- Specialty & Fine Chemicals

- Aminic Antioxidant Market

Aminic Antioxidant Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Aminic Antioxidant Market by Product Type (Diphenylamine Derivatives, Phenyl-α-Naphthylamine (PANA), Alkylated Phenyl-α-Naphthylamine (Alkyl-PANA), Others), Source, Application, Industry, Regional Analysis, 2025 - 2032

Aminic Antioxidant Market Size and Trend Analysis

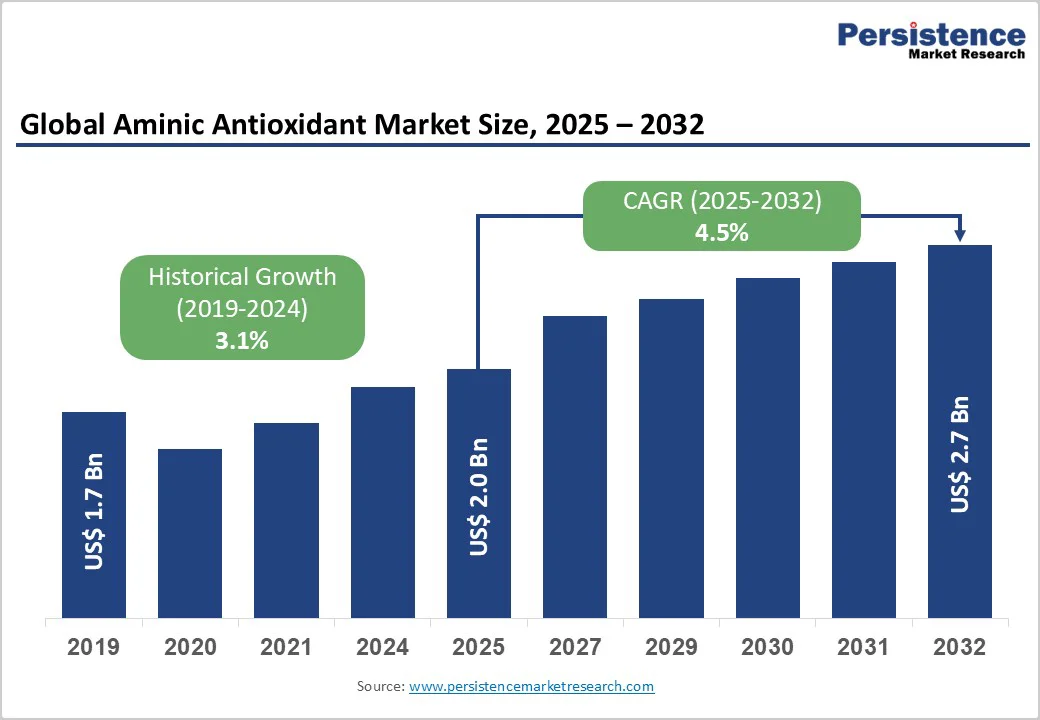

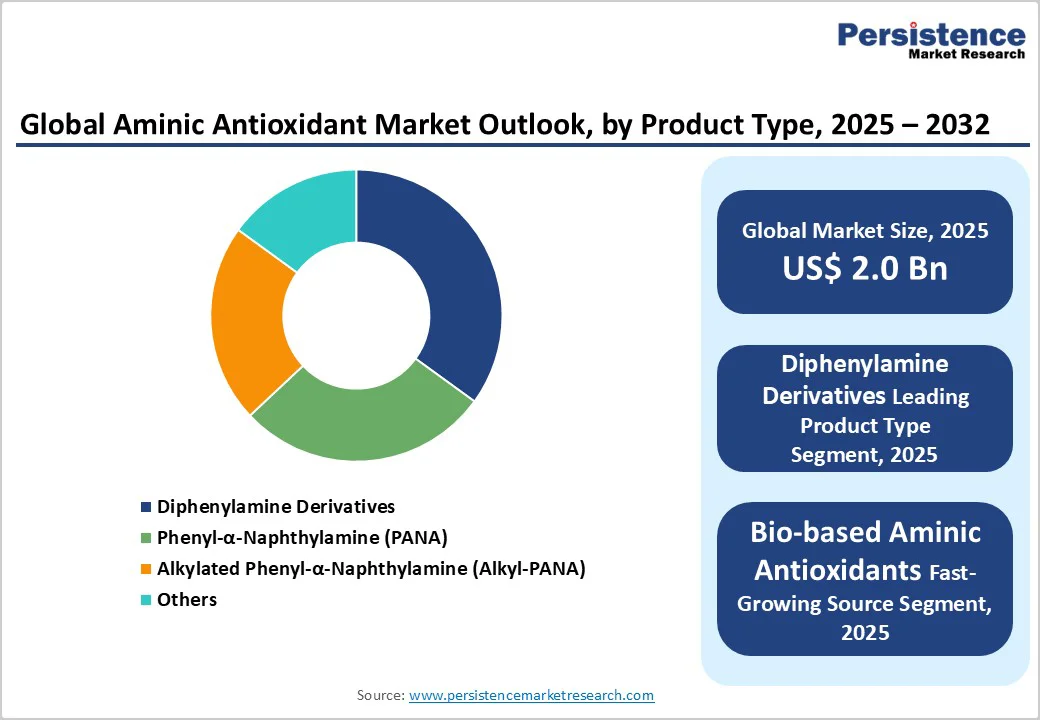

The global aminic antioxidant market size is likely to value at US$ 2.0 billion in 2025 and is projected to reach US$ 2.7 billion by 2032, growing at a CAGR of 4.5% between 2025 and 2032.

Rising demand for high-performance stabilizers in lubricants and polymers to enhance product longevity and performance under extreme conditions is one of the key factors driving the market growth. This growth is also supported by the growing need for advanced additives in the automotive industry to meet emission standards and improve fuel efficiency will further drive market growth.

Key Market Highlights:

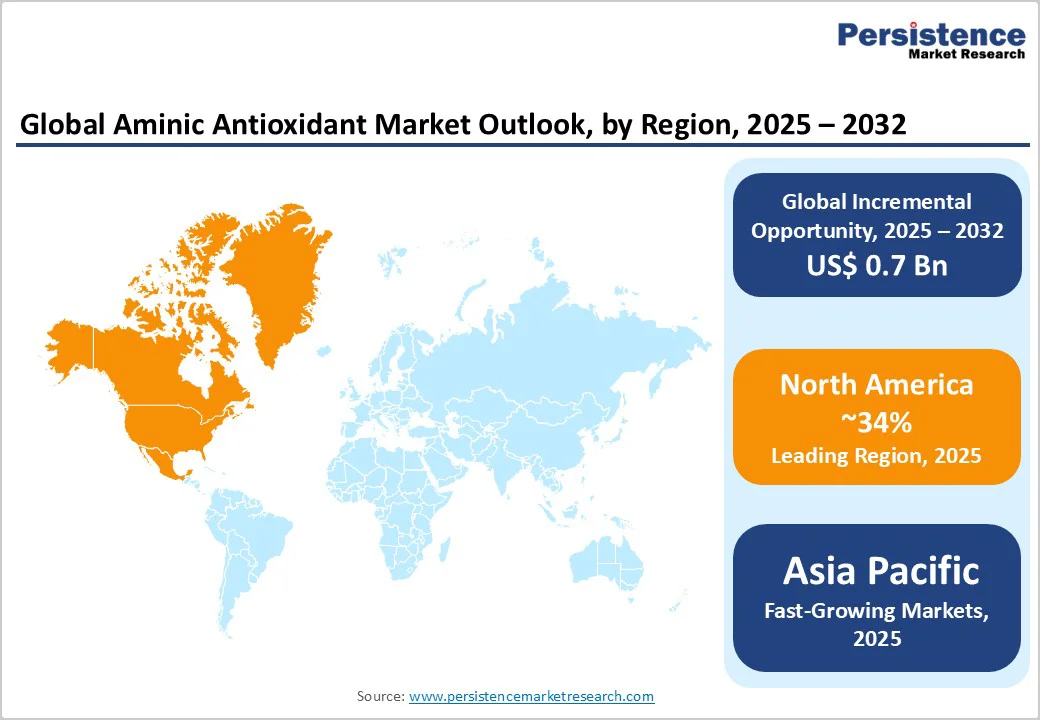

- Leading Region: North America dominates as the leading region with a 34% share, due to advanced manufacturing and stringent U.S. regulations promoting high-performance antioxidants in automotive lubricants.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by rapid industrialization in China and India, boosting demand for polymer stabilizers in exports.

- Leading Segment: Diphenylamine Derivatives are the dominant Product Type segment with approximately 50% market share, offering exceptional thermal stability essential for industrial applications.

- Fastest-Growing Segment: Bio-based Aminic Antioxidants represent the fastest-growing Source segment, aligned with global sustainability policies like the EU Green Deal.

- Key Opportunity: Expansion in aerospace applications offers a key opportunity, with high-temperature needs driving innovation in durable fuel additives.

| Key Insights | Details |

|---|---|

| Aminic Antioxidant Market Size (2025E) | US$ 2.0 billion |

| Market Value Forecast (2032F) | US$ 2.7 billion |

| Projected Growth CAGR (2025 - 2032) | 4.5% |

| Historical Market Growth (2019 - 2024) | 3.1% |

Market Dynamics

Driver - Rising Demand in Automotive Lubricants

The automotive industry's expansion is a primary driver for the aminic antioxidant market, as these compounds are essential for protecting engine oils from oxidation at high temperatures. With global vehicle production reaching over 90 million units annually, as reported by the International Organization of Motor Vehicle Manufacturers (OICA), aminic antioxidants extend lubricant life by up to 50%, reducing maintenance costs and emissions.

This is particularly evident in the shift toward electric and hybrid vehicles, where thermal stability is critical for battery and transmission fluids, supported by advancements from companies like BASF SE. Consequently, the integration of these antioxidants enhances fuel efficiency and complies with stringent standards such as Euro 7, fostering market growth.

Advancements in Polymer Stabilization

Rapid advancements in polymer processing technologies are significantly increasing the demand for aminic antioxidants, which play a crucial role in preventing oxidative degradation of plastics and rubbers used across packaging, automotive, and construction industries.

These antioxidants safeguard polymer chains from thermal and UV-induced breakdown, thereby extending material life and preserving performance under harsh conditions. According to the American Chemistry Council, the U.S. plastics industry produced over 100 billion pounds of resins in 2024, underscoring the scale at which stabilizing additives are required.

Aminic antioxidants are particularly valued for their high-temperature resistance and synergistic compatibility with phenolic antioxidants, ensuring durability in recycled and bio-based polymers. Their application enhances mechanical strength, color retention, and recyclability, enabling manufacturers to produce longer-lasting materials that align with circular economy principles.

Consequently, these innovations are fostering a shift toward sustainable, high-performance polymer formulations worldwide.

Restraint - Stringent Environmental Regulations

Regulatory hurdles, such as the EU REACH framework and U.S. EPA guidelines, restrict the use of certain synthetic aminic antioxidants due to potential toxicity concerns, impacting market accessibility.

For instance, the European Chemicals Agency has classified some diphenylamine derivatives as persistent environmental contaminants, leading to bans in sensitive applications and increasing compliance costs by up to 20% for manufacturers. This restraint hampers innovation in traditional formulations, forcing shifts to costlier alternatives and slowing adoption in regions with tight controls.

Volatility in Raw Material Prices

Fluctuations in petrochemical feedstocks, driven by geopolitical tensions, pose a significant barrier, with crude oil prices varying by 30% in 2024 according to the U.S. Energy Information Administration. Aminic antioxidants, derived from aniline and alkyl halides, face supply chain disruptions, raising production expenses and squeezing margins for smaller players. This volatility discourages investment in expansion, particularly in emerging markets, and limits the scalability of bio-based variants still in early development stages.

Opportunity - Shift Toward Bio-based Antioxidants

The transition to bio-based aminic antioxidants presents a major opportunity, aligning with global sustainability goals like the EU Green Deal, which aims to reduce chemical emissions by 55% by 2030. Derived from renewable sources such as vegetable oils, these variants offer comparable efficacy to synthetics while being biodegradable, with early pilots showing 40% lower environmental impact per the International Union of Pure and Applied Chemistry (IUPAC).

Companies like SI Group are investing in R&D, with bio-content exceeding 95% in new accelerators, targeting the growing eco-friendly lubricants segment projected to expand rapidly in Asia Pacific. This opportunity is bolstered by consumer preferences for green products, driving demand in the Antioxidants Market for non-toxic stabilizers.

Expansion in Aerospace and Oil & Gas Sectors

Emerging applications in aerospace and oil & gas offer substantial growth potential, where high-temperature stability is paramount, as per NASA guidelines requiring additives to withstand 200°C without degradation. The global aerospace market is forecasted to have an opportunity US$ 9 trillion by 2040 according to Boeing, increasing the need for aminic antioxidants in sealants and fuels to prevent oxidation during extreme operations.

Recent developments, including LANXESS's sustainable rubber additives certified under ISCC PLUS in 2024, highlight innovations for these sectors, with potential revenue growth from enhanced durability in drilling fluids. Policy support through the U.S. Inflation Reduction Act incentivizes low-emission technologies, positioning this as a key pocket for market players.

Category-wise Insights

Product Type Analysis

Diphenylamine Derivatives dominate the product type segment with approximately 50% market share, owing to their superior thermal stability and versatility in lubricant formulations. Sub-types like Nonylated Diphenylamine (NDPA) and Octylated Diphenylamine (ODPA) are widely used for their ability to inhibit free radicals effectively, as demonstrated in ASTM D943 oxidation tests where they extend oil life by 2-3 times compared to alternatives.

This leadership is supported by high demand in automotive applications, where these derivatives ensure compliance with API SN standards for engine performance. Their cost-effectiveness and compatibility with blends further solidify their position in industrial settings.

Source Analysis

Synthetic Aminic Antioxidants lead the Source category with around 85% share, driven by their proven efficacy and scalability in large-volume production. Manufactured via processes like alkylation of aniline, these antioxidants provide consistent performance in preventing peroxidation, as validated by ISO 4263 standards showing reduced sludge formation in fuels.

The dominance stems from established supply chains and lower costs compared to bio-based options, with major producers like BASF SE optimizing formulations for high-temperature environments. This segment benefits from ongoing R&D to meet regulatory demands, ensuring reliability across polymers and elastomers.

Application Analysis

Lubricants hold the top position in the Application segment with about 40% market share, fueled by their critical role in enhancing oxidative resistance in engine and industrial oils. According to SAE International, lubricants treated with aminic antioxidants demonstrate up to 60% longer service intervals, reducing downtime in heavy machinery.

This leadership is justified by the global lubricants market's growth, where these additives address challenges from bio-fuels and electric vehicle fluids. Their widespread use in hydraulic systems and greases underscores their importance in maintaining efficiency.

Industry Analysis

Automotive commands the Industry category with roughly 35% share, as aminic antioxidants are indispensable for protecting tires, belts, and fluids from thermal degradation.

Data from the International Energy Agency indicates that automotive production surged by 5% in 2024, amplifying the need for these stabilizers to meet CAFE fuel economy standards. The segment's prominence is evidenced by their application in over 70% of synthetic engine oils, improving longevity and reducing emissions. Innovations tailored for hybrid systems further reinforce this dominance.

Regional Insights

North America Aminic Antioxidant Market Trends

North America leads the Aminic Antioxidant Market with a 34% share, driven by robust U.S. automotive and manufacturing sectors. The U.S. Environmental Protection Agency (EPA) enforces strict guidelines under the TSCA, promoting high-performance additives that reduce volatile emissions, with innovations like BASF SE's capacity expansions in Mexico enhancing supply resilience.

This regulatory framework fosters an innovation ecosystem, where R&D investments exceed US$ 2 billion annually per the National Science Foundation, supporting advanced formulations for electric vehicles. The region's trends also reflect a focus on sustainability, with bio-based pilots gaining traction amid the Clean Air Act amendments, positioning North America as a hub for next-gen antioxidants.

Europe Aminic Antioxidant Market Trends

Europe's market is characterized by harmonized regulations under REACH, emphasizing low-toxicity aminic antioxidants in Germany and the U.K. Germany's chemical industry, contributing 8% to EU GDP as per CEFIC, drives demand through automotive giants like Volkswagen, where these additives ensure compliance with Euro 6 norms. France and Spain are advancing sustainable variants, with LANXESS expanding capacities to meet regional needs for eco-friendly lubricants.

Performance analysis shows a 10% CAGR in polymer applications, supported by the EU Circular Economy Action Plan, which mandates recyclable materials and boosts antioxidant use in construction. This harmonization accelerates adoption across borders, enhancing market stability.

Asia Pacific Aminic Antioxidant Market Trends

Asia Pacific emerges as the fastest-growing region, propelled by manufacturing booms in China and India. China's output of over 50 million vehicles in 2024, per the China Association of Automobile Manufacturers, fuels demand for lubricants stabilized by aminic antioxidants. India's petrochemical sector, growing at 7% annually according to the Ministry of Petroleum and Natural Gas, leverages cost advantages for polymer production.

Growth dynamics in ASEAN countries highlight export-oriented manufacturing, with Songwon Industrial Co. introducing high-performance blends for sustainable plastics. This region's advantages in low-cost labor and raw materials position it for 5% annual expansion, outpacing global averages.

Competitive Landscape

The global aminic antioxidant market is characterized by a consolidated competitive landscape, dominated by a select group of major players with strong integrated production networks and robust R&D capabilities. Strategies focus on capacity expansions and partnerships, as seen with BASF SE's investments in Mexico, to secure raw materials and enter high-growth regions like Asia Pacific.

Leaders differentiate via proprietary formulations offering superior thermal stability, while emerging models emphasize sustainability, such as bio-based blends to comply with global eco-regulations. R&D trends prioritize multifunctional additives, reducing market fragmentation and enhancing barriers to entry for smaller firms.

Key Market Developments:

- In March, 2025: BASF SE announced a major investment at its Puebla (Mexico) manufacturing site aimed at expanding aminic antioxidant production for lubricants-addressing rising global demand for long-life oils and bolstering supply reliability.

- In April, 2024: Songwon Industrial Co. unveiled its SONGNOX® binary antioxidant blends at NPE 2024, designed to improve thermal and process stability of recycled and bio-based polymers-supporting circular-economy goals in plastics.

- In March, 2025: LANXESS presented its ISCC PLUS-certified rubber antioxidant (Vulkanox HS Scopeblue) at the Tire Technology Expo 2025, enabling automotive tire makers to adopt eco-friendly additive solutions without changing existing manufacturing processes.

Companies Covered in Aminic Antioxidant Market

- Songwon Industrial Co.

- BASF SE

- Si Group

- Jiyi Chemical

- Yasho Industries

- King Industries

- LANXESS

- Sea-Land Chemical Company

- Hangzhou Sungate Chemical

- Solvay

- Eastman Chemical Company

- Nouryon

Frequently Asked Questions

The Aminic Antioxidant Market is valued at US$ 2.0 billion in 2025 and expected to reach US$ 2.7 billion by 2032, growing at a CAGR of 4.5%.

Key drivers include rising automotive production and polymer innovations, with global vehicle output over 90 million units annually, enhancing the need for oxidative stability in lubricants.

Diphenylamine Derivatives lead with 50% share, due to their thermal stability in high-performance applications like engine oils.

North America leads with a 34% share in 2025, supported by U.S. regulatory frameworks and manufacturing strength.

The shift to bio-based variants offers significant potential, with over 95% biocarbon content in new products meeting sustainability demands.

Major players include BASF SE, Songwon Industrial Co., and LANXESS, focusing on capacity expansions and sustainable innovations.