Market Trends

Europe is expected to hold a significant share of the specialty paints and coatings market in 2025, driven by robust environmental regulations, sustainable construction practices, and advancements in coating technologies. Countries such as Germany, France, and the UK are leading demand, especially in architectural, automotive, and industrial applications.

The region’s strict VOC limits and emphasis on circular economy practices have driven high adoption of waterborne and powder coatings. Government incentives for energy-efficient buildings and renovation projects further boost market growth. With a well-established industrial base and growing focus on green innovation, Europe remains a key contributor to global coatings demand.

Asia Pacific Specialty Paints and Coatings Market Trends

Asia Pacific dominates the specialty paints and coatings market in 2025 with a commanding 42% market share, driven by rapid urbanization, industrialization, and infrastructure development in countries such as China and India. Strong demand from the construction, automotive, and manufacturing sectors drives growth, supported by an increase in residential and commercial projects. The region is also witnessing increasing adoption of eco-friendly, low-VOC coatings due to tightening environmental regulations.

Additionally, government initiatives promoting smart cities and sustainable development further accelerate market expansion. With a large consumer base and continuous investments in industrial modernization, the Asia Pacific region remains the leading growth hub for specialty coatings globally.

Competitive Landscape

The global specialty paints and coatings market features a highly competitive landscape driven by innovation and sustainability. Leading manufacturers focus on developing eco-friendly, low-VOC formulations and advanced coating technologies such as waterborne and powder coatings. Strategic expansions, mergers, and acquisitions strengthen their global presence and production capacity.

Companies prioritize R&D to meet rising demand in construction, automotive, and industrial sectors. This dynamic competition fosters product differentiation and market growth, positioning key players to capitalize on the increasing emphasis on sustainable and high-performance specialty coatings worldwide.

Industry Developments:

- In January 2025: Axalta Coating Systems partnered with Dürr Systems AG to launch digital painting solutions tailored for automotive OEMs. This collaboration integrates Axalta’s NextJet™ precision paint application technology with Dürr’s cutting-edge robotics systems. The joint effort focuses on advancing overspray-free, maskless painting techniques for tutone and vehicle graphics, aiming to improve design versatility, minimize material waste, and boost production efficiency. This strategic alliance is set to drive innovation in automotive coating processes and support more sustainable manufacturing practices.

- In June 2023: AkzoNobel Powder Coatings launched the Interpon Futura Collection, featuring three contemporary color palettes: Merging World, Healing Nature, and Soft Abstraction. This innovative collection is completely free of solvents and volatile organic compounds (VOCs), aligning with AkzoNobel’s commitment to sustainability. By offering eco-friendly powder coating options, the Interpon Futura Collection supports greener manufacturing practices while meeting modern design trends, reinforcing the company’s leadership in sustainable coatings solutions.

Companies Covered in Specialty Paints and Coatings Market

- The Sherwin-Williams Company (US)

- PPG Industries Inc. (US)

- AkzoNobel N.V. (Netherlands)

- Axalta Coating Systems LLC (US)

- Jotun A/S (Norway)

- Nippon Paint Holdings Co., Ltd. (Japan)

- Kansai Paint Co., Ltd. (Japan)

- RPM International Inc. (US)

- Hempel A/S (Denmark)

- BASF Coatings GmbH (Germany)

- Others

Frequently Asked Questions

The specialty paints and coatings market is projected to reach US$ 210 Bn in 2025, driven by demand in architectural and protective coatings.

Key drivers include global construction growth, eco-friendly coating demand, and urbanization.

The specialty paints and coatings market is expected to grow at a CAGR of 4.5% from 2025 to 2032, reaching US$ 285.8 Bn.

Opportunities include sustainable coating formulations, smart city projects, and e-commerce growth.

Leading players include The Sherwin-Williams Company, PPG Industries Inc., AkzoNobel N.V., and Axalta Coating Systems LLC.