- Specialty & Fine Chemicals

- Polymeric Membrane Market

Polymeric Membrane Market Size, Share, and Growth Forecast, 2026-2033

Polymeric Membrane Market by Product Type (Reverse Osmosis, Nanofiltration, Ultrafiltration, Microfiltration, Ion-Exchange Membranes, Gas Separation Membranes), Application (Water & Wastewater Treatment, Desalination, Food & Beverage, Pharmaceuticals, Chemical Processing, Oil & Gas, Energy & Hydrogen, Healthcare, Residential Water Purification), Material Type (Polyethersulfone, Polyvinylidene Fluoride, Polyacrylonitrile, Polypropylene, Polysulfone, Polyamide, Bio-based Polymers, Polymer Blends), and Regional Analysis for 2026-2033

Polymeric Membrane Market Share and Trends Analysis

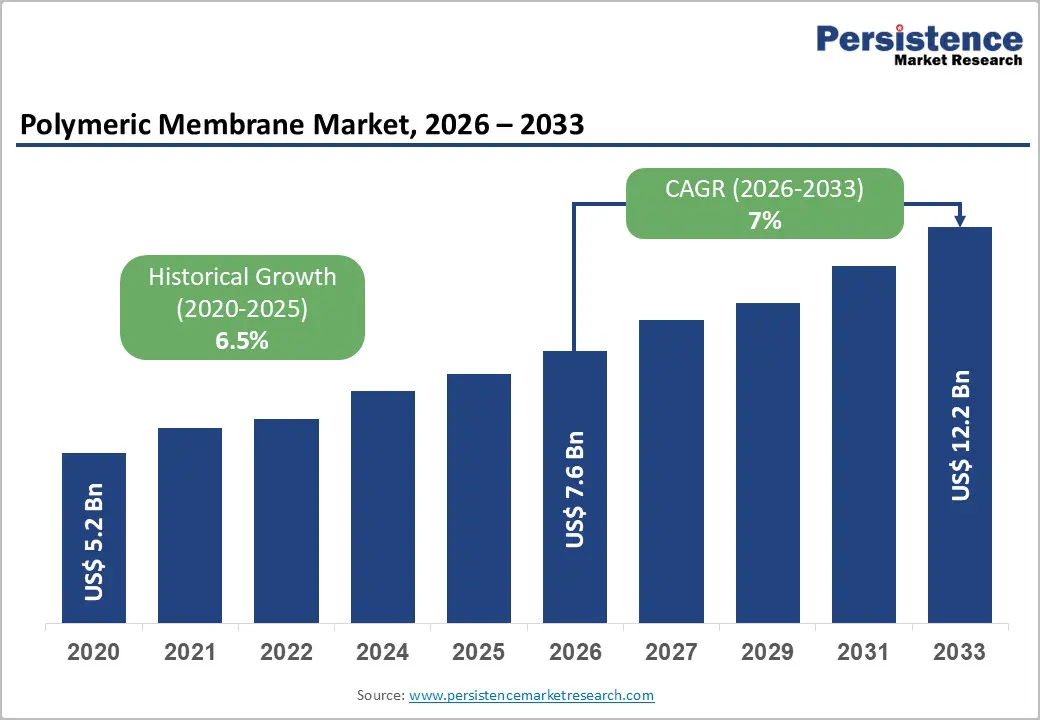

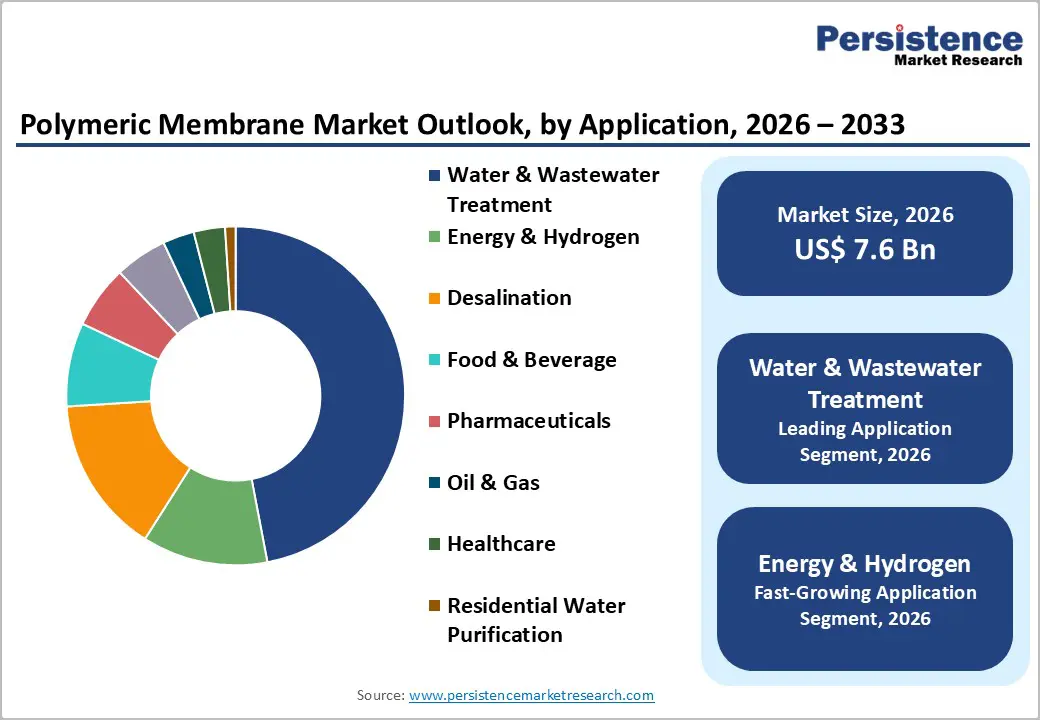

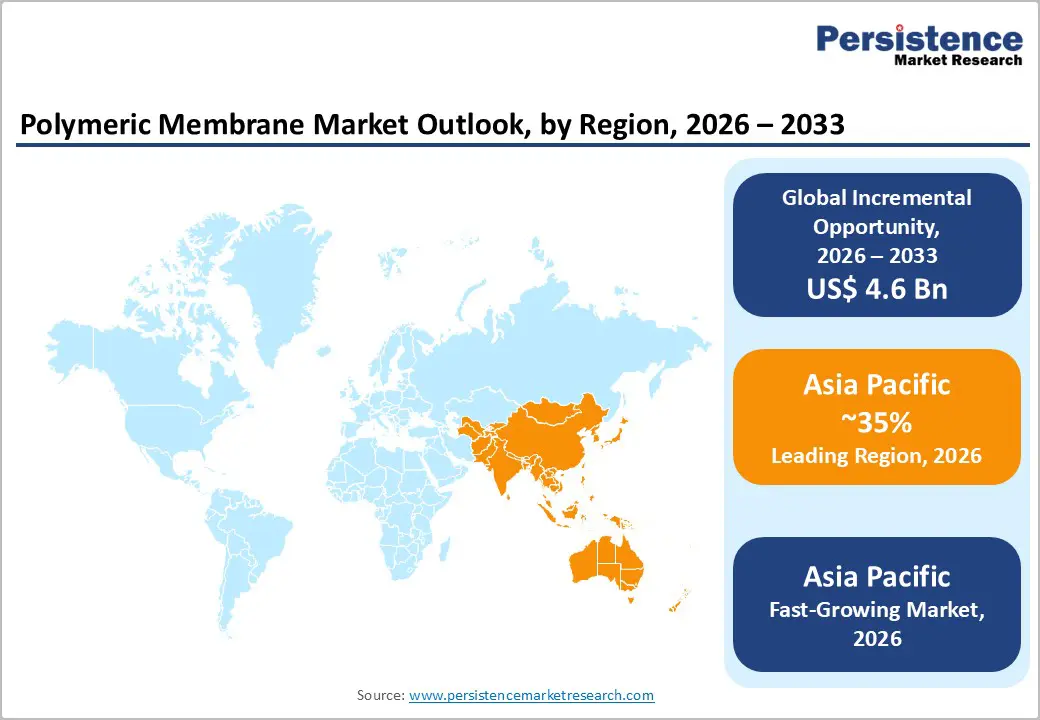

The global polymeric membrane market size is likely to be valued at US$ 7.6 billion in 2026, and is projected to reach US$ 12.2 billion by 2033, growing at a CAGR of 7% during the forecast period 2026–2033.

Steady expansion of water and wastewater treatment infrastructure across both developed and emerging economies is mainly driving market growth. Governments are increasing capital allocation toward upgrading aging municipal systems and deploying advanced treatment technologies to meet stricter potable water and discharge standards. Rising investments in desalination technologies, particularly in water-stressed regions, are accelerating demand for high-efficiency reverse osmosis membranes. Expanding pharmaceutical manufacturing and bioprocessing capacity requires high-performance filtration systems to ensure product purity. The regulatory tightening on industrial effluents, alongside growth in hydrogen production and gas separation applications, is reinforcing long-term adoption of advanced membrane solutions.

Key Industry Highlights

- Dominant Product Types: Reverse osmosis membranes are set to command around 39% revenue share in 2026, while gas separation membranes are likely to grow the fastest at through 2033, supported by hydrogen and carbon capture deployment.

- Leading Applications: Water & wastewater treatment is projected to hold nearly 47% share in 2026, while energy & hydrogen applications are expected to expand at about 9.5% CAGR during 2026–2033, reflecting decarbonization investments.

- Material leadership: Polyvinylidene fluoride (PVDF) is anticipated to account for close to 32% of market share in 2026, whereas bio-based polymers are forecast to grow the fastest through 2033, aligned with sustainability regulations.

- Regional Leadership: Asia Pacific is poised to capture approximately 35% of global revenue in 2026 and register around 8.3% CAGR through 2033, driven by industrialization and desalination capacity additions.

- Competitive Environment: Industry participants are increasing capacity and allocating a considerable portion of their annual revenues to R&D, focusing on energy-efficient and low-fouling membrane technologies.

| Key Insights | Details |

|---|---|

| Polymeric Membrane Market Size (2026E) | US$ 7.6 Bn |

| Market Value Forecast (2033F) | US$ 12.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Water Stress and Accelerated Infrastructure Investment

According to the UN, over 2 billion people live in countries experiencing high water stress, and global water demand is projected to increase by approximately 20–30% by 2050. The World Bank (WB) estimates that billions of dollars are invested annually in water infrastructure upgrades, particularly in emerging economies. In 2025, the U.S. Department of Energy (DOE) announced a US$ 25 million initiative to extract critical minerals from wastewater streams, reinforcing federal commitment to advanced treatment technologies. These policy-backed investments signal that wastewater is increasingly viewed as a recoverable resource rather than waste. Infrastructure modernization is therefore expanding both primary membrane installations and replacement demand cycles.

This macro trend directly accelerates adoption of reverse osmosis (RO) and ultrafiltration (UF) membranes for municipal and industrial water treatment systems. Governments are mandating wastewater recycling targets, increasing membrane replacement cycles and boosting long-term recurring revenues for manufacturers. In 2025, industry coverage highlighted accelerated deployment of decentralized wastewater systems across urbanizing regions, further strengthening membrane demand in modular treatment units. Desalination projects in water-scarce regions continue to scale, embedding RO systems as foundational infrastructure assets. As public utilities transition toward reuse-focused frameworks, membrane systems are becoming integral to long-term water security strategies.

Regulatory Compliance Expansion and Energy Transition Deployment

The International Energy Agency (IEA) reports sustained growth in global industrial output, particularly in Asia-Pacific. Simultaneously, environmental authorities such as the U.S. Environmental Protection Agency have strengthened discharge norms under the Clean Water Act, tightening permissible contaminant thresholds. These regulatory developments are compelling industries to adopt higher-efficiency microfiltration, nanofiltration, and ion-exchange membranes. In 2025, leading news coverage reported rising investments in gas separation infrastructure across the United States, Europe, and Asia to improve CO2 management efficiency. Compliance-driven upgrades are increasingly linked to corporate decarbonization commitments and ESG reporting frameworks.

The International Renewable Energy Agency highlights that global electrolyzer capacity is expanding rapidly to support green hydrogen production. Proton exchange membrane (PEM) electrolyzers depend on specialized polymer membranes for efficient ion transport. In 2026, peer-reviewed scientific publications emphasized advancements in polymer-based CO2 separation materials, signaling accelerated R&D activity aligned with carbon capture goals. Gas separation membranes are also being integrated into biogas upgrading and industrial hydrogen purification systems. This convergence of environmental regulation and energy transition investment is diversifying membrane demand beyond water treatment. As hydrogen projects scale through 2033, advanced gas separation and ion-exchange membranes are positioned to outperform overall market growth.

Membrane Fouling, Performance Degradation, and Rising Operating Costs

Membrane fouling reduces system efficiency and increases operational costs. Industry associations such as the American Water Works Association (AWWA) emphasize that fouling remains a leading cause of plant downtime. Replacement cycles every 3–7 years represent significant lifecycle costs for operators. In 2026, a news coverage highlighted that membrane cleaning and fouling management can account for 15–25% of total operating expenditure in advanced water treatment facilities. Organic and biological fouling continues to reduce permeate flux and increase energy consumption. These recurring efficiency losses reinforce lifecycle cost pressures across municipal and industrial plants.

High-performance polymeric membranes require pretreatment systems and chemical cleaning, increasing total cost of ownership. For cost-sensitive municipalities and small industrial units, these capital and operating expenditures can delay procurement decisions, limiting short-term adoption in developing regions. Technical bulletins published in 2025 industry analysts noted continued operational concerns around membrane system maintenance and chemical usage in high-load industrial environments. Frequent chemical cleaning can also shorten membrane lifespan if not carefully managed. Skilled technical oversight is necessary to maintain consistent system efficiency. These operational complexities remain a structural constraint despite strong long-term demand fundamentals.

Raw Material Price Volatility and Petrochemical Supply Risks

Polymeric membranes rely on specialty polymers such as polyethersulfone and polyvinylidene fluoride. Price volatility in petrochemical feedstock, influenced by global crude oil trends reported by the U.S. Energy Information Administration, impacts manufacturing margins. In 2025, discussions at the Asia Pacific Petroleum Conference highlighted procurement caution among petrochemical producers amid fluctuating crude benchmarks and trade tensions. Feedstock price swings directly affect resin costs used in membrane fabrication. This volatility reduces pricing stability across long-term supply agreements. Margin sensitivity is therefore elevated during periods of raw material instability.

Supply chain disruptions and geopolitical tensions can constrain polymer availability, leading to procurement risks. Industry news coverage throughout late 2025 emphasized cautious sourcing strategies among Asian petrochemical producers due to cross-border trade uncertainties. Smaller manufacturers face margin pressure, potentially limiting R&D investments and slowing innovation cycles. Extended lead times for specialty resins can delay project execution schedules for large water and industrial installations. In competitive tenders, cost unpredictability weakens pricing confidence. These structural supply risks create uncertainty across the value chain and may temper near-term capacity expansion decisions.

Desalination Scale-Up and Industrial Water Reuse Expansion

The International Desalination Association (IDA) reports steady capacity additions in the Middle East and Asia that reflect a strategic shift toward large-scale desalination deployment. In late 2025, Toray’s membrane fabrication facility in Saudi Arabia began integrated operations to support regional desalination needs, marking increased upstream investment in membrane supply capacity. Governments in arid regions are elevating water security as industrial policy, with planned capacity expansions expected to increase reverse osmosis utilization across municipal and industrial projects. This reinforces membrane demand as foundational to long-term water infrastructure.

Given desalination’s dependence on reverse osmosis membranes, the segment offers multi-billion-dollar addressable opportunities through 2033. Major national projects such as the Jordan desalination initiative, backed by international financial institutions and designed to serve millions of people, are progressing toward construction, signaling strong near-term procurement pipelines. Policymakers are advancing public-private partnership models that encourage technology upgrades and shared financing for membrane systems. Industrial water reuse initiatives in centers of manufacturing growth are also expanding, integrating tertiary treatment with reuse targets. These intertwined drivers support sustained demand for high-flux polymeric membranes across water reuse and desalination applications.

Sustainable Materials Innovation and High-Purity Water Demand

Sustainability policies across major economies are increasingly promoting circular materials and reduced carbon footprints, creating demand for green membrane technologies. In late 2025, research developments highlighted next-generation membranes engineered for energy-efficient water purification and inherent biodegradability, supporting the transition toward eco-friendly separation systems. These scientific and policy signals suggest momentum for low-impact and sustainable polymeric materials that align with environmental compliance. Regulatory agencies are prioritizing reduced environmental liabilities for end-of-life membrane disposal as part of broader circular economy frameworks.

Global semiconductor expansion, supported by initiatives such as the U.S. CHIPS Act, is driving demand for ultrapure water used in fabrication processes, which relies on high-rejection nanofiltration and reverse osmosis membranes. With semiconductor fabs expanding capacity across Asia and North America, demand for precision membrane modules is consistently linked to fab lifecycle upgrades. High-purity water requirements are tied to yield optimization in semiconductor manufacturing and technology supply chain localization policies. Together, sustainability innovation and high-purity water use cases create a high-margin growth corridor for advanced polymeric membranes through 2033.

Category-wise Analysis

Material Type Insights

Polyvinylidene fluoride (PVDF) is estimated to lead with approximately 32% of the polymeric membrane market revenue share in 2026. Its dominance is expected to remain supported by strong chemical resistance and long operational lifespan in harsh environments. In 2025, expansion updates from Middle Eastern petrochemical facilities reported by Arab News indicated continued investment in high-durability membrane systems for brine treatment and industrial reuse. Such developments suggest sustained reliance on PVDF-based ultrafiltration and microfiltration modules. Industrial wastewater recycling and desalination pretreatment applications are anticipated to further reinforce material demand. These structural advantages are likely to maintain PVDF’s leadership over the forecast horizon.

Bio-based polymers are projected to be the fastest-growing material types, expected to expand at an estimated 8.8% CAGR through 2033. Sustainability mandates and circular economy strategies are likely to accelerate research commercialization. In 2025, innovation funding initiatives aligned with European environmental policy frameworks were reported by European Commission, supporting development of low-carbon and bio-derived industrial materials. Early-stage pilot programs focused on renewable polymer chemistry are anticipated to gradually transition toward commercial membrane applications. As environmental compliance criteria tighten, demand for sustainable material alternatives is expected to increase. This evolving shift may create premium growth avenues within the broader membrane materials landscape.

Application Insights

Water & wastewater treatment is expected to remain the leading application, estimated to account for approximately 47% of the polymeric membrane market share in 2026. Growth is likely to be supported by continued regulatory enforcement and infrastructure modernization initiatives. In 2025, the United States Environmental Protection Agency announced additional funding allocations under national water infrastructure programs aimed at upgrading filtration systems to meet stricter contaminant standards. Such policy-backed investments are expected to accelerate membrane retrofit cycles across municipal facilities. Industrial wastewater compliance requirements are also anticipated to reinforce steady procurement activity. Replacement demand and capacity expansion projects together are likely to sustain this segment’s dominant position.

Energy & hydrogen is poised to be the fastest-growing application, anticipated to register around 9.5% CAGR through 2033. Clean hydrogen deployment strategies across Europe and Asia are expected to increase integration of membrane-based gas purification systems. In 2026, policy updates linked to hydrogen infrastructure expansion under Germany’s national hydrogen roadmap were reported by Reuters, indicating continued public funding support for electrolyzer capacity scale-up. Carbon capture and industrial decarbonization clusters are also likely to incorporate advanced membrane separation technologies. As hydrogen production scales commercially, technology-intensive filtration systems are expected to see rising demand. This positions the segment as a structurally high-growth application area over the forecast period.

Regional Insights

Asia Pacific Polymeric Membrane Market Trends

Asia Pacific is projected to be both the leading and fastest-growing regional market for polymeric membranes, anticipated to hold nearly 36% of global revenue share in 2026, while expanding at an approximate 2026-2033 CAGR of 9.8%. Strong policy-backed infrastructure investment across China, India, and Japan continues to accelerate membrane deployment. In 2025, the Ministry of Water Resources of the People's Republic of China (PRC) announced expanded funding for wastewater recycling and river basin restoration projects, reinforcing long-term filtration demand. Rapid urbanization and industrial expansion are increasing freshwater treatment requirements. Government-supported desalination capacity additions are further enlarging the installed membrane base. These structural drivers position the region at the forefront of global market growth.

Industrial diversification is expected to further strengthen momentum. In 2026, infrastructure financing updates reported by Nikkei Asia highlighted increased coastal desalination and advanced treatment investments across major Asian economies. Expanding semiconductor and pharmaceutical manufacturing hubs are projected to elevate high-purity filtration requirements. Cost-competitive production ecosystems enable regional manufacturers to scale exports while serving domestic demand. Environmental compliance enforcement is gradually tightening across emerging economies. Public-private partnership models are accelerating technology adoption. These factors are likely to sustain Asia Pacific’s leadership and high-growth trajectory through the forecast period.

North America Polymeric Membrane Market Trends

North America remains a strategically significant market for polymeric membranes, supported by regulatory enforcement and technological advancement. Federal oversight by the U.S. DOE in 2025 expanded funding initiatives linked to hydrogen commercialization and industrial decarbonization, indirectly reinforcing advanced membrane applications. Municipal water utilities are expected to continue upgrading aging infrastructure to meet evolving contaminant standards. Replacement demand remains a stable revenue contributor across established installations. Industrial wastewater compliance requirements further strengthen procurement visibility. These factors collectively maintain North America’s strong and innovation-driven profile.

High-value manufacturing expansion is also expected to support steady demand. In 2026, fabrication plant developments reported by The Wall Street Journal indicated continued semiconductor capacity buildouts in the United States, increasing reliance on ultrapure water systems. Advanced gas separation membranes are projected to gain traction in hydrogen and carbon capture applications. Strong R&D ecosystems and university–industry collaboration networks foster continuous innovation. Established domestic suppliers enhance supply chain resilience. While growth may be comparatively moderate, the region is likely to remain technologically influential and commercially important.

Europe Polymeric Membrane Market Trends

Europe continues to demonstrate stable demand conditions, largely shaped by regulatory alignment and sustainability priorities. In 2025, the European Environment Agency emphasized stricter wastewater monitoring and nutrient discharge compliance across member states, reinforcing advanced treatment requirements. Industrial water reuse programs in Germany, France, and the United Kingdom are expected to sustain membrane procurement. EU sustainability mandates continue to prioritize lifecycle efficiency and low-emission technologies. Compliance-driven infrastructure upgrades remain a consistent market catalyst. These regulatory frameworks create a structured and predictable demand environment.

Southern Europe is anticipated to contribute incremental expansion through desalination and drought resilience initiatives. In 2026, funding developments reported by BBC News highlighted Spain’s renewed investments in desalination modernization projects. Mediterranean economies are projected to expand advanced filtration capacity to mitigate water scarcity risks. Harmonized standards across the European Union streamline cross-border technology adoption. Public tenders increasingly emphasize environmental performance criteria. Although growth rates may be moderate relative to Asia Pacific, Europe is likely to remain a stable and sustainability-driven regional market.

Competitive Landscape

The global polymeric membrane market structure is moderately consolidated, with major players such as DuPont, Toray Industries, SUEZ, and Hydranautics holding a significant combined revenue share. These companies leverage established municipal and industrial relationships, vertically integrated production capabilities, and broad product portfolios across reverse osmosis, ultrafiltration, and nanofiltration technologies. Continuous investment in material innovation, fouling resistance, and energy-efficient designs supports their competitive positioning. Strong aftermarket services and replacement demand further enhance recurring revenue stability.

Regional and specialized competitors such as LG Chem and Koch Separation Solutions focus on application-specific solutions and geographic expansion. High capital requirements, certification standards, and technical validation processes create entry barriers for new players. However, increasing integration of digital monitoring and performance optimization tools is enabling collaboration with technology-driven firms. Strategic partnerships and selective acquisitions are expected to gradually intensify consolidation. Sustainability-focused innovation is likely to become a key differentiator over the forecast period.

Key Industry Developments

- In October 2025, ACCIONA introduced a state-of-the-art AI platform at its desalination facility in Qatar, integrating simulation tools and machine learning to optimize reverse osmosis operations. The deployment significantly enhances energy efficiency, real-time performance monitoring, and membrane lifecycle management.

- In October 2025, Membrane Group India secured a US$ 50 million investment commitment from GEF Capital’s South Asia Growth Fund III to expand advanced water and wastewater membrane solutions. The funding supports scaling of project execution, R&D expansion, and resource recovery technologies, indicating strong financial backing for polymeric membrane innovation.

- In May 2025, India’s Defence Research and Development Organisation (DRDO) announced the development of an indigenous high-pressure nanoporous polymeric membrane designed for seawater desalination under extreme conditions. The breakthrough strengthens India’s domestic membrane manufacturing capabilities while improving durability and performance efficiency.

Companies Covered in Polymeric Membrane Market

- DuPont

- Toray Industries

- SUEZ

- LG Chem

- Hydranautics

- Koch Separation Solutions

- Pall Corporation

- Asahi Kasei

- 3M

- Pentair

- Mitsubishi Chemical Group

- Toyobo

Frequently Asked Questions

The global polymeric membrane market is projected to reach US$ 7.6 billion in 2026.

Rising investments in water treatment infrastructure, desalination expansion, industrial wastewater compliance, and hydrogen production are driving market growth.

The market is poised to witness a CAGR of 7% from 2026 to 2033.

Desalination capacity expansion, sustainable bio-based membrane innovation, and high-purity water demand from semiconductor and hydrogen industries present major opportunities.

DuPont, Toray Industries, SUEZ, and LG Chem are some of the key players in the market.