- Advanced Materials

- Global Expansion Vessel Membrane Market

Global Expansion Vessel Membrane Market Size, Share, and Growth Forecast 2026 - 2033

Expansion Vessel Membrane Market by Membrane Type (Diaphragm Membrane, Bladder Membrane), Material Type (EPDM Rubber, Butyl Rubber, NBR / HNBR (Nitrile Rubber), Application (Heating Systems, HVAC & Cooling Systems, Domestic/Potable Water Systems, Industrial Process Systems), and Regional Analysis, 2026–2033

Global Expansion Vessel Membrane Market Size and Trend Analysis

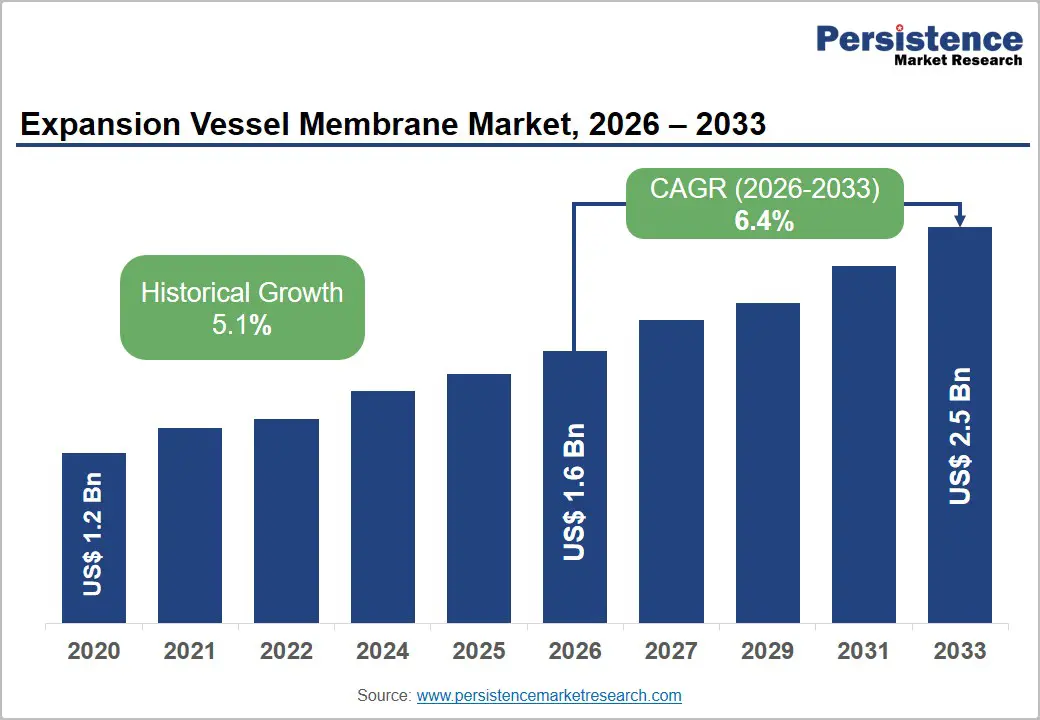

The global expansion vessel membrane market size, is expected to be valued at US$ 1.6 billion in 2026 and projected to reach US$ 2.5 billion, growing at a CAGR of 6.4% between 2026 and 2033. This steady growth is underpinned by the non-negotiable role of expansion vessel membranes as safety-critical pressure management components across heating, HVAC, and potable water systems applications, whose installation base is structurally expanding with global construction activity, building retrofit programs, and energy efficiency mandates.

Europe’s stringent building energy performance requirements under EU Directive 2024/1275 (recast EPBD) are compelling mass-scale hydronic heating system upgrades across the continent’s residential and commercial building stock, while Asia Pacific’s urbanization-driven construction boom and infrastructure formalization are generating new installation demand for pressure management components across district heating, potable water, and industrial fluid systems that require certified expansion vessel membranes at every installation point.

Key Industry Highlights:

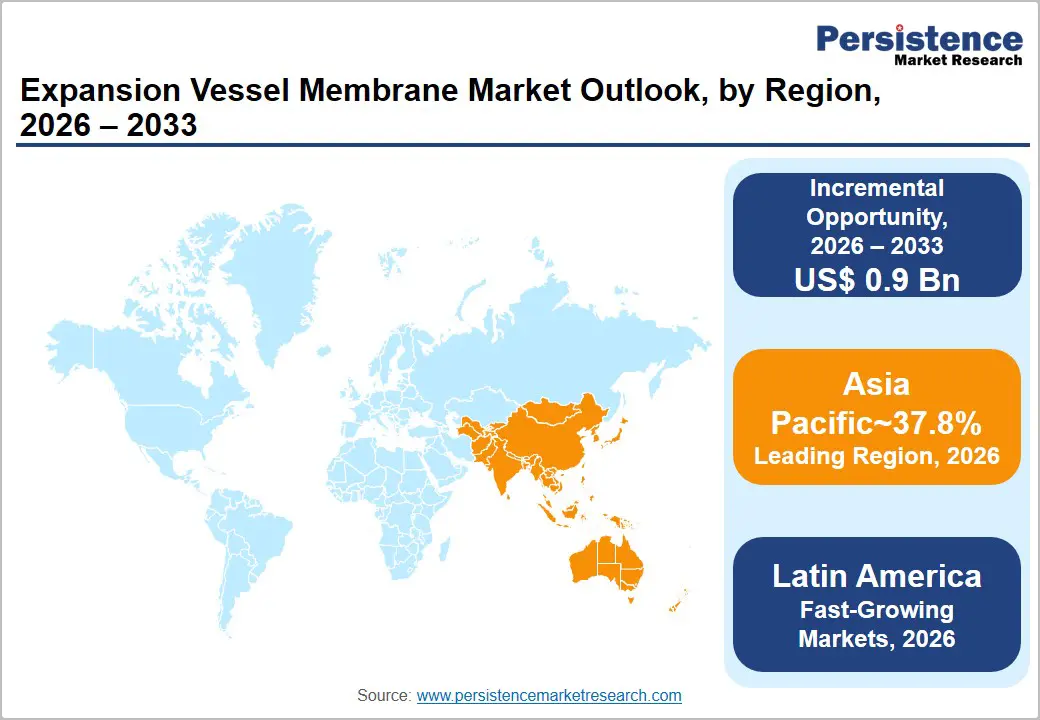

- Leading Region: Asia Pacific leads the global expansion of the vessel membrane market with 41.8% market share in 2026, anchored by China’s 10 billion m² district heating network per CDHA data and India’s NCAP-driven HVAC sector formalisation, generating commercial building hydronic system expansion vessel demand.

- Fast-Growing Market: Asia Pacific is also the fastest growing region with India’s US$ 132.7M market driven by ISHRAE-documented HVAC commercial construction penetration doubling, China’s 14th Five-Year Plan district heating extension, and South Korea’s G-SEED green building standards driving hydronic system adoption.

- Dominant Membrane Type: Diaphragm Membranes command approximately 63% market share in 2026, underpinned by their EN 13831 standard qualification as the default configuration in residential and light commercial expansion vessels across Europe’s 100+ million installed heating system base and North American retrofit markets.

- Fast-Growing Membrane Type: Bladder Membranes represent the fastest growing type at 7% CAGR driven by WRAS, KTW, and NSF/ANSI 61 potable water certification requirements, solar thermal pressurised system adoption, and industrial process fluid expansion vessel demand, where bladder design prevents waterlogging.

- Key Opportunity: Europe’s EPBD 2024/1275-driven building renovation wave mandating 55% GHG reduction by 2030, combined with Germany’s GEG 2024 heat pump mandate and France’s MaPrimeRénov’ €5 billion+ annual retrofit program, represents a concentrated membrane replacement and new installation opportunity through 2033.

DRO Analysis

Drivers - Building Retrofit Mandates and Hydronic System Upgrades Driving Membrane Replacement Cycles

European and North American building decarbonization policies are compelling the systematic replacement and upgrade of hydronic heating systems across tens of millions of existing buildings, directly generating membrane demand through new installation and replacement cycles. The EU Energy Performance of Buildings Directive (EPBD 2024/1275) mandates that all buildings reach minimum energy performance standards, with EU member states required to develop national building renovation plans targeting 55% reduction in GHG emissions by 2030. Heat pump retrofits for which expansion vessels with compatible membranes are mandatory, pressure management components are central to the European heating decarbonization strategy.

The European Heat Pump Association (EHPA) reported heat pump sales surpassing 3 million units in Europe in 2022, each requiring expansion vessel membrane-equipped systems, creating consistent demand for EPDM and butyl rubber membrane components across EU retrofit and new-build markets.

Global Construction Output Sustaining New Vessel Membrane Installation Demand

Global construction activity remains a fundamental contributor to expansion vessel membrane demand, as every new hydronic heating, HVAC, potable water pressurisation, and industrial process fluid system installation requires pressure management vessels fitted with certified membranes. The Global Construction Perspectives and Oxford Economics’ Global Construction 2030 report projected global construction output to reach US$ 15.5 trillion by 2030, with Asia Pacific led by China and India accounting for over 57% of new construction value.

In residential and commercial construction, hydronic heating systems are standard in Northern and Central European climates, while district heating network expansion in China, South Korea, and Eastern Europe is generating bulk installation demand for expansion vessels across large-scale fluid distribution infrastructure projects, each requiring membrane-fitted vessels at multiple pressure regulation points throughout the network.

Restraints - Competition from Stainless Steel Diaphragm Vessels and Maintenance-Free Tank Technologies

Expansion vessel membrane products face competitive pressure from diaphragm-free stainless steel expansion tanks and closed-cell foam expansion systems in specific application segments, particularly industrial process fluid and domestic hot water applications in regions with high water quality standards. Non-membrane expansion technologies, which eliminate the periodic membrane replacement service requirement, are preferred by facility managers seeking reduced lifecycle maintenance costs in high-temperature or chemically aggressive fluid environments where rubber membrane durability is a concern, moderating membrane product revenue growth in premium industrial application sub-segments.

Rubber Material Price Volatility and Supply Chain Disruptions

Expansion vessel membranes manufactured from EPDM (Ethylene Propylene Diene Monomer), butyl rubber, and nitrile rubber (NBR/HNBR) are directly exposed to petroleum-derived synthetic rubber feedstock price volatility. EPDM rubber prices are correlated with ethylene and propylene monomer supply conditions, which experienced a significant cost rise between 2021 and 2023 petrochemical cycle. These material cost fluctuations compress membrane manufacturer margins and create procurement planning uncertainty for expansion vessel OEMs and aftermarket distributors, particularly during periods of concurrent raw material cost pressure and competitive market pricing that limit cost pass-through to customers in price-sensitive OEM supply agreements.

Opportunities - Bladder Membrane Segment: Fastest Growing Type Through High-Pressure and Potable Water Certification Demand

Bladder membranes represent the fastest growing membrane type in the expansion vessel membrane market at 7% CAGR over 2026–2033, driven by their superior pressure containment performance in high-pressure potable water systems, industrial process fluid applications, and solar thermal pressurised systems, where bladder design prevents water-to-gas contact and avoids waterlogging degradation.

Regulatory certifications, including WRAS (Water Regulations Advisory Scheme) in the U.K., KTW Guideline in Germany, and NSF/ANSI 61 in the U.S., mandate potable water contact-approved materials for expansion vessel membranes in drinking water system applications. Certifications that bladder designs meet more efficiently than conventional diaphragm configurations. The global expansion of pressurised solar thermal and heat pump hot water systems creates a growing bladder membrane demand base across all major geographies.

Asia Pacific Smart Building and District Heating Infrastructure Generating Membrane Procurement Demand

Asia Pacific’s combination of urbanisation-driven construction and infrastructure formalisation is creating the largest regional incremental demand base for expansion vessel membranes over the forecast period. China’s 14th Five-Year Plan specifically allocates investment to district heating network extension across northern provincial cities, with China’s district heating network covering approximately 10 billion m² of floor space per China District Heating Association (CDHA) data, each requiring expansion vessel installations throughout the distribution infrastructure.

India’s HVAC market is formalising rapidly, with ISHRAE (Indian Society of Heating, Refrigerating and Air Conditioning Engineers) reporting above-average HVAC system adoption in commercial construction, generating expansion vessel membrane demand across closed-loop cooling system applications. South Korea’s mandatory Green Building Certification (G-SEED) standards and Japan’s ZEB (Zero Energy Building) policy incentives are similarly driving hydronic system adoption that anchors membrane component procurement.

Category-wise Analysis

Membrane Type Insights

Diaphragm membranes dominate the expansion vessel membrane market by membrane type, commanding approximately 63.4% of share in 2026. Diaphragm-type membranes which are permanently fixed to the vessel interior and flex under pressure differential are the standard configuration in the majority of residential and light commercial hydronic heating, HVAC, and potable water expansion vessels due to their simpler manufacturing process, lower unit cost relative to replaceable bladder designs, and compatibility with the predominant small-to-medium vessel sizes (2–50 liters) installed in single-family and multi-family residential buildings.

EN 13831:2007 (the European standard for closed expansion vessels with diaphragm or bladder for installations) and PED 2014/68/EU (Pressure Equipment Directive) certification requirements apply to both membrane types, but diaphragm vessels have historically achieved faster OEM qualification timelines, sustaining their majority market share across European and North American standard residential heating applications.

Material Type Insights

EPDM (Ethylene Propylene Diene Monomer) rubber represents the dominant material type in the expansion vessel membrane market, holding around 46.8% share in 2026, accounting for the largest share of membrane production volumes globally. EPDM’s leadership is attributable to its exceptional resistance to water, steam, and glycol-water heat transfer fluids, the standard working fluids in hydronic heating systems, combined with a broad operating temperature range capability (−50°C to +150°C), excellent ozone and UV resistance, and proven long-service-life performance in pressurised closed-loop systems.

DIN EN 681-1 and EN 13831 standard references confirm EPDM’s established material qualification status in European hydronic system applications. Leading membrane manufacturers, including Reflex Winkelmann GmbH, Zilmet S.p.A., and Flamco BV, supply EPDM-membrane-equipped expansion vessels as their standard product configurations across the majority of their residential and commercial heating portfolios.

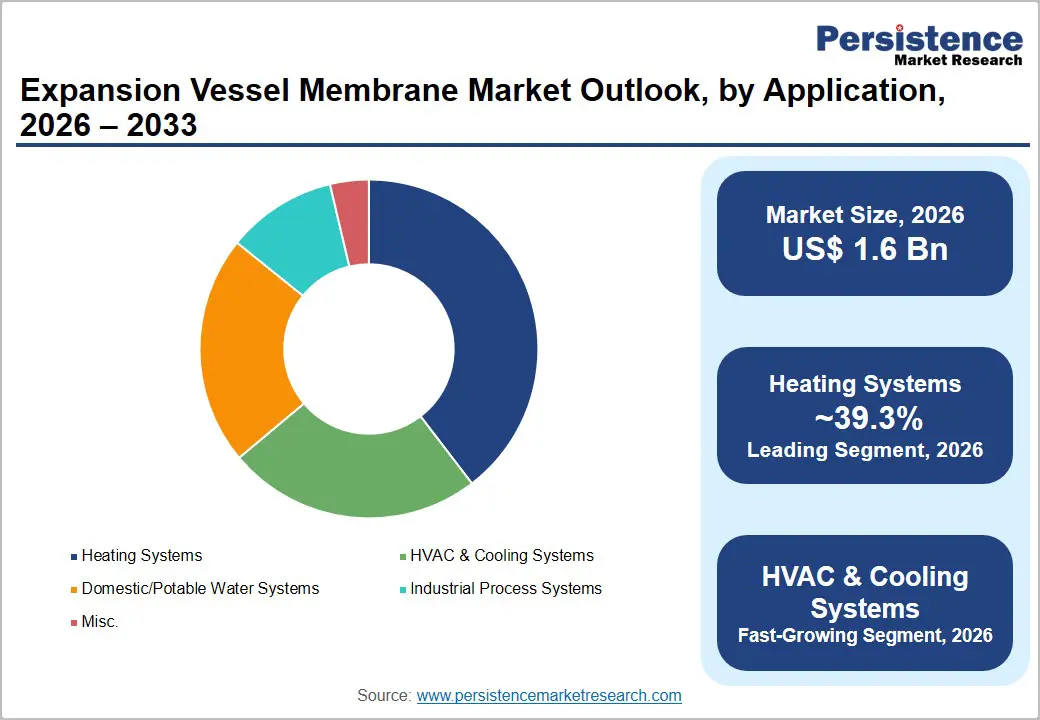

Application Insights

Heating systems represent the dominant application segment in the expansion vessel membrane market, holding a share of around 39.6% in 2026, accounting for the largest share of membrane demand globally. Closed-loop hydronic heating systems in which water or glycol-water mixtures are circulated through boilers, heat pumps, or solar thermal collectors and radiator/underfloor distribution networks require expansion vessels to safely accommodate thermal pressure changes during system heating cycles. EN 12828:2012+A1:2014 (European standard for heating systems in buildings) mandates expansion vessel sizing and specification as a fundamental safety requirement in all closed-loop hydronic heating system designs.

The European Boiler and Burner Association (EHI) data confirms that Europe’s installed base of over 100 million heating systems generates both replacement membrane demand and new installation volume, with heat pump retrofit programs continuously adding new expansion vessel installations requiring EPDM or butyl rubber membrane-fitted components.

Regional Insights

North America Expansion Vessel Membrane Market Trends and Insights

North America holds approximately 18.6% of the global expansion vessel membrane market in 2026, characterised by a mature installed base of hydronic heating systems in the Northeastern U.S. and Canadian residential and commercial buildings, active replacement membrane demand from aging system infrastructure, and accelerating heat pump retrofit adoption under the U.S. Inflation Reduction Act’s residential energy efficiency tax credits that are driving new expansion vessel installations across cold-climate states.

U.S. Expansion Vessel Membrane Market Size

The U.S. expansion vessel membrane market was valued at approximately US$ 242.2 million in 2026, underpinned by the U.S. Department of Energy’s (DOE) heat pump water heater and hydronic heat pump incentive programs under IRA Section 25C that generated over 10 million heat pump tax credit claims in 2023 alone. Each heat pump retrofit into a closed-loop hydronic system mandates expansion vessel replacement or new installation with certified EPDM or butyl membranes, driving consistent replacement and new-build membrane demand across New England, the Mid-Atlantic, and Pacific Northwest contractor markets.

Europe Expansion Vessel Membrane Market Trends and Insights

Europe holds the second-largest regional share at approximately 29.4% of the global expansion vessel membrane market in 2026, driven by the continent’s highest hydronic heating system density globally, mandatory EN 13831 and PED 2014/68/EU compliance for all expansion vessel products, and the EPBD recast 2024/1275-driven building renovation wave that is generating systematic expansion vessel replacements and new installations across 27 EU member state building stock upgrades. Germany, France, Italy, and Poland are the highest-volume national markets, reflecting their large installed bases of hydronic heating systems.

Germany Expansion Vessel Membrane Market Size

Germany’s expansion of the vessel membrane market was valued at approximately US$ 95.3 million in 2026, anchored by the Bundesförderung für effiziente Gebäude (BEG) subsidy program funding heat pump and hydronic system retrofits across German residential buildings.

Germany’s Gasänderungsgesetz (GEG 2024) mandating a minimum 65% renewable energy share in new heating systems from 2024 has driven a structural shift toward heat pump-coupled hydronic systems, each requiring expansion vessel membrane replacement, generating above-EU-average membrane procurement volumes across German plumbing and heating wholesalers.

France Expansion Vessel Membrane Market Size

France’s expansion vessel membrane market was valued at approximately US$ 69.7 million in 2026, driven by the MaPrimeRénov’ energy renovation subsidy program, which allocated over €5 billion in 2023 to residential heating system upgrades, including heat pump installations and RT 2020 (Réglementation Environnementale 2020) requirements mandating high-efficiency hydronic systems in new construction.

French ATG (Avis Technique Général)-certified expansion vessels using EPDM membranes are the specification standard across French plumbing and heating contractors, sustaining consistent demand from both retrofit and new construction channels.

Asia Pacific Expansion Vessel Membrane Market Trends and Insights

Asia Pacific holds the largest regional share of the global expansion vessel membrane market at approximately 41.8% in 2026, driven by China’s world-scale district heating network, India’s formalising HVAC sector, and South Korea and Japan’s advanced hydronic building system markets. China’s district heating infrastructure, covering approximately 10 billion m² of floor space per CDHA data, generates consistent bulk expansion vessel procurement across state-owned heat supply enterprises, while China’s residential construction pipeline sustains new installation membrane demand.

China Expansion Vessel Membrane Market Size

China’s expansion of the vessel membrane market was valued at approximately US$ 192.2 million in 2026, driven by China’s 14th Five-Year Plan district heating network extension targeting an additional 1.5 billion m² of heated floor space across northern Chinese cities. GB 12137-2015 (China’s national standard for pressure vessels, including expansion tanks) and CJ/T 193 specifications govern membrane material certifications for Chinese utility and construction procurement, with domestic suppliers including Amtrol China and regional manufacturers competing against European brands at scale.

India Expansion Vessel Membrane Market Size

India’s expansion vessel membrane market is likely to be valued at approximately US$ 132.7 million in 2026, reflecting rapid HVAC sector formalisation driven by India’s National Cooling Action Plan (NCAP) targeting a 20–25% reduction in cooling energy demand by 2037–38. India’s commercial construction boom, with HVAC penetration in commercial buildings doubling between 2019 and 2024 per ISHRAE data, is integrating closed-loop HVAC systems requiring expansion vessel membrane components across hospital, hotel, IT park, and data center construction projects at an unprecedented scale.

Competitive Landscape

The global expansion vessel membrane market is moderately consolidated, with European membrane and expansion vessel manufacturers holding dominant technical and commercial positions globally through established EN 13831 and PED certification infrastructure. Flamco BV (Netherlands), Reflex Winkelmann GmbH (Germany), Zilmet S.p.A. (Italy), Varem S.p.A. (Italy), and Calpeda S.p.A. collectively supply the majority of European and export expansion vessel membrane requirements. Amtrol Inc. (U.S.) leads the North American market.

Key competitive differentiators include EN/PED and WRAS certification breadth, EPDM vs. butyl material formulation expertise for specific fluid compatibility, bladder configuration capabilities for potable water certification, and regional distribution density for aftermarket replacement membrane supply.

Key Developments:

- March 2025: Flamco BV introduced the Flexcon Top® series with an enhanced butyl rubber bladder membrane configuration certified under WRAS and NSF/ANSI 61 for potable water applications across the European and North American plumbing system markets.

- October 2024: Reflex Winkelmann GmbH expanded its Reflexomat® pressure maintenance vessel line with EPDM membrane-fitted variants optimised for heat pump and solar thermal closed-loop systems, targeting the German GEG 2024 heat pump retrofit market across residential heating contractors.

- January 2024: Zilmet S.p.A. launched its CAL-PRO® Solar expansion vessel range with high-temperature-rated EPDM membranes certified for pressurised solar thermal system applications, targeting the Southern European solar thermal installation market across Italy, Spain, and France.

Global Expansion Vessel Membrane Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 1.2 Billion |

|

Current Market Value (2026) |

US$ 1.6 Billion |

|

Projected Market Value (2033) |

US$ 2.5 Billion |

|

CAGR (2026–2033) |

6.4% |

|

Leading Region |

Asia Pacific, 41.8% market share (2026) |

|

Dominant Membrane Type (Category-1) |

Diaphragm Membrane, 63% market share (2026) |

|

Top-ranking Material Type (Category-2) |

EPDM Rubber, leading share (2026) |

|

Incremental Opportunity |

US$ 0.9 Billion (2026–2033) |

Companies Covered in Global Expansion Vessel Membrane Market

- Flamco

- Spirotech

- Pure Aqua, Inc.

- RWC

- Varem Spa

- WATTS Water Technologies, Inc

- Zilmet Spa

- Emmeti Group

- Caleffi S.p.A.

- Sanhua

- HSC Water

- Oldrati

- Reliance Valves

- Aalberts N.V.

Frequently Asked Questions

The global expansion vessel membrane market is projected to be valued at US$ 1.6 billion in 2026.

Primary drivers are the EU Energy Performance of Buildings Directive (EPBD 2024/1275) compelling systematic hydronic heating system upgrades across tens of millions of European buildings with Germany’s GEG 2024 mandating 65% renewable heating from 2024 driving heat pump retrofits requiring expansion vessel membrane replacement and Asia Pacific’s construction boom with Global Construction 2030 projecting the region to account for 57% of global construction output by 2030.

Asia Pacific leads with approximately 41.8% market share in 2026, driven by China’s 14th Five-Year Plan district heating extension targeting 1.5 billion m² additional heated floor space, India’s NCAP-driven HVAC sector generating US$ 132.7M in national expansion vessel membrane demand, and South Korea’s G-SEED and Japan’s ZEB policy standards embedding hydronic system requirements in commercial construction.

The significant opportunity is the bladder membrane segment growing at 7% CAGR, driven by WRAS (U.K.), KTW Guideline (Germany), and NSF/ANSI 61 (U.S.) potable water certification mandates, combined with Europe’s MaPrimeRénov’ and BEG subsidy programs generating consistent hydronic system replacement cycles where certified bladder membranes are required in pressurized solar thermal and heat pump closed-loop potable water configurations.

Key players include Flamco BV, Reflex Winkelmann GmbH, Zilmet S.p.A., Varem S.p.A., Amtrol Inc., Calpeda S.p.A., Pneumatex AG, and Watts Water Technologies.