- Medical Devices

- Medical Membrane Device Market

Medical Membrane Device Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Medical Membrane Device Market by Product Type (Microfiltration Membranes, Ultrafiltration Membranes, Nanofiltration Membranes, Reverse Osmosis Membranes), Application (Dialysis, Drug Delivery, Tissue Engineering, Cell Separation), End-use, and Regional Analysis for 2025 - 2032

Medical Membrane Device Market Size and Trends Analysis

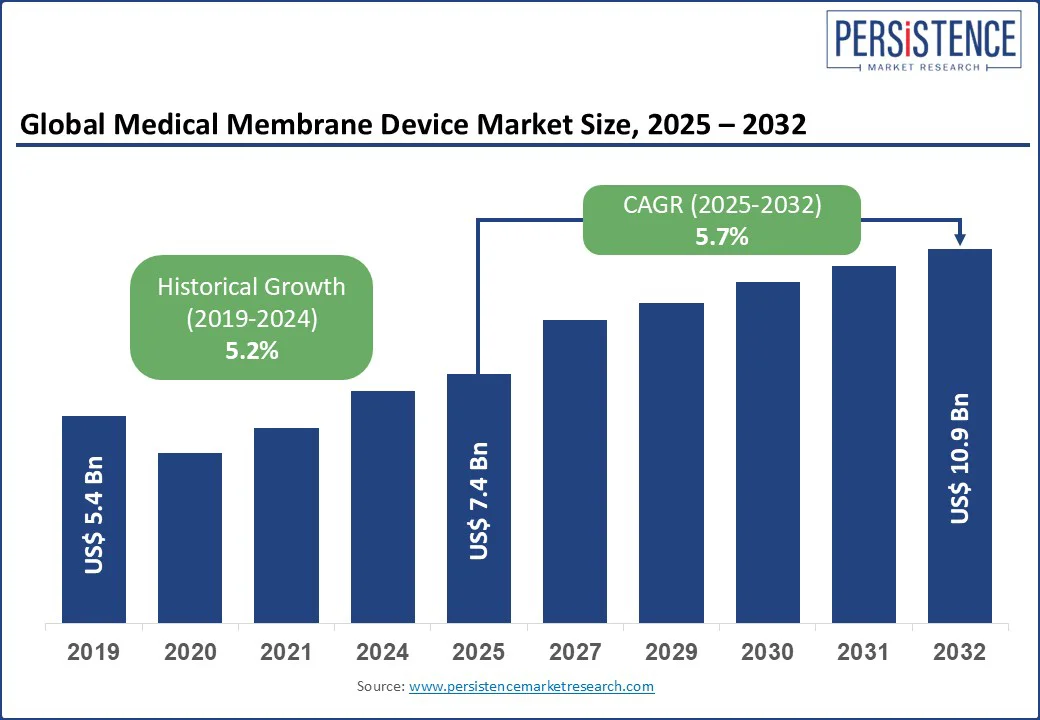

The global medical membrane device market size is likely to be valued at US$7.4 Bn in 2025, expected to reach US$10.9 Bn by 2032, at a CAGR of 5.7% during the forecast period 2025 - 2032.

The medical membrane device industry is experiencing robust growth, driven by rising demand for advanced filtration, separation, and drug delivery solutions in healthcare. These devices are widely used in hemodialysis, drug formulation, intravenous therapy, and sterilization processes, ensuring patient safety and treatment efficiency.

The increasing prevalence of chronic kidney disease, diabetes, and other lifestyle-related disorders boosts demand for dialysis membranes. At the same time, the growing adoption of biologics and specialty drugs fuels the need for membranes in pharmaceutical manufacturing.

Key Industry Highlights

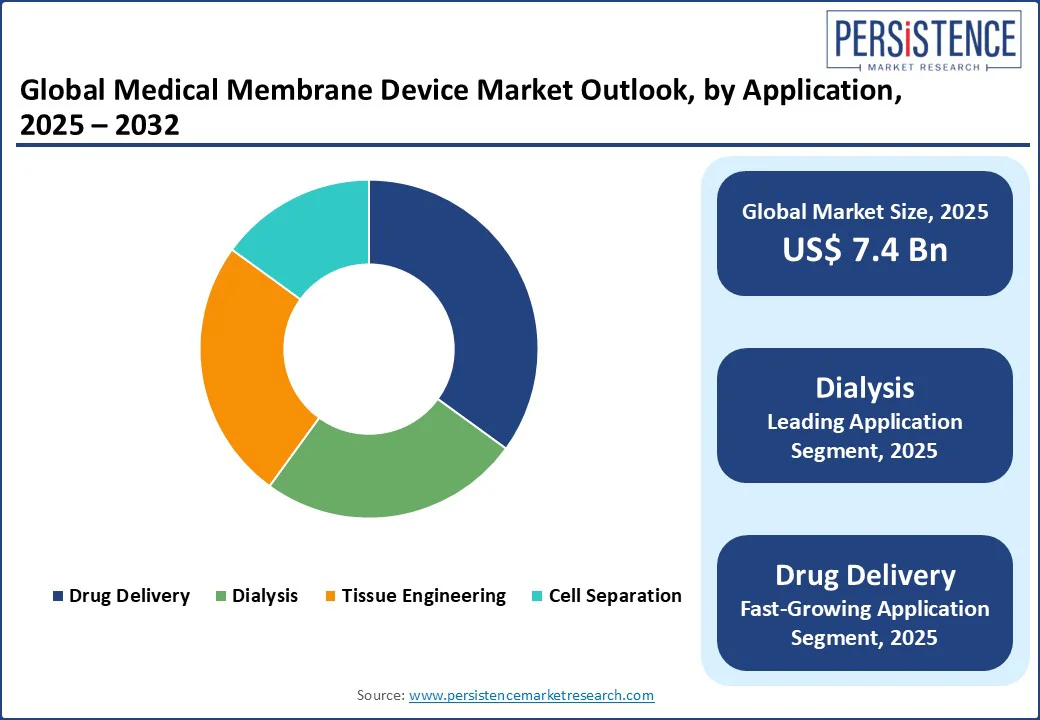

- Leading Application: Dialysis application holds a 45% market share in 2025, driven by dialysis membranes and hemodialysis devices.

- Ultrafiltration Growth: Ultrafiltration membranes are fueled by blood purification membranes. They ensure efficient fluid and toxin removal during dialysis and hemofiltration, making them a core technology in renal and critical care therapies.

- Hospitals Surge: Hospitals' end-use is driven by extensive use in critical care and renal therapy, while pharmaceutical companies leverage membranes for drug purification and controlled release systems.

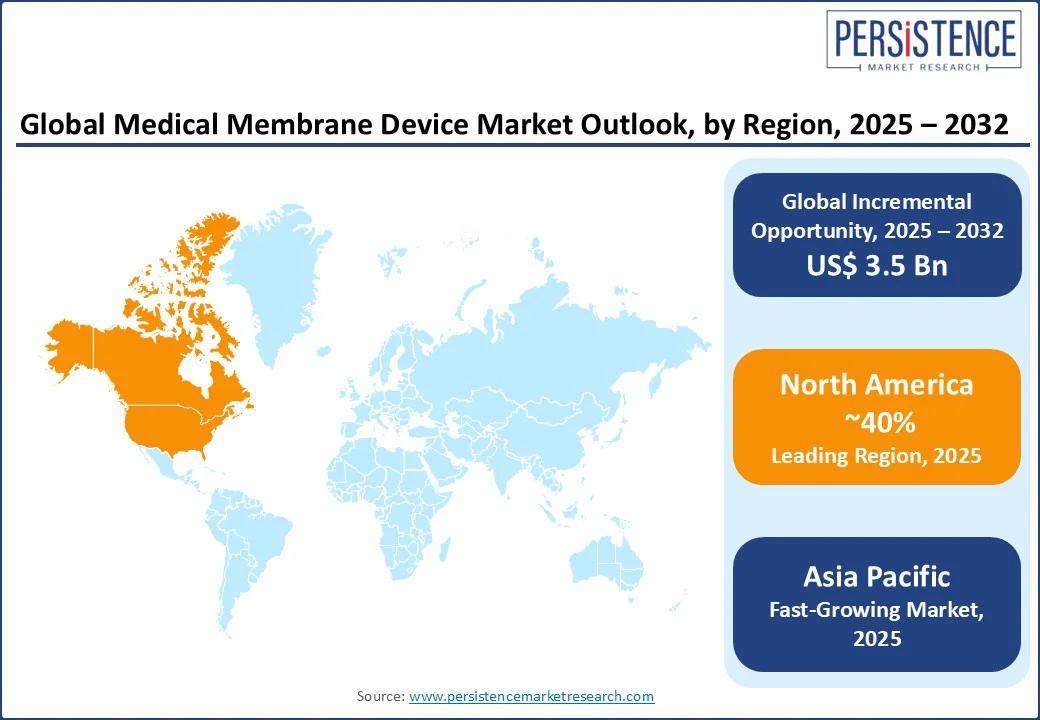

- Regional Dominance: North America commands a 40% market share. It leads the market with its advanced healthcare ecosystem, strong regulatory framework, and widespread adoption of membrane-based therapies, while the Asia Pacific is the fastest-growing, with 20%.

- Innovation Impact: Medical membrane technology for drug delivery and biocompatible membranes for healthcare devices boost membrane-based medical devices by 12% in 2025.

- Technological Advancements: Hollow fiber membranes in medicine drive 10% growth in clinical filtration membranes. These membranes feature a unique structure consisting of thousands of microscopic fibers, providing an exceptionally high surface area for filtration within a compact design.

- Healthcare Demand: Polymeric medical membranes enhance medical-grade membrane systems by 15%.

|

Global Market Attribute |

Key Insights |

|

Medical Membrane Device Market Size (2025E) |

US$7.4 Bn |

|

Market Value Forecast (2032F) |

US$10.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.2% |

Market Dynamics

Driver: Rising Prevalence of Chronic Kidney Diseases Can Push the Medical Membrane Device Market

The medical membrane device market is driven by the rising prevalence of chronic kidney diseases (CKD), increasing demand for dialysis membranes, hemodialysis devices, and blood purification membranes. Globally, 13% of the population suffers from CKD, driving the need for therapeutic membrane devices and dialysis consumables in hospitals and clinics.

High-performance membranes for medical applications, such as polyether sulfone (PES) membranes and hollow fiber membranes, ensure efficient filtration and biocompatibility, supporting clinical filtration membranes.

The adoption of membrane-based medical devices in dialysis treatments enhances patient outcomes, while medical-grade membrane systems cater to the growing demand for membrane separation technology in healthcare settings, aligning with the increasing focus on chronic disease management and advanced medical treatments.

Restraint: High Manufacturing Costs Could Delay Product Launches

The medical membrane device market faces a significant restraint due to high manufacturing costs, impacting the production of filtration membranes and membrane-based medical devices.

The cost of producing biocompatible membranes for healthcare devices, such as ultrafiltration membranes and polymeric medical membranes, is elevated due to advanced materials and stringent quality standards, with manufacturing expenses increasing by 20% in 2025.

This limits affordability for smaller healthcare facilities and restricts the scalability of dialysis consumables, clinical filtration membranes, and therapeutic membrane devices, particularly in cost-sensitive regions, hindering market penetration for Baxter filtration devices and hollow fiber membranes in medicine.

Opportunity: Advancements in Drug Delivery Systems Will Propel the Market Growth

Advancements in medical membrane technology for drug delivery present a significant opportunity for the medical membrane device market. With 15% growth in controlled-release drug delivery systems in 2025, there is increasing demand for polymeric medical membranes and membrane-based medical devices for precise drug administration.

This trend drives innovation in biocompatible membranes for wearable healthcare devices and hollow fiber membranes in medicine, particularly for drug delivery applications in pharmaceutical companies and research institutions.

The focus on personalized medicine and targeted therapies aligns with global healthcare trends, encouraging manufacturers to develop medical-grade membrane systems and clinical filtration membranes, positioning the market for growth in advanced therapeutic applications.

Category-wise Analysis

Product Type Insights

Ultrafiltration Membranes hold a 40% market share in 2025, driven by their critical role in blood purification membranes and dialysis membranes. With 45% adoption in hemodialysis devices, these membranes are essential for therapeutic membrane devices in dialysis and cell separation, offering high filtration efficiency and biocompatibility.

Their dominance stems from high-performance membranes for medical applications, supported by polyether sulfone (PES) membranes and membrane separation technology.

Nanofiltration Membranes are fueled by their use in clinical filtration membranes for drug delivery and tissue engineering. With 12% growth in 2025, these membranes are gaining traction in medical-grade membrane systems, driven by their ability to filter smaller particles and support advanced biocompatible membranes for healthcare devices.

Application Insights

Dialysis commands a 45% market share in 2025, driven by the widespread use of dialysis membranes and hemodialysis devices in treating chronic kidney diseases. With 50% adoption in 2025, this segment benefits from blood purification membranes and Baxter filtration devices, supporting high-demand hospital and clinic settings with dialysis consumables.

Drug delivery is fueled by advancements in medical membrane technology for drug delivery. With 10% growth in 2025, this segment is driven by polymeric medical membranes and hollow fiber membranes in medicine, as pharmaceutical companies adopt therapeutic membrane devices for controlled-release systems.

End-use Insights

Hospitals hold a 50% market share in 2025, driven by the extensive use of hemodialysis devices and therapeutic membrane devices. With 55% adoption in 2025, hospitals rely on dialysis membranes and clinical filtration membranes for patient care, supported by medical-grade membrane systems. This dominance stems from their critical role in providing specialized care such as renal dialysis, critical care filtration, and treatments that rely on advanced membrane systems.

Pharmaceutical Companies are fueled by demand for medical membrane technology for drug delivery. With 11% growth in 2025, this segment is driven by polymeric medical membranes and hollow fiber membranes in medicine, supporting drug development and production processes. The pharmaceutical sector’s increasing reliance on biologics, injectables, and controlled-release drugs fuels the adoption of polymeric and hollow fiber membranes.

Regional Insights

North America Medical Membrane Device Market Trends

North America holds a 40% global market share in 2025, with the U.S. leading due to its advanced healthcare infrastructure and high CKD prevalence, generating US$ 2.96 Bn in sales in 2025. The U.S. market is driven by demand for dialysis membranes and hemodialysis devices, with 70% of dialysis centers using blood purification membranes in 2025.

Key drivers include a 15% increase in dialysis patients, boosting Baxter filtration devices and therapeutic membrane devices. Medical membrane technology for drug delivery sees 10% growth, supported by Fresenius Medical Care and Baxter International, which drive 25% of regional revenue. The focus on advanced healthcare fuels clinical filtration membranes and high-performance membranes for medical applications, aligning with U.S. healthcare trends.

Europe Medical Membrane Device Market Trends

Europe accounts for a 30% global share, led by Germany, the UK, and France. Germany’s market grows at a CAGR of 5.6%, driven by a robust healthcare sector and CKD prevalence, with 60% of hospitals using dialysis consumables in 2025. The UK’s market is propelled by therapeutic membrane devices, with NHS hospitals adopting ultrafiltration membranes.

France witnessed 12% growth in medical membrane technology for drug delivery, driven by its pharmaceutical industry and demand for polymeric medical membranes. EU healthcare investments, with €150 Mn in funding for medical devices in 2025, boost biocompatible membranes for healthcare devices. Asahi Kasei Medical holds a 10% market share, leveraging hollow fiber membranes in medicine.

Asia Pacific Medical Membrane Device Market Trends

Asia Pacific is the fastest-growing region, with a CAGR of 6.2%, led by China, Japan, and India. China holds a 45% regional market share, driven by a 20% increase in healthcare infrastructure investments in 2025, which has boosted demand for dialysis membranes and hemodialysis devices. India’s market grows at a CAGR of 6.4%, fueled by rising CKD cases, with 75% of urban hospitals using blood purification membranes in 2025.

Japan’s clinical filtration membranes drive 10% growth in therapeutic membrane devices, supported by its aging population. Toray Industries and Nipro Corporation lead, supported by US$3 Bn in healthcare investments by 2030, enhancing medical-grade membrane systems and membrane separation technology.

Competitive Landscape

The global medical membrane device market is highly competitive, with medical device companies focusing on innovation, biocompatibility, and performance. Toray Industries and Fresenius Medical Care lead in dialysis membranes, while Baxter International excels in filtration devices.

Clinical filtration membranes, biocompatible membranes for healthcare devices, and hollow fiber membranes in medicine drive competition. Strategic partnerships and R&D investments in high-performance membranes for medical applications are key differentiators, with companies addressing chronic disease management and advanced therapeutic needs.

Key Industry Developments

- In May 2025, CorWave, a medical device company, announces the world’s first implantation in a patient of its Left Ventricular Assist System (LVAS), the first heart pump based on breakthrough wave membrane technology. The procedure was performed by the team at St Vincent’s Hospital in Sydney, Australia. This implantation represents a major technological milestone in the field of durable mechanical circulatory support, 27 years after the first use of a durable rotary pump, a technology that has since become the standard of care.

- In September 2024, Medtronic plc, the global leader in medical technology, announced the launch of a new ECMO system called VitalFlow™, which is a configurable one-system ECMO solution, built on simplicity and performance. The VitalFlow™ ECMO System bridges the gap between bedside care and intra-hospital transport, offering physicians and clinicians an easier, smarter ECMO experience.

- In May 2021, Trinity Technology Group (TTG, Inc.) applied the company’s substantial polymer engineering expertise and proprietary manufacturing technology to create the CELLATEX line of microporous expanded PTFE (ePTFE) membranes, tapes, and laminated textiles. Medical device engineers now have a new option for high-performance ePTFE products that are specifically designed for medical applications and are made in the USA.

Companies Covered in Medical Membrane Device Market

- Toray Industries

- Ameda

- Synder Filtration

- Koch Membrane Systems

- Medtronic

- Danaher Corporation

- Fresenius Medical Care

- Nipro Corporation

- Terumo Corporation

- Pall Corporation

- Asahi Kasei Medical

- Baxter International

- Merck Group

- Others

Frequently Asked Questions

The medical membrane device market is projected to reach US$ 7.4 Bn in 2025, driven by dialysis membranes and hemodialysis devices.

Rising CKD prevalence, affecting 13% of the global population, drives demand for blood purification membranes.

The medical membrane device market grows at a CAGR of 5.7% from 2025 to 2032, reaching US$ 10.9 Bn by 2032.

Medical membrane technology for drug delivery, with 15% growth in controlled-release systems, offers opportunities.

Key players include Toray Industries, Fresenius Medical Care, Baxter International, and Asahi Kasei Medical.