- Biotechnology

- Global Ocular Genetic Diagnostics Market

Global Ocular Genetic Diagnostics Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Ocular Genetic Diagnostics Market by Test Type (Single Gene Testing, Panel Testing, Whole Exome Sequencing (WES), and Whole Genome Sequencing (WGS)), by Technology (Sequencing Technology, Polymerase Chain Reaction (PCR), Microarray Technology, and Next-Generation Sequencing (NGS)), by Application (Retinal Disorders, Cataract Diagnosis, Inherited Ocular Disorders, Age-Related Macular Degeneration, and Other) by End User (Hospitals, Diagnostic Laboratories, Academic And Research Institutes, Others), and Regional Analysis from 2026 to 2033

Ocular Genetic Diagnostics Market Size and Trends Analysis

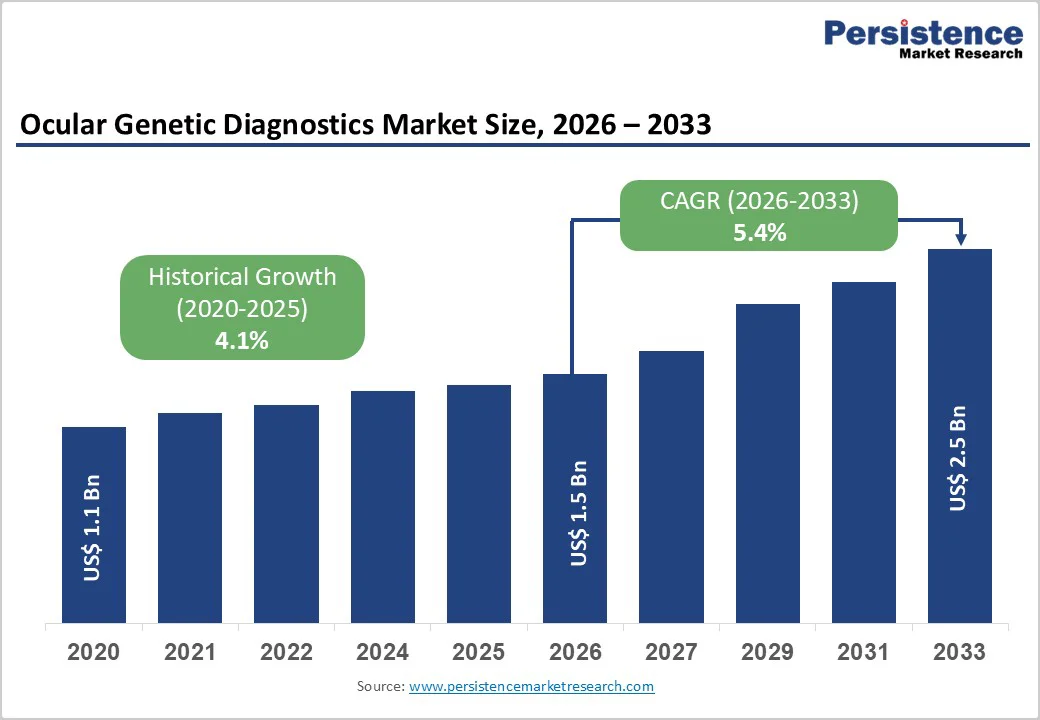

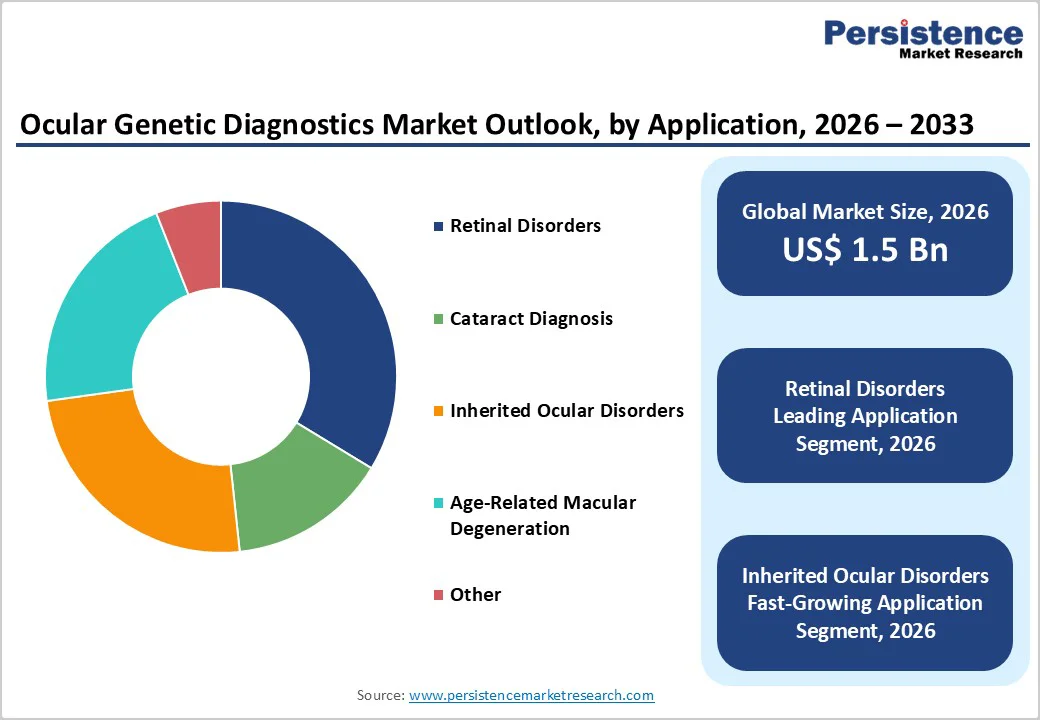

The global ocular genetic diagnostics market size is estimated to grow from US$ 1.5 Bn in 2026 to US$ 2.5 Bn by 2033. The market is projected to record a CAGR of 5.4% during the forecast period from 2026 to 2033.

Global demand for ocular genetic diagnostics is rising steadily, driven by the increasing prevalence of inherited ocular disorders, including inherited retinal diseases (IRDs), congenital cataracts, corneal dystrophies, optic neuropathies, and syndromic eye conditions linked to systemic genetic abnormalities. The growing burden of rare genetic eye diseases, combined with improving survival rates and longer life expectancy among pediatric and adult patients, is increasing long-term diagnostic, prognostic, and monitoring requirements. Expanding newborn and pediatric screening initiatives, improved access to molecular diagnostics, and rising indicate awareness among ophthalmologists and genetic specialists are contributing to sustained testing volumes.

Rapid advances in genomic technologies—particularly next-generation sequencing (NGS), whole-exome sequencing (WES), and whole-genome sequencing (WGS)—are enhancing diagnostic accuracy, reducing turnaround times, and enabling earlier disease detection. Increasing integration of genetic testing into precision ophthalmology workflows, alongside rising healthcare investments in specialized diagnostic laboratories and tertiary eye-care centers, is accelerating global adoption. Concurrently, ongoing research into novel gene–phenotype correlations and disease pathways continues to reinforce long-term market expansion across both developed and emerging regions.

Key Industry Highlights

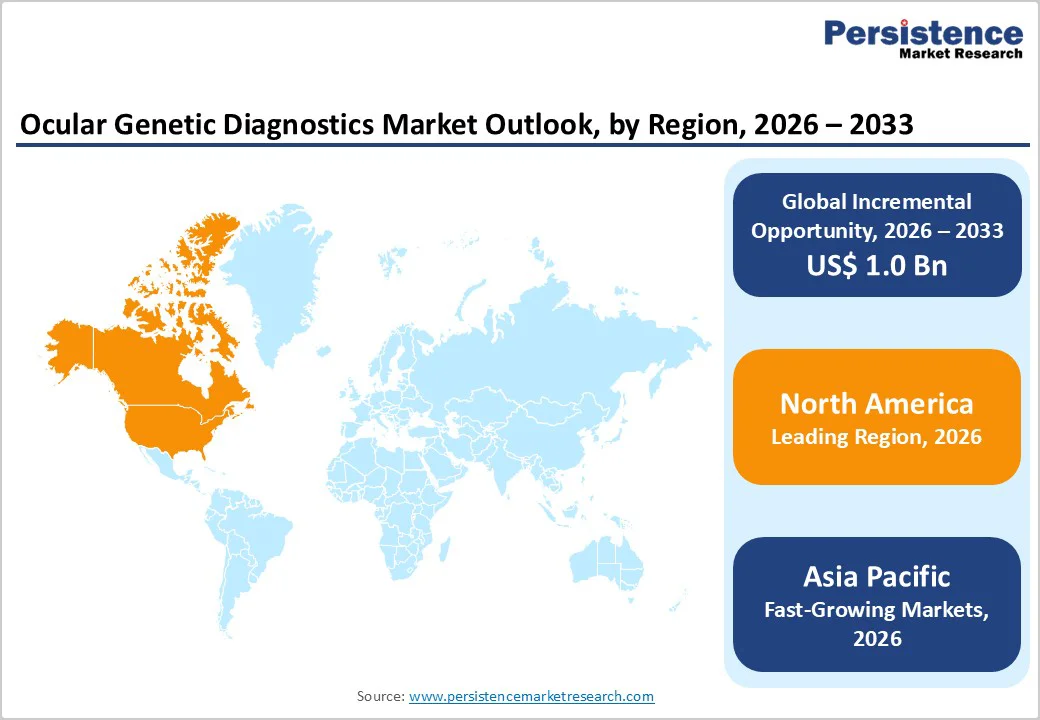

- Leading Region: North America holds the largest market share at 47.7%, supported by advanced molecular diagnostics infrastructure, high testing volumes for inherited ocular disorders, strong reimbursement frameworks, and widespread adoption of precision medicine.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace due to a large patient pool, rising awareness of genetic eye diseases, rapid expansion of diagnostic laboratories, and increasing government support for newborn and rare disease screening.

- Leading Test Type Segment: Panel testing dominates the market owing to its cost-effectiveness, high diagnostic yield, and suitability for detecting multiple ocular disease–associated genes simultaneously.

- Fastest-Growing Test Type Segment: Whole genome sequencing (WGS) is witnessing rapid growth as its clinical utility expands for complex, undiagnosed, and ultra-rare ocular genetic conditions.

- Leading Application Segment: Retinal disorders represent the largest application segment due to high utilization in symptomatic patients and confirmatory testing following abnormal clinical or imaging findings.

- Fastest-Growing Application Segment: Inherited ocular disorders are expanding rapidly as early diagnosis initiatives, genetic counseling, and public health mandates gain momentum globally.

| Global Market Attributes | Key Insights |

|---|---|

| Ocular Genetic Diagnostics Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 2.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver – Rising Prevalence of Inherited Ocular Disorders and Advancements in Genomic Technologies Driving Market Growth

The rising global prevalence of inherited ocular disorders is a primary driver fueling sustained demand for ocular genetic diagnostics. Conditions such as retinitis pigmentosa, Stargardt disease, Leber congenital amaurosis, congenital cataracts, optic atrophies, and syndromic eye diseases are increasingly being diagnosed across both pediatric and adult populations. Improved disease awareness among ophthalmologists, expanded referral networks, and better survival outcomes among affected patients are contributing to a growing diagnosed patient pool. Many inherited ocular conditions present with overlapping phenotypes or nonspecific clinical manifestations, making genetic confirmation essential for accurate diagnosis, prognosis assessment, treatment planning, and family counseling.

Technological advancements are significantly accelerating market growth. Rapid evolution of next-generation sequencing (NGS), whole-exome sequencing (WES), and whole-genome sequencing (WGS) has improved diagnostic yield while reducing turnaround times and per-sample costs. Integration of targeted multi-gene panels into routine ophthalmic diagnostics enables efficient screening of genetically heterogeneous conditions. These advancements support early disease detection, personalized treatment strategies, and eligibility assessment for emerging gene therapies. Collectively, increasing disease burden and continuous innovation in genomic technologies are driving steady and long-term expansion of the global ocular genetic diagnostics market.

Restraints – High Testing Costs and Limited Access to Specialized Genetic Services Limiting Market Adoption

High costs associated with advanced ocular genetic diagnostics remain a key restraint, particularly in low- and middle-income countries. While sequencing costs have declined over time, significant expenses related to laboratory infrastructure, sequencing platforms, bioinformatics pipelines, data storage, and confirmatory testing continue to limit widespread adoption. Comprehensive approaches such as WES and WGS involve additional costs for data interpretation and variant validation, further restricting accessibility. Limited reimbursement coverage for ocular genetic testing in several regions exacerbates financial barriers, reducing patient uptake and delaying diagnosis.

Moreover, limited access to specialized genetic services constrains market penetration. Shortages of trained clinical geneticists, ophthalmic genetic specialists, and genetic counselors hinder effective test utilization and accurate interpretation of results. In many emerging markets, fragmented referral pathways and uneven diagnostic infrastructure lead to delayed or missed diagnoses. Variability in testing standards, reporting practices, and follow-up care further impacts clinician confidence and test adoption. These structural and economic limitations continue to restrain broader market growth despite increasing recognition of the clinical value of ocular genetic diagnostics.

Opportunity – Expansion of Newborn Screening and Precision Ophthalmology Creating New Growth Opportunities

The expansion of newborn and early childhood screening programs represents a significant growth opportunity for the global ocular genetic diagnostics market. Governments and public health agencies are increasingly incorporating genetic testing into screening frameworks to enable early detection of inherited ocular disorders, allowing timely intervention and improved long-term visual outcomes. Advances in high-throughput sequencing, automation, and cost-efficient testing workflows are making large-scale screening programs more feasible, particularly in Asia Pacific, the Middle East, and Latin America. Early diagnosis through screening reduces disease burden and long-term healthcare costs, supporting policy-level adoption.

Furthermore, the growing adoption of precision medicine in ophthalmology is creating new demand across both clinical and research settings. Genetic insights are increasingly guiding personalized treatment strategies, eligibility for gene and cell therapies, and patient stratification for clinical trials. Investments in specialized diagnostic laboratories, integration of genomics into tertiary eye-care centers, and expansion of rare disease research initiatives are strengthening the role of ocular genetic diagnostics. As precision ophthalmology continues to evolve, demand for accurate and comprehensive genetic testing is expected to expand significantly, supporting long-term market growth.

Category-wise Analysis

By Test Type, Panel Testing Leads Owing to Comprehensive Coverage and Cost Efficiency

The panel testing segment is projected to dominate the global ocular genetic diagnostics market in 2026, accounting for a revenue share of 38.4%. Its leadership is primarily driven by the clinical efficiency of targeted gene panels, which enable simultaneous screening of multiple genes associated with inherited ocular disorders such as retinitis pigmentosa, cone–rod dystrophy, congenital cataracts, and optic neuropathies. Panel-based assays offer an optimal balance between diagnostic yield, cost-effectiveness, and turnaround time, making them highly suitable for routine clinical workflows in ophthalmology and pediatric care. Physicians increasingly prefer panel testing as a first-line diagnostic approach due to its ability to provide actionable results without the complexity and cost associated with whole-exome or whole-genome sequencing. Established clinical guidelines, growing physician familiarity, and compatibility with existing NGS platforms further support adoption. Panel testing is also widely utilized in confirmatory diagnostics following abnormal clinical findings or imaging results. While WES and WGS are gaining traction for complex cases, panel testing remains the backbone of ocular genetic diagnostics due to its scalability and clinical practicality.

By Application, Retinal Disorders Emerges as the Dominant Segment Driven by Clinical Necessity

The retinal disorders segment is projected to dominate the global ocular genetic diagnostics market in 2026, accounting for a revenue share of 33.7%. Segment leadership is attributed to the high prevalence and genetic heterogeneity of inherited retinal diseases (IRDs), including retinitis pigmentosa, Stargardt disease, Leber congenital amaurosis, and choroideremia. These conditions often present with overlapping phenotypes, making molecular genetic confirmation essential for accurate diagnosis, prognosis, and disease classification. Genetic testing plays a critical role in determining eligibility for emerging gene therapies and clinical trials, further driving demand in this segment. Increasing referrals from ophthalmologists, retinal specialists, and pediatricians, along with improved access to advanced diagnostic platforms, continue to support growth. Additionally, advances in imaging technologies combined with genetic diagnostics are enabling earlier disease detection and intervention. As research into retinal gene therapies accelerates, demand for precise genetic characterization is expected to remain strong, reinforcing the segment’s dominant position.

By End User, Hospitals Hold the Largest Share Due to High Testing Volumes and Specialized Capabilities

The Hospitals segment is projected to dominate the global ocular genetic diagnostics market in 2026, accounting for a revenue share of 39.8%. Hospitals serve as primary centers for diagnosis and management of inherited ocular disorders, offering integrated care that includes ophthalmology, genetics, pediatrics, and neurology. Availability of advanced diagnostic infrastructure, multidisciplinary expertise, and access to high-throughput sequencing platforms enables hospitals to manage complex genetic cases efficiently. High patient footfall, increasing inpatient and outpatient referrals, and growing adoption of in-house genetic testing services support segment dominance. Hospitals also play a key role in newborn screening follow-up, rare disease diagnosis, and long-term patient monitoring. Furthermore, academic hospitals frequently participate in clinical research and gene therapy trials, driving additional demand for genetic testing. Increasing investment in tertiary care centers and expansion of hospital-based genomics programs continue to strengthen the leadership of this segment.

Region-wise Insights

North America Ocular Genetic Diagnostics Market Trends

The North America ocular genetic diagnostics market is expected to dominate globally with a value share of 47.7% in 2026, led primarily by the United States. The region benefits from a highly advanced healthcare ecosystem characterized by widespread availability of molecular diagnostic technologies and strong integration of genetic testing into routine ophthalmic practice. High awareness of inherited ocular disorders among clinicians, combined with established referral networks and access to genetic counseling services, supports early diagnosis and sustained testing volumes.

Favorable reimbursement policies and strong payer coverage facilitate adoption of both panel-based testing and advanced sequencing approaches such as WES and WGS. North America also has a robust presence of reference laboratories, academic medical centers, and biotechnology companies actively engaged in ocular genetics research. High participation in clinical trials, particularly for gene and cell therapies targeting retinal disorders, further drives demand for precise genetic diagnostics. Regulatory clarity, standardized testing protocols, and continuous investment in precision medicine reinforce the region’s leadership position.

Europe Ocular Genetic Diagnostics Market Trends

The Europe ocular genetic diagnostics market is expected to grow steadily, supported by increasing recognition of inherited eye diseases and strong emphasis on early diagnosis and long-term disease management. Countries including Germany, the United Kingdom, France, Italy, and the Nordic region are key contributors due to well-established public healthcare systems and broad access to genetic testing services. Expansion of national newborn screening initiatives and increased adoption of molecular diagnostics in pediatric ophthalmology are driving consistent demand.

European healthcare frameworks emphasize evidence-based diagnostics, encouraging the use of panel testing and targeted sequencing approaches. Cross-border research collaborations, harmonized regulatory standards, and strong funding for rare disease programs further support market growth. Increasing integration of genomic data into clinical decision-making, along with rising awareness among ophthalmologists and genetic specialists, is strengthening the role of ocular genetic diagnostics across the region. Continued investment in genomics infrastructure and digital health initiatives is expected to sustain long-term expansion.

Asia Pacific Ocular Genetic Diagnostics Market Trends

The Asia Pacific ocular genetic diagnostics market is expected to register the fastest growth, with a CAGR of approximately 8.6% between 2026 and 2033, driven by rapid healthcare infrastructure development and a large undiagnosed patient population. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are experiencing rising diagnosis rates due to improved access to molecular diagnostics and specialized eye care services.

Rapid expansion of diagnostic laboratories, increasing availability of trained geneticists, and rising healthcare expenditure are improving test accessibility across the region. Government-led newborn screening programs and rare disease policies are accelerating adoption, while partnerships with global diagnostic companies are enhancing technology transfer. Growing awareness of inherited ocular disorders, coupled with increasing emphasis on early intervention and precision medicine, is expected to sustain strong growth across Asia Pacific in the coming years.

Market Competitive Landscape

The global ocular genetic diagnostics market is highly competitive, with key players such as Quest Diagnostics, Myriad Genetics, Inc., PerkinElmer, Inc., Natera, Inc., and Centogene N.V. leveraging advanced sequencing technologies, broad test portfolios, and strong global laboratory networks to maintain market presence. These companies focus on expanding ocular disease gene coverage, improving bioinformatics interpretation, and reducing turnaround times to enhance clinical utility and physician adoption.

Competition is further intensified by ongoing investments in research collaborations, participation in gene therapy and rare disease studies, and geographic expansion into emerging markets. Continuous innovation in next-generation sequencing, automation, and data analytics is strengthening differentiation, supporting sustained market growth and long-term evolution.

Key Industry Developments:

- In October 2025, AviadoBio Ltd. and UgeneX Therapeutics announced an exclusive option and license agreement for the development and commercialization of UGX-202, an investigational AAV-based gene therapy currently in clinical development for patients with retinitis pigmentosa (RP). Under the agreement, UGX-202 is also expected to be evaluated in a second undisclosed indication, with clinical entry anticipated by the end of 2025, reflecting continued expansion of gene therapy pipelines targeting inherited retinal disorders.

- In June 2025, Ocugen, Inc. announced that the U.S. FDA cleared an IND amendment to initiate a Phase 2/3 pivotal trial of OCU410ST, a modifier gene therapy for Stargardt disease and other ABCA4-associated retinopathies. The program has received Rare Pediatric Disease and Orphan Drug designations, highlighting its significance in treating inherited retinal disorders.

Frequently Asked Questions

The global ocular genetic diagnostics market is projected to be valued at US$ 1.5 Bn in 2026.

Rapid increase in the prevalence of inherited and age-related eye disorders, technological advancements in genetic testing (NGS, WES/WGS), growing adoption of precision medicine, and rising awareness of early genetic diagnosis.

The global ocular genetic diagnostics market is poised to witness a CAGR of 5.4% between 2026 and 2033.

Expansion of AI-enabled genetic analysis platforms, integration of advanced sequencing technologies, growth in personalized and prenatal ocular genetic screening, and emerging demand in developing regions with improving healthcare infrastructure

Quest Diagnostics, Myriad Genetics, Inc., PerkinElmer, Inc., Natera, Inc., and Centogene N.V. are some of the key players in the ocular genetic diagnostics market.