- Pharmaceuticals

- Autism Spectrum Disorder Treatment Market

Autism Spectrum Disorder Treatment Market Size, Share, and Growth Forecast, 2026 – 2033

Autism Spectrum Disorder Treatment Market by Communication & Behavioral Therapies (Applied Behavior Analysis, Speech & Language Therapy, Others), Drug Therapy (Antipsychotic Drugs, Others), Drug Distribution Channel, and Regional Analysis 2026 – 2033

Autism Spectrum Disorder Treatment Market Size and Trends Analysis

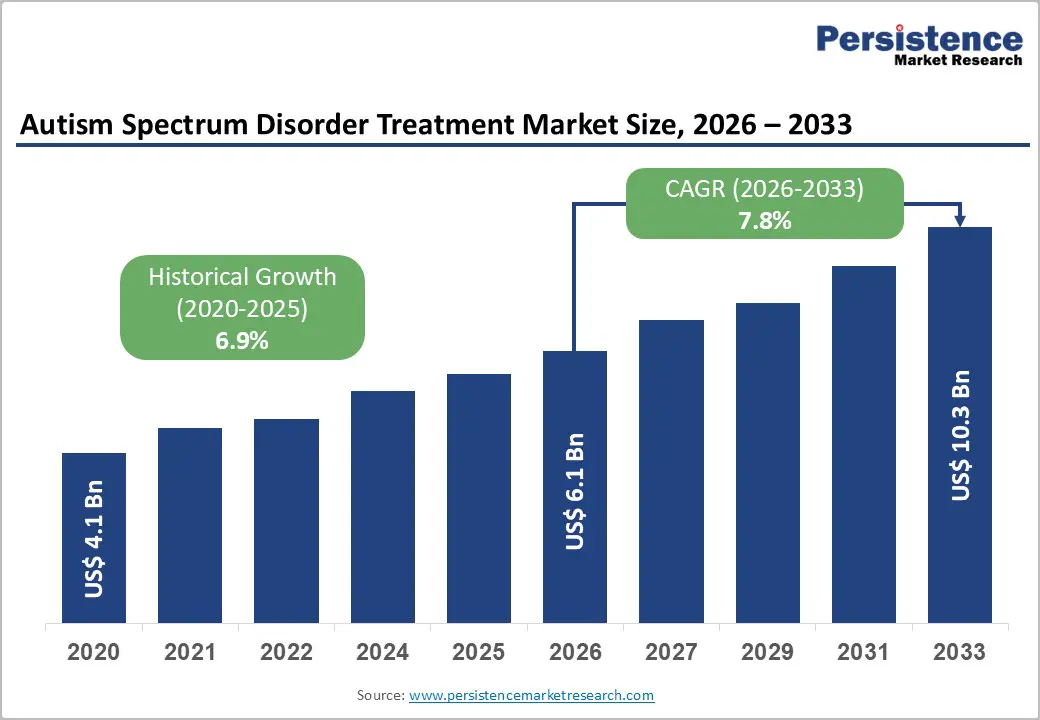

The global autism spectrum disorder treatment market size is likely to be valued at US$6.1 billion in 2026 and is expected to reach US$10.3 billion by 2033, growing at a CAGR of 7.8% during the forecast period from 2026 to 2033, driven by the rising global prevalence of ASD, which has spurred significant investments in behavioral intervention infrastructures and pharmacological research. Advanced diagnostic capabilities and increased government mandates for insurance coverage of behavioral therapies are the primary catalysts for market expansion. Furthermore, the integration of digital health tools and the expansion of specialized clinic franchises are optimizing service delivery across both developed and emerging economies.

Key Industry Highlights:

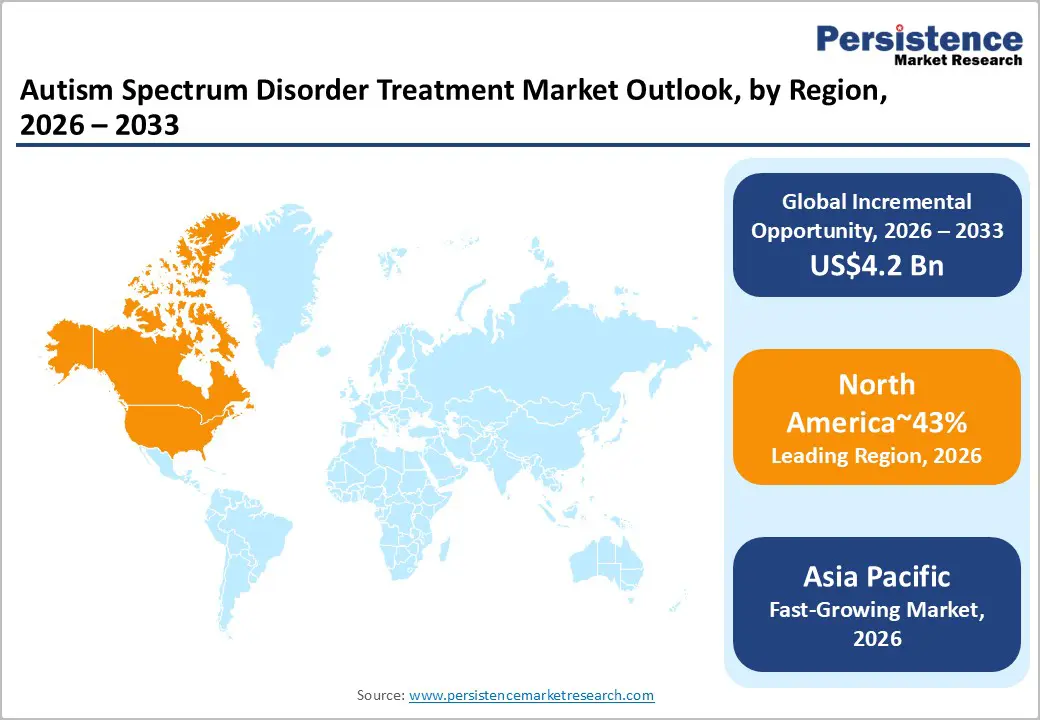

- Leading Region: North America is projected to lead due to highly structured healthcare systems, early screening mandates, and integrated behavioral-pharmacological service models, accounting for approximately 43% share in 2026, supported by AI-driven diagnostics, telehealth integration, and mature provider networks.

- Fastest-Growing Region: Asia Pacific is anticipated to grow fastest due to rapid urbanization, government-led screening initiatives, tele-ABA adoption, and expanding private healthcare access across multiple countries.

- Leading Communication & Behavioral Therapy: Applied Behavior Analysis (ABA) is expected to lead, accounting for approximately 59% share in 2026 through standardized clinical adoption, validated outcome tracking, integrated digital platforms, and high-value pediatric applications.

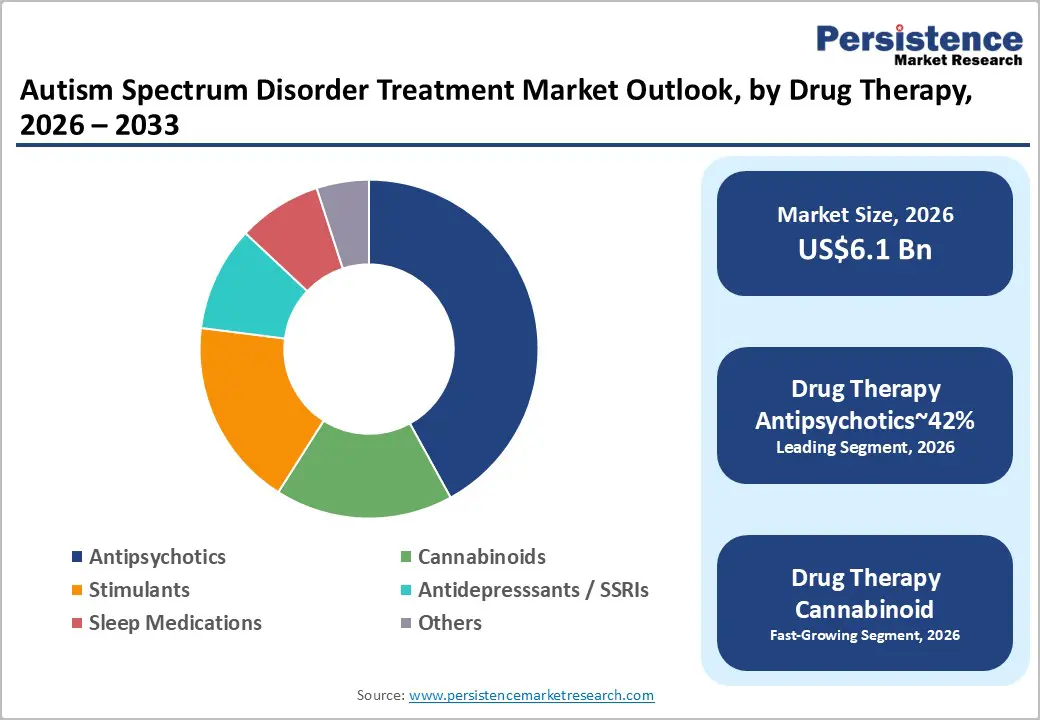

- Leading Drug Therapy: Antipsychotic drugs are projected to dominate due to their established clinical efficacy, widespread adoption, and functional integration across pediatric and adolescent care settings, holding approximately 42% share in 2026.

| Report Attribute | Details |

|---|---|

|

Autism Spectrum Disorder Treatment Market Size (2026E) |

US$6.1 Bn |

|

Market Value Forecast (2033F) |

US$10.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Expanding Diagnostic Recognition and Early Intervention Demand in Autism Care

The rising recorded prevalence of autism spectrum disorder is structurally expanding demand across diagnostic, therapeutic, and support services. Public health surveillance increasingly reports higher identification rates among children due to refined clinical screening protocols. Broader diagnostic criteria introduced through modern psychiatric classification frameworks have expanded the clinical recognition of autism spectrum disorder. Pediatric healthcare providers now implement standardized developmental screening during routine early childhood medical assessments. Greater caregiver awareness and educational outreach also improve early symptom recognition across multiple healthcare systems. The resulting service utilization momentum directly reinforces long-term growth dynamics across the autism treatment ecosystem.

Early intervention frameworks are becoming embedded within healthcare and educational policy structures across major economies. Legislative mandates supporting developmental disability services require structured therapy access during formative childhood developmental stages. Clinical research increasingly demonstrates that early therapeutic engagement improves functional independence and developmental outcomes. Improved long-term outcomes simultaneously reduce lifetime care burdens for healthcare systems and social services. This evidence base strengthens government funding support for therapy infrastructure and specialist workforce development. The expanding ecosystem stimulates investment across diagnostic technologies, therapy training programs, and multidisciplinary treatment facilities.

Digital Therapeutics and Telehealth Integration: Transforming Autism Care Delivery

Rapid adoption of telehealth platforms is reshaping therapeutic delivery models within autism spectrum disorder treatment ecosystems. Digital consultation systems enable remote behavioral therapy sessions, expanding accessibility across geographically dispersed patient populations. This transition reduces reliance on centralized therapy facilities and mitigates longstanding appointment scheduling bottlenecks. Technology-enabled service delivery also supports continuity of care during periods of limited clinical mobility. Digital platforms facilitate caregiver participation in therapy routines, strengthening treatment adherence within home environments.

Emerging digital therapeutics are introducing advanced monitoring and engagement tools into autism treatment protocols. Artificial intelligence-driven applications continuously track behavioral patterns and therapy response indicators across patient populations. These systems generate structured data streams enabling clinicians to refine intervention strategies through evidence-based adjustments. Data-centric therapeutic models strengthen clinical outcome measurement and improve personalization of developmental support programs. Technology integration simultaneously attracts capital investment from digital health developers and specialized medical software providers. The expanding ecosystem links behavioral therapy delivery with advanced analytics, strengthening operational efficiency across autism care systems.

Barrier Analysis – High Long-Term Treatment Intensity Creating Financial and Operational Constraints

Autism spectrum disorder treatment requires sustained multidisciplinary therapy, creating structurally high long-term care expenditures. Behavioral intervention programs frequently demand intensive weekly therapy engagement across extended developmental periods. These treatment models require specialized clinicians trained in behavioral, speech, and developmental therapy disciplines. Insurance coverage frameworks partially offset expenses but frequently impose deductibles and copayment obligations. These cost-sharing structures transfer a meaningful financial burden onto households requiring long-duration therapy programs. Consequently, treatment affordability challenges reduce therapy adoption rates across price-sensitive healthcare markets.

Operational economics within therapy networks further intensify cost pressures across autism care delivery systems. Evidence-based treatment protocols require consistently low therapist-to-patient interaction ratios. Smaller providers particularly face margin compression due to recruitment, certification, and staff retention requirements. High operational overhead also complicates geographic expansion into underserved or resource-constrained healthcare regions. Financial constraints among families simultaneously reduce service continuity and long-term therapy adherence rates. Subsequently, cost intensity remains a structural restraint limiting the broader scalability of autism treatment services.

Workforce Shortage and Regulatory Barriers Limiting Autism Therapy Service Expansion

Autism treatment markets face persistent workforce shortages across behavioral therapy, speech therapy, and occupational therapy disciplines. Demand for specialized clinicians continues to rise as diagnostic recognition expands across pediatric healthcare systems. These requirements lengthen workforce development cycles and slow the entry of qualified professionals into therapy networks. Healthcare providers, therefore, encounter structural staffing limitations while attempting to expand treatment capacity. Service providers frequently maintain extended patient waitlists due to insufficient therapist availability. Limited workforce depth particularly constrains service delivery within rural communities and geographically underserved regions.

Regulatory frameworks governing professional licensure further complicate operational scalability within autism treatment service ecosystems. Licensing requirements often vary across jurisdictions, creating administrative barriers for therapists seeking multi-regional practice authorization. Healthcare organizations, therefore, encounter compliance burdens when attempting to expand therapy networks across multiple geographic markets. These governance mechanisms protect treatment quality but simultaneously slow workforce mobility and service expansion. Providers must invest substantial resources into recruitment, credential verification, and continuing professional development programs. These operational complexities elevate staffing costs while limiting the rapid deployment of therapy professionals.

Opportunity Analysis – Emerging Cannabinoid Therapeutics Addressing Behavioral and Sleep Disorders in Autism Care

Growing clinical exploration of cannabinoid-based compounds is opening new therapeutic pathways within autism treatment frameworks. These pharmacological candidates target behavioral symptoms frequently associated with autism, including anxiety regulation and sleep disturbances. As a result, healthcare researchers increasingly investigate cannabinoid derivatives for their neuromodulatory potential in developmental disorders. Early clinical observations suggest measurable improvements in behavioral stability and sleep quality among selected patient groups. Regulatory experimentation across multiple jurisdictions has begun enabling controlled therapeutic access through supervised medical programs. This evolving policy environment gradually expands clinical research infrastructure surrounding cannabinoid based treatment approaches.

Advancing research activity is encouraging collaboration between biotechnology developers, academic research institutions, and specialized clinical centers. Expanded trial activity simultaneously strengthens regulatory evidence requirements necessary for formal therapeutic approval pathways. Investment interest within the neurodevelopmental drug landscape is increasing as potential treatment gaps remain insufficiently addressed. The pharmaceutical ecosystem, therefore, recognizes cannabinoid based therapies as a potential adjunct to existing symptom management strategies. Continued investigation may diversify available pharmacological options within autism care, particularly for sleep and anxiety-related conditions. These developments support a gradually expanding opportunity space within neurodevelopmental therapeutics research.

Digital Pharmacy Platforms and Telehealth Ecosystems Expanding Autism Treatment Accessibility

The convergence of telehealth platforms with online pharmacy infrastructure is reshaping therapeutic access within autism treatment systems. Digital healthcare ecosystems allow patients and caregivers to obtain prescriptions and therapy support through integrated virtual channels. Teleconsultation services enable clinicians to evaluate symptoms, adjust medication protocols, and coordinate multidisciplinary treatment plans remotely. These capabilities reduce logistical barriers associated with repeated clinic visits, particularly for families managing long-term developmental therapy programs. Healthcare systems increasingly recognize remote access models as critical tools for expanding developmental disorder care. Consequently, digital pharmacy ecosystems are becoming an essential distribution channel within the evolving autism treatment market.

Advanced telecommunications networks support reliable teleconsultation, remote monitoring, and integrated prescription management platforms. These digital capabilities align strongly with changing healthcare consumption patterns among technologically engaged populations. Younger caregiver demographics increasingly prefer mobile-based healthcare access that integrates consultation, prescription, and monitoring functions. Pharmaceutical distributors and digital health providers are therefore investing in interoperable platforms linking telehealth consultations with medication fulfillment systems. Expanding e-pharmacy ecosystems are also creating cross-border opportunities for regulated digital medication distribution. Collectively, these developments position telehealth-enabled pharmacy networks as a major growth pathway within autism treatment infrastructure.

Category–wise Analysis

Communication & Behavioral Therapies Insights

Applied behavior analysis (ABA) therapy is expected to lead, accounting for approximately 59% share in 2026, underpinned by its entrenched clinical positioning as the primary behavioral intervention across pediatric developmental care settings. Adoption remains anchored in its structured, data-driven framework that systematically improves communication, social interaction, and adaptive behavior through reinforcement methodologies validated by extensive clinical research. Healthcare providers prioritize ABA due to its measurable treatment outcomes and compatibility with multidisciplinary therapy workflows involving speech and occupational interventions. Ongoing platform evolution, including AI-enabled behavior tracking, digital documentation systems, and predictive analytics tools, continues to strengthen therapy planning and clinical oversight. Leading providers such as BlueSprig Pediatrics, Centria Autism, and Hopebridge integrate technology ecosystems from CentralReach and Rethink Behavioral Health to standardize clinical workflows. This mature service infrastructure and strong provider ecosystem sustain ABA’s dominance across institutional autism treatment programs.

Applied behavior analysis therapy delivered through franchise-based center expansion is expected to be the fastest-growing segment, driven by scalability advantages and operational standardization across behavioral therapy networks. Large multi-site operators increasingly deploy standardized treatment protocols, workforce training models, and centralized data management systems to replicate clinic performance across geographic markets. Technology platforms such as CentralReach, Catalyst by DataFinch, and Rethink Behavioral Health enable real-time therapy documentation, progress analytics, and remote supervision capabilities. Expanding corporate providers, including Action Behavior Centers, BlueSprig, and Centria Autism, continue to establish new treatment centers to meet rising diagnosis rates. As digital workflow integration and operational scale improve, franchise-driven ABA delivery models are positioned to accelerate therapy accessibility across emerging autism care markets.

Drug Therapy Insights

Antipsychotic drugs are expected to lead, accounting for approximately 42% share in 2026, underpinned by their established clinical role in managing irritability, aggression, and severe behavioral dysregulation associated with autism. Adoption remains anchored by long-standing therapeutic familiarity and strong integration into psychiatric treatment protocols across pediatric and adolescent care environments. Physicians prioritize antipsychotics such as risperidone and aripiprazole due to their validated efficacy in stabilizing disruptive behavioral symptoms that frequently complicate developmental therapy programs. Continuous pharmacological optimization and improved dosing strategies are strengthening treatment tolerability and adherence across long term care settings. Pharmaceutical portfolios from companies including Johnson & Johnson and Bristol Myers Squibb maintain a dominant presence through established antipsychotic drug platforms.

Cannabinoid based therapies are expected to be the fastest-growing segment, driven by increasing scientific exploration of the endocannabinoid system’s role in regulating neurological and behavioral functions. Emerging pharmacological research highlights the potential of cannabinoid derived compounds in addressing anxiety, sleep disturbances, and emotional dysregulation frequently observed in autism patients. Biotechnology innovators are advancing clinical pipelines focused on cannabinoid formulations designed for neurodevelopmental disorders, supported by expanding clinical trial activity. Companies such as DeFloria and Charlotte’s Web are progressing investigational therapies, including AJA001, while broader industry participants explore multi cannabinoid drug platforms. Parallel growth in patient-driven interest toward alternative neurological therapies further accelerates market momentum.

Regional Insights

North America Autism Spectrum Disorder Treatment Market Trends

North America holds the leading position in the autism spectrum disorder market, accounting for 43% of the global share in 2026. The region benefits from highly structured healthcare delivery systems and mature regulatory governance frameworks. Public policy instruments continue strengthening early screening, therapy access, and specialized education programs. Federal legislation, such as the Individuals with Disabilities Education Act, mandates structured educational and therapeutic assistance for children diagnosed with autism spectrum disorder. This policy environment supports sustained demand for behavioral therapy, diagnostics, and pharmaceutical research. Advanced digital infrastructure enables integration of AI-assisted diagnostic platforms and digital screening technologies. Earlier diagnosis cycles expand the treatment window and extend long-term service engagement. As a result, therapy providers and diagnostic technology firms experience sustained demand expansion.

The U.S. shapes regional market momentum through deep research investment and strong clinical innovation capacity. Federal agencies, including the National Institutes of Health, support large research programs investigating neurological and developmental disorders. Regulatory oversight by the U.S. Food and Drug Administration accelerates approvals for emerging diagnostic technologies and treatment innovations. One prominent case includes the EarliPoint Evaluation developed by EarliTec Diagnostics and deployed at clinical centers including Marcus Autism Center. Organizations such as the Center for Autism and Related Disorders, Hopebridge LLC, and BlueSprig continue strengthening therapy capacity through structured behavioral intervention programs. Pharmaceutical research efforts from companies including Otsuka Pharmaceutical and Johnson & Johnson further expand treatment innovation pipelines.

Europe Autism Spectrum Disorder Treatment Market Trends

Europe represents the second-largest regional market for autism spectrum disorder services and therapeutics. The region maintains stable expansion supported by universal healthcare coverage and structured clinical treatment pathways. Countries including Germany, the U.K., and France lead regional demand through nationwide autism strategies and early screening programs. Public healthcare systems allocate significant resources toward speech therapy, occupational therapy, and behavioral interventions. Institutions such as the National Health Service fund a large portion of autism therapy services across the U.K. Regulatory coordination across member states continues to strengthen through the work of the European Medicines Agency and clinical evaluation frameworks such as the National Institute for Health and Care Excellence. As a result, therapy providers operate under strict reimbursement frameworks while expanding integrated care delivery models.

Research activity and healthcare innovation continue to reinforce Europe’s role in neurodevelopmental disorder research. Pharmaceutical developers increasingly invest in precision medicine and neurological drug discovery across the region. French biotechnology firm Aelis Farma recently initiated a multicenter clinical trial for AEF0217 targeting cognitive deficits in neurodevelopmental disorders. Digital health platforms are gradually entering behavioral therapy monitoring and clinical care management systems. For example, Roche expanded its Navigator digital health platform across Germany and the U.K. to enable remote behavioral therapy tracking. Despite strong public healthcare support, diagnostic waiting lists and reimbursement variation across member states remain operational challenges for therapy providers and healthcare institutions.

Asia Pacific Autism Spectrum Disorder Treatment Market Trends

Asia Pacific represents the fastest expanding regional market, driven by countries including China, Japan, India, and Southeast Asian economies. Rapid urbanization and improving healthcare infrastructure are increasing access to specialized neurodevelopmental treatment centers. Governments are also strengthening national screening initiatives and disability certification frameworks. India expanded standardized screening through the India Scale for Assessment of Autism digital platform across state healthcare systems. Regulatory institutions such as the Pharmaceuticals and Medical Devices Agency in Japan and the National Medical Products Administration in China are introducing faster approval pathways for neurodevelopmental drugs.

Technological integration and cost advantages continue shaping the regional market landscape. Telehealth platforms and mobile-based therapy programs are expanding quickly due to widespread smartphone adoption. In India, the Apollo Tele ABA Platform enables remote behavioral therapy sessions and digital monitoring for autism patients. Pharmaceutical companies are also strengthening their regional footprint through local manufacturing and generic antipsychotic production. Companies such as Otsuka Pharmaceutical and Johnson & Johnson maintain strong prescribing presence across hospitals and specialty clinics. Digital diagnostic tools, including AI-driven eye tracking systems, are increasingly used in rural screening programs.

Competitive Landscape

The global autism spectrum disorder treatment market is moderately consolidated, with leadership concentrated among pharmaceutical and behavioral therapy providers, including Centria Healthcare, ABA Centers of America, Otsuka Pharmaceutical, Roche, and Jazz Pharmaceuticals. These leaders exert significant functional influence through established clinical expertise, evidence-based protocols, and integrated care models that combine pharmacological and behavioral interventions. High entry barriers linked to professional credentialing and specialized training further strengthen incumbent positioning, allowing top players to maintain influence across regional and national networks while supporting quality and compliance standards.

Competitive positioning is defined by vertical integration in therapy provision and pharmaceutical portfolios, contrasted with niche specialization in tele-ABA and digital monitoring services. Leaders differentiate through validated clinical outcomes, operational scale, and multi-channel service networks, while market dynamics are shaped by private equity consolidation of smaller clinics, platform evolution, and cross-border partnerships.

Key Industry Developments:

- In February 2026, General Atlantic acquired Ally Pediatric Therapy through its ACES ABA platform. This acquisition reflects the continued private equity trend of consolidating multidisciplinary ASD service providers into a large-scale national platform.

- In September 2025, the U.S. FDA fast-tracked the approval of Leucovorin (folinic acid) for children with cerebral folate deficiency (CFD) exhibiting autism symptoms. This marks a milestone in precision medicine, offering a targeted pharmacological option for a specific physiological subtype of autism.

- In May 2025, DeFloria (a joint venture involving Charlotte’s Web) began preparations for Phase 2 trials of AJA001, the first full-spectrum CBD-based drug cleared by the FDA for an IND. The trial focuses on establishing titration for treating irritability in adolescents and young adults with ASD, marking a milestone for cannabinoid research.

Companies Covered in Autism Spectrum Disorder Treatment Market

- Centria Healthcare

- ABA Centers of America

- Otsuka Pharmaceutical

- Roche

- Jazz Pharmaceuticals

- Johnson & Johnson (Janssen)

- Center for Autism and Related Disorders (CARD)

- BlueSprig Pediatrics

- Eli Lilly and Company

- Acadia Pharmaceuticals

- Hopebridge Autism Therapy Centers

- Stepping Stones Group

- AstraZeneca

- Pfizer Inc.

- GW Pharmaceuticals

- CentralReach

Frequently Asked Questions

The global autism spectrum disorder treatment market is projected to be valued at US$6.1 billion in 2026 and is expected to reach US$10.3 billion by 2033, driven by rising prevalence, expanded early intervention programs, and integration of digital health platforms.

Early intervention and expanded diagnostic recognition are primary drivers, as structured screening protocols, caregiver awareness, and legislative mandates improve therapy initiation, functional outcomes, and long-term treatment adherence across pediatric populations.

The autism spectrum disorder treatment market is forecast to grow at a CAGR of 7.8% from 2026 to 2033, reflecting rising global prevalence and adoption of digital therapeutic delivery models.

Asia Pacific is the fastest-growing regional market, fueled by rapid urbanization, government-led screening initiatives, telehealth adoption, and regional cost advantages in behavioral therapy and pharmacological treatments.

The market is moderately consolidated, with key players including Centria Healthcare, ABA Centers of America, Otsuka Pharmaceutical, Roche, Jazz Pharmaceuticals, Johnson & Johnson (Janssen), Center for Autism and Related Disorders (CARD), BlueSprig Pediatrics, Eli Lilly and Company, Acadia Pharmaceuticals, Hopebridge Autism Therapy Centers, Stepping Stones Group, AstraZeneca, Pfizer Inc., GW Pharmaceuticals, and CentralReach.