- Off-Road Equipment & Machinery

- North America Ride-On Power Trowel Market

North America Ride-On Power Trowel Market Size, Share, Trends, Regional, Forecasts 2026 - 2033

North America Ride-On Power Trowel Market by Product Type (Mechanical, Hydrostatic), By Material (Steel Pans, Stainless Steel Pans, Carbon Steel Pans, High Carbon Pans, Others), By Size (6-Foot Class (Twin 36

North America Ride-On Power Trowel Market Analysis

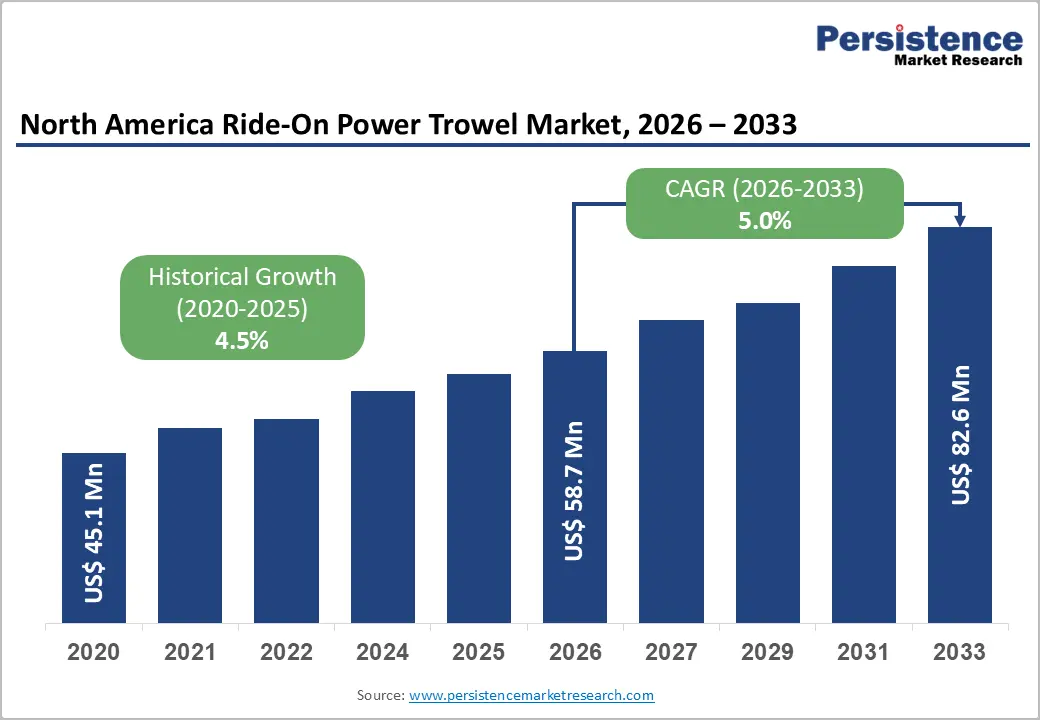

The North America ride-on power trowel market size is likely to be valued at US$58.7 million in 2026 and is projected to reach US$82.6 million by 2033, growing at a CAGR of 5.0% between 2026 and 2033.

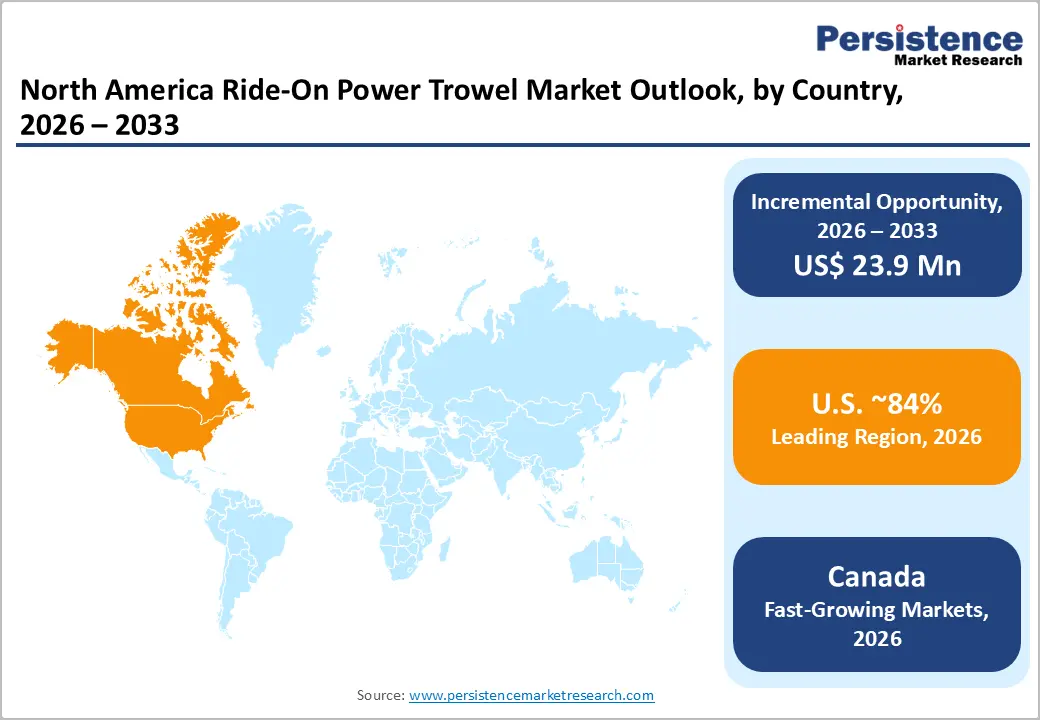

Market expansion is driven by labor shortages pushing contractors toward mechanized finishing, rising demand for polished concrete finishes meeting flooring standards, and expanding commercial and infrastructure projects requiring high surface quality. The United States leads with 84% share, while Canada grows at a 5.3% CAGR, supported by development and infrastructure modernization.

Key Industry Highlights:

- Mechanical trowels hold 68% market share, while hydrostatic systems grow at 5.3% CAGR, driven by premium project adoption and the Multiquip MD105 launch.

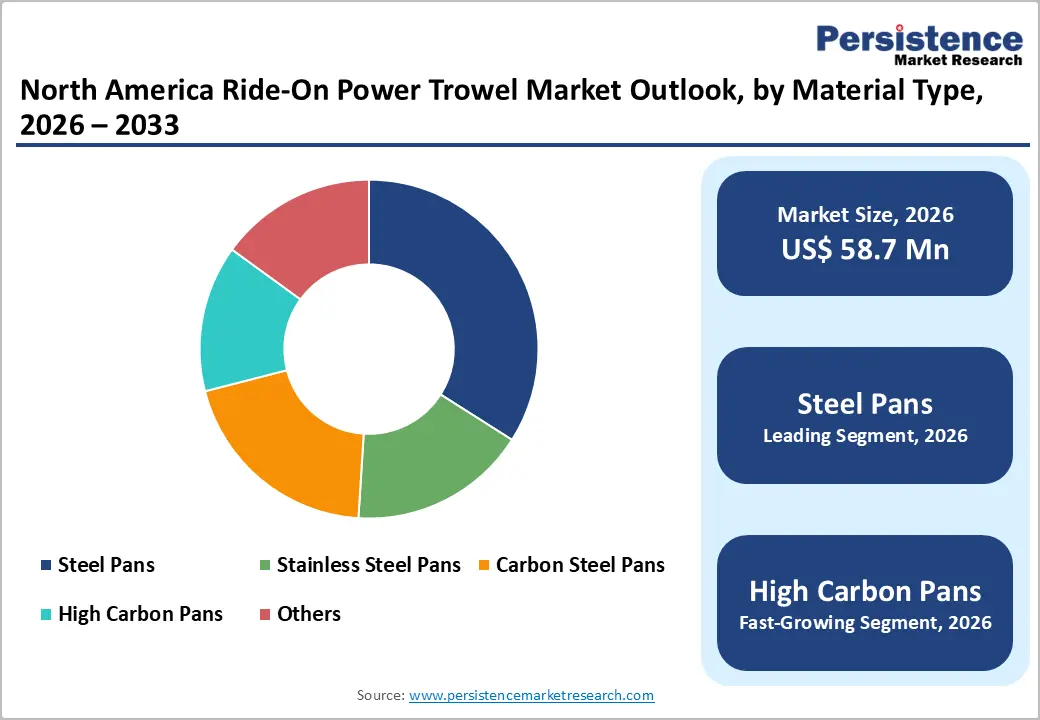

- Steel pans account for ~34% of the market share, while high-carbon steel is growing at a 5.5% CAGR due to durability and lifecycle cost benefits.

- The 8-foot class dominates with ~46% share, while 10-foot-plus units expand at 5.4% CAGR on mega-slab projects.

- The United States leads with a ~84% share, while Canada grows at a 5.3% CAGR in infrastructure and industrial development.

- MD105 innovation, low-emission pilots, and Bartell’s expansion highlight strong competitive and geographic momentum.

| Key Insights | Details |

|---|---|

|

North America Ride-on Power Trowel Market Size (2026E) |

US$ 4.1 Million |

|

Market Value Forecast (2033F) |

US$ 12.4 Million |

|

Projected Growth CAGR (2026-2033) |

17.3% |

|

Historical Market Growth (2020-2025) |

15.9% |

Market Dynamics Analysis

Drivers - Chronic Labor Shortages and Mechanization Necessity in Concrete Finishing Trades

Chronic labor shortages in skilled concrete finishing trades are systematically compelling contractors to adopt mechanized solutions including ride-on power trowels, with single ride-on units capable of replacing three or more manual laborers, significantly improving project economics and addressing workforce availability constraints across North American construction markets. The global concrete finishing equipment market is expanding from USD 2.8 billion in 2025 to USD 3.9 billion by 2032, driven by sustained demand for mechanized solutions to address labor challenges. Single-operator productivity gains with ride-on trowels exceed manual finishing by 200-300% on large slabs exceeding 5,000 square feet. Operator fatigue reduction enables longer operational duration and improved work quality, sustaining competitive advantage. Consistent surface quality, eliminating variation from manual labor, supporting specification compliance and customer satisfaction. Labor cost pressures and worker availability constraints are incentivizing equipment investment over an expanded workforce supporting mechanization adoption across contractor demographics.

Rise in Polished Concrete Architectural Specifications and Premium Floor Demand

Growing demand for polished concrete flooring in architectural and commercial applications is driving the adoption of ride-on trowels, with polished concrete becoming a design standard across retail stores, data centers, logistics hubs, and institutional facilities that require high-quality base surface preparation. Architectural specifications increasingly mandate high-performance ride-on trowels to achieve consistent substrates before polishing. Premium flooring valuation supports contractor investment in advanced finishing equipment, enabling competitive differentiation and superior aesthetic outcomes. Expanding decorative concrete trends create sustained demand for specialized finishing capabilities aligned with architectural design intent.

Exclusive flatness and levelness requirements, including FF/FL specifications, further drive equipment purchasing to ensure compliance, quality assurance, and customer satisfaction on premium projects where visual uniformity, durability, and long-term performance are critical success factors. These dynamics reinforce the adoption of mechanized finishing, support productivity optimization, reduce rework risk, and align contractor capabilities with evolving architectural expectations nationwide.

Restraints - High Equipment Costs and Capital Investment Barriers for Direct Ownership

Ride-on power trowel equipment exhibits substantial capital costs, creating purchase barriers, particularly for smaller contractors. Hydrostatic models command significant premiums relative to mechanical alternatives, limiting ownership to larger firms and rental fleet operators, and constraining direct-purchase market growth and profitability. Equipment cost limitations restrict ownership to larger contractors and rental firms, reducing the addressable market. Financing constraints affecting mid-size contractor purchasing decisions and capital allocation. Rental-dependent market structure supporting equipment access without capital commitment, but constraining OEM direct sales and margin sustainability. Premium technology pricing on hydrostatic models is limiting adoption among cost-sensitive contractors preferring mechanical alternatives.

Supply Chain Constraints and Component Availability Pressures on Manufacturers

Ride-on power trowel manufacturing exhibits supply chain vulnerabilities, affecting component availability and equipment delivery timelines. Specialized hydraulic components and precision-engineered blades face sourcing challenges, limiting production capacity and extending customer wait times during demand surges. The complexity of component sourcing across hydraulic systems, engines, and specialized materials creates manufacturing dependencies. Manufacturing capacity constraints during demand surge periods are limiting equipment delivery timelines and customer satisfaction. Lead-time variability affects project scheduling and contractor planning, creating operational challenges. Service parts availability is creating maintenance bottlenecks and customer downtime challenges, impacting fleet utilization and revenue realization.

Opportunity - Hydrostatic Technology Adoption and Premium Equipment Market Expansion

Hydrostatic drive technology adoption represents a substantial market opportunity driven by approximately 20% faster finishing on large pours, superior torque modulation, smoother controls, and longer operational life. North America shows an accelerating preference for hydrostatic systems on high-specification projects, reinforcing premium positioning and margin expansion. Growth in North America and Western Europe outpaces mechanical trowels, supporting the development of the premium segment. Contractors favor reduced operator fatigue, precise control, and consistent performance, improving productivity and finish quality. High-specification projects, including polished concrete floors and premium commercial applications, increasingly specify hydrostatic equipment. These dynamics enable higher-margin business models, stronger profitability, and differentiation for manufacturers and rental fleets targeting performance-driven customers. Adoption trends reflect contractor sophistication, lifecycle cost focus, and evolving project quality expectations nationwide.

Low-Emission and Electric Trowel Technology Development and Regulatory Compliance

Low-emission and electric power trowel development represents an emerging market opportunity driven by stringent state-level emission regulations in California, Washington, and other jurisdictions mandating compliant construction equipment. Hybrid and battery-assist pilot programs are demonstrating commercial viability, accelerating technology maturation and reducing adoption risk for contractors and rental fleets. Regulatory pressure supports early deployment, while quieter, cleaner operation aligns with operator preferences for indoor environments such as basements, tunnels, warehouses, and enclosed commercial spaces. Government incentive programs and sustainability mandates further encourage emissions-reduction investments, enabling fleet transition strategies and long-term compliance planning. As technology performance improves and operating costs decline, next-generation low-emission trowels are positioned to gain traction across urban projects, infrastructure modernization programs, and environmentally regulated construction markets nationwide.

Category-wise Analysis

Product Type Insights

Mechanical trowel systems command 68% of North America market share, representing established technology preferred for cost-effectiveness, ease of maintenance, proven reliability, and broad applicability supporting widespread adoption across diverse project scales and contractor demographics. Cost-effective positioning supporting broad contractor adoption, particularly among smaller firms and regional specialists. Established service infrastructure with widespread technical expertise, parts availability, and local service support. Simplified maintenance requirements reduce operational complexity, downtime risk, and service costs. Proven reliability and industry acceptance supporting market confidence, purchasing preferences, and long-term investment decisions across contractor segments.

Hydrostatic systems expand at 5.3% CAGR, driven by faster finishing, smoother control, longer life, and reduced fatigue, enabling premium positioning on high-specification projects. Performance advantages support pricing power, margin expansion, and operator satisfaction. North America leads adoption, reflecting sophisticated contractor preferences, reinforced by Multiquip’s January 2025 MD105 hydrostatic 10-foot platform.

Material Insights

Steel pan construction commands 34% of the market share, representing the standard material selection, balancing cost-effectiveness with durability, and supporting broad application across diverse project types and contractor economics. Cost-effectiveness supporting market leadership positioning and broad accessibility. Durability characteristics suitable for standard applications and extended equipment lifecycle. Wide availability, enabling ready access and equipment continuity, supporting contractor satisfaction. Established infrastructure with widespread manufacturing and service support enabling efficient supply chains.

High-carbon steel pans grow at a 5.5% CAGR, driven by superior wear resistance, longer service life, lower maintenance, and strong performance on abrasive mixes, enabling lifecycle cost optimization and premium positioning. Durability reduces total ownership costs, extends blade life, lowers maintenance expenses, and supports adoption by contractors across premium applications.

Size Insights

Eight-foot class trowels command ~46% of market share, representing standard equipment size, optimizing balance between finishing capacity, maneuverability, operator control, and accessibility, supporting broad applicability across diverse project types and contractor preferences. Standard specification across industry supporting manufacturing scale, cost efficiency, and supplier standardization. Maneuverability balance supporting effective deployment across diverse project contexts and site conditions. Operator familiarity enables rapid adoption and productivity achievement across contractor experience levels. Rental fleet standardization supporting inventory optimization, maintenance efficiency, and customer availability across regional rental operators.

Ten-foot-plus class trowels grow at 5.4% CAGR, driven by large commercial and infrastructure projects requiring extended coverage for mega-slab applications exceeding 50,000 square feet. Large-slab growth boosts adoption across parking structures and logistics hubs. Extended coverage improves productivity, accelerates timelines, supports premium positioning, higher margins, and sustained expansion momentum.

Regional Insights

United States Ride on-power Trowel Market Trends

The United States dominates the North America market, commanding an 84% regional market share, driven by a mature construction industry, sophisticated project specifications, extensive rental fleet infrastructure, established distribution networks, and technology innovation leadership supporting advanced equipment adoption and continuous market development. Construction industry maturity supports the specification and adoption of advanced equipment across contractor segments. Sophisticated project requirements are particularly in commercial, institutional, and infrastructure sectors. Comprehensive rental fleet infrastructure supporting equipment accessibility and project flexibility without capital barriers. Technology innovation leadership supporting product development and market advancement including hydrostatic adoption and telematics integration.

The U.S. market is characterized by a strong mechanical trowel presence, supplemented by accelerating adoption of hydrostatic systems on premium projects. Rental fleet dominance enabling equipment access without capital investment supporting market growth. Regional variations supporting diverse equipment specifications across climate zones and project types. Leading firms, including Multiquip, maintain market leadership through the Whiteman series product dominance and continuous innovation.

Canada Ride on-power Trowel Market Analysis

Canada demonstrates prominent growth at 5.3% CAGR, driven by industrial facility expansion, construction sector modernization, infrastructure development initiatives, and growing equipment rental market penetration, supporting sustained equipment demand across provincial markets and project types. Industrial development supporting the construction of commercial and warehouse facilities across provinces. Infrastructure modernization is driving public and institutional project activity, including transportation and utility projects. Equipment rental market growth, enabling technology adoption without capital investment. Regional construction recovery is supporting project activity expansion and equipment purchasing decisions.

The Canadian market is characterized by technology adoption aligned with U.S. standards and a growing rental fleet infrastructure supporting equipment accessibility. The expanding industrial sector is creating sustained finishing demand across resource and manufacturing industries. Provincial variations support diverse project specifications across geographic regions and climate conditions.

Competitive Landscape

The North American ride-on power trowel market shows moderate consolidation, led by Multiquip through its Whiteman series, and supported by specialized manufacturers such as Bartell Global, Elco Trowel, Daly Machine, and Atlas Trowel Systems, serving distinct segments. Major rental fleets, including United Rentals, Herc Rentals, H&E Equipment Services, and NES Rentals, control significant equipment volumes and remain critical distribution channels for OEM products.

Strategic Developments

- In June 2025, Multiquip launched the WBH-16BAT zero-emission battery-powered power buggy advancing sustainable construction technology and expanding electric equipment portfolio supporting environmental compliance and emission-reduction objectives for construction projects.

- In February 2025, Herc Rentals completed acquisition of H&E Equipment Services for USD 5.3 billion including USD 1.5 billion debt consolidating market position as third-largest rental company with 600+ locations supporting equipment portfolio expansion.

- In January 2025, Multiquip unveiled revolutionary MD105 ride-on trowel featuring reduced-weight fully hydrostatic design optimized for early-entry decking applications with dual engines, LED lighting, enhanced accessibility supporting market innovation leadership and market segment expansion.

Companies Covered in North America Ride-On Power Trowel Market

- Multiquip Inc.

- Bartell Global

- Elco Trowel Machine

- Daly Machine

- Atlas Trowel Systems

- Somero Enterprises

- Dynamic Manufacturing

- United Rentals

- Herc Rentals

- H&E Equipment Services

- NES Rentals

- United Equipment Rentals

Frequently Asked Questions

The North America ride on-power trowel market is likely to be valued at US$ 58.7 million in 2026 and is projected to reach US$ 82.6 million by 2033, led by the U.S. with 84% share, while Canada grows at a 5.3% CAGR.

Growth is driven by labor shortages, rising polished concrete specifications, and increasing large-scale commercial and infrastructure projects requiring mechanized finishing solutions.

The market is projected to expand at a 5.0% CAGR between 2026 and 2033.

Key opportunities include hydrostatic technology adoption, low-emission and battery-assist development, and connected equipment with telematics for fleet optimization.

Major players include Multiquip Inc., Bartell Global, Elco Trowel, Daly Machine, and Atlas Trowel Systems, with strong influence from rental fleets such as United Rentals, Herc Rentals, and H&E Equipment Services.