- Healthcare IT

- Medical Oncology Software Market

Medical Oncology Software Market Size, Share, and Growth Forecast, 2025 - 2032

Medical Oncology Software Market By Solution Type (Oncology Information Systems, Chemotherapy Management Software), Application Area (Medical Oncology, Radiation, Others), End-user (Hospitals & Cancer Centers, Others) and Regional Analysis for 2025 - 2032

Medical Oncology Software Market Size and Trends Analysis

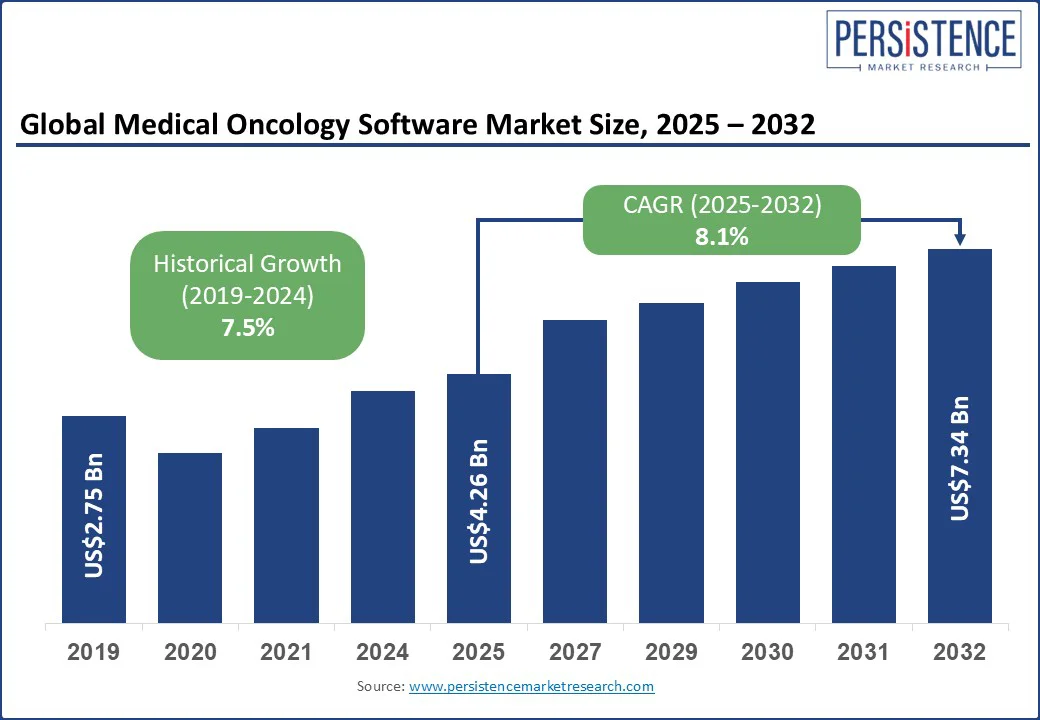

The global medical oncology software market size is projected to rise from US$4.26 Bn in 2025 to US$7.34 Bn by 2032. It is anticipated to witness a CAGR of 8.1% during the forecast period from 2025 to 2032.

The growth of the medical oncology industry is driven by rising cancer incidence, the increasing complexity of treatment regimens, and demand for integrated, data-driven care coordination across hospitals, clinics, and research networks. The market encompasses oncology information systems, chemotherapy management platforms, cancer registry solutions, and related decision-support tools designed to streamline cancer care delivery.

Key Industry Highlights

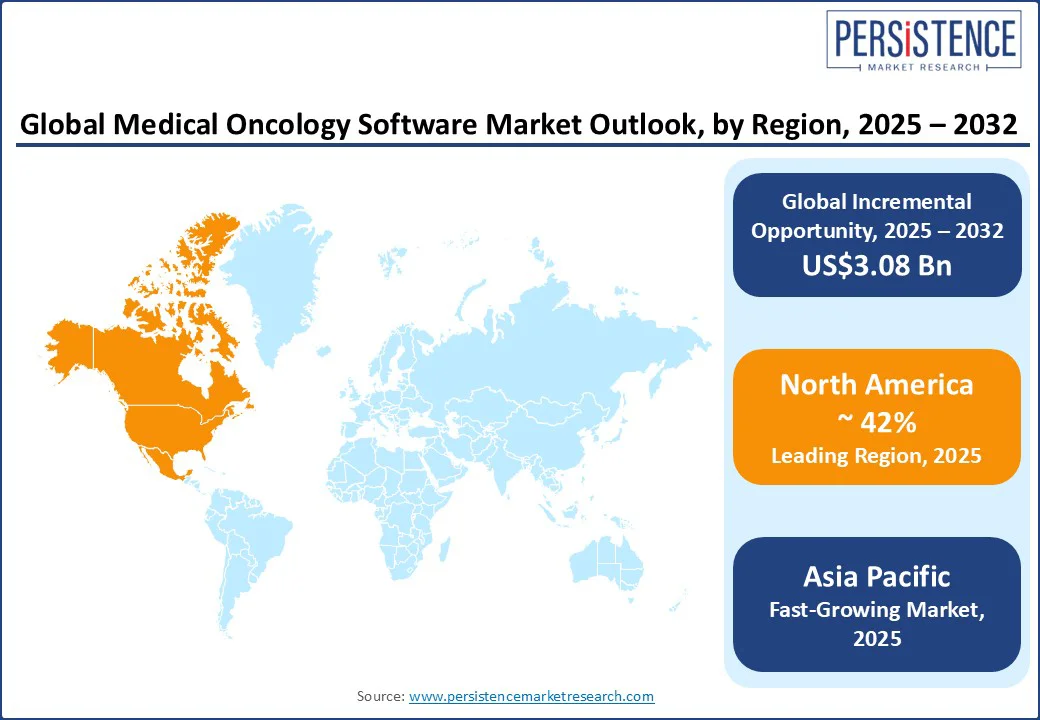

- Leading Region: North America, anticipated to hold around 42% market share in 2025, supported by advanced healthcare IT infrastructure, high oncology EHR adoption, and the strong presence of industry leaders such as Elekta, Varian, and Flatiron Health.

- Fastest-growing Region: Asia Pacific, projected to expand at a high CAGR, driven by large-scale cancer screening programs, national precision oncology initiatives in countries including China and India, and rapid adoption of cloud-based OIS platforms.

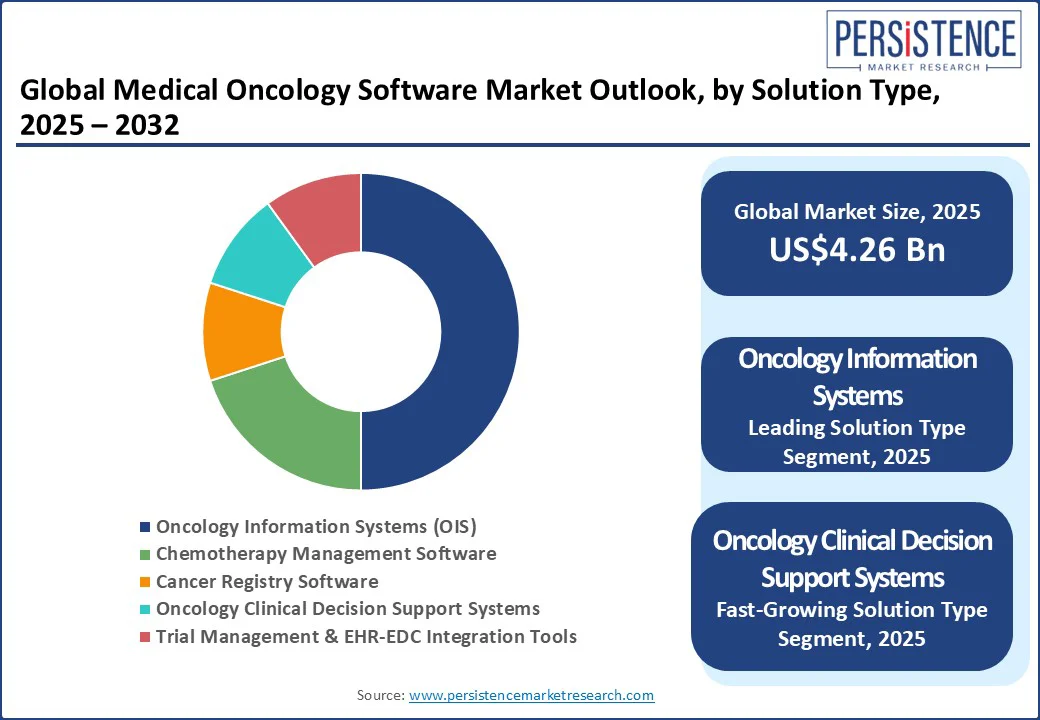

- Dominant Solution Type: Oncology information systems (OIS), anticipated to account for approximately 50% share in 2025, as they unify patient records, treatment planning, and multidisciplinary coordination in a single platform.

- Leading Application Area: Medical Oncology, expected to capture approximately 60% market share, driven by the high demand for chemotherapy order safety, infusion documentation, and survivorship management modules not offered by generic EMRs.

|

Global Market Attribute |

Key Insights |

|

Medical Oncology Software Market Size (2025E) |

US$4.26 Bn |

|

Market Value Forecast (2032F) |

US$7.34 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.5% |

Market Dynamics

Driver - Rising Complexity of Oncology Care Fuels Demand for Advanced, Integrated Software Solutions

The increasing incidence of cancer and longer patient survivorship are expanding oncology caseloads, driving demand for long-term, coordinated care platforms.

Hospitals are adopting chemotherapy order-entry systems to reduce dosing errors, while infusion centers are investing in workflow automation to optimize chair utilization, sterile compounding, and scheduling. Oncology-specific decision support tools are being integrated into these systems to manage targeted therapy dosing, monitor toxicities, and prevent drug-drug interactions.

The rise of precision medicine is also fueling demand for software that integrates genomic data at the point of care. Clinicians require electronic health records (EHRs) capable of ingesting next-generation sequencing (NGS) reports, mapping variants to clinical guidelines, and triggering targeted therapy alerts.

Life sciences companies are adopting real-world evidence (RWE) platforms to support label expansion and external control arm studies. Cancer centers are also implementing EHR-powered trial-matching engines and EHR-to-electronic data capture (EDC) pipelines to accelerate trial enrollment.

The growth of tele-oncology and home-infusion models is also boosting demand for remote chemotherapy monitoring and integrated scheduling solutions. In 2025, Varian Medical Systems launched an enhanced ARIA oncology information system with AI-driven order verification and real-time toxicity alerts, significantly improving treatment safety and operational efficiency.

Restraint - Workflow Fragmentation and Interoperability Gaps Hinder Seamless Software Adoption

Despite rapid advances, data fragmentation and poor interoperability remain critical barriers. Inconsistent normalization of NGS reports makes it difficult to automate genomic data integration into structured EHR fields, preventing timely decision-support alerts.

Similarly, frequent failures in reconciling chemotherapy orders between the OIS and EHRs force clinicians to rely on manual workarounds, leading to inefficiencies and heightened risk of errors. Clinical decision support (CDS) systems face challenges with “alert fatigue,” as oncologists override excessive or low-value safety prompts, undermining trust in toxicity and dosing alerts.

Trial-matching engines often yield false positives or miss eligible patients, limiting their usefulness in precision oncology programs. RWE initiatives are also slowed by inconsistent coding standards and missing data fields, forcing tumor boards to rely on manual reviews that reduce scalability.

Ransomware attacks, in particular, can cripple healthcare providers, leading to delayed treatments, disrupted clinical operations, and significant financial penalties and reputational damage. Specifically, IS Partners, LLC's healthcare cybersecurity statistics for 2024 indicate a 9.3% increase in healthcare data breaches affecting around 500 records in the first half of 2024 compared to the same period in 2023.

Opportunity - AI-Enabled Precision Oncology and Remote Infusion Care to Create High-Growth Niches

Artificial intelligence (AI) is emerging as a major growth catalyst for oncology software. AI-powered toxicity prediction models are helping clinicians identify high-risk patients before treatment, supporting proactive dose adjustments. EHR-integrated NGS interpretation (via FHIR Genomics) can now inject actionable variants directly into workflows and trigger precision therapy alerts.

RWE platforms leveraging AI are accelerating the creation of comparator arms for clinical trials, reducing time-to-label and enhancing payer negotiation strategies. Players that combine explainable AI with high-quality real-world data are well-positioned to win premium partnerships with pharma and cancer networks.

The shift toward home-based and decentralized oncology care is creating demand for specialist solutions. Remote infusion monitoring, smart pump auto-programming, and closed-loop EMR-pump integration are reducing intravenous (IV) administration errors and automating documentation.

In clinical trials, EHR-to-EDC connectors and FHIR-based matching tools are cutting enrollment timelines and screening failures. In 2025, Flatiron Health presented data from five million cancer patient records at ASCO, including the largest real-world ctDNA study in early breast cancer, showcasing how AI-enabled evidence platforms can transform trial efficiency and precision oncology.

Category-wise Analysis

Solution Type Insights

Oncology Information Systems (OIS) is projected to hold the largest market share of approximately 50% in 2025. OIS remains dominant as it consolidates patient records, scheduling, treatment planning, and multidisciplinary coordination into a unified platform.

Large cancer centers and hospital networks prefer these systems over multiple point solutions, as they seamlessly connect with pharmacy systems, infusion pumps, and radiation oncology equipment. This all-in-one capability reduces operational complexity, ensures regulatory compliance, and improves patient safety, factors especially valued in high-volume oncology practices in North America and Europe.

Oncology clinical decision support systems (AI-CDS) represent the fastest-growing segment, driven by the integration of advanced analytics into oncology workflows, including chemotherapy toxicity prediction models, biomarker-based therapy recommendations, and NGS variant interpretation.

Hospitals and cancer centers are increasingly adopting AI-CDS to enable precision oncology, reduce adverse events, and improve real-time clinical decision-making. The surge in demand is further supported by regulatory encouragement for evidence-based treatment protocols and the integration of AI-CDS with OIS and EHRs, making it the most dynamic in the medical oncology software market.

Application Area Insights

Medical oncology is anticipated to account for the largest market share at 60% in 2025. The segment leads because it manages the largest patient volume across oncology disciplines. Systemic therapies such as chemotherapy, targeted therapy, and immunotherapy form the backbone of most cancer treatment regimens, creating a sustained need for specialized software to manage orders, monitor toxicities, and coordinate care.

High integration requirements with pharmacy and infusion workflows also strengthen its dominance. Medical oncology continues to be the fastest-growing field as cancer incidence is rising, treatment regimens are becoming more personalized, and payers are pushing for quality metrics and documentation to justify high-cost therapies. The global shift toward outpatient and home infusion models further increases reliance on digital systems for safe, remote care coordination.

Regional Insights

North America Medical Oncology Software Market Trends - Robust Healthcare Infrastructure and Early AI Adoption Driving Growth

North America is projected to lead the medical oncology software market in 2025, accounting for approximately 42% of the market share. This leadership is driven by product innovation, large-scale commercial deployments, and deep electronic medical record (EMR) penetration, especially within major U.S. cancer networks. Demand is growing for enterprise OIS, AI-enabled CDS, and EHR-to-EDC integration tools.

In the U.S., RWD players such as Flatiron are expanding clinical-pipeline and evidence-generation solutions that integrate directly into oncology workflows. These partnerships are accelerating the adoption of EHR-to-OIS connectivity and eSource tools, as sponsors seek more efficient trial execution and data capture.

Notably, Flatiron’s recent collaborations with academic and NCI-designated networks highlight the growing reliance on RWD for trial design and external-control arms. U.S. cancer networks and academic centers are also piloting AI tools for chemotherapy toxicity prediction and NGS interpretation, creating demand for scalable, explainable AI-CDS solutions. These pilots, especially when backed by payer interest in outcomes, often evolve into enterprise-wide contracts, rather than remaining limited to point solutions.

In Canada, provincial cancer registries and national initiatives such as the Pan-Canadian Cancer Data Strategy and Ontario Cancer Statistics are fueling investments in registry, analytics, and population-health oncology platforms. Centralized procurement processes, often led by provincial agencies, favor vendors capable of province-wide deployments and standardized reporting. These multi-year tenders offer significant opportunities in areas such as cancer registries, electronic patient-reported outcomes (ePRO), and tele-oncology, but require strong public-sector compliance and integration capabilities.

Europe Medical Oncology Software Market Trends - Precision Oncology Initiatives and Cross-Border Research Collaborations Accelerate Adoption

The Europe market is shaped by national digital health initiatives, trust-level procurements, and growing demand for integrated oncology solutions that combine medical and radiation workflows. Buyer behavior differs across countries, with the U.K. focusing on centralized, standards-driven procurements, while Germany emphasizes feature-rich, compliance-oriented hospital purchases.

In the U.K., NHS England’s Cancer 360 program and multiple SACT ePRO procurements highlight ongoing efforts to centralize cancer patient tracking lists (PTLs), digitize SACT pathways, and standardize ePRO sourcing across trusts. Recent procurement notices, such as the East of England SACT ePRO, point to near-term buying opportunities for ePRO solutions, pathway orchestration, and PTL dashboards.

The NHS favors vendors who can demonstrate national governance, data security, and interoperability. While centralization accelerates adoption at scale, it also imposes strict procurement, data-governance, and integration requirements, favoring established or well-partnered suppliers.

In Germany, cancer centers show a strong demand for integrated radiation and medical oncology suites. Vendors such as Elekta (MOSAIQ) and Varian/Siemens Healthineers are leading incumbents, offering bundled solutions that combine radiation therapy planning with OIS capabilities.

Elekta’s real-world product testing and continued investments reinforce this preference. German hospitals place a high value on quality assurance, documentation, and device interoperability with infusion pumps and radiotherapy systems, creating strong demand for vendor solutions with robust integration and regulatory-grade audit trails.

Asia Pacific Medical Oncology Software Market Trends - Expanding Cancer Burden and Digital Health Investments Propel Demand

Asia Pacific is the fastest-growing region, driven by a high CAGR. China is at the forefront with rapid AI adoption in oncology workflows, while India represents a volume-driven market fueled by tele-oncology, cloud-based SaaS solutions, and hub-and-spoke care delivery models.

In China, hospitals and health tech firms are aggressively piloting and deploying AI in diagnostics and oncology workflows, including imaging AI, NGS interpretation, and lesion detection. Large pharma and biotech companies are also investing in China-based AI partnerships, increasing commercial opportunities for oncology software that supports RWE and local regulatory submissions.

In India, tele-oncology pilots and hub-and-spoke models are expanding to improve access, with multiple recent district telemedicine projects and home-infusion monitoring pilots emerging. Hospitals are increasingly adopting low-cost, cloud-based SaaS deployments to reach rural populations.

Cost-sensitive buyers prefer modular, cloud-hosted solutions with simple integration, such as ePRO, teleconsultation, and scheduling, rather than large on-premise enterprise OIS installations. India represents a high-volume, low-price growth opportunity for SaaS tele-oncology, remote monitoring, and ePRO solutions that enable outreach and decentralization of care.

Competitive Landscape

The global medical oncology software market is moderately consolidated, with a mix of global health IT leaders and niche oncology-focused players competing on integration capabilities, regulatory compliance, and AI-driven innovations.

Key players, such as Varian Medical Systems (Siemens Healthineers), Elekta AB, and Cerner (Oracle Health), dominate due to their comprehensive OIS platforms, robust interoperability features, and established hospital networks. Their ability to bundle oncology solutions with broader EMR and imaging systems strengthens market share, particularly in mature regions such as North America and Europe.

Emerging players, including Flatiron Health, RaySearch Laboratories, and Tempus, are gaining traction by focusing on precision oncology, cloud-native platforms, and AI-powered CDS. Strategic partnerships with cancer research centers, pharma companies, and genomic labs enable these players to offer specialized capabilities such as NGS data integration and biomarker-driven treatment recommendations. Mergers, acquisitions, and regional distribution alliances remain critical strategies to expand market reach and accelerate innovation cycles.

Key Industry Developments

- In May 2025, Flatiron Health announced that 14 abstracts leveraging real-world oncology data and AI, from over five million cancer patient records, were accepted for the ASCO 2025 annual meeting. These studies included the largest real-world ctDNA testing in early-stage breast cancer and assessments of trial enrollment efficiency, reinforcing Flatiron’s expanding role in AI-enabled evidence generation and oncology workflows.

- In May 2025, Varian Medical Systems unveiled an enhanced ARIA Oncology Information System, integrating AI-driven workflow automation to streamline chemotherapy order verification and deliver real-time toxicity alerts, improving patient safety and operational efficiency.

Companies Covered in Medical Oncology Software Market

- Varian Medical Systems, Inc. (Siemens Healthineers)

- Elekta AB

- Philips Healthcare

- Cerner Corporation (Oracle)

- McKesson Corporation

- Flatiron Health, Inc. (Roche)

- RaySearch Laboratories AB

- IBM Watson Health (Merative)

- F. Hoffmann-La Roche Ltd.

- Epic Systems Corporation

- OncoEMR (Altos Solutions)

- CureMD Healthcare

- Koninklijke Philips N.V.

- MEDITECH (Medical Information Technology, Inc.)

- OncoHealth

- NeoGenomics Laboratories

- Intelerad Medical Systems

- Cota, Inc.

- Tempus, Inc.

- Syapse, Inc.

Frequently Asked Questions

The global medical oncology software market is valued at US$ 4.26 Bn in 2025.

The medical oncology software market is projected to reach US$ 7.34 Bn by 2032.

Key trends include AI-powered CDS integration, NGS (Next-Generation Sequencing) and precision oncology adoption, cloud-based OIS platforms, and growing interoperability between EHR and trial management systems.

Oncology Information Systems (OIS) lead the market, holding about 50% share in 2025, driven by their ability to unify patient records, treatment planning, and multi-disciplinary workflows.

The medical oncology software market is expected to grow at a CAGR of 8.1% from 2025 to 2032, driven by increasing cancer incidence, precision medicine expansion, and demand for integrated digital oncology ecosystems.

Elekta AB, Varian Medical Systems (Siemens Healthineers), Flatiron Health (Roche), Philips Healthcare and Cerner Corporation (Oracle Health).