- Oil & Gas

- Oil and Gas Market

Oil and Gas Market Size, Share, and Growth Forecast, 2025 - 2032

Oil and Gas Market By Value Chain (Upstream, Midstream, Downstream), Service (Workover & Completion, Production, Drilling, Subsea, Seismic, Processing & Separation, Others), Application (Residential, Commercial, Industrial, Others), and Regional Analysis for 2025 - 2032

Oil and Gas Market Share and Trends Analysis

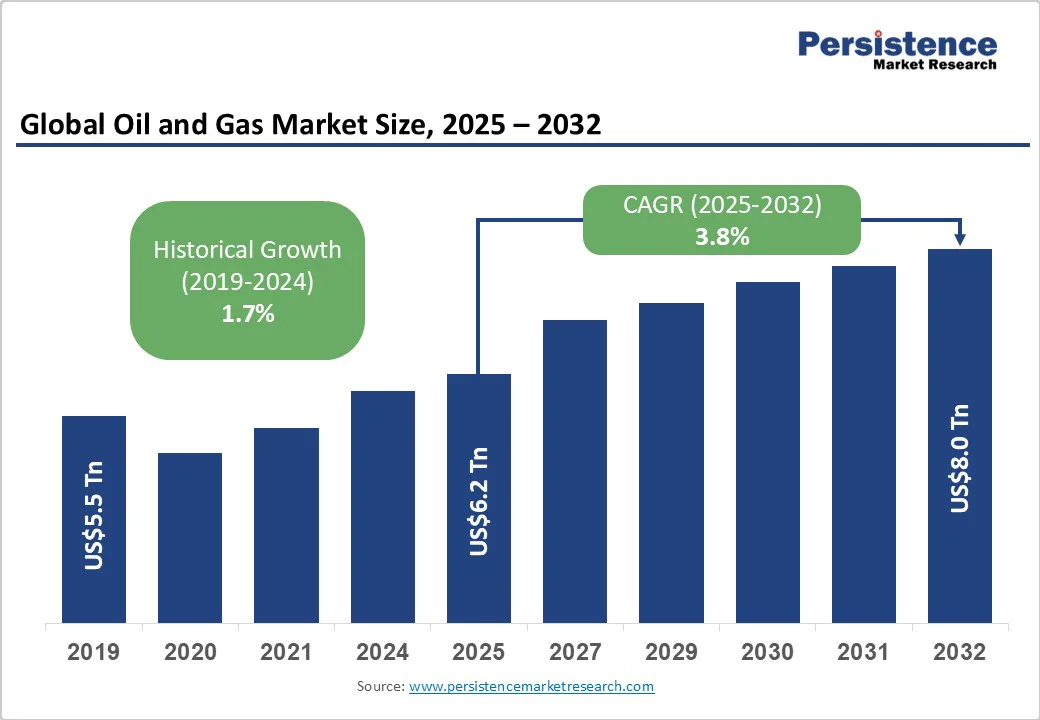

The global oil and gas market size is likely to be valued at US$6.2 Trillion in 2025, and is estimated to reach US$8.0 Trillion by 2032, growing at a CAGR of 3.8% during the forecast period 2025-2032, driven by the soaring energy demand in emerging economies and robust upstream investments in unconventional resources.

The market’s rapid growth is spurred by increased LNG infrastructure investments, expanded refining capacity in Asia Pacific and the Middle East, and enhanced upstream output via digital oilfield analytics and carbon-capture technologies.

Key Industry Highlights

- Leading & Fastest-growing Value Chain Segments: Upstream is set to maintain a dominant 48% share in 2025, while midstream is predicted to be the fastest-growing segment through 2032.

- Leading & Fastest-growing Application Segments: Industrial end-users are likely to represent around 35% of application revenues in 2025, whereas the demand for oil and gas from the residential sector is slated to witness the fastest growth from 2025 to 2032.

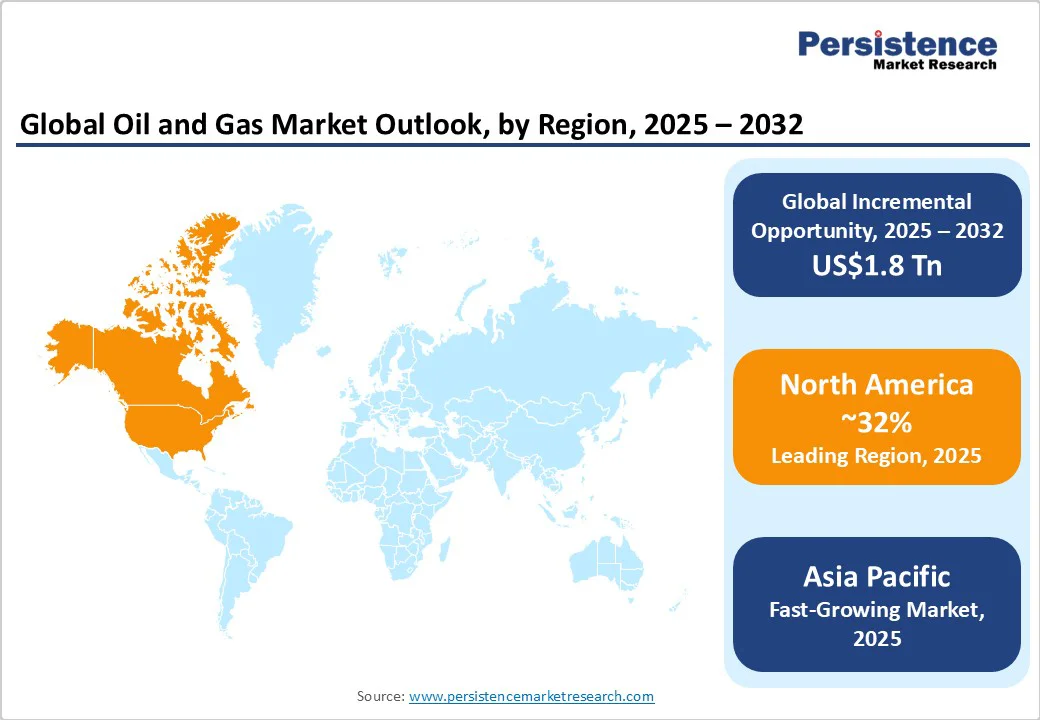

- Dominant Region & Fastest-growing Regional Market: North America is anticipated to hold approximately 32% of the market revenue in 2025, with Asia Pacific exhibiting the fastest growth during 2025-2032.

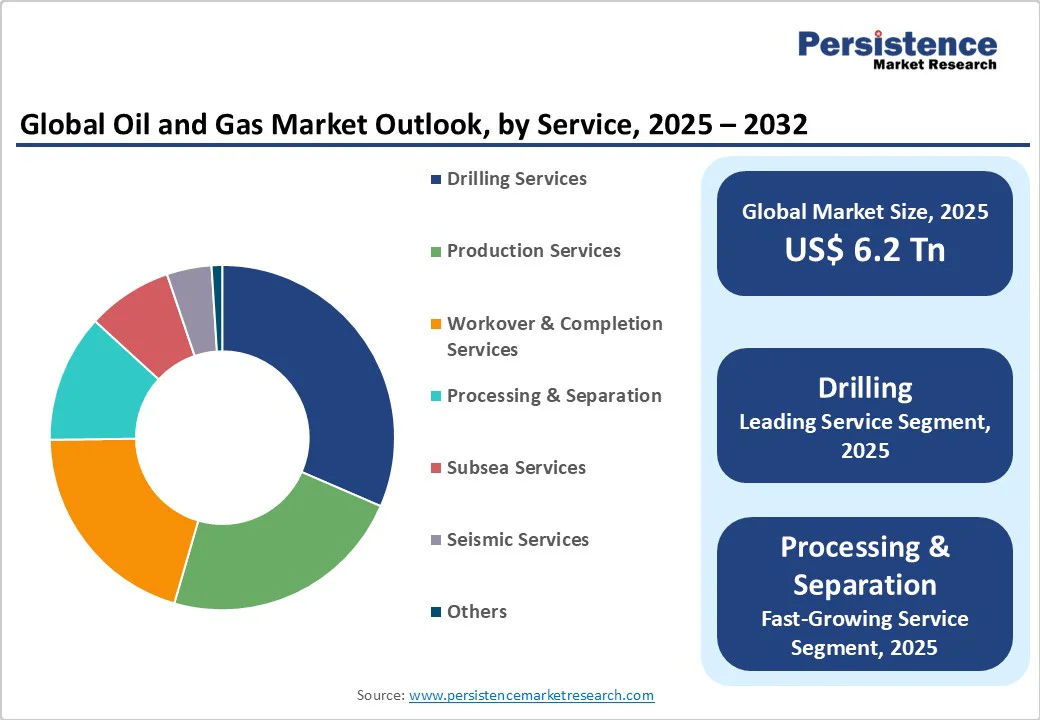

- Dominant & Fastest-growing Services: Drilling services are poised to lead with a 29% share, and processing & separation services are expected to grow at a high CAGR through 2032.

- July 2025: PetroChina invested US$9.6 Billion to transform its Dalian refinery into an integrated refining and petrochemical complex, boosting crude processing capacity from 410,000 to 600,000 barrels of oil per day (bopd) and tripling petrochemical output to 3.8 million tons annually by 2030.

| Key Insights | Details |

|---|---|

|

Oil and Gas Market Size (2025E) |

US$6.2 Tn |

|

Market Value Forecast (2032F) |

US$8.0 Tn |

|

Projected Growth (CAGR 2025 to 2032) |

3.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

1.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - LNG Infrastructure Build-out to Brighten Market Prospects

LNG infrastructure is attracting unprecedented capital allocation, with global export capacity slated to rise from 467 mtpa in 2024 to 620 mtpa by 2030, according to the International Energy Agency (IEA). This expansion is fueled by Europe’s post-Ukraine pivot away from Russian pipeline gas and Asia’s pursuit of cleaner fuels, bolstered by upstream drilling in North America and Australia. The midstream sector is responding with new floating storage regasification units and coastal LNG terminals in Pakistan and East Africa, each representing investments surpassing US$1 Billion by 2027, as per the World LNG Report. For oil and gas operators, this translates into actionable opportunities in EPC contracting and long-term offtake contracts, with average EBITDA margins for terminal operators forecast at 22% by 2028.

Digital Oilfield Adoption to Chart New Growth Trajectories

Digital transformation is revolutionizing reservoir management and production optimization, with global digital oilfield spending surpassing US$15 Billion in 2024 and forecast to accelerate at a 12% CAGR through 2030, as estimated by the Society of Petroleum Engineers. Key enablers in the form of AI-driven predictive maintenance and cloud-based production surveillance are slashing downtime considerably and reducing operating expenses by up to US$2 per barrel of oil equivalent. Regulatory encouragement of methane-emission monitoring is further propelling digital sensor deployments on offshore platforms, spurred by initiatives such as the U.S. EPA Methane Challenge. Companies prioritizing digital integration are seeing 10%–15% uplift in recovery factors, unlocking high-ROI pockets in mature fields.

Barrier Analysis - Upstream Capital Intensity to Constrain Market Growth

Exploration and production (E&P) operations require outsized capital, with average break-even costs for new deepwater projects being significantly high. Volatile Brent prices oscillating between US$60 and US$80 have narrowed margin buffers, making the sanctioning of new projects risky. Credit constraints are intensifying, with the global E&P capex dropping 6% year-on-year in 2024, shrinking financing pools for smaller independents, as highlighted in the IEA Financial Statement Report. Risk quantification indicates a spike in the probability of project delays or cancellations when WTI dips below US$65 for two consecutive quarters, directly suppressing 2025–2032 production CAGR by a notable margin.

Regulatory Compliance Costs to Deter Investments

Stringent emissions regulations in the U.S., European Union (EU), and Canada have imposed sizeable incremental costs, and these are rising by 4% annually due to tougher methane standards set by the U.S. EPA and the European Environment Agency. Non-compliance penalties have escalated litigation risks. Operators are earmarking 8% of annual capex to environmental remediation and monitoring, diverting funds from core E&P activity. Risk-adjusted net present value (NPV) has declined by 7% for high-carbon assets, constraining project returns and deterring brownfield expansions under current regulatory trajectories.

Opportunity Analysis - Carbon Capture and Storage (CCS) Integration to Present Novel Opportunities

CCS spending is set to surge from US$2 Billion in 2024 to US$12 Billion by 2030, at a 36% CAGR, according to the Global CCS Institute. With over 40 MMtpa of CO? capture capacity in development, oil and gas operators can monetize CO?-EOR (enhanced oil recovery) fields that unlock incremental reserves of 10%–15% per project. Early movers stand to generate additional US$1.5 - US$2 per barrel through blended hydrocarbon-CO? streams, while securing low-carbon product premiums in European and Asian markets. Strategic partnerships with engineering, procurement, & construction (EPC) contractors and specialized service firms can accelerate modular CCS deployment, with internal rate of returns (IRRs) estimated at 12% under the current EU Allowances (EUA) of €50/ton.

Floating LNG (FLNG) Projects to Expand Market Scope

FLNG projects are unlocking stranded gas assets offshore West Africa and the Eastern Mediterranean, with four projects expected online by 2028, adding 25 mtpa capacity, according to some industry estimates. FLNG capital outlays average US$1.6 Billion for a 2 mtpa train, yielding project-level free cash flows of US$200 Million annually. These assets bypass costly pipeline builds and tap near-field markets, enhancing project economics with payback periods under five years. Investors can achieve up to 14% project IRRs by negotiating tolling agreements and securing more than 80% long-term utilization rates.

Category-wise Analysis

Value Chain Insights

The upstream segment is expected to command nearly half of the revenue share at an estimated 48% in 2025, reflecting sustained investment in unconventional shale plays and deepwater exploration. Leading operators are leveraging advanced drilling techniques and digital reservoir modeling to optimize recovery and reduce unit costs below US$25 per barrel of oil equivalent (boe). Production volumes in key basins such as the Permian and Santos are driving upstream revenues, while national oil companies in the Middle East are scaling unconventional gas output to diversify export profiles.

Midstream is set to register the fastest growth during 2025-2032, underpinned by LNG liquefaction projects in Australia and pipeline expansions in Central Asia. Gas pipeline throughput is projected to increase by nearly a third by 2032, with new interconnectors linking Central Asian gas fields to the European grid. The convergence of hydrogen blending mandates and cross-border energy trade agreements is creating additional demand for compressor stations and metering infrastructure. As midstream operators are securing long-term tolling contracts, EPC firms focused on modular design and digital SCADA integration are capturing premium margins.

Application Insights

Among applications, the industrial end-use sector is slated to retain leadership with about 35% of the total consumption in 2025. Petrochemical complexes in China, South Korea, and the U.S. Gulf Coast are generating robust feedstock demand, translating to stable offtake contracts for refineries and gas processing units. Industrial natural gas consumption is projected to grow by 2.5% annually through 2032, driven by ammonia and methanol production ramps required for clean energy vectors.

The residential segment is emerging as the fastest-growing end-user. Government subsidies for household gas connections in Southeast Asia and Eastern Europe are accelerating residential network expansions. By 2032, piped gas coverage in India is expected to double to 50% of urban households, fueling new opportunities in last-mile distribution and smart-meter deployments. Appliance manufacturers and local utilities are collaborating on modular, pre-fabricated network solutions to accelerate rollout and guarantee service reliability.

Service Insights

Drilling services are predicted to lead the oilfield services market with an estimated 29% share in 2025, supported by elevated rig counts in North America and Brazil. Enhanced drilling automation and real-time logging-while-drilling tools are enabling average drilling efficiency gains of 18%, which are translating into shorter well-cycle times and lower per-foot costs. Service providers offering integrated drilling-geosteering packages are securing multi-year contracts with supermajors and independents alike.

Processing & separation services are forecast to expand at a high CAGR from 2025 to 2032, making it the fastest-growing service segment. Aging refinery and gas-processing assets are being retrofitted with modular separation skids and membrane technologies to improve product yields and meet tighter environmental standards. Demand for turnkey EPC solutions is rising by 22% annually as operators seek to balance sustainability compliance with throughput optimization. Service firms that are bundling digital performance monitoring with aftermarket maintenance are capturing higher recurring revenue streams.

Regional Insights

North America Oil and Gas Market Trends

North America is likely to maintain approximately 32% of the market share in 2025, powered by U.S. shale output reaching 13 MMbpd and Canadian Oil Sands production stabilizing near 2 MMbpd. The regional market is forecast to achieve a high CAGR through 2032 as Permian expansions and Gulf Coast LNG exports ramp up. The U.S. regulatory environment is enabling faster offshore lease awards and incentivizing carbon storage hubs under Section 45Q tax credits, which have attracted US$20 Billion in investments through 2026.

Technological innovation is flourishing, with operators piloting unmanned well pads and digital midstream platforms to reduce OPEX by up to 12%. Competitive dynamics remain concentrated, with oil & gas industry behemoths and leading independents controlling 65% of regional production, while mid-tier service companies are capitalizing on niche automation and environmental monitoring contracts. Infrastructure investment is increasingly targeting hydrogen blending trials in Texas and advanced pipeline integrity management systems, positioning North America as a testbed for next-generation energy transition projects.

Europe Oil and Gas Market Trends

Europe is slated to account for about 18% of the market share in 2025, with Germany, the U.K., France, and Spain leading the charge, driven by hydrogen repurposing of North Sea pipelines and Mediterranean floating storage solutions. The EU’s Fit for 55 regulatory package is mandating methane emission cuts of 65% by 2030, triggering retrofit investments in existing refineries and compressing investor IRRs by an estimated 1.2 percentage points.

The competitive landscape is moderately consolidated, with integrated majors controlling 55% of the market share, while specialized service clusters in Norway and the Netherlands are securing decarbonization contracts and strengthening their regional and global presence. Investment trends include offshore wind-oil hybrid development and cross-border CO?-EOR pilot collaborations, which are unlocking co-investment opportunities across energy and climate portfolios.

Asia Pacific Oil and Gas Market Trends

Asia Pacific is anticipated to capture an estimated market revenue share of 28% in 2025, with China, Japan, and India serving as primary growth engines. The regional market is projected to expand at the highest CAGR through 2032, propelled by India’s downstream refinery capacity additions and Southeast Asia’s LNG import terminal build-out. Cost advantages in EPC execution and lower labor rates are forecast to attract billions in new petrochemical complexes across Malaysia and Vietnam by 2028.

Regulatory incentives in Singapore and Australia are underpinning carbon capture hubs and digital midstream initiatives, with government grants covering up to 30% of initial capex. The competitive landscape features state-owned enterprises partnering with global service providers to transfer technology and co-finance large-scale infrastructure. Investment flows are also targeting hydrogen blending pilots in South Korea and port-based FLNG anchorage solutions, highlighting the role of Asia Pacific as both consumer and innovator in the evolving energy mix.

Competitive Landscape

The global oil and gas market structure is moderately consolidated, with the top five players, Saudi Aramco, ExxonMobil, Shell, BP, and Chevron, capturing nearly two-fifths of revenues. Mid-tier independents and national oil companies fill the next 30%, while a fragmented base of service providers accounts for the remainder. Leading players are leveraging integrated business models and digital ecosystems to sustain margins under price volatility.

Market leaders are pursuing innovation leadership, deploying AI and automation to drive down operating costs. Cost leadership remains central, with standardized modular equipment reducing capex by 8%. Market expansion measures focus on emerging markets in Asia and Africa. Integrated players are testing subscription-based service models for midstream asset operations, blending O&M with digital analytics.

Key Industry Developments

- In September 2025, BP and Total expanded U.S. investments: BP advancing a Louisiana carbon-capture facility sequestering 1.5 million tons CO? annually, and Total investing US$3 Billion to convert Port Arthur refinery to low-carbon fuels, highlighting decarbonization efforts.

- In September 2025, Iran’s Oil Ministry and NIOC acquired 350- and 400-foot offshore drilling rigs under IOOC oversight to accelerate Persian Gulf joint field development, enhance national oil and gas output, and sustain offshore production amid sanction challenges.

- In September 2025, ExxonMobil approved the US$6.8 Billion Hammerhead project on Guyana’s Stabroek block, adding an FPSO producing 150,000?bopd, boosting total block capacity to 1.5?million?bopd, with first oil expected in 2029.

Companies Covered in Oil and Gas Market

- Saudi Arabian Oil Company (Aramco)

- Exxon Mobil Corporation

- Shell plc

- BP p.l.c.

- Chevron Corporation

- TotalEnergies SE

- Abu Dhabi National Oil Company (ADNOC)

- PetroChina Company Limited

- Rosneft Oil Company

- Equinor ASA

- Eni S.p.A.

- ConocoPhillips Company

- Occidental Petroleum Corporation

- Petroliam Nasional Berhad

- Woodside Energy Group Ltd.

Frequently Asked Questions

The global oil and gas market is projected to reach US$6.2 Billion in 2025.

The surging energy demand in emerging economies and robust upstream investments in unconventional resources are driving the market.

The oil and gas market is poised to witness a CAGR of 3.8% from 2025 to 2032.

Stronger capital deployment in liquefied natural gas (LNG) infrastructure and downstream refining capacity expansions, optimized recovery technologies ramping up upstream output, and technology integration in digital oilfield analytics and carbon-capture initiatives are key market opportunities.

Saudi Arabian Oil Company (Aramco), Exxon Mobil Corporation, and Shell plc are some of the key players in the oil and gas market.