- Processed Food

- Linseed Oil Market

Linseed Oil Market Size, Share, and Growth Forecast, 2025 - 2032

Linseed Oil Market By Product Type (Raw Linseed Oil, Boiled Linseed Oil), Application (Paints & Varnishes, Food & Nutraceuticals), Nature, and Regional Analysis for 2025 - 2032

Linseed Oil Market Size and Trends Analysis

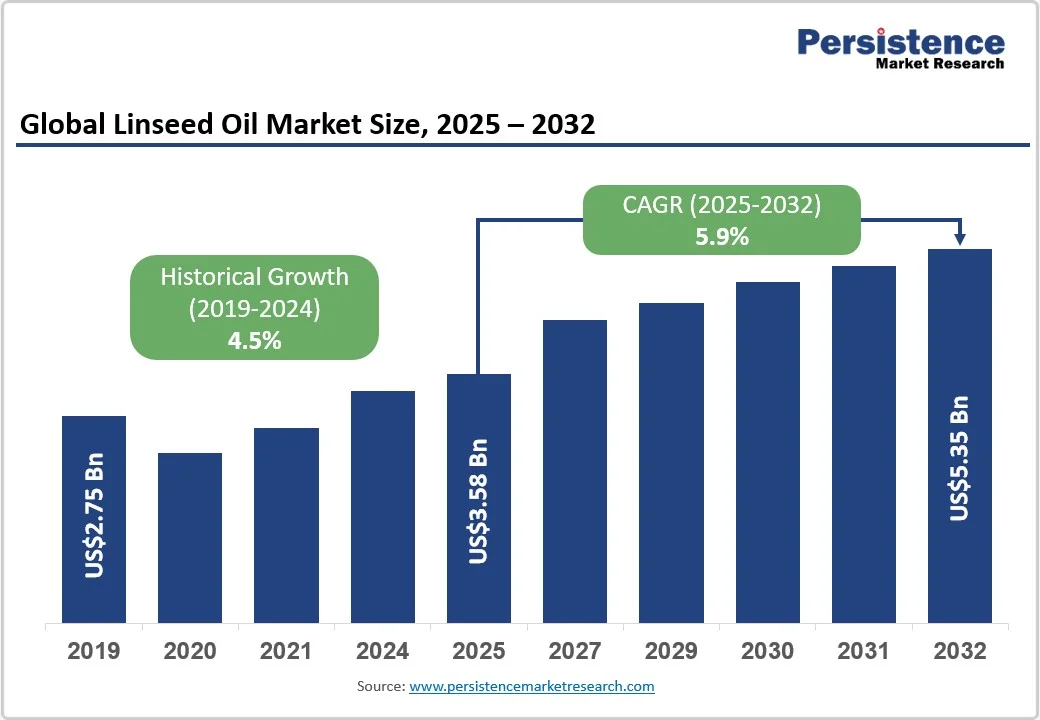

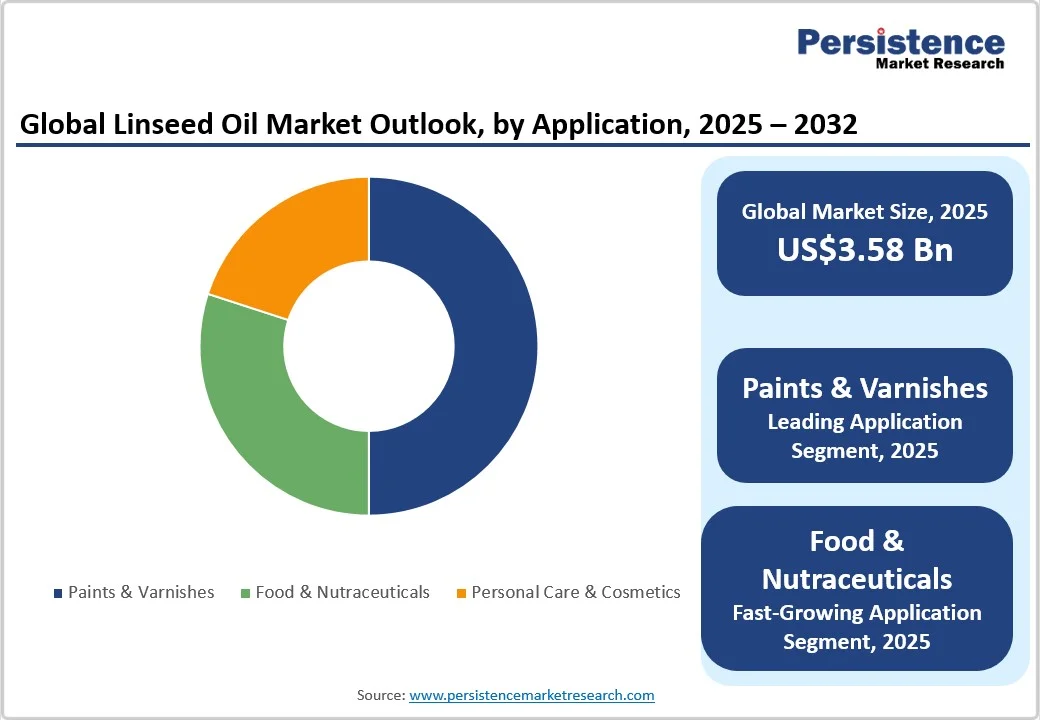

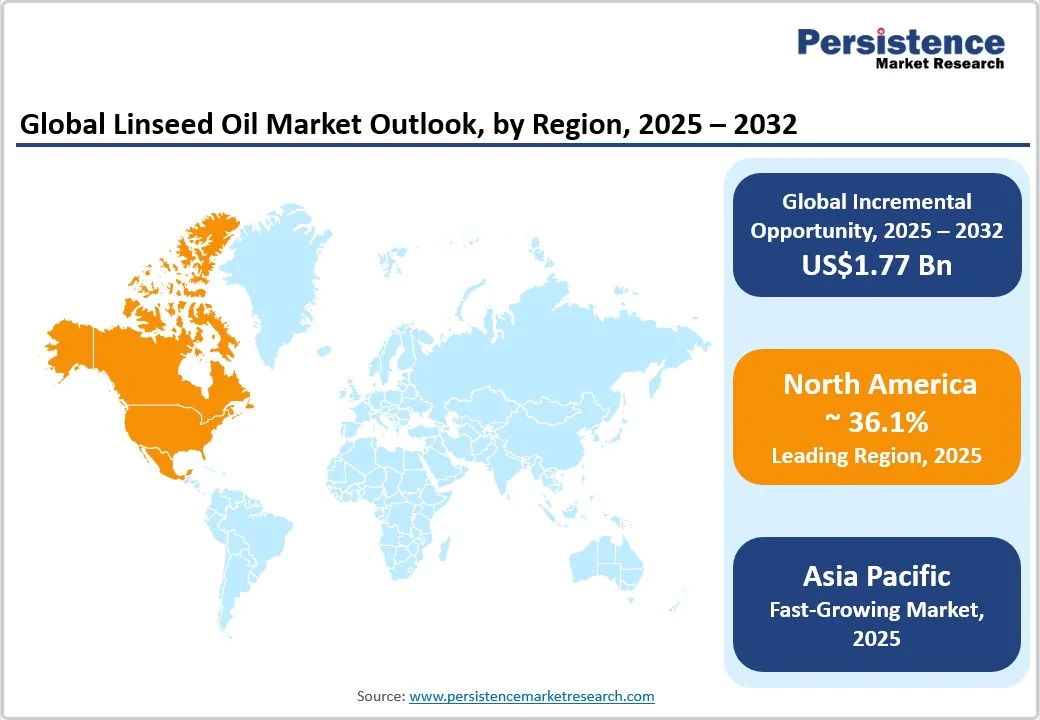

The global linseed oil market size is likely to be valued at US$3.58 Bn in 2025 and is expected to reach US$5.35 Bn by 2032, growing at a CAGR of 5.9% during the forecast period from 2025 to 2032, driven by its wide-ranging applications across paints and varnishes, food and nutraceuticals, and personal care formulations.

Valued for its natural drying properties and high alpha-linolenic acid (ALA) content, linseed oil serves both industrial and health-focused markets, creating a diversified demand base.

Key Industry Highlights:

- Leading Region: North America is likely to account for 36.1% of global share in 2025, supported by strong industrial coatings demand and the world’s largest nutraceutical sector.

- Fastest-growing Region: Asia Pacific, projected to expand at a CAGR of 8.5% between 2025 and 2032, driven by China, India, and ASEAN markets.

- Dominant Product Type: Raw linseed oil, contributing over 41.2% of total sales in 2025, supported by widespread industrial applications in paints, varnishes, and wood finishing.

- Leading Application: Paints & varnishes, accounting for nearly 49.8% of market demand in 2025, as linseed oil remains a preferred natural drying binder in coatings.

| Key Insights | Details |

|---|---|

| Linseed Oil Market Size (2025E) | US$3.58 Bn |

| Market Value Forecast (2032F) | US$5.35 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Market Growth Driven by Sustainable Applications and Health Trends

The commercial growth of the linseed oil market is closely linked to the demand for bio-based drying oils in paints and coatings. Higher regulatory pressure on volatile organic compounds (VOCs) and procurement preference for sustainable binders raise demand for natural drying oils.

The conversion of legacy oil-based formulations to linseed-enhanced formulations can increase unit value by 5-12%, prompting manufacturers to secure multi-year supply contracts and invest in capacity expansion.

Health-driven demand for flax (linseed) oil as a plant source of ALA (alpha-linolenic acid) has increased its use in dietary supplements and fortified foods. Producers report stronger retail and Direct-to-Consumer (DTC) channels for cold-pressed/organic linseed oil. Food-grade and organic product segments command a price premium, shifting mix toward higher-margin SKUs and encouraging processors to separate food vs. industrial streams.

Manufacturers of biolubricants, adhesives, and specialty polymers increasingly source vegetable oils as feedstock. This expands the total addressable market for linseed derivatives beyond traditional paints and food, creating mid-single digit price growth and new B2B contracts for refined and polymerized linseed oil grades.

Barrier Analysis - Feedstock volatility, Competitive pressure from synthetic substitutes, and scale economics

Linseed (flax) production is concentrated in a few key regions, making the supply chain vulnerable to weather-related yield changes and shifts in global oilseed prices. These factors can lead to significant fluctuations in input costs. When flaxseed prices spike, processing margins are squeezed, often prompting manufacturers, particularly in price-sensitive segments such as low-cost paints, to switch to more affordable synthetic resins.

Historical data show that flaxseed prices can swing 15-35% within a single year during periods of extreme weather. To manage this volatility, companies typically rely on multi-sourcing strategies and forward purchasing contracts.

In high-volume, low-margin applications such as commodity paints and certain industrial oils, petroleum-based resins and synthetic binders continue to dominate due to their cost efficiency and consistent performance. As a result, linseed oil's market penetration is limited in these segments. In conservative estimates, such substitution could reduce linseed oil’s addressable market volume by up to 20%.

Opportunity Analysis - Organic and Value-Added Linseed Oil Markets

Organic and cold-pressed linseed products are the fastest-growing sub-segment. Revenue from organic linseed oil is projected to grow at a faster rate than the overall market, fueled by increasing consumer health awareness and a shift towards premium products. Companies investing in segregated processing lines and certification (EU Organic, USDA Organic) can capture higher margins by supplying nutraceuticals, functional foods, and direct-to-consumer channels.

Polymerized and modified linseed oils (stand oil, double-boiled grades) command higher prices and open doors to adhesives, specialty coatings, and biodegradable lubricants. Investment in fractionation and R&D yields outsized margin improvement.

After oil extraction, linseed meal (the byproduct) is typically used in low-value animal feed. The growing demand for plant-based proteins and dietary fiber presents significant opportunities to upcycle this byproduct into high-value ingredients for human nutrition.

With proper processing, defatted linseed meal can be used in protein powders, fiber-rich supplements, and functional food formulations. Investments in food-grade processing facilities and partnerships with plant-based food brands can unlock new revenue streams. This could improve overall profitability and support zero-waste and sustainability positioning, further enhancing appeal in health-conscious and eco-aware consumer segments.

Category-wise Analysis

Product Type Insights

Raw linseed oil accounts for a 41.2% share, supported by its broad application base in paints, varnishes, wood finishing, and putty formulations. It is favored for being a cost-effective, naturally-derived drying oil that provides strong penetration and protection to wooden surfaces.

Industrial manufacturers also use raw linseed oil in sealants, mastics, and printing inks. In 2025, this segment represented well over 41.2% of global sales by value, reflecting its dominant role in industrial and construction applications. The wide availability of flaxseed feedstock, along with relatively simple processing, further reinforces its market leadership.

Double-boiled and polymerized linseed oils are experiencing the fastest growth, with forecast CAGR exceeding the overall market. These modified oils improve drying time, durability, and film strength, making them indispensable in specialty coatings, adhesive formulations, and industrial finishing products. Demand is reinforced by their use in high-performance architectural coatings and wood treatments that require resilience in varying climatic conditions.

Manufacturers highlight polymerized oils as a value-added product stream that captures higher margins. Investments in advanced refining and polymerization technologies, especially in Europe and Asia Pacific, are accelerating supply growth, positioning this segment as a key revenue driver by 2032.

Application Insights

Paints and varnishes continue to dominate the linseed oil market, holding a share of 49.8% in 2025. The oil’s natural drying properties and ability to create a durable, water-resistant film make it highly sought after in both decorative and industrial coatings.

The segment benefits from regulatory trends encouraging the use of bio-based binders to replace petrochemical resins, especially in environmentally conscious regions such as Europe and North America. Restoration projects, premium woodworking, and niche protective coatings also ensure steady demand. In monetary terms, paints and varnishes collectively contribute nearly half of all linseed oil consumption worldwide.

The food and nutraceuticals segment is the fastest-growing, with double-digit demand growth in several developed markets. Cold-pressed linseed oil is rich in alpha-linolenic acid (ALA), making it a plant-based omega-3 source that appeals to health-conscious consumers seeking vegetarian alternatives to fish oil.

Its adoption in dietary supplements, functional foods, and fortified products has accelerated due to rising awareness of cardiovascular and cognitive health benefits. North America and Europe lead uptake, while the Asia Pacific is witnessing the rapid entry of supplement brands targeting urban consumers. Organic certification and premium packaging enhance retail margins, amplifying the growth momentum of this application.

Nature Insights

Conventional linseed oil dominates the market with a share of 71%, with its widespread use in industrial applications such as coatings, adhesives, printing inks, and flooring products. Bulk procurement by manufacturers keeps this segment cost-competitive, as certification is generally not a requirement in these applications.

Producers in North America, China, and India supply large-scale conventional oils that feed into established industrial supply chains. The relative affordability, higher yields per hectare, and compatibility with large-volume processing ensure that conventional linseed oil maintains the largest revenue share globally, especially across construction and manufacturing-linked markets.

Organic linseed oil, particularly cold-pressed variants, represents the fastest-growing nature-based category. Consumers increasingly value traceable, chemical-free production methods, especially for oils intended for food, nutraceuticals, and personal care. Premium positioning allows producers to charge 30-50% higher prices than conventional products, creating attractive margins.

Retail sales in health stores and e-commerce platforms reinforce the trend. While absolute volume remains smaller than conventional supply, growth rates are projected to outpace the broader market significantly through 2032, driven by consumer health awareness, stricter organic certification standards, and government-led promotion of sustainable agriculture.

Regional Market Insights

North America Linseed Oil Market Trends - Industrial use and health demand boosted by VOC and labeling rules

North America represents the largest regional market for linseed oil, accounting for a share of 36.1% in 2025. The U.S. is the primary demand center, with high consumption across paints, coatings, and industrial finishes, supported by steady construction activity and renovation projects. The nutraceutical industry, which is the largest worldwide, further boosts demand for cold-pressed and organic linseed oil due to its omega-3 content.

Canada contributes as a flaxseed producer and an emerging market for organic oil exports. Regulatory factors play a critical role: U.S. VOC emission limits encourage coatings manufacturers to incorporate natural binders, while supplement labeling rules create a favorable environment for health-positioned oils.

The market structure is led by major agribusinesses such as ADM and Cargill, which supply industrial and food-grade oils, complemented by regional niche firms serving organic and specialty segments. Current investment trends emphasize regenerative agriculture, traceable sourcing, and segregated processing lines for food-grade applications.

The combination of a strong industrial base, high consumer spending on health, and policy-driven sustainability incentives makes North America the most stable and mature linseed oil market globally.

Asia Pacific Linseed Oil Market Trends - Industrialization and Functional Foods Backed by Bio-based Policies

Asia Pacific is the fastest-growing region for linseed oil, with China leading both demand and processing capacity. The region benefits from rapid industrialization, booming consumer spending on health and nutrition, and government support for oilseed cultivation.

China is the largest consumer within the region, applying linseed oil in industrial coatings, flooring products, and increasingly in functional foods. India shows strong momentum in nutraceuticals, personal care, and Ayurveda-linked formulations using cold-pressed linseed oil. ASEAN countries, particularly Indonesia, Thailand, and Vietnam, represent emerging demand centers driven by middle-class expansion and rising awareness of plant-based nutrition.

Policy initiatives encouraging bio-based materials and domestic value addition further stimulate market opportunities. The region’s growth is also supported by rising e-commerce penetration, which boosts direct-to-consumer sales of organic oils in urban markets.

Europe Linseed Oil Market Trends - Coatings and Organic Oil Growth Under the Green Deal and REACH

Europe is also exhibiting high growth in the linseed oil market, particularly in high-quality coatings, nutraceuticals, and certified organic segments. Germany, France, and the Benelux countries dominate industrial demand due to their strong paints, chemicals, and construction industries. The U.K. and Spain have growing consumer markets, with rising interest in organic supplements and natural personal care products.

Regulatory frameworks under the European Green Deal, eco-label certifications, and REACH chemical safety compliance create structural incentives for bio-based ingredients such as linseed oil. Specialty European processors such as Henry Lamotte Oils and Gustav Heess maintain a strong competitive edge in refined, food-grade, and certified organic oils, supplying both local and export markets.

Investments in Europe focus on cold-pressing facilities, advanced refining, and cross-border supply partnerships to ensure traceability and compliance with strict certification schemes. Moreover, regional consumer preference for plant-based omega-3 supplements provides consistent demand growth for health-oriented oils.

While Europe’s overall consumption volume is smaller than that of Asia, its higher value per unit, stringent sustainability requirements, and established premium product demand make it a critical hub for strategic expansion in linseed oil markets.

Competitive Landscape

The global linseed oil market is characterized by a dual structure. Top-tier agribusinesses such as Cargill, ADM, and Wilmar International dominate large-volume industrial supply chains, ensuring stable access to paints, coatings, and adhesives manufacturers.

In contrast, high-value food and nutraceutical oils are led by European specialists such as Henry Lamotte Oils and Gustav Heess, which emphasize certified organic and cold-pressed variants. While the industrial-grade market is relatively consolidated, the organic and retail-focused segment remains fragmented, with numerous regional players competing on niche positioning and certification-driven price premiums.

Market leaders emphasize product premiumization, vertical integration, and sustainability certification to capture higher margins. Agribusiness majors leverage scale for cost efficiency, while European specialists differentiate through organic, cold-pressed, and specialty polymerized oils. Partnerships with coatings and nutraceutical formulators are increasingly common, embedding linseed oil derivatives into value-added, bio-based applications.

Key Industry Developments:

- In May 2024, Cargill announced investments in regenerative flaxseed agriculture across Canada, aiming to enhance traceable supply chains for food-grade linseed oil. The initiative strengthened sustainability positioning and aligns with the growing demand for certified oils.

- In March 2024, ADM entered a strategic partnership with a U.S.-based coatings manufacturer to co-develop bio-based binders using polymerized linseed oil. The collaboration underscores the growing industrial interest in sustainable alternatives to petrochemical resins.

Companies Covered in Linseed Oil Market

- Cargill, Incorporated

- Archer Daniels Midland Company (ADM)

- Wilmar International Ltd.

- Henry Lamotte Oils GmbH

- Gustav Heess GmbH

- AOS Products Pvt. Ltd.

- Krishi Oils Ltd.

- Spectrum Chemical Mfg. Corp.

- Palace Chemicals Ltd.

- ConnOils LLC

- Sunnyside Corporation

- ECO Overseas / A.G. Industries

- Jamieson Natural Sources

- Vandeputte Group

- Louis Dreyfus Company

- Bunge Limited

- Fieldstone Oils Pvt. Ltd.

- Royal Green Oils

- Van Drunen Farms

- Solvent Extractors Ltd.

Frequently Asked Questions

The linseed oil market size in 2025 is estimated at US$3.58 Bn.

By 2032, the market is projected to reach US$5.35 Bn, growing at a CAGR of 5.9% between 2025 and 2032.

Key trends include the shift toward bio-based coatings and adhesives, increasing demand for organic and cold-pressed linseed oil in nutraceuticals, and investments in regenerative agriculture and sustainable sourcing.

By product type, raw linseed oil leads due to strong demand in paints and varnishes, accounting for the largest share of factory-gate sales. By application, paints & varnishes remain the dominant application segment, contributing the highest revenue share in 2025.

The market is projected to grow at a CAGR of 5.9% from 2025 to 2032.

Some of the leading companies include Cargill, Incorporated, Archer Daniels Midland Company (ADM), Wilmar International, Henry Lamotte Oils GmbH, and Gustav Heess GmbH.