- Industrial Machinery

- Order Picker Market

Order Picker Market Size, Share, and Growth Forecast 2026 – 2033

Order Picker Market Product Type (Electric Power, Diesel/Oil Power, Gas Power), Sales Channel (Offline, Online), Application (Retail & Logistics, E-Commerce, General Manufacturing, Construction, Healthcare), Region Analysis 2026-2033

Order Picker Market Size and Share Analysis

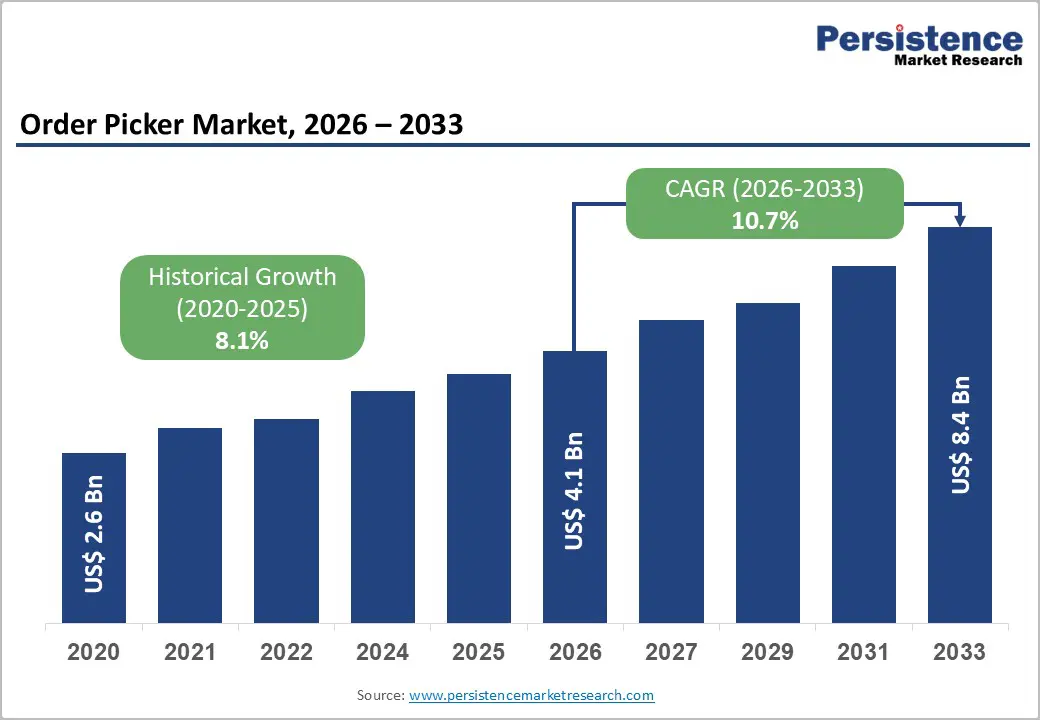

The global Order Picker Market size is likely to be projected at US$ 4.1 Billion in 2026 and is projected to reach US$ 8.4 Billion by 2033, growing at a CAGR of 10.8% between 2026 and 2033.

Market expansion is driven by e-commerce explosion growing at 14.4% CAGR with USD 5.5 trillion projected market by 2027 creating sustained warehouse automation demand, systematic warehouse automation acceleration with 64% of companies investing in automation and 30% expanding material handling equipment for labor efficiency, and technological advancement integrating AI-powered robotics, IoT-enabled real-time monitoring, and advanced warehouse management systems optimizing order fulfillment operations.

Key Highlights Summary

- Electric power order pickers command 61% market share emphasizing sustainability and automation compatibility, while diesel/oil expands at 6% CAGR supporting heavy-duty applications and regions with limited infrastructure.

- Offline sales channel leads at 71% market share with established dealer networks, while online expands at 13.7% CAGR supporting emerging digital procurement platforms and SME operators.

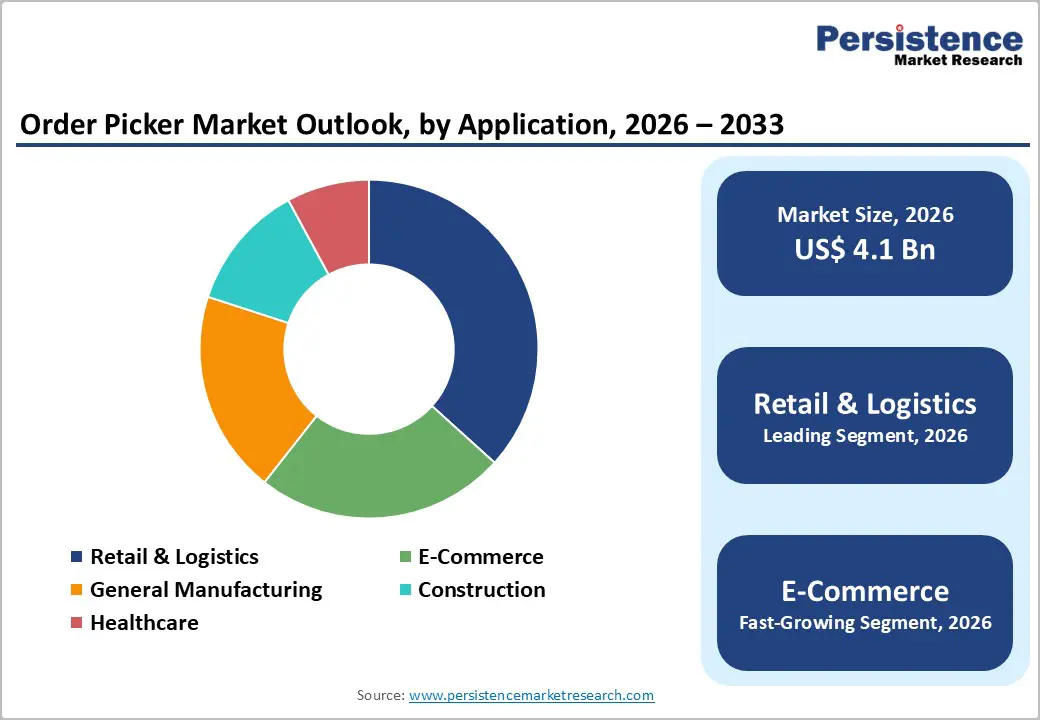

- Retail & logistics maintains 36.7% market share as largest application segment, while e-commerce expands at 13.6% CAGR driven by same-day fulfillment requirements and emerging fulfillment center expansion.

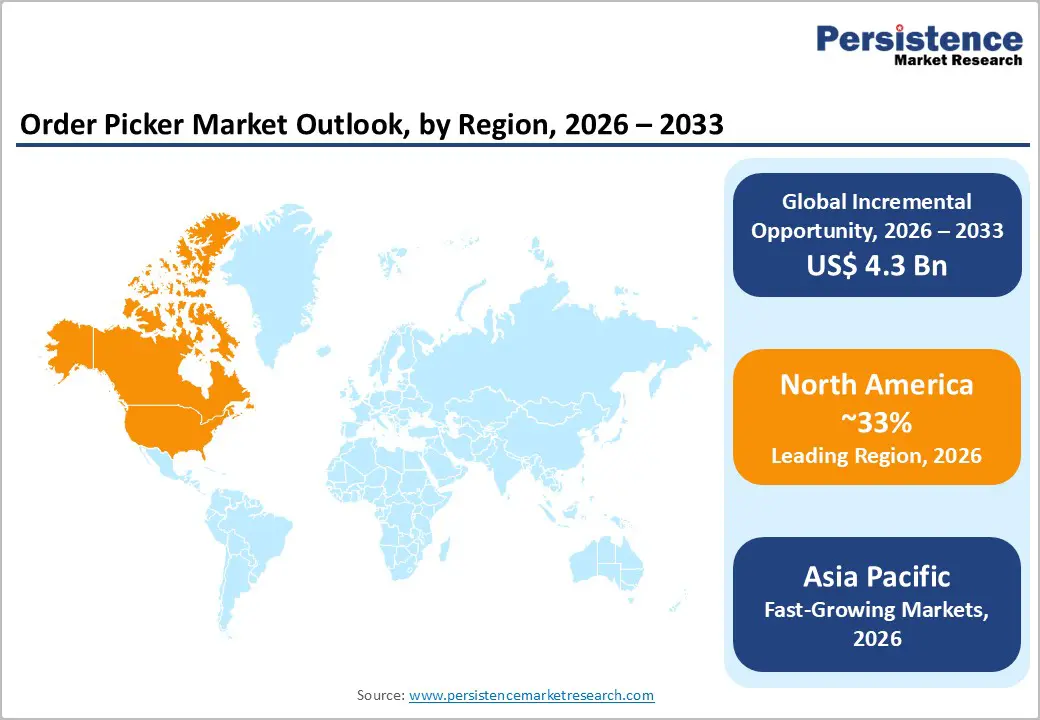

- North America grows at 10.3% CAGR with safety compliance focus, Europe maintains 26% share at 9.4% CAGR with sustainability emphasis, Asia Pacific dominates with 31% share and fastest growth with China (6.9%) and India (6.4%) CAGR.

- Jungheinrich introduces automated order picking systems (January 2024), Ocado unveils autonomous mobile robot (March 2025), manufacturers launch AI-powered camera systems (February 2025) demonstrating automation advancement and technology leadership momentum.

| Key Insights | Details |

|---|---|

| Order Picker Market Size (2026E) | US$ 4.1 billion |

| Market Value Forecast (2033F) | US$ 8.4 billion |

| Projected Growth CAGR (2026-2033) | 10.8% |

| Historical Market Growth (2020-2025) | 8.1% |

Market Dynamics Analysis

Market Drivers

E-Commerce Sector Expansion and Same-Day Fulfillment Requirements Accelerating

E-commerce sector expansion and same-day fulfillment requirements are systematically driving order picker demand, as global online retail growth creates sustained pressure for faster, more accurate material handling operations. The shift toward high-frequency, low-latency order cycles forces warehouses to optimize picking speed, accuracy, and labor utilization. Parallel expansion of business-to-business e-commerce further amplifies high-volume fulfillment needs, where reliability and throughput become mission critical. In this environment, order pickers function as core assets within modern warehouse logistics networks, enabling rapid picking, reduced error rates, and consistent operational performance. These efficiency improvements justify ongoing capital investment, particularly across retail and logistics operations where fulfillment intensity, service-level expectations, and competitive differentiation increasingly depend on advanced order picking capabilities across global supply chain ecosystems worldwide.

Warehouse Automation Acceleration and Labor Efficiency Focus

Warehouse automation acceleration and heightened focus on labor productivity are systematically driving order picker adoption across global warehouses. Survey insights show widespread investment in automation and technology, with many companies prioritizing information systems and material handling equipment to improve throughput and accuracy. A significant share of respondents anticipate meaningful increases in material handling spending, reflecting sustained automation momentum rather than short-term experimentation. In this environment, order pickers equipped with advanced automation capabilities, ergonomic design enhancements, and predictive maintenance functionality directly address labor shortages, safety concerns, and uptime requirements. These features deliver measurable efficiency gains, lower operating risk, and faster return on investment, creating a compelling business case for equipment upgrades, particularly for electric-powered solutions aligned with operational efficiency objectives.

Market Restraints

High Capital Investment and Charging Infrastructure Requirements

Market expansion is constrained by high capital investment requirements for advanced order picker systems and associated infrastructure, particularly as electric fleet transitions demand significant charging and power upgrades. These upfront costs create adoption barriers for small and mid-sized warehouses and operators in developing regions. In addition, equipment price volatility, supply chain uncertainty, and limited access to financing restrict purchasing decisions among budget-constrained users. As a result, replacement cycles are extended and technology adoption slows, potentially moderating growth momentum in cost-sensitive segments despite strong long-term efficiency and automation benefits overall globally.

Supply Chain Disruption and Labor Skill Requirements

Market expansion is constrained by high capital investment requirements for advanced order picker systems and associated infrastructure, particularly as electric fleet transitions demand significant charging and power upgrades. These upfront costs create adoption barriers for small and mid-sized warehouses and operators in developing regions. In addition, equipment price volatility, supply chain uncertainty, and limited access to financing restrict purchasing decisions among budget-constrained users. As a result, replacement cycles are extended and technology adoption slows, potentially moderating growth momentum in cost-sensitive segments despite strong long-term efficiency and automation benefits overall globally.

Market Opportunities

Asia Pacific Rapid Industrialization and E-Commerce Infrastructure Development

Asia Pacific represents a substantial opportunity, holding nearly 31% market share and demonstrating the fastest growth trajectory, driven by rapid industrialization and accelerating e-commerce expansion across China and India. Rising consumer demand, expanding fulfillment networks, and increasing SKU complexity are pushing warehouses toward modernization and higher material handling efficiency. Government-led infrastructure investments in logistics parks, freight corridors, and industrial zones further strengthen regional supply chain capabilities. Simultaneously, manufacturers and construction players are scaling capacity, supporting sustained equipment demand beyond retail logistics. These factors collectively create high-volume adoption potential for order picker equipment across manufacturing, construction, and distribution environments. As regional players transition from manual handling to semi-automated warehouses, demand for reliable, cost-efficient, and scalable order picking solutions accelerates rapidly regionwide.

Advanced Material Handling Automation and Autonomous Mobile Robots

Advanced automation integration represents a major opportunity as autonomous mobile robots and collaborative robots gain traction, with nearly 30% of companies actively evaluating AMR adoption for storage, order fulfillment, and pick-and-place operations. This shift supports the emergence of robotic integration and hybrid automation models that combine human flexibility with machine precision. Simultaneously, AI-driven robotics and IoT-enabled connectivity are transforming order picking into scalable, intelligent, and adaptable systems capable of real-time decision-making and predictive optimization. These technologies improve throughput, accuracy, and uptime while reducing labor dependency and operational risk. As a result, solution providers can justify premium pricing through demonstrable efficiency gains, future-ready architectures, and differentiated technology leadership across modern, high-velocity warehouse and logistics environments globally to sustain long-term competitive advantage.

Segmentation Analysis

Product Type Analysis

Electric power order pickers command 61% of market share, representing dominant product type with zero-emissions operation, lower operational costs, reduced noise pollution, and advanced automation compatibility. Superior integration with warehouse management systems, extended battery technology, and charging infrastructure maturity support broad adoption across retail, logistics, and e-commerce sectors driving consistent volume growth and market stability anchor.

Diesel/oil powered order pickers expand at 6% CAGR driven by extended range capabilities, outdoor warehousing applications, and regions with limited charging infrastructure. Heavy-duty capabilities and operational flexibility support emerging demand particularly in construction and general manufacturing applications justifying continued investment in alternative power solutions.

Sales Channel Analysis

Offline sales channel commands 71% of market share, representing established distribution model with direct dealer relationships, comprehensive equipment demonstrations, and aftermarket support. Established dealer networks and equipment evaluation capabilities support consistent sales momentum particularly among large logistics operators and fleet buyers requiring equipment testing and customization.

Online sales channel expands at 13.7% CAGR driven by digital marketplace platforms, direct-to-customer sales models, and equipment comparison capabilities. Emerging preference for remote purchasing, faster ordering, and logistics optimization support emerging high-growth channel particularly among SME operators and emerging market buyers seeking efficient procurement.

Application Analysis

Retail and logistics applications command 36.7% of market share, driven by high-volume distribution requirements, rapid inventory turnover, and order fulfillment complexity. Established warehouse infrastructure and operational maturity support consistent demand across major retail chains, logistics hubs, and distribution centers sustaining market stability anchor.

E-commerce applications expand at 13.6% CAGR driven by explosive online shopping growth, same-day delivery requirements, and fulfillment center expansion. Emerging customer expectations for speed and accuracy and e-commerce CAGR of 14.4% globally support fastest application segment growth creating sustained demand for automated order picking solutions justifying substantial capital investment particularly in advanced automation capabilities.

Regional Market Insights

North America

North America expands at 10.3% CAGR supported by established warehouse automation ecosystem, stringent safety regulations (OSHA standards), and technology innovation leadership driving consistent capital investment in advanced material handling equipment. Mature e-commerce infrastructure with rapid last-mile delivery requirements and strong purchasing power support sustained demand for premium order picker equipment with advanced automation capabilities particularly in major logistics hubs including California, Texas, and New Jersey. Established dealer networks and comprehensive aftermarket support enabling rapid technology adoption and equipment optimization. Strong emphasis on safety compliance and operator ergonomics driving adoption of advanced features. Partnership ecosystems supporting innovation in autonomous systems integration.

Europe

Europe maintains 26% market share with 9.4% CAGR growth driven by stringent environmental regulations promoting electric equipment adoption, regulatory harmonization (CE marking), and advanced technical expertise particularly in Germany, United Kingdom, and France. Strong sustainability emphasis and energy-efficiency focus supporting premium electric-powered equipment adoption with advanced features prioritized across diverse warehouse applications from retail distribution to manufacturing. Established technical expertise in custom solutions and specialized applications. Strong emphasis on operator safety and ergonomic design. Advanced logistics infrastructure supporting efficient equipment deployment and utilization.

Asia Pacific

Asia Pacific dominates with 31% market share and fastest regional growth momentum driven by rapid e-commerce expansion, warehouse modernization, and manufacturing scale advantages particularly with China and India establishing manufacturing hubs. Government infrastructure investment in logistics networks and e-commerce platform growth supporting emerging high-volume demand with cost-competitive manufacturing enabling rapid regional supply chain development and market penetration across diverse applications. Emerging manufacturing capabilities and cost-competitive production enabling regional market dominance. Rapid infrastructure development supporting warehouse automation expansion. Rising e-commerce adoption driving fulfillment center expansion across major cities.

Competitive Landscape

Strategic Developments

- In January 2024, Jungheinrich announced expanded product portfolio including automated order picking systems designed to enhance operational efficiency through advanced warehouse management system integration, ergonomic improvements, and predictive maintenance capabilities supporting emerging market demand for intelligent picking solutions.

- In March 2025, Ocado presented advanced autonomous mobile robot system enabling warehouse workflow automation including cross-docking, bulk-item picking, putaway, and pallet movement demonstrating emerging robotic integration in material handling operations.

- In February 2025, Manufacturers launched advanced AI-powered camera systems enabling real-time material handling visibility and warehouse efficiency optimization through computer vision and intelligent object recognition supporting predictive maintenance and operational optimization.

Business Strategies

Market leaders employ innovation-focused product development advancing AI-powered automation and IoT connectivity, cost leadership through manufacturing optimization and supply chain efficiency, geographic expansion targeting high-growth Asia Pacific markets, sustainability positioning through electric equipment advancement, and comprehensive aftermarket support excellence. Regional specialists focus on local expertise and equipment customization. Online-first retailers emphasize digital sales transformation and direct customer engagement.

Companies Covered in Order Picker Market

- Crown Equipment Corporation

- Toyota Material Handling

- Jungheinrich

- Raymond Corporation

- CLARK Material Handling

- Linde Material Handling

- Hyster-Yale

- Nichiyu

- Mitsubishi Logisnext

- STILL

- UniCarriers

- BT

- Balkancar

- Heli Forklift

Frequently Asked Questions

The global Order Picker Market is anticipated at US$ 4.1 Billion in 2026 and is projected to reach US$ 8.4 Billion by 2033.

Market growth is primarily driven by the e-commerce boom requiring faster fulfillment, rising warehouse automation adoption to address labor shortages, and technological advancements such as AI-powered robotics, IoT-based monitoring, and predictive maintenance that significantly improve picking efficiency and uptime.

The market expands at 10.8% CAGR between 2026 and 2033.

Key opportunities include Asia-Pacific warehouse modernization, expanding autonomous and hybrid automation systems, and the fast-growing online sales channel, enabling OEMs to scale digital distribution and advanced order-picking solutions.

Leading players include Crown Equipment Corporation, Toyota Material Handling, and Jungheinrich, supported by Raymond, Linde, and CLARK, with continuous innovation driven by automated systems, AI-powered solutions, and autonomous mobile robot integration.