- Electrical Equipment & Services

- Medium Voltage Drives Market

Medium Voltage Drives Market Size, Share, and Growth Forecast 2025 - 2032

Medium Voltage Drives Market Analysis By Drive Type (AC Drives, DC Drives, Servo Drives), Power Rating (Up to 3 MW, 3.1 – 7.5 MW, 7.6 – 15 MW, Above 15 MW), Voltage Range (3.3 kV, 4.16 kV, 6.6 kV, 10 – 13.8 kV), Application, End-use and Regional Analysis 2025 - 2032

Medium Voltage Drives Market Share and Trends Analysis

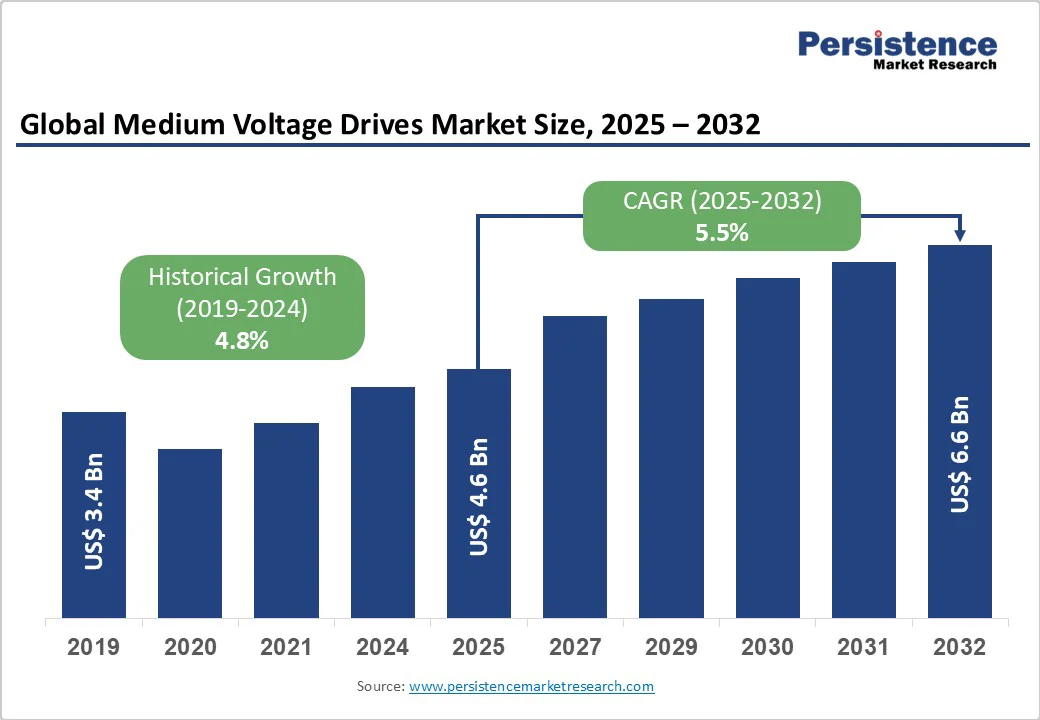

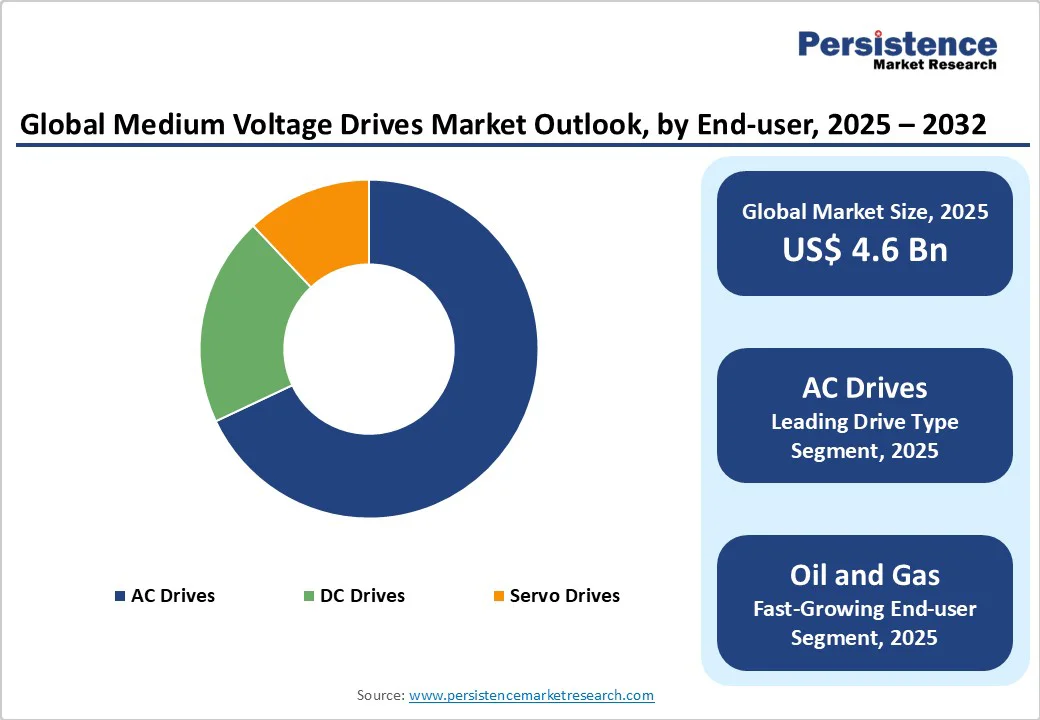

The global medium voltage drives market size is likely to be valued at US$4.6 billion in 2025 and is projected to reach US$6.6 billion by 2032, growing at a CAGR of 5.5% between 2025 and 2032. The increasing demand for industrial automation, stringent energy efficiency regulations, and the growing adoption of renewable energy integration systems across various industries underscore the need for medium voltage drives.

Key Market Highlights

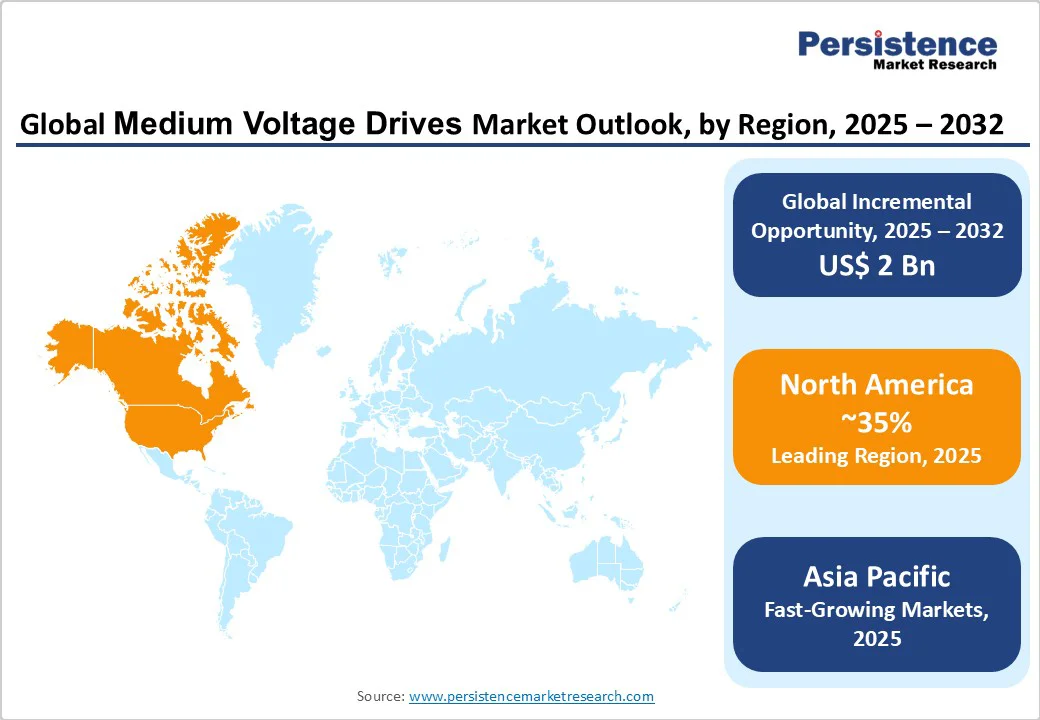

- Leading region: North America leads the global medium voltage drives market, thanks to its mature industrial infrastructure and supportive regulatory frameworks that promote energy efficiency investments across the oil and gas sectors.

- Fastest growing region: Asia Pacific represents the fastest-growing regional market with a 5.4% CAGR driven by rapid industrialization in China and India, supported by substantial infrastructure development programs.

- Dominant segment: AC drives dominate the market with a 68% share due to superior versatility and compatibility with existing industrial motor infrastructure across multiple application segments.

- The fastest-growing segment is pump applications, which show the strongest growth potential with a 35% share, benefiting from cubic power-speed relationships that enable

- substantial energy savings in variable flow conditions.

- Key market opportunity: The integration of Industrial Internet of Things (IIoT) presents a significant market opportunity as companies seek predictive maintenance capabilities and digital transformation solutions to optimize their operations.

| Key Insights | Details |

|---|---|

|

Medium Voltage Drives Market Size (2025E) |

US$ 4.6 Billion |

|

Market Value Forecast (2032F) |

US$ 6.6 Billion |

|

Projected Growth CAGR(2025-2032) |

5.5% |

|

Historical Market Growth (2019-2024) |

4.8% |

Market Dynamics

Growing Industrial Automation and Infrastructure Modernization

The accelerating pace of industrial automation across manufacturing, oil and gas, water treatment, and power generation sectors represents a fundamental growth driver for the medium voltage drives market. Industrial facilities are increasingly adopting Industry 4.0 frameworks that require sophisticated motor control systems capable of integrating with Industrial Internet of Things (IIoT) platforms. According to industry data, approximately 23% of the world's industrial motors are currently equipped with variable frequency drives, indicating substantial room for market expansion. The International Energy Agency projects electricity demand to increase by 4% annually through 2027, primarily driven by industrial production and data center expansion. Medium-voltage drives play a crucial role in efficiently managing this increased electrical load. Modern drives incorporate advanced features such as predictive maintenance capabilities, real-time performance monitoring, and seamless integration with digital ecosystems, making them essential components in smart factory implementations.

Energy Efficiency Regulatory Mandates and Sustainability Goals

Stringent energy efficiency regulations and corporate sustainability commitments are driving compelling demand for medium-voltage drives across multiple industries. Regulatory frameworks, such as the EU's Ecodesign Directive, mandate specific energy performance standards for industrial motor systems, while companies face mounting pressure to reduce their carbon footprints and achieve net-zero emissions targets. Medium voltage drives enable motor speed and torque optimization, typically delivering energy consumption reductions of 20-40% compared to fixed-speed motor operations.

For industrial applications involving pumps, fans, and compressors, variable frequency drives can significantly reduce electricity consumption during variable load conditions. The growing emphasis on Energy Star certifications and ISO 50001 energy management standards further accelerates adoption. Additionally, utility companies increasingly offer incentive programs for energy-efficient motor control systems, creating additional financial motivation for industrial facility upgrades.

High Initial Capital Investment and Technical Complexity

The substantial upfront costs associated with medium voltage drive procurement, installation, and commissioning present significant market restraints, particularly for small and medium-sized industrial operations. Complete medium voltage drive systems can require investments ranging from hundreds of thousands to several million dollars, depending on power ratings and application requirements. These systems require specialized technical expertise for proper installation, configuration, and ongoing maintenance, which creates additional operational complexities.

Many facilities lack in-house technical personnel with knowledge of medium voltage electrical systems, necessitating reliance on external service providers and increasing the total cost of ownership. The technical complexity extends to integration challenges with existing electrical infrastructure, particularly in retrofit applications where compatibility issues may require additional system modifications.

Skilled Labor Shortage and Maintenance Requirements

The medium voltage drives market faces constraints from the limited availability of qualified electrical technicians and engineers with specialized knowledge in high-voltage motor control systems. The installation and maintenance of these drives require extensive safety training and certification due to the inherent risks associated with medium-voltage electrical systems. Unplanned downtime resulting from maintenance issues can result in substantial financial losses, particularly in continuous process industries such as cement, steel, and chemicals. The specialized nature of medium voltage drive components often requires proprietary spare parts and manufacturer-specific service protocols, which can limit maintenance flexibility and increase dependency on original equipment manufacturers.

Renewable Energy Integration and Grid Modernization Opportunities

The global transition toward renewable energy sources presents substantial growth opportunities for medium-voltage drives, particularly in wind and solar power applications. Wind turbines utilize medium voltage drives for generator control and grid synchronization, while large-scale solar installations employ drives for tracking systems and power conditioning equipment.

According to renewable energy investment data, clean energy investments have exceeded $1.7 trillion globally in recent years, with a significant portion allocated to projects requiring medium-voltage motor control systems. Grid modernization initiatives, including smart grid implementations and energy storage systems, increasingly rely on medium voltage drives for power quality management and harmonic mitigation.

The integration of drives with renewable energy systems enables improved grid stability, voltage regulation, and reactive power compensation. These applications benefit from drives' regenerative capabilities, which can feed excess energy back to the grid during braking or deceleration cycles. Government incentives for renewable energy projects and infrastructure modernization programs provide additional market momentum.

Industrial Internet of Things and Predictive Maintenance Integration

The convergence of medium voltage drives with Industrial Internet of Things (IIoT) technologies and artificial intelligence presents significant market opportunities for enhanced operational efficiency and reduced maintenance costs. Modern drives incorporate advanced sensors and connectivity features that enable real-time performance monitoring, remote diagnostics, and predictive maintenance algorithms. These capabilities allow facility operators to identify potential equipment failures before they occur, minimizing unplanned downtime and optimizing maintenance scheduling. The integration of machine learning algorithms with drive control systems enables continuous performance optimization based on historical operating data and real-time conditions.

Cloud-based monitoring platforms offer centralized visibility across multiple industrial sites, facilitating enhanced asset management and operational coordination. The global push toward digital transformation in industrial operations creates a substantial demand for intelligent drive systems that can seamlessly integrate with enterprise resource planning and manufacturing execution systems.

Category-wise Insights

Drive Type Analysis

AC drives dominate, accounting for 68% share in 2025, establishing a clear leadership in this segment. The dominance stems from AC drives' superior versatility and widespread compatibility with existing industrial motor infrastructure. AC drives excel in applications requiring variable torque control, such as pumps, fans, and compressors, which represent the majority of medium-voltage motor applications across various industries. Their three-phase power configuration aligns seamlessly with standard industrial electrical systems, minimizing installation complexity and reducing system integration costs. AC drives incorporate advanced vector control algorithms that enable precise speed and torque regulation, essential for process optimization in industries such as oil and gas, water treatment, and power generation.

The technology offers excellent energy efficiency through sophisticated pulse width modulation techniques and regenerative braking capabilities. Recent technological advances include enhanced harmonic mitigation, improved power factor correction, and integration with Industrial Internet of Things platforms for remote monitoring and predictive maintenance capabilities.

Power Rating Analysis

The 3.1 - 7.5 MW power rating segment captures approximately 42% of the medium voltage drives market, representing the largest share among power categories. This segment's dominance reflects the optimal balance between power capacity and cost-effectiveness for major industrial applications, including large-scale pumping systems, industrial compressors, and heavy-duty fans. Applications in this power range typically serve critical infrastructure projects such as water treatment facilities, oil refinery operations, and power generation plants where reliable, high-capacity motor control is essential.

The 3.1 - 7.5 MW range accommodates most heavy industrial motor requirements while remaining within manageable cost parameters for capital equipment investments. These drives incorporate multi-pulse transformer configurations that ensure excellent power quality and low harmonic distortion, meeting stringent grid compliance requirements. The segment benefits from standardized product offerings from major manufacturers, which improves availability and reduces lead times compared to higher-power, custom solutions.

Voltage Range Analysis

4.16 kV voltage range commands approximately 38% share, establishing itself as the leading segment in the medium voltage drives market. This voltage level represents the most commonly specified standard in North American industrial electrical systems, particularly in manufacturing, oil and gas, and municipal utility applications. The 4.16 kV specification aligns with standard industrial transformer configurations and existing electrical infrastructure, minimizing system modification requirements and reducing installation costs. This voltage range provides optimal efficiency for medium-power applications typically ranging from 1 MW to 10 MW, covering the majority of industrial motor control requirements.

Drives operating at 4.16 kV benefit from mature technology platforms with proven reliability records and extensive service support networks. The standardization around this voltage level has resulted in competitive pricing and broad supplier availability, contributing to its market leadership position.

Application Analysis

Pump applications represent approximately 35% of the medium voltage drives market, maintaining the largest share among application categories. This dominance reflects the critical role of pumping systems across diverse industries ,including water and wastewater treatment, oil and gas processing, chemical and petrochemical operations, and power generation facilities. Pump

applications particularly benefit from variable frequency drive control due to the cubic relationship between pump speed and power consumption, enabling substantial energy savings during variable flow conditions. Medium-voltage drives enable precise flow control, pressure regulation, and system optimization, while reducing mechanical stress on pumping equipment and extending operational lifespans. The segment encompasses various pump types including centrifugal, axial, and positive displacement designs, each requiring specific control characteristics that medium voltage drives can accommodate. Recent developments include integration with smart grid technologies and advanced process control systems that optimize pumping operations based on real-time demand patterns and energy pricing structures.

Industry Analysis

The oil and gas sector accounts for approximately 36% revenue share in 2025, establishing clear dominance among end-use industries. This leadership position arises from the sector's extensive use of high-power motor applications, including drilling equipment, compression systems, and fluid-handling pumps across upstream, midstream, and downstream operations. The harsh operating environments and remote locations typical of oil and gas facilities demand robust, reliable drive systems with embedded fault diagnostics and remote monitoring capabilities.

Medium-voltage drives enable precise control of critical processes, such as gas compression, crude oil pumping, and refinery operations, while meeting stringent safety and environmental regulations. The industry's focus on operational efficiency and emission reduction drives continued investment in advanced motor control technologies. Global energy infrastructure investments and the need for process optimization in aging facilities support sustained demand for medium voltage drive upgrades and new installations.

Regional Insights

North America Medium Voltage Drives Trends

North America maintains its position as a leading region in the medium voltage drives market, driven primarily by United States market leadership and robust regulatory frameworks promoting energy efficiency. The region benefits from a mature industrial base with significant investments in infrastructure modernization, particularly in oil and gas, power generation, and water treatment sectors. The U.S. chemical industry experienced 3.9% production growth in 2022, driving increased demand for sophisticated motor control systems in chemical processing applications.

Regulatory initiatives such as energy efficiency mandates and utility rebate programs create favorable conditions for medium voltage drive adoption. The region's innovation ecosystem, anchored by leading technology companies and research institutions, drives

continuous advancement in drive control algorithms, power electronics, and digital integration capabilities. North American facilities increasingly prioritize predictive maintenance and Industrial Internet of Things integration, creating demand for intelligent drive systems with advanced monitoring and diagnostic features.

Europe Medium Voltage Drives Trends

European markets demonstrate strong growth momentum driven by aggressive energy efficiency regulations and ambitious carbon reduction commitments across the European Union. Germany, United Kingdom, France, and Spain lead regional adoption with substantial investments in industrial automation and renewable energy integration projects. The EU's Ecodesign Directive establishes stringent energy performance requirements that favor medium voltage drive implementations over traditional fixed-speed motor systems.

European industries increasingly focus on circular economy principles and sustainable manufacturing practices, driving demand for energy-optimized motor control systems. The region's offshore wind energy sector represents a significant growth driver, with medium voltage drives playing crucial roles in wind turbine generator control and grid synchronization systems. Regulatory harmonization across EU member states facilitates standardized product approvals and cross-border market access, supporting efficient market development and technology deployment.

Asia Pacific Medium Voltage Drives Trends

Asia Pacific emerges as the fastest-growing regional market with 5.4% CAGR projected through 2034, led by substantial industrial expansion in China, India, and ASEAN countries. China is positioned to reach USD 680 million market size by 2034, driven by massive infrastructure investments and manufacturing capacity expansion across multiple industrial sectors including steel, cement, and chemicals.

India's rapid industrialization and infrastructure development programs create significant demand for medium voltage drives in water treatment, mining, and power generation applications. The region's manufacturing advantages, including lower production costs and expanding local supply chains, attract global investment in industrial automation technologies. Government initiatives supporting clean energy transition, such as Australia's Future Made in Australia Act with USD 15 billion allocated for clean energy measures, drive regional market growth and technology adoption across the Asia Pacific.

Competitive Landscape

The medium voltage drives market exhibits a moderately consolidated structure with leading global manufacturers commanding significant market shares, while numerous specialized regional players serve niche applications and geographic markets. Market concentration centers around established industrial automation companies with extensive research and development capabilities, comprehensive service networks, and proven track records in high-voltage electrical systems. Key competitive differentiators include product reliability, energy efficiency performance, digital integration capabilities, and global service support infrastructure.

Leading companies pursue growth strategies emphasizing technological innovation, strategic partnerships, and geographic expansion into emerging markets. Recent industry trends include increased focus on Industrial Internet of Things integration, artificial intelligence-enhanced control algorithms, and sustainable manufacturing practices. The market structure supports both large-scale standardized products for common applications and customized solutions for specialized industrial requirements.

Key Market Developments

- November 2024: ABB introduced the ACS8080 medium-voltage air-cooled drive designed to enhance industrial performance and reliability, delivering up to 98% efficiency with reduced harmonic distortion for improved power quality and grid compliance.

- June 2024: ABB developed the world's first medium voltage speed-controlled motor concept, combining complete speed control within a single energy-efficient unit to address the fact that large motors account for 10% of global electricity consumption.

- April 2024: The Australian Government unveiled the Future Made in Australia Act industrial policy, allocating USD 15 billion

- in budget measures to support clean energy transition infrastructure requiring advanced motor control systems.

Companies Covered in Medium Voltage Drives Market

- Johnson Controls

- ABB

- Schneider Electric

- Eaton, Fuji Electric Co., Ltd.

- Rockwell Automation, Inc.

- WEG

- Yaskawa Electric Corporation

- Nidec Corporation

- GE

- Delta Electronics, Inc.

- Hitachi

- TMEIC

- Danfoss

Frequently Asked Questions

The global medium voltage drives market is projected to reach US$ 6.6 billion by 2032, growing at a CAGR of 5.5% from the 2025 baseline of US$ 4.6 billion.

Key demand drivers include increasing industrial automation, stringent energy efficiency regulations, renewable energy integration requirements, and the growing emphasis on Industrial Internet of Things integration for predictive maintenance capabilities.

AC drives dominate the market with approximately 68% market share due to their superior versatility, widespread compatibility with existing industrial infrastructure, and excellent performance in variable torque applications.

Asia Pacific represents the fastest-growing regional market with 5.4% CAGR driven by rapid industrialization in China and India, supported by substantial infrastructure development and clean energy transition programs.

The integration of Industrial Internet of Things and predictive maintenance technologies presents significant opportunities as companies seek digital transformation solutions for enhanced operational efficiency and reduced maintenance costs.

Market leaders include ABB, Schneider Electric, Rockwell Automation, Johnson Controls, Eaton, Siemens, and WEG, with ABB maintaining the strongest global market position through technological innovation and comprehensive product portfolios.