- Advanced Materials

- Speaker Membrane Market

Speaker Membrane Market Size, Share, and Growth Forecast 2026 - 2033

Speaker Membrane Market by Material Type (Paper, Polypropylene (PP), PET, Metallic, Carbon Fiber, Others), Speaker Type (Home Audio, Portable Audio, Automotive Audio, Professional Audio), Distribution Channel (OEM, Aftermarket, Distributors & Wholesalers, Online Retail, Direct Sales), End-user, by Regional Analysis, 2026 - 2033

Speaker Membrane Market Size and Trend Analysis

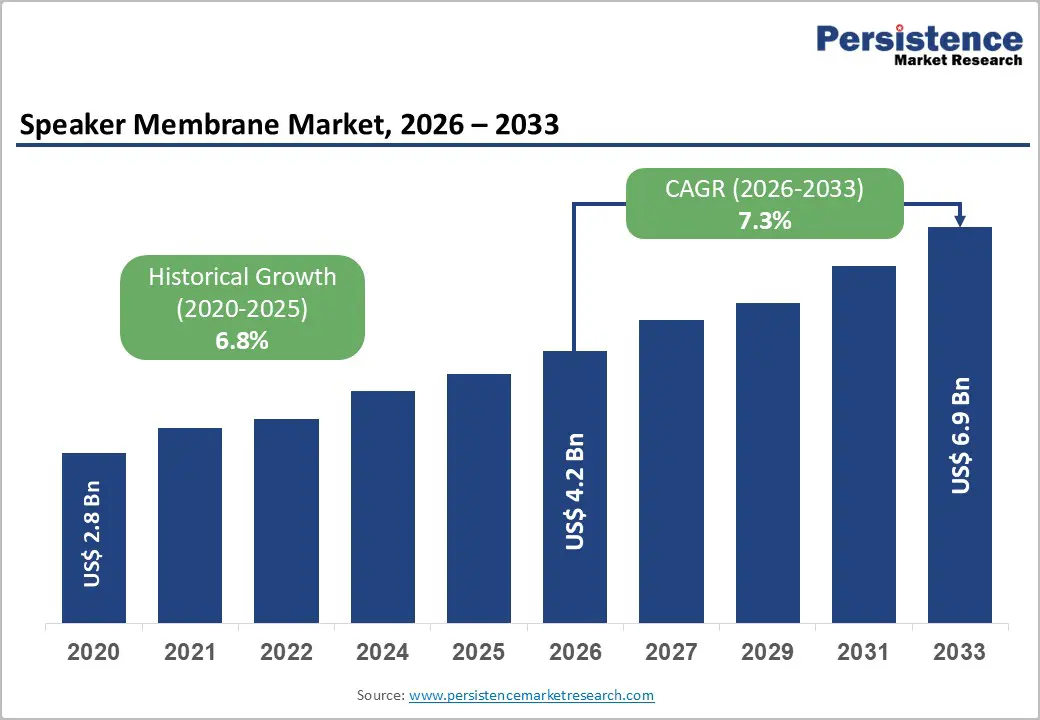

The global speaker membrane market size is likely to be valued at US$ 4.2 billion in 2026 and is expected to reach US$ 6.9 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033. The speaker membrane market is experiencing robust expansion driven by exponential growth in consumer electronics demand, particularly from smartphone proliferation and wireless audio adoption, coupled with technological advancements in membrane materials enabling superior acoustic performance and durability.

Key Industry Highlights:

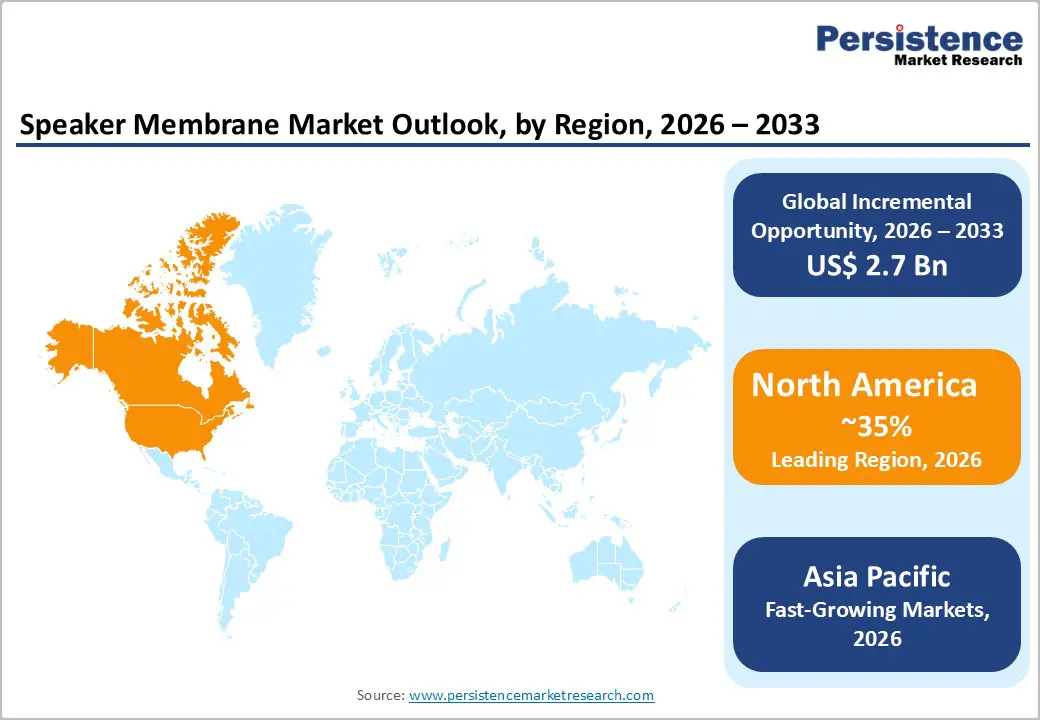

- Leading Region: North America commands significant market dominance through extensive premium audio adoption, sophisticated automotive infotainment integration, and professional audio demand, with U.S. market representing the largest single-country opportunity generating sustained consumer electronics and aftermarket demand supporting continued regional expansion.

- Fastest-Growing Region: Asia Pacific emerges as the fastest-growing regional market at an 8.7% CAGR, driven by China's 60% global smartphone production share, India's 169 million smartphone sales in 2024, and accelerating smart speaker adoption at a 22.6% CAGR, creating substantial incremental membrane demand.

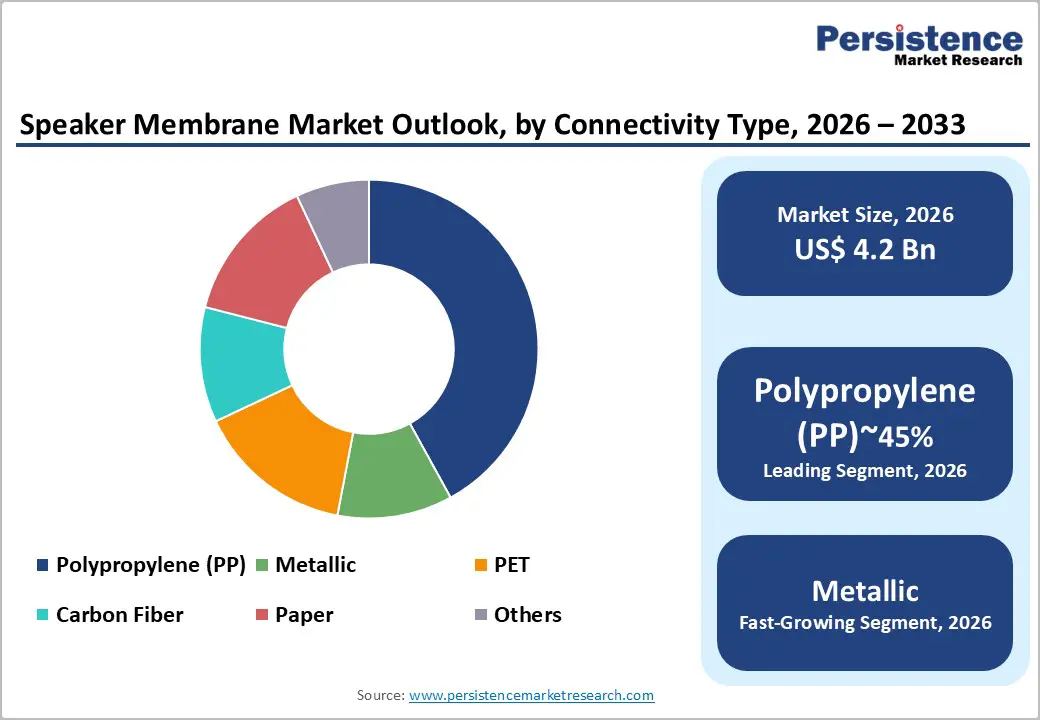

- Leading Segment: Polypropylene membranes maintain market leadership with a 42% market share, driven by superior durability, moisture resistance, and design flexibility, enabling optimization across diverse automotive, portable audio, and professional applications.

- Fastest-Growing Segment: Metallic membranes are the fastest-growing material segment, with an 8.2% CAGR, driven by increasing demand for high-performance audio systems, superior power-handling capabilities, and enhanced frequency-response characteristics that command premium pricing in luxury consumer and professional audio markets.

- Key Opportunity: Advanced materials, such as graphene and nanocomposites, are redefining acoustic performance standards and creating premium growth opportunities for manufacturers.

| Key Insights | Details |

|---|---|

|

Speaker Membrane Market Size (2026E) |

US$ 4.2 Billion |

|

Market Value Forecast (2033F) |

US$ 6.9 Billion |

|

Projected Growth CAGR(2026-2033) |

7.3% |

|

Historical Market Growth (2020-2025) |

6.8% |

Market Dynamics

Drivers - Rapid Adoption of Wireless Audio Devices and Smart Home Ecosystems is Significantly Expanding Global Demand for Advanced Speaker Membrane Technologies

The wireless audio segment is witnessing rapid growth, driven largely by the global expansion of smart home ecosystems. Platforms such as Samsung SmartThings, which surpassed 350 million users by August 2024, have significantly increased demand for advanced speaker membrane technologies that support voice control, smart assistants, and seamless multi-device connectivity. Speakers are no longer limited to basic audio playback; they now function as central control units that manage lighting, appliances, and home security systems.

This shift is pushing manufacturers to develop membranes that deliver improved frequency response, lower distortion, and higher power-handling efficiency. At the same time, the widespread removal of headphone jacks from premium smartphones has accelerated the adoption of Bluetooth. As wireless earbuds and headphones become standard consumer accessories, demand is rising for compact yet durable membrane solutions that maintain sound quality despite reduced device size. Together, these trends are expanding the market footprint and strengthening long-term growth prospects.

Rising Smartphone Production and Accelerating Electric Vehicle Adoption are Driving Innovation and Premiumization in Speaker Membrane Applications

The consumer electronics segment accounted for approximately 48% of the global speaker membrane market in 2024, with smartphones representing nearly 35% of total demand. Based on global handset production, this translates into an estimated requirement of over 2.4 billion individual speaker membranes annually. Meanwhile, the automotive sector is undergoing a strong transformation, supported by the rapid adoption of electric vehicles. EVs create quieter cabin environments, making audio quality more noticeable and increasingly important to buyers.

As a result, the in-car audio systems market is projected to grow at a CAGR of 11.6% from 2025 to 2035. Automotive manufacturers are investing heavily in premium sound systems, with several reporting up to 15% improvement in vehicle sales after introducing advanced audio features. Additionally, professional audio applications such as concerts, studios, broadcasting, and corporate events continue to grow steadily, requiring membranes deliver consistent performance under demanding operating conditions.

Restraints - Volatile Raw Material Prices and Persistent Supply Chain Disruptions Continue To Pressure Manufacturing Costs And Limit Profitability Across The Industry

Fluctuating raw material prices remain a major challenge for speaker membrane manufacturers, particularly for petroleum-based polymers. In 2024, polyethylene terephthalate (PET) prices increased by approximately 18% year-over-year, significantly impacting production costs for companies operating in price-sensitive markets. Ongoing supply chain disruptions following the pandemic have further complicated procurement strategies, forcing manufacturers to diversify suppliers and invest in regional manufacturing facilities. While these steps improve supply stability, they also entail substantial capital expenditures, placing financial pressure on small and mid-sized firms.

In addition, limited availability of specialty polymers and advanced metal components used in high-performance membranes has intensified competition among buyers. Long lead times and inconsistent supply schedules make inventory planning difficult and delay order fulfillment. The growing use of advanced materials such as carbon fiber composites and graphene also relies on a narrow supplier base, creating production bottlenecks that constrain the expansion of large-scale manufacturing.

Market Commoditization and Aggressive Low-Cost Competition are Reducing Differentiation Opportunities And Intensifying Pricing Pressure For Established Manufacturers

The speaker membrane market faces increasing commoditization, particularly in standard product categories. Manufacturing capacity has expanded rapidly in low-cost regions, especially China, which accounts for over 60% of global smartphone production. This has resulted in oversupply of conventional membranes, intensifying price competition and compressing margins. Standardized membrane specifications used in high-volume electronics reduce opportunities for differentiation, shifting competition toward cost efficiency rather than innovation.

As a result, suppliers focused on premium quality often struggle to compete with low-cost alternatives. Chinese manufacturers have aggressively scaled production of polypropylene and paper membranes by leveraging lower labor costs and operational efficiencies. This has enabled them to capture market share from established global suppliers. Persistent downward pricing pressure challenges manufacturers that are unwilling to compromise performance or durability. Over time, this environment limits investment capacity for research and development, potentially slowing technological advancement across the broader market.

Opportunities - Advanced Materials Such as Graphene and Nanocomposites are Redefining Acoustic Performance Standards and Enabling Premium Growth Opportunities For Manufacturers

Advanced material innovation presents a major growth opportunity for speaker membrane manufacturers. Graphene-enhanced membranes are emerging as a breakthrough technology capable of significantly improving acoustic performance. For example, ORA Graphene Audio’s GrapheneQ membrane exhibits high stiffness, low density, and a Young’s modulus of nearly 130 GPa. These characteristics support wider frequency response, clearer sound reproduction, and improved energy efficiency. Reduced power consumption makes such membranes especially attractive for portable and wireless devices. Improved thermal conductivity also minimizes overheating risks during prolonged use.

Many graphene-based membranes can be integrated into existing manufacturing lines as drop-in replacements, lowering adoption barriers. In addition, nanomaterial integration through techniques such as 3D printing enables rapid prototyping and customized acoustic tuning. Development of bio-based polymer alternatives further supports sustainability goals. Manufacturers investing in these advanced materials can command premium pricing from audiophiles, automotive OEMs, and professional audio brands seeking superior sound differentiation.

Expanding Manufacturing Capacities and Smartphone Adoption in Emerging Asian Economies Have Created Robust Opportunities for the Regional Supply Chain

Asia-Pacific is the fastest-growing region in the speaker membrane market, with an estimated CAGR of 8.7%. Growth is driven by rapid urbanization, rising disposable incomes, and strong consumer electronics manufacturing across China, India, Japan, and South Korea. India alone recorded smartphone sales of approximately 169 million units in 2024, while smart speaker adoption is growing at over 22% CAGR due to multilingual voice assistant integration. Government initiatives such as India’s Production Linked Incentive schemes are encouraging local manufacturing and increasing component demand. Vietnam, Thailand, and Indonesia are emerging as cost-competitive production hubs that support regional supply chain diversification. Japan continues to lead in precision manufacturing and advanced material research, enabling high-performance membrane development. South Korea’s electronics leaders, including Samsung and LG, are driving demand for specialized membranes used in display-integrated audio systems. These combined factors create strong partnership and localization opportunities for membrane suppliers.

Category-wise Analysis

Material Type Insights

Polypropylene (PP) membranes account for approximately 42% of the global market share, making them the most widely used material type. Their dominance is supported by high durability, stable acoustic performance, and excellent resistance to temperature and humidity fluctuations. These characteristics make polypropylene membranes particularly suitable for automotive, outdoor, and portable audio applications. The material benefits from well-established supply chains and mature manufacturing processes, allowing producers to maintain cost competitiveness while ensuring consistent quality.

Polypropylene’s design flexibility also enables manufacturers to tailor membrane properties for different speaker sizes and performance requirements. It is widely used across applications ranging from smartphone micro-speakers to large automotive woofers. Additionally, advanced polypropylene composites reinforced with carbon fiber or ceramic particles are gaining traction. These enhanced variants bridge the performance gap between traditional polymers and metallic membranes, allowing suppliers to offer differentiated products for niche and high-performance audio segments.

Speaker Type Insights

Home audio systems continue to show strong growth, supported by rising consumer investment in smart and connected entertainment environments. Smart speaker adoption is expanding at nearly 20% CAGR as voice-controlled devices become standard household equipment. Streaming platforms such as Spotify, with over 615 million monthly active users, further drive demand for speakers that deliver consistent sound quality across music and voice functions. Premium home audio systems increasingly rely on advanced membrane materials that optimize full-spectrum frequency response.

Portable speakers represent the fastest-growing segment, driven by consumer preference for wireless, compact, and travel-friendly audio solutions. Bluetooth-enabled speakers are widely adopted for personal, outdoor, and social use. Automotive audio systems are also expanding at approximately 8.2% CAGR, particularly within electric vehicles. Quieter EV cabins enhance sound perception, motivating automakers to integrate premium audio systems that improve customer experience and strengthen brand differentiation.

Distribution Channel Insights

The Original Equipment Manufacturer (OEM) segment remains the dominant distribution channel in the speaker membrane market. OEM customers include smartphone manufacturers, automotive suppliers, consumer electronics producers, and professional audio equipment companies. These relationships offer long-term volume stability and predictable demand, although they require strict quality compliance, competitive pricing, and customized product specifications. The aftermarket segment is growing steadily as consumers upgrade audio systems in existing vehicles and home entertainment setups.

Demand is particularly strong for high-performance replacement membranes that offer better sound quality than factory-installed components. Online retail channels have also expanded rapidly, enabling direct-to-consumer sales of speaker components through e-commerce platforms. While this channel improves accessibility, it requires strong digital marketing and customer education due to the technical nature of products. Traditional distributors and wholesalers remain important in regional markets, especially within professional audio and automotive aftermarket segments where technical guidance influences purchasing decisions.

Regional Insights

North America Speaker Membrane Market Trends

North America holds a strong market position supported by high consumer spending, advanced manufacturing capabilities, and widespread adoption of premium audio technologies. The United States represents the largest single-country market due to strong demand for home entertainment systems, smart speakers, and automotive audio upgrades. Smart home penetration is high, with voice-controlled speakers becoming common across residential environments. Automotive manufacturers increasingly use premium sound systems as value-added features, particularly in luxury and electric vehicle segments.

The region also maintains a robust professional audio industry, with continuous demand from touring events, music production studios, broadcasting companies, and large venues. Strong innovation ecosystems and research capabilities support ongoing development of advanced acoustic technologies. Combined with a mature consumer base that prioritizes audio quality, North America remains a key hub for product innovation, early technology adoption, and premium membrane commercialization.

Europe Speaker Membrane Market Trends

Europe represents a mature and quality-driven speaker membrane market, characterized by strong demand for premium audio performance and sustainable manufacturing practices. Germany leads the regional market due to its advanced industrial base, strong automotive production, and well-established audio engineering heritage. The United Kingdom, France, and Spain also contribute significantly through consumer electronics demand, professional audio applications, and automotive aftermarket sales. European manufacturers operate under strict environmental regulations such as RoHS and REACH, which encourage the development of eco-friendly membrane materials and cleaner production processes.

Sustainability and material traceability are increasingly important in supplier selection. Smart home adoption continues to grow steadily, with consumers integrating voice-enabled speakers into daily routines. Automotive demand remains strong, particularly among luxury brands in Germany and Scandinavia, where premium audio systems are key differentiators and drive ongoing investment in advanced membrane technologies.

Asia Pacific Speaker Membrane Market Trends

Asia Pacific is the fastest-growing regional market, supported by rapid urbanization, rising electronics consumption, and large-scale manufacturing expansion. China dominates global production, accounting for more than 60% of smartphone manufacturing and generating demand for approximately 720 million speaker membranes annually from smartphones alone. Government initiatives promoting domestic innovation have encouraged both local and international brands to expand regional manufacturing operations.

India is emerging as a high-growth market, with smartphone sales reaching 169 million units in 2024 and smart speaker adoption rising rapidly due to regional language support. Japan continues to lead in precision engineering and advanced materials research, supporting high-end audio component development. South Korea drives innovation in display-integrated and compact audio systems through global brands such as Samsung and LG. While economic volatility and import duties pose challenges, strong fundamentals such as population growth and digital adoption support long-term regional expansion.

Competitive Landscape

The speaker membrane market is highly fragmented, with global manufacturers competing alongside specialized regional players. Companies such as Murata Manufacturing maintain strong market presence through advanced capabilities in electronic components, while Loudspeaker Components LLC focuses on customized acoustic solutions. Industry consolidation is gradually increasing, as demonstrated by B&C Speakers’ acquisition of Eminence Speaker during 2023–2024, forming an integrated global manufacturing network across the U.S., China, and Europe.

Manufacturers are increasingly adopting vertical integration strategies to control quality, reduce dependency on suppliers, and improve cost efficiency. Investment in research and development remains a key competitive factor, particularly in advanced material innovation. Technologies such as ORA Graphene Audio’s GrapheneQ membranes highlight growing emphasis on material science differentiation. Licensing models and regional partnerships are also gaining traction, enabling technology transfer while reducing capital investment. At the same time, stricter quality control standards are being implemented to ensure consistency across high-volume production.

Key Developments:

- In January 2024: B&C Speakers finalized the acquisition of Eminence Speaker LLC, integrating its U.S. and China manufacturing operations with a workforce of around 90 employees, expanding capacity for professional audio and automotive aftermarket membrane components under unified global production.

- In May 2025, at Prolight+Sound Guangzhou, B&C Speakers unveiled the Eminence Pro series, emphasizing global production capability across China, Europe, and the United States and featuring Italian-manufactured diaphragms integrated into consistent, internationally competitive professional audio specifications.

Companies Covered in Speaker Membrane Market

- Murata Mfg Co. Ltd

- Loudspeaker Components, LLC

- Dass & Company

- CX Technology Corporation

- Wizard India Pvt Ltd

- GuoGuang Electric Company Ltd

- Radian Audio Engineering Inc.

- Klippel GmbH

- Dr. Kurt Muller GmbH & Co, KG

- ORA Graphene Audio Inc.

- Falcon Acoustics UK

- Bestron USA Inc.

- Dayton Audio

- Eminence Speaker LLC

- Taixing Yangsheng Electronic Co Ltd

- AAC Technologies Holdings Inc.

- B&C Speakers

- Focal (Polyglass Technology)

- Bowers & Wilkins

- JL Audio

Frequently Asked Questions

The global speaker membrane market is projected to grow from US$ 4.2 billion in 2026 to US$ 6.9 billion by 2033 at a CAGR of 7.3%.

The market growth is driven by increase in smartphone shipments, rapid wireless audio adoption, expanding smart speaker usage, and increasing automotive infotainment demand.

Polypropylene membranes lead the market due to their durability, environmental resistance, cost efficiency, and broad suitability across audio applications.

North America leads the market supported by high consumer spending, premium audio adoption, and strong automotive and entertainment technology demand.

Graphene-enhanced and advanced composite membranes present major growth opportunities by delivering superior sound performance and enabling premium product differentiation.

Leading companies include Murata, Eminence Speaker, ORA Graphene Audio, Loudspeaker Components, and several global and regional acoustic component manufacturers.