- Home Appliances

- Mini Refrigerator Market

Mini Refrigerator Market Size, Share, Trends, Regional Forecasts 2026 - 2033

Mini Refrigerator Market by Product Type (Single Door Refrigerators, Double Door Refrigerators), Capacity Segment (Less Than 1 cu. Ft, 1–1.9 cu. Ft, 2–2.9 cu. Ft, 3–3.9 cu. Ft, 4–5 cu. Ft), Application (Residential, Commercial), Sales Channel (Wholesalers / Distributors, Exclusive Stores, Independent Small Stores, Online Retailers, Other Sales Channels), and Regional Analysis from 2026 - 2033

Mini Refrigerator Market Share and Trends Analysis

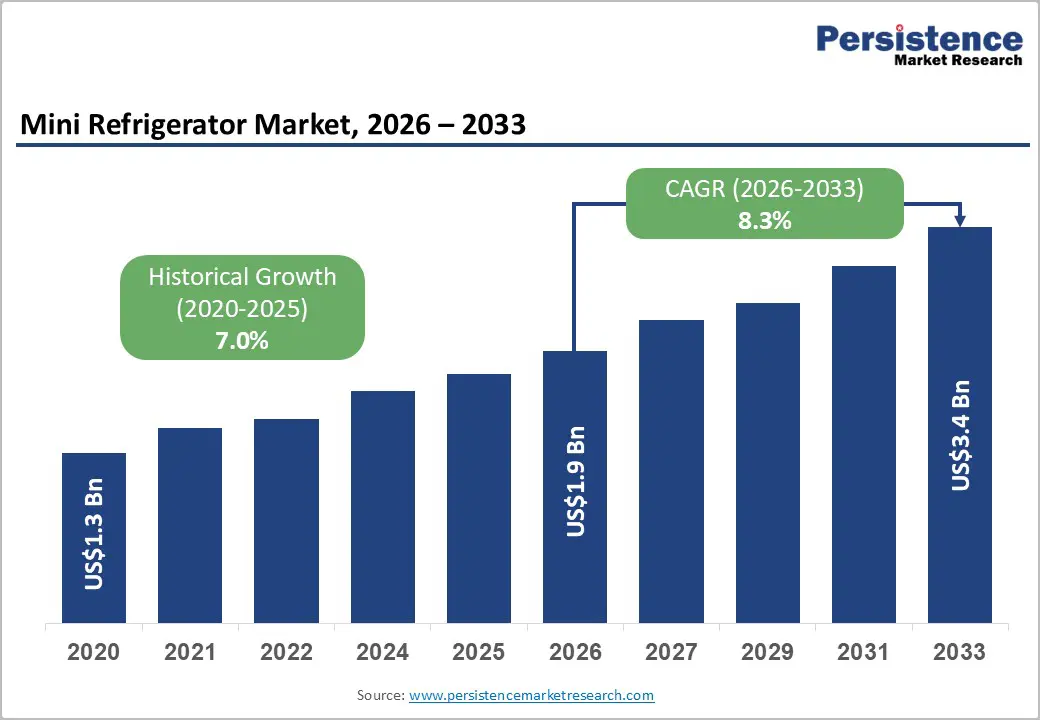

The global mini refrigerator market size is anticipated at US$ 1.9 billion in 2026 and is projected to reach US$ 3.4 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033.

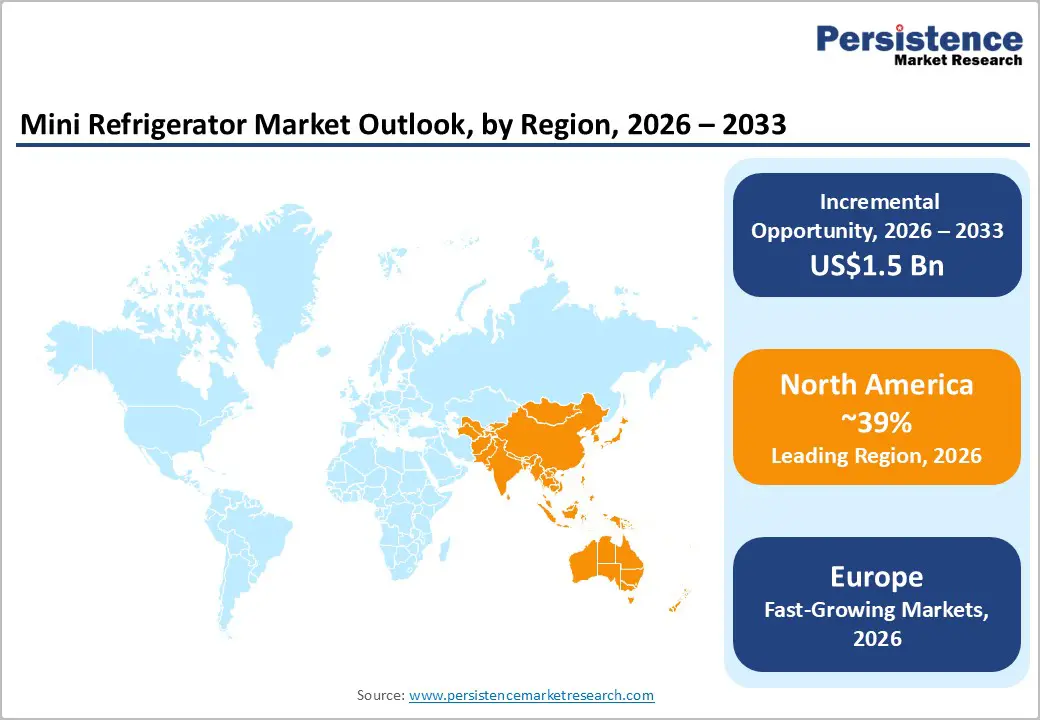

Market expansion is driven by accelerating urbanization and micro-apartment proliferation, which require space-saving appliances, remote work and home-office expansion that support personal beverage and snack storage, and smart-home integration with IoT, enabling voice-controlled, app-managed cooling. North America grows at 7.8% CAGR, Europe holds 22% share via sustainability and hospitality demand, while the Asia Pacific leads with 39% share globally today.

Key Industry Highlights:

- Single-door refrigerators command 64% market share, reflecting cost-effectiveness and broad adoption, while double-door models expand at 8.8% CAGR

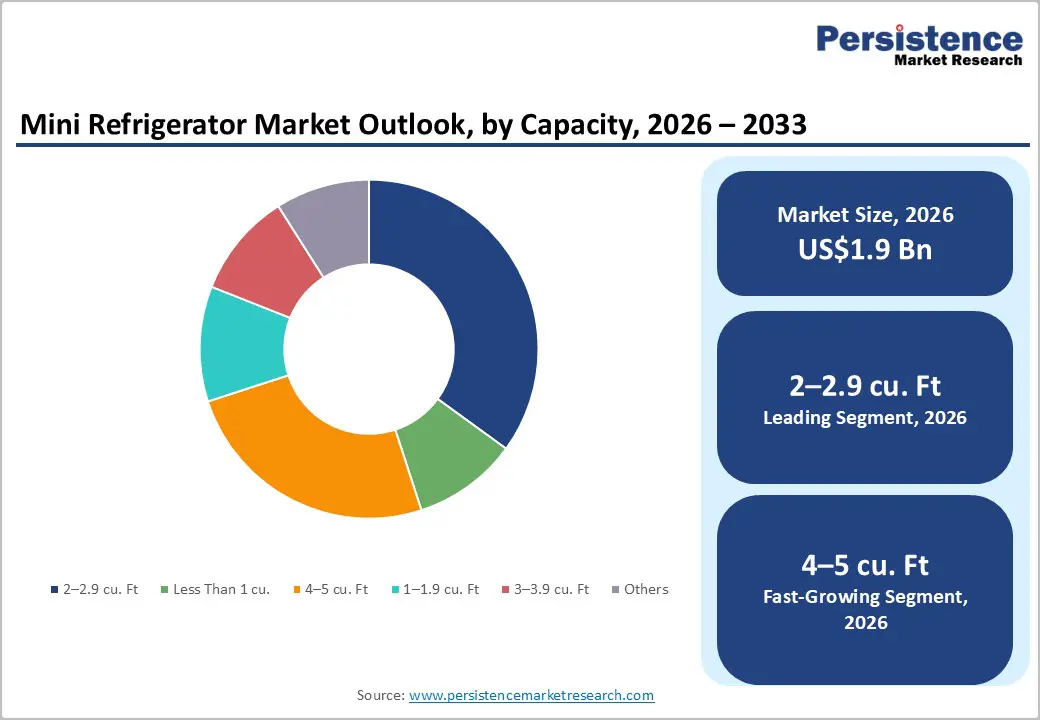

- 2-2.9 cu. ft capacity dominates at 29% share, reflecting optimal storage balance, while 4-5 cu. ft segment expands at 9.1% CAGR, supporting commercial and premium residential applications.

- Residential applications lead at 63% market share, while the commercial segment expands at 9% CAGR driven by hospitality sector modernization and office space requirements.

- Europe maintains 22% market share with a sustainability emphasis, Asia Pacific commands 39% with emerging market growth momentum, and North America grows at 7.8% CAGR with remote work and RV popularity.

- Samsung launches AI Hybrid Cooling with Peltier module, achieving a 25-liter capacity increase (December 2024), improves food freshness 1.4x-1.2x (2025), and manufacturers introduce Wi-Fi smart mini-fridges with voice control (2024-2025), demonstrating technology innovation and smart home integration momentum.

| Key Insights | Details |

|---|---|

|

Mini Refrigerator Market Size (2026E) |

US$ 1.9 billion |

|

Market Value Forecast (2033F) |

US$ 3.4 billion |

|

Projected Growth CAGR (2026-2033) |

8.3% |

|

Historical Market Growth (2020-2025) |

7.0% |

Market Dynamics Analysis

Driver - Urbanization and Micro-Apartment Living Driving Compact Appliance Demand

Urbanization and the proliferation of micro-apartments are accelerating the adoption of mini-refrigerators, as consumers increasingly favor compact living solutions and space-efficient appliances that deliver reliable, affordable cooling. Sustained demand is evident across urban residential units, student dormitories, and shared living environments where functionality and footprint efficiency are critical. The expansion of single-person households further supports personal refrigeration demand, while rising student populations in metropolitan centers increase uptake. The growth of shared living and co-housing models increases demand for individual cooling units in constrained spaces. Space limitations, affordability advantages over full-size refrigerators, and ease of portability, which enables frequent relocation, remain key purchase drivers. Additionally, diverse color palettes and modern design options enhance aesthetic integration, supporting acceptance among style-conscious urban consumers seeking efficiency, flexibility, and long-term value.

Remote Work Expansion and Home Office Demand Supporting Residential Mini Fridge Adoption

The proliferation of remote work and the widespread adoption of home offices are systematically increasing demand for residential mini-refrigerators, as professionals increasingly maintain dedicated workspaces that require personal beverage and snack storage. Residential applications command roughly 63% of market share, reinforcing sustained growth across micro-apartments and work-from-home environments and reflecting fundamental workplace evolution. Home office beverage storage supports uninterrupted workflows, while convenient access enhances daily productivity and comfort. Cost savings from reduced commuting and home-based work encourage incremental investment in appliances. Flexible and hybrid work arrangements further justify long-term household purchases. Rising prioritization of home convenience, combined with personal space customization preferences, supports the adoption of compact refrigeration solutions. As hybrid work models mature, mini-refrigerators function as productivity enablers, aligning efficiency, affordability, and lifestyle flexibility within residential settings.

Restraints - Limited Storage Capacity and Specialized Application Constraints Affecting Mass-Market Appeal

Mini refrigerator market expansion is constrained by inherent capacity limitations, with typical units ranging from one to five cubic feet, offering insufficient storage for large families or bulk grocery needs and restricting adoption in traditional households. The strong single-person usage focus limits family penetration, while reduced freezer space hampers bulk storage. Despite its compact size, power consumption remains a concern for value buyers. Budget models raise durability and longevity concerns; temperature consistency can vary; replacement cycles are shorter; and necessary feature trade-offs driven by size constraints further narrow suitability across segments.

Supply Chain Disruptions and Component Sourcing Constraints Affecting Production

Mini refrigerator market expansion faces constraints from supply chain vulnerabilities impacting compressors, thermostats, and electronic control systems, resulting in production delays and longer lead times, particularly for emerging market suppliers and smaller manufacturers competing in cost-sensitive segments. Compressor sourcing challenges and refrigerant availability constraints raise input risks, while dependence on electronic components exposes manufacturers to shortages. Global logistics disruptions increase freight costs and uncertainty. Ongoing supplier consolidation reduces the number of alternative sourcing options, thereby intensifying quality assurance pressures. Additionally, geopolitical tensions and trade restrictions elevate supply chain risk, complicating capacity planning and inventory management.

Opportunities - Emerging Market Middle-Class Expansion and Commercial Hospitality Sector Growth

Emerging market middle-class expansion and rapid hospitality sector growth represent a substantial opportunity, driven by Asia Pacific commanding nearly 39% market share. Accelerating urbanization and expanding hotel and restaurant infrastructure are supporting the widespread deployment of mini-refrigerators across commercial hospitality, food service, and residential applications, enabling growth beyond mature developed markets. Hotels and resorts increasingly require in-room mini-fridges, while food service operators depend on compact refrigeration for efficient back-end storage. Restaurants and cafés rely on beverage cooling to improve service speed. Rising consumer purchasing power in emerging economies strengthens residential adoption. Manufacturing cost advantages across Asia enhance supply competitiveness, while government support for hospitality development and sustained tourism momentum further reinforce long-term demand fundamentals across diversified end-use segments worldwide over the forecast period.

Portable and Off-Grid Mini Refrigerator Solutions Supporting Travel and RV Markets

Portable and off-grid mini-refrigerator solutions represent an emerging opportunity, as van life adoption and recreational vehicle ownership continue expanding globally. The development of solar-powered and battery-operated mini-fridges is supporting a niche market serving mobile consumers, outdoor enthusiasts, and remote users seeking reliable cooling without grid dependence. The RV and van life segment drives demand for compact, rugged designs optimized for mobility. Camping and outdoor recreation further expand usage, while solar-powered variants enable sustainable operation in remote settings. Battery-operated portability enhances flexibility across travel, work, and leisure scenarios. Off-grid applications also support emergency backup refrigeration during power outages. Additionally, portable cooling solutions are increasingly deployed at temporary events, festivals, and outdoor gatherings, allowing premium pricing through specialized features, durability, and energy efficiency.

Category-wise Analysis

Product Type Insights

Single-door mini-refrigerators command 64% of market share, representing dominant product type reflecting cost-effectiveness, space efficiency, and simplicity supporting broad consumer adoption across budget-conscious segments, student housing, offices, and emerging markets. Entry-level pricing advantage. Compact space footprint. Economical operation, power consumption. Easy maintenance and cleaning. Straightforward functionality design. Reversible door options. Global market dominance positioning.

Double-door mini-refrigerators expand with 8.8% CAGR as the fastest-growing product category, driven by the premium market segment seeking enhanced storage organization and freezer capability supporting emerging demand in luxury hospitality, premium residential, and specialized applications where enhanced compartmentalization and freezing capability justify premium pricing. Separate freezer compartment. Food organization capability. Frost-free technology integration. Premium features focus. Larger capacity accommodation. Luxury hotel application. Emerging affluent consumer segment.

Capacity Insights

2-2.9 cubic feet capacity segment commands 29% of market share, representing the optimal sweet spot reflecting an ideal balance between storage functionality and spatial footprint supporting broad consumer adoption across dorms, offices, bedrooms, and small apartments.

4-5 cubic feet capacity segment expands as the fastest-growing category with a CAGR of 9.1%, driven by commercial operators and affluent consumers seeking expanded storage without a full-size refrigerator commitment, supporting emerging demand for premium compact solutions in hospitality, commercial offices, and upscale residential settings, reflecting consumer preference for enhanced capacity.

Application Insights

Residential applications command 63% of market share, representing a dominant end-use segment reflecting primary consumer focus on dorms, bedrooms, offices, and micro-apartments with broad household adoption supporting sustained market growth across diverse demographic segments.

Commercial applications are the fastest-growing end-use segment, with a 9.0% CAGR, driven by growth in the hospitality sector, retail environments, and food-service operator requirements. Emerging demand for commercial-grade mini-refrigerators with enhanced reliability and capacity is supporting hotel, restaurant, and retail operations.

Sales Channel Insights

Wholesalers and distributors command 31% of the market, reflecting a traditional dominant sales channel with established distribution networks, B2B relationships, and bulk purchase support, enabling broad market penetration across retail outlets, dorm furnishers, and hospitality suppliers. Online retailers are the fastest-growing sales channel, with a 10% CAGR, driven by direct-to-consumer convenience, price comparison, and home delivery, which are supporting emerging e-commerce dominance among convenience-driven consumers and digital-native shoppers increasingly purchasing mini-refrigerators online.

Regional Insights

North America Mini Refrigerator Market Share and Trends

North America is likely to experience expansion at a 7.8% CAGR over the forecast period. The market here is driven by the prevalence of remote work, the popularity of recreational vehicles, and technological innovation. Remote work adoption drives investment in home offices. The North American market is characterized by technology leadership and diverse application adoption, with manufacturers investing in smart and energy-efficient solutions.

Europe Mini Refrigerator Market Share and Trends

Europe maintains a 22% market share, with considerable growth, driven by an emphasis on sustainability, the prevalence of micro-apartments, regulatory efficiency standards, and the modernization of the hospitality sector, which supports the adoption of advanced technologies. The European market is characterized by heightened sustainability consciousness and regulatory compliance, with manufacturers focusing on energy-efficient and environmentally friendly designs. Strong emphasis on premium and specialized products, including wine coolers and under-counter models.

Asia Pacific Mini Refrigerator Market Trends

Asia Pacific commands a significant 39% market share, driven by rapid urbanization, student population growth, emerging middle-class expansion, and manufacturing scale advantages supporting market growth exceeding global averages. Asia Pacific is characterized by rapid growth and emerging market opportunities, with China and India driving high-growth trajectories. Cost-competitive production is attracting global supply chain development. Student and youth demographic focus supporting the residential segment. Government support and infrastructure investment are accelerating adoption and infrastructure development.

Competitive Landscape

The mini-refrigerator market shows moderate consolidation, led by multinational players such as Haier, Whirlpool, LG Electronics, and Samsung, leveraging global distribution, innovation, and strong brands. Regional specialists like Danby, Dometic, and Midea focus on geography and applications, while emerging direct-to-consumer brands exploit e-commerce and digital marketing to drive technology-led differentiation.

Strategic Developments

- In December 2024, Samsung announced next-generation AI Hybrid Cooling refrigerators featuring Peltier module semiconductor technology, combining a compressor with solid-state cooling, achieving 4.1x greater inertia efficiency and increasing interior capacity by 25 liters while reducing energy consumption, demonstrating technology advancement momentum.

Companies Covered in Mini Refrigerator Market

- Haier Group Corporation

- Whirlpool Corporation

- LG Electronics

- Samsung Electronics

- Danby Products

- Dometic Group AB

- Midea Group

- Godrej & Boyce

- Cooluli (EcoSmart Solutions)

- NewAir (Overland Brands)

- Tropicool

- Kelvinator

- Hisense

- Crownful

Frequently Asked Questions

The global mini refrigerator market is anticipated at US$ 1.9 Billion in 2026 and is projected to reach US$ 3.4 Billion by 2033.

Market growth is fueled by rapid urbanization and micro-apartment living, expanding remote work and home office usage accounting for 63% residential demand, and rising smart home adoption with IoT- and voice-enabled cooling solutions.

The market is projected to expand at an 8.3% CAGR between 2026 and 2033.

Key opportunities lie in Asia Pacific’s emerging middle class and hospitality growth, rising demand for portable and off-grid mini-fridges, and premium energy-efficient models leveraging advanced Peltier and eco-friendly technologies.

The market is led by Haier, Whirlpool, LG Electronics, Samsung, Danby, and Dometic, with competition intensifying through smart, energy-efficient, and application-specific product innovations.