- Specialty & Fine Chemicals

- Oil Line Corrosion Inhibitors Market

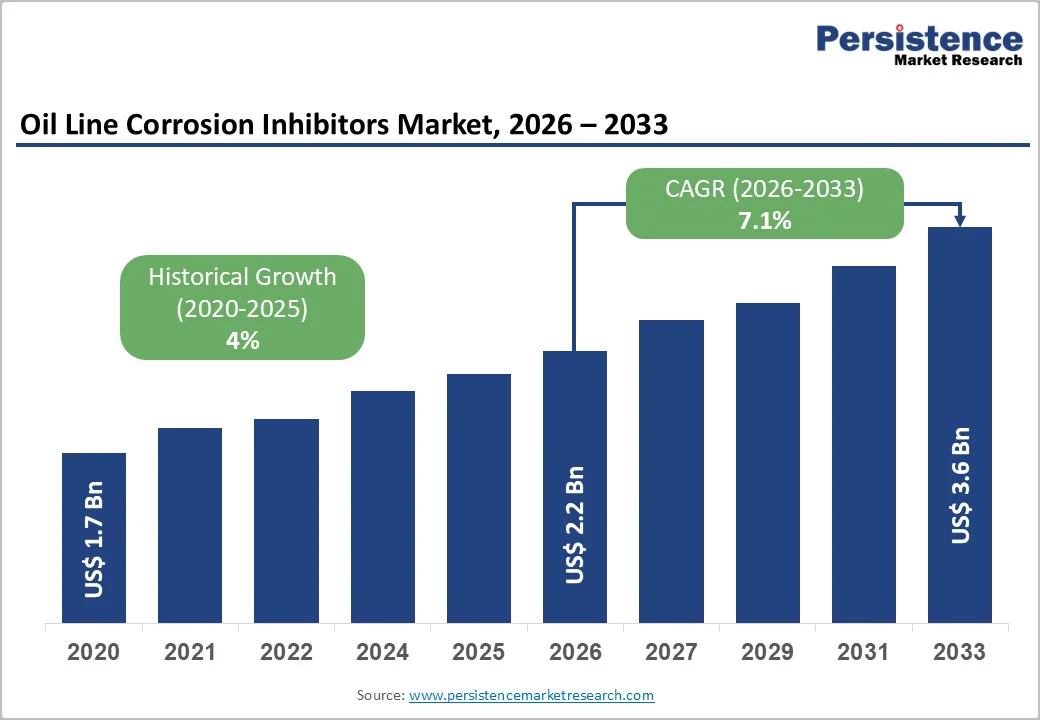

Oil Line Corrosion Inhibitors Market Size, Share, and Growth Forecast, 2026 - 2033

Oil Line Corrosion Inhibitors Market by Product Type (Organic Inhibitors, Inorganic Inhibitors), Application (Oil & Gas Production, Water Treatment, Process & Product Additives), End-User (Oil & Gas Industry, Power Generation, Metals Processing), and Regional Analysis for 2026-2033

Oil Line Corrosion Inhibitors Market Share and Trends Analysis

The global oil line corrosion inhibitors market size is likely to be valued at US$ 2.2 billion in 2026, and is projected to reach US$ 3.6 billion by 2033, growing at a CAGR of 7.1% during the forecast period 2026−2033. This substantial growth trajectory reflects the critical importance of corrosion protection in maintaining the integrity and longevity of oil transport infrastructure globally. The market expansion is primarily driven by aging pipeline infrastructure requiring enhanced protection, increased oil and gas exploration activities in challenging environments, and stringent regulatory mandates for environmental safety and operational reliability. The rising global energy demand, coupled with infrastructure investments in emerging economies, further amplifies the need for advanced corrosion management solutions across upstream, midstream, and downstream operations.

Key Industry Highlights

- Dominant Region: North America is expected to command about 37% market share in 2026, supported by its extensive oil and gas infrastructure.

- Fastest-growing Market: Asia Pacific is slated to be the fastest-growing market through 2033, owing to accelerated industrialization and large-scale infrastructure development.

- Leading & Fastest-growing Product Types: Organic inhibitors are poised to lead with an estimated 2026 share of 65%, while inorganic inhibitors are likely to register the highest CAGR during the 2026-2033 forecast period.

- Leading & Fastest-growing Applications: Oil & gas production is set to dominate with around 38% revenue share in 2026, with water treatment anticipated to grow the fastest from 2026 to 2033.

- Major Driver: With the expansion of oil and gas operations into increasingly complex and extreme environments, the demand for advanced corrosion control measures is likely to become highly critical.

- Market Opportunities: The integration of corrosion inhibitors with AI and IoT platforms is transforming modern asset protection strategies in the oil and gas industry.

| Report Attribute | Details |

|---|---|

|

Oil Line Corrosion Inhibitors Market Size (2026E) |

US$ 2.2 Bn |

|

Market Value Forecast (2033F) |

US$ 3.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Oil and Gas Infrastructure Investment and Aging Pipeline Networks

The global oil and gas industry is facing an increasingly complex challenge as its infrastructure ages, underscoring the urgent need for effective corrosion protection strategies. Corrosion has long been a hidden threat to profitability, gradually degrading pipelines, storage tanks, and production equipment across upstream, midstream, and downstream operations. This persistent issue not only endangers safety and environmental integrity but also disrupts production efficiency and drives up maintenance costs. As the industry continues to evolve, operators are placing greater emphasis on preventive maintenance and advanced corrosion mitigation solutions to extend asset lifespans and maintain a consistent energy supply. The growing adoption of digital monitoring, predictive maintenance, and material innovation highlights a broader transformation focused on preserving infrastructure integrity in an increasingly demanding operating environment.

As oil and gas activities expand into increasingly complex and extreme environments, the demand for advanced corrosion control measures is becoming more critical. Exploration in deepwater, Arctic, and unconventional reserves exposes assets to severe chemical and thermal conditions, accelerating corrosion and complicating maintenance operations. To mitigate these challenges, companies are investing in next-generation corrosion inhibitors designed to resist aggressive agents such as hydrogen sulfide, carbon dioxide, and high-salinity environments. These innovative solutions serve as a vital line of defense, supporting operational reliability, cost efficiency, and long-term asset sustainability.

Competition from Alternative Corrosion Protection Technologies

The oil line corrosion inhibitors market growth is facing mounting competition from alternative protection technologies that offer durable and often more sustainable solutions. Corrosion-resistant alloys, protective coatings, and cathodic protection systems have emerged as effective substitutes, particularly for new infrastructure projects. Although chemical inhibitors remain efficient and cost-effective for existing assets, the increasing use of materials such as stainless steel, duplex alloys, and composite structures reflects a broader shift toward inherently corrosion-resistant options. This advancement in material engineering enables operators to design longer-lasting systems and reduce reliance on continuous chemical treatments. As technology continues to evolve, these alternatives are redefining performance expectations, driving inhibitor manufacturers to innovate and diversify their product portfolios to remain competitive in a changing market.

However, evolving economic conditions and structural shifts in the energy sector continue to add complexity to market dynamics. Periods of low oil prices often compel operators to reduce operational spending, resulting in deferred maintenance schedules and lower frequencies of chemical treatment applications. Moreover, the global transition toward cleaner energy sources and the growing emphasis on renewables create uncertainty around long-term investments in traditional oil and gas infrastructure. This strategic shift may shape future demand patterns for corrosion inhibitors, prompting manufacturers to diversify into adjacent industrial sectors and emerging sustainable energy applications.

Digital Integration and Smart Corrosion Management Systems

The integration of corrosion inhibitors with digital technologies, AI, and IoT platforms is transforming modern asset protection strategies in the oil and gas industry. Smart corrosion management systems are now combining chemical applications with continuous digital monitoring to enhance operational control. Equipped with advanced sensors and predictive analytics, these systems enable real-time assessment of corrosion behavior, allowing operators to adjust inhibitor dosage and treatment timing with greater precision. This data-driven approach improves operational efficiency by optimizing chemical use, minimizing waste, and extending asset life. By incorporating intelligence into corrosion control processes, companies are shifting from reactive maintenance to proactive risk management, using insights from real-time data to detect and address potential issues before they escalate.

The growing adoption of connected monitoring systems signals a broader shift toward integrated digital ecosystems across industrial operations. Companies that combine chemical expertise with advanced analytics platforms are reshaping the value proposition of corrosion protection moving from standalone product sales to comprehensive, service-based models. Through remote diagnostics, automated reporting, and predictive maintenance tools, these integrated solutions deliver greater cost efficiency and higher reliability. Furthermore, the continuous flow of performance data fuels product innovation, strengthens customer relationships, and promotes long-term sustainability. Together, these developments highlight the rising importance of technology-driven asset integrity management in an increasingly digital industrial landscape.

Category-wise Analysis

Product Type Insights

Organic inhibitors are slated to maintain a dominant position in the market, with an estimated share of 65% in 2026. These inhibitors are in high demand due to their exceptional versatility, environmental compatibility, and superior performance across diverse operating conditions. Compounds such as amines, azoles, and polymer-based additives act by forming protective films on metal surfaces, preventing corrosive agents from directly contacting critical infrastructure. Their ability to perform effectively at low concentrations, combined with lower toxicity compared to inorganic alternatives, makes them a preferred choice for oil and gas operations. Furthermore, their stability across wide temperature and pressure ranges ensures consistent performance in challenging environments

Inorganic inhibitors is likely to be the fastest-growing segment during the 2026-2033 forecast period. This accelerated growth highlights the exceptional performance of inorganic inhibitors under extreme conditions involving high temperatures, elevated pressures, and aggressive chemical environments commonly found in refining operations and process equipment. These inhibitors are highly effective at forming passive protective films on metal surfaces, making them well-suited for critical infrastructure such as power generation facilities and chemical processing plants, where operating demands often exceed the capabilities of organic alternatives. Recent advancements in zinc-based and silicate-based formulations have further improved their performance while mitigating the environmental concerns historically linked to chromate-based products.

Application Insights

Oil & gas production is slated to dominate with an estimated 38% of the oil line corrosion inhibitors market revenue share in 2026. This dominance reflects the essential role of corrosion inhibitors in protecting pipelines, wellheads, production equipment, and gathering systems from corrosion-induced failures. The segment encompasses upstream operations, including drilling systems, production facilities, and transportation networks that require continuous corrosion protection to ensure operational reliability and safety. Corrosion inhibitors are injected into production fluids, drilling muds, and pipelines to mitigate damage from corrosive gases, formation waters, and process chemicals. Investment in oil and gas exploration, particularly in challenging environments such as offshore deepwater and high-pressure high-temperature (HPHT) reservoirs, drives sustained demand for specialized high-performance inhibitors.

Water treatment is anticipated to exhibit the highest CAGR between 2026 and 2033, fueled by increasing awareness of water quality management and infrastructure protection in industrial cooling systems, municipal water systems, and desalination facilities. Corrosion in water treatment plants poses significant operational challenges due to chemical exposure and constant water contact, necessitating effective inhibitor programs to protect tanks, pipes, heat exchangers, and distribution networks. The segment benefits from global water scarcity challenges that drive investment in water recycling, purification, and desalination infrastructure, all requiring comprehensive corrosion protection. Regulatory mandates for water quality and infrastructure safety, particularly in developed markets, further support the adoption of advanced inhibitor solutions.

End-User Insights

The oil and gas industry is set to lead with an approximate 36% revenue share in 2026. The corrosion inhibitors span the entire oil and gas value chain, encompassing upstream exploration and production, midstream transportation and storage, and downstream refining and distribution. This broad adoption reflects the industry's vast network of infrastructure vulnerable to corrosion, including extensive pipeline systems, offshore platforms, refineries, and storage facilities that require continuous protection. The segment’s dominance is reinforced by the high value of assets involved, strict safety requirements, and the severe economic impact of corrosion-related failures, all of which justify sustained investments in preventive measures.

Power generation is expected to grow the fastest across the 2026-2033 forecast period. Power plants, including coal-fired, gas-fired, nuclear, and renewable facilities, employ corrosion inhibitors to protect critical equipment such as turbines, boilers, heat exchangers, cooling systems, and condensers from degradation. The segment's growth is driven by global electrification trends, population growth-driven energy demand, and infrastructure investments in emerging markets. Developing nations in Asia Pacific and Africa are constructing substantial power generation capacity to support industrial growth and improve access to electricity, creating sustained demand for corrosion inhibitors.

Regional Insights

North America Oil Line Corrosion Inhibitors Market Trends

North America is set to command a significant portion of the oil line corrosion inhibitors market share at approximately 37% in 2026. The region’s dominance is supported by its extensive oil and gas infrastructure, which includes vast pipeline networks, mature production fields, large-scale shale development, and advanced refining capacity concentrated mainly in the United States and Canada. The U.S. market drives most of this regional demand, fueled by ongoing shale gas development in major basins such as the Permian, Eagle Ford, and Bakken, which require intensive corrosion management to mitigate the effects of aggressive production chemistries.

Key growth drivers include aging infrastructure that requires enhanced protection to prevent failures and environmental incidents, stringent regulatory frameworks enforced by agencies such as the Environmental Protection Agency (EPA) and the Department of Transportation (DOT), and continuous technological innovation supported by the region’s strong research and development ecosystem. The regulatory landscape places particular emphasis on pipeline integrity management, mandating regular inspections, maintenance, and corrosion prevention activities that sustain steady demand for inhibitor products and related services. North American companies remain at the forefront of global innovation in corrosion inhibitor technology, investing heavily in eco-friendly formulations, smart monitoring platforms, and tailored application solutions designed to address diverse operational requirements.

Europe Oil Line Corrosion Inhibitors Market Trends

The corrosion inhibitors market in Europe is shaped by stringent environmental regulations, mature oil and gas infrastructure, and a strong regional commitment to sustainability and circular economy principles. Key countries such as Germany, the United Kingdom, France, Spain, and Norway contribute to market demand through diverse industrial bases and energy-related activities. Germany remains a central hub, supported by its advanced manufacturing sector, chemical industry expertise, and focus on environmentally responsible production. Leading manufacturers leverage the country’s research and development capabilities to design high-performance, eco-friendly corrosion inhibitors aligned with European Union (EU) environmental standards. The United Kingdom’s market strength is sustained by offshore oil and gas operations, refining capacity, and chemical processing industries, while France’s nuclear and petrochemical sectors require specialized protection solutions.

The regulatory framework in Europe, defined by harmonized EU standards and strict compliance requirements, plays a pivotal role in shaping innovation and product development. It has accelerated the shift toward green chemistry, promoting biodegradable and low-toxicity inhibitor formulations. Collaboration among manufacturers, research institutions, and regulatory agencies continues to drive advanced solution development and digital integration. Growing opportunities lie in energy transition infrastructure, bio-based product innovation, and industrial expansion across emerging Eastern European economies.

Asia Pacific Oil Line Corrosion Inhibitors Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for oil line corrosion inhibitors through 2033, propelled by accelerated industrialization, urban expansion, and large-scale infrastructure development. The region’s growth is underpinned by expanding energy production, rising manufacturing output, and increasing investment in oil and gas infrastructure. China leads regional demand through its extensive refining and energy networks, while India follows closely, fueled by infrastructure modernization and supportive government initiatives. Japan continues to maintain steady demand with its advanced industrial base, high technological standards, and commitment to quality-driven operations.

Regional market growth is reinforced by government policies that promote energy security, industrial competitiveness, and long-term asset integrity. Continued investment in pipelines, refineries, and petrochemical facilities is driving strong demand for advanced corrosion protection solutions. The wide range of operating environments from offshore platforms to arid onshore fields has created a need for tailored, condition-specific inhibitors capable of addressing unique regional challenges. The competitive landscape features global corporations expanding their manufacturing and R&D presence alongside emerging local producers that provide cost-effective alternatives. Increasing focus on localization, smart corrosion monitoring, and environmentally sustainable formulations continues to shape market evolution across the region.

Competitive Landscape

The global oil line corrosion inhibitors market structure shows moderate consolidation, with leading players including Schlumberger Limited, Baker Hughes Company, Halliburton Company, BASF SE, and Ecolab Inc. collectively commanding 50–55% of total market share. These established firms leverage substantial manufacturing economies of scale, continuous research and development (R&D) investment programs, and long-standing partnerships with major petroleum and natural gas operators to maintain competitive advantages. Differentiation strategies emphasize technological innovation capabilities, application-specific technical expertise, service quality standards, and geographic market coverage. The resulting market structure facilitates constructive competition while preserving stability through incumbent leaders that possess adequate financial resources, technical infrastructure, and organizational capabilities to sustain ongoing innovation and comprehensive customer support across global regions.

Leading companies operate efficiently across integrated supply chains, leveraging their scale to absorb research expenses, navigate regulatory environments, and respond quickly to evolving customer requirements. Smaller and medium-sized enterprises can compete effectively through specialized product development, niche market focus, or superior technical service in underserved geographic regions or application segments. This consolidation also suggests barriers to entry for new innovators without substantial capital or existing market relationships. Forward-thinking industry entrants should therefore consider differentiation strategies such as developing superior formulations with extended inhibition duration, environmental compliance features, or predictive corrosion monitoring integration capabilities.

Key Industry Developments

- In October 2025, Bashneft commenced trial commercial operation of a composite material pipeline at the Munir Gallyamov field in Russia, replacing conventional steel and achieving five-fold faster installation speed through pipe make-up methods. The composite pipeline features non-corrosive properties, warranted service life of 50 years, reduced hydraulic losses through smooth inner surface geometry, and elimination of deposit accumulation.

- In May 2025, Hexigone Inhibitors Limited partnered with Alfaa Chem to deliver high-performance anti-corrosion technologies throughout the Gulf Cooperation Council (GCC) region with focus on construction, petroleum and natural gas, and infrastructure maintenance applications. Hexigone's proprietary Intelli-ion® technology enables effective corrosion protection at remarkably low loadings of 0.5%, reducing overall inhibitor content requirements by up to 66%.

- In February 2025, Blue Seal Energy Group inaugurated its state-of-the-art Chemical Production Plant in Nigeria, manufacturing a diverse portfolio of industrial and specialty chemicals including demulsifiers, scale inhibitors, sodium hypochlorite, corrosion inhibitors, and hydrogen sulfide (H2S) scavengers, among others. The facility has been established in response to the expanding demand for high-quality industrial chemicals across petroleum and natural gas, manufacturing, and construction sectors in Africa.

Companies Covered in Oil Line Corrosion Inhibitors Market

- Schlumberger

- Baker Hughes

- Halliburton

- BASF SE

- Ecolab Inc.

- Dow Inc.

- Nalco Champion

- SUEZ Water Technologies & Solutions

- Henkel AG & Co. KGaA

- Cortec Corporation

- Clariant AG

- Lubrizol Corporation

- Lonza Group

- Solvay S.A.

- Innospec Inc.

Frequently Asked Questions

The global oil line corrosion inhibitors market is projected to reach US$ 2.2 billion in 2026.

Extensive oil and gas production operations, aging pipeline infrastructure, and stringent safety and environmental regulations that demand robust pipeline integrity and leak prevention are driving the market.

The market is poised to witness a CAGR of 7.1% from 2026 to 2033.

Key market opportunities include the development of eco-friendly adoption of smart monitoring and nanotechnology-based solutions, and deployment in expanding offshore, unconventional, and new pipeline infrastructure projects.

Schlumberger, Baker Hughes, Halliburton, BASF SE and Ecolab are some of the key players in the market.