- Medical Devices

- Wearable Healthcare Devices Market

Wearable Healthcare Devices Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Wearable Healthcare Devices Market by Product Type (Trackers, Smart Watches, Patches, and Smart Clothing), by Device Type (Diagnostic and Monitoring Devices, and Therapeutic Devices) by Application (General Health and Fitness, Remote Patient and Post-Surgical Care, Home Healthcare, and Others), by Distribution Channel (Pharmacies, Online Channel, Hypermarkets/General Retail Stores, and Specialty Retailer Stores), and Regional Analysis from 2026 - 2033

Wearable Healthcare Devices Market Share and Trends Analysis

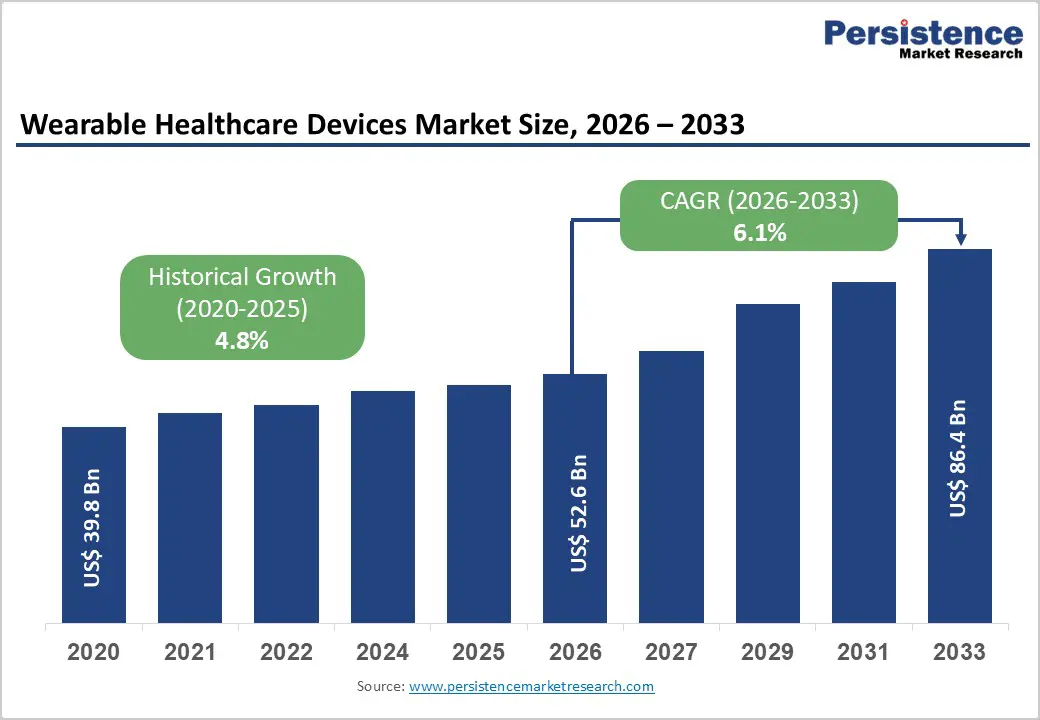

The global wearable healthcare devices market size is likely to be valued at US$ 52.6 billion in 2026 and projected to reach US$ 86.4 billion by 2033 growing at a CAGR of 6.1% during the forecast period from 2026 to 2033.

Global demand for wearable healthcare devices is rising steadily, driven by increasing health awareness, growing prevalence of chronic conditions, and the expanding shift toward preventive and remote healthcare delivery models.

Healthcare providers and consumers are increasingly adopting wearable technologies to enable continuous health monitoring, early disease detection, and real-time data-driven clinical decision-making. Hospitals, homecare settings, and outpatient facilities are witnessing higher adoption as wearable devices are increasingly integrated into remote patient monitoring, post-surgical recovery, and long-term disease management pathways.

Key Industry Highlights

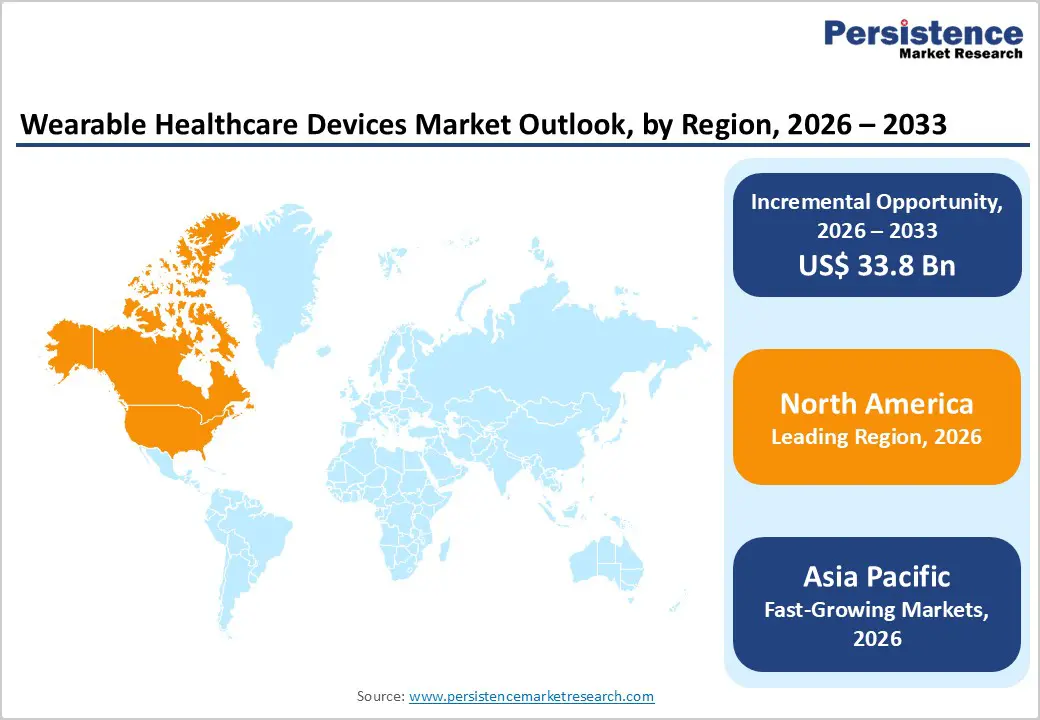

- Leading Region: North America accounts for the largest share at 46.5%, supported by strong digital health infrastructure, widespread adoption of remote patient monitoring programs, high consumer spending on connected health technologies, and early access to FDA-cleared wearable healthcare devices.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace, driven by a large and increasingly health-conscious population, improving access to healthcare services, rapid expansion of private healthcare facilities, growing medical tourism, and rising investments in digital health and remote monitoring solutions.

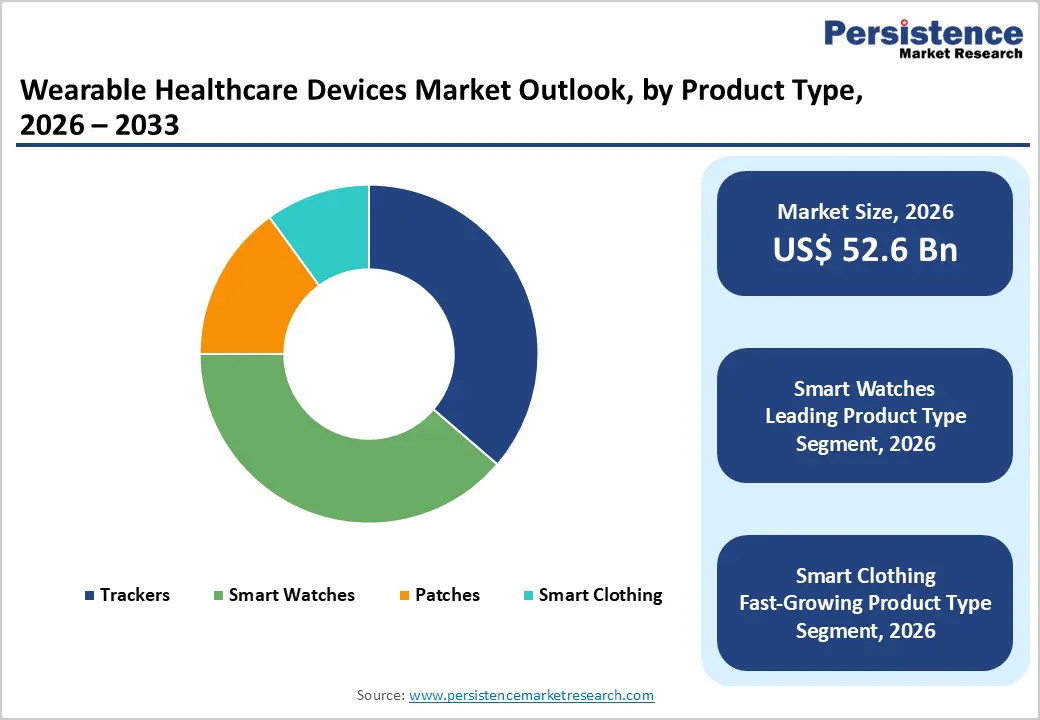

- Leading Product Type Segment: Smartwatches dominate the market due to their widespread use as first-line health monitoring tools, ease of use, continuous data tracking capabilities, repeat usage across preventive and clinical applications, and strong physician acceptance for remote monitoring and wellness management.

- Fastest-Growing Product Type Segment: Smart clothing is witnessing rapid growth as clinical adoption increases for continuous physiological monitoring, rehabilitation support, and long-term health tracking, supported by non-intrusive designs, improving sensor integration, and expanding availability of clinically validated smart textile solutions.

- Leading Application Segment: Remote patient and post-surgical care remains the leading segment, driven by a large patient pool requiring continuous monitoring for recovery, chronic disease management, and early complication detection, along with increasing adoption of hospital-at-home and value-based care models.

- Fastest-Growing Application Segment: Home healthcare is growing rapidly due to rising demand for long-term health monitoring, increasing adoption of wearable devices for elderly care and chronic condition management, and expanding availability of user-friendly, clinically reliable wearable technologies for home-based care.

| Key Insights | Details |

|---|---|

|

Wearable Healthcare Devices Market Size (2026E) |

US$ 52.6 Bn |

|

Market Value Forecast (2033F) |

US$ 86.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.8% |

Market Dynamics

Driver - Rising Burden of Chronic Diseases and Advancements in Sensor and Connectivity Technologies

The global wearable healthcare devices market is being significantly driven by the rising prevalence of chronic diseases, including cardiovascular disorders, diabetes, respiratory conditions, and obesity. These conditions require continuous, long-term monitoring rather than episodic clinical assessments, creating strong demand for wearable devices capable of real-time tracking of vital parameters such as heart rate, blood glucose trends, physical activity, oxygen saturation, and sleep patterns. Healthcare systems are increasingly relying on wearable-based monitoring to enable early intervention, reduce hospital admissions, and improve disease management outcomes. The growing aging population, coupled with lifestyle-related health risks, further accelerates adoption of wearable devices as cost-effective tools for chronic disease surveillance and preventive care across both clinical and home healthcare settings.

The rapid advancements in sensor technology and connectivity are enhancing the clinical reliability and usability of wearable healthcare devices. Innovations in biosensors, including improved optical, electrochemical, and motion sensors, are delivering higher data accuracy and consistency. Integration of AI-driven analytics, cloud-based platforms, and advanced wireless connectivity enables continuous data transmission, real-time alerts, and seamless integration with electronic health records and telehealth systems. These technological improvements are increasing physician confidence, expanding regulatory clearances, and supporting broader clinical adoption of wearable devices for chronic disease management, remote patient monitoring, and personalized healthcare delivery.

Restraints - Data Privacy, Cyber security, and Clinical Validation Challenges

Data privacy and cybersecurity concerns represent a major restraint for the global wearable healthcare devices market, particularly in clinical and institutional healthcare settings. Wearable devices continuously collect and transmit sensitive patient health data, increasing the risk of data breaches, unauthorized access, and misuse of personal health information. Compliance with stringent data protection regulations such as HIPAA, GDPR, and other regional privacy frameworks adds complexity for manufacturers and healthcare providers. Concerns around data ownership, interoperability, and secure integration with hospital information systems further limit large-scale deployment. As healthcare organizations prioritize patient confidentiality and risk mitigation, unresolved cybersecurity vulnerabilities can slow adoption and delay integration of wearable technologies into routine clinical workflows.

Moreover, challenges related to data accuracy and clinical validation continue to hinder physician confidence in wearable healthcare devices, especially consumer-grade products. Variability in sensor performance, inconsistent data quality across different use environments, and limited validation across diverse patient populations raise concerns about clinical reliability. Many devices lack robust, large-scale clinical trials demonstrating equivalence to traditional medical-grade monitoring equipment. This gap restricts regulatory approvals, reimbursement eligibility, and formal inclusion in clinical guidelines. Without standardized validation frameworks and stronger clinical evidence, healthcare providers may remain cautious about relying on wearable-generated data for diagnosis, treatment decisions, and long-term patient management.

Opportunity - AI-Enabled Predictive Healthcare and Expansion of Home-Based Care

The integration of artificial intelligence and machine learning with wearable healthcare devices presents a significant growth opportunity by enabling predictive and personalized healthcare delivery. Advanced algorithms can analyze large volumes of continuous wearable data to identify early disease patterns, detect subtle physiological changes, and generate actionable insights before symptoms become clinically apparent. This capability supports proactive interventions, personalized treatment planning, and risk stratification for conditions such as cardiovascular disease, diabetes, and neurological disorders. As healthcare systems increasingly shift toward preventive and value-based care models, AI-enabled wearable platforms offer strong potential to improve outcomes, optimize clinical resources, and reduce long-term healthcare costs.

Furthermore, the growing adoption of home healthcare and elderly care is creating substantial demand for wearable monitoring devices. Rapidly aging populations, rising prevalence of age-related chronic conditions, and increasing preference for aging-in-place solutions are driving the need for continuous, non-intrusive monitoring outside traditional hospital settings. Wearable devices enable real-time tracking of vital signs, mobility, and adherence, while providing caregivers and clinicians with timely alerts and remote visibility into patient health status. Expanding homecare services, supportive government policies, and increasing acceptance of digital health solutions among older adults further position wearable healthcare devices as essential tools in home-based and long-term care environments.

Category-wise Analysis

By Product Type, Smart Watches Dominate Globally Owing to High Clinical Utility and Broad Consumer Adoption

The smart watches segment is projected to dominate the global wearable healthcare devices market in 2026, accounting for a revenue share of 38.7%. This leadership is primarily driven by the multifunctional clinical utility of smartwatches, which integrate continuous heart rate monitoring, ECG, SpO2 tracking, sleep analysis, physical activity monitoring, and increasingly, arrhythmia detection and fall alerts within a single device. Smartwatches serve as a first-line wearable solution for both preventive health management and chronic disease monitoring, supporting widespread adoption across consumer, clinical, and enterprise healthcare settings.

High user acceptance, real-time health insights, seamless smartphone integration, and growing physician endorsement for remote monitoring applications further strengthen segment dominance. In addition, continuous innovation in sensor accuracy, battery life, AI-driven analytics, and regulatory-cleared health features supports sustained utilization. Expanding reimbursement pilots, employer wellness programs, and aging populations increasingly relying on connected health devices further reinforce smartwatches as the leading product category globally.

By Application, Remote Patient and Post-Surgical Care Dominates Globally Owing to Continuous Monitoring Needs

The remote patient and post-surgical care segment is projected to dominate the global wearable healthcare devices market in 2026, accounting for a significant revenue share of 46.60%. This dominance is attributed to the expanding use of wearable devices for continuous vital-sign monitoring, recovery tracking, early complication detection, and adherence management following hospital discharge. Wearables enable clinicians to monitor patients remotely, reducing hospital readmissions while improving outcomes for post-operative, cardiac, orthopedic, and chronic care patients. The increasing shift toward value-based care models, rising surgical volumes, and pressure on healthcare systems to reduce inpatient stays have accelerated adoption of remote monitoring solutions.

Additionally, advances in cloud connectivity, data interoperability with electronic health records, and AI-enabled alert systems have enhanced clinical confidence in wearable-based monitoring. Growing acceptance among providers, payers, and patients continues to support high utilization and recurring revenue generation within this application segment.

By Distribution Channel, Online Channel Dominates Globally Due to Accessibility and Digital Health Adoption

The online channel segment is expected to dominate the global wearable healthcare devices market in 2026, capturing a revenue share of 59.2%. This leadership is driven by increasing consumer preference for direct-to-consumer purchasing models, wider product availability, competitive pricing, and access to detailed product information and user reviews through digital platforms. Online channels enable manufacturers to rapidly scale distribution while reaching both urban and remote populations with limited access to physical retail or healthcare outlets.

The expansion of telehealth ecosystems, digital prescription models, and remote onboarding of wearable devices further supports online sales growth. Subscription-based services, bundled software offerings, and seamless device activation also enhance customer retention through online platforms. Strong logistics networks, flexible financing options, and growing trust in e-commerce for medical-grade devices continue to reinforce the online channel as the dominant distribution route globally.

Regional Insights

North America Wearable Healthcare Devices Market Trends

North America is expected to maintain its dominance in the global wearable healthcare devices market, accounting for an estimated 46.5% market share, supported by high technology adoption rates, strong digital health infrastructure, and early integration of wearable data into clinical workflows. The U.S. remains the primary contributor due to widespread availability of FDA-cleared wearable devices, strong penetration of remote patient monitoring programs, and high consumer awareness of preventive healthcare technologies.

The region benefits from favorable reimbursement initiatives for remote monitoring, strong presence of leading wearable device manufacturers, and extensive collaborations between healthcare providers, technology firms, and payers. Additionally, high smartphone penetration, employer-sponsored wellness programs, and growing adoption among aging populations continue to support sustained market leadership. Continuous innovation in AI-driven diagnostics and regulatory support for digital health further strengthen North America’s long-term growth outlook.

Europe Wearable Healthcare Devices Market Trends

Europe demonstrates steady and mature growth in the wearable healthcare devices market, supported by robust public healthcare systems, strong regulatory oversight, and increasing adoption of connected care solutions across countries such as Germany, the U.K., France, Italy, Spain, and the Nordic region. Rising prevalence of chronic diseases, aging populations, and growing emphasis on preventive care are driving sustained demand for wearable monitoring devices.

European healthcare providers prioritize clinical validation, data privacy, and cost-effectiveness, leading to gradual but consistent adoption of approved wearable technologies. Integration of wearables into national digital health strategies, along with expanding reimbursement pilots for remote monitoring, supports market expansion. While pricing pressures and regulatory complexity remain challenges, increasing standardization of digital health frameworks across the region continues to enable moderate, stable growth.

Asia Pacific Wearable Healthcare Devices Market Trends

Asia Pacific is projected to be the fastest-growing region, registering a CAGR of approximately 8.4%, driven by rising health awareness, expanding middle-class populations, and rapid digitalization of healthcare services. Key markets including China, India, Japan, South Korea, and Southeast Asian countries are witnessing accelerating adoption of wearable healthcare devices for fitness tracking, chronic disease management, and remote patient monitoring across both urban and semi-urban areas.

Government initiatives to strengthen healthcare infrastructure, increasing penetration of smartphones and internet connectivity, and growth of private healthcare providers are significantly boosting market growth. Medical tourism, improving affordability of wearable technologies, and expanding local manufacturing capabilities further support adoption. Enhanced practitioner training, favorable regulatory developments, and strong consumer demand position Asia Pacific as a critical growth engine for global wearable healthcare device manufacturers and solution providers.

Competitive Landscape

The global wearable healthcare devices market is moderately to highly competitive, with key participants including Koninklijke Philips N.V., Fitbit, Basis Science, Garmin, Medtronic, and Omron Corp. These companies reinforce their market positions through diversified wearable portfolios spanning diagnostic, monitoring, and therapeutic applications, supported by proprietary sensor technologies, advanced analytics software, and well-established global distribution, after-sales service, and clinical support networks across hospitals, homecare settings, and consumer health channels.

Market participants are increasingly focused on developing interoperable and data-driven wearable ecosystems that integrate vital-sign monitoring, chronic disease management, and remote patient monitoring capabilities to enhance clinical decision-making and patient outcomes. Strategic priorities include continuous product innovation, regulatory approvals in key markets, expansion of installed device bases, investments in digital health platforms and AI-enabled insights, geographic expansion into emerging economies, and partnerships with healthcare providers, insurers, and telehealth platforms to accelerate adoption and support long-term market growth.

Key Industry Developments:

- In December 2025, Neupulse announced a first-of-its-kind wearable device that has demonstrated significant reduction in tic frequency and urge among individuals with Tourette Syndrome, representing a major advancement in drug-free, non-invasive therapy. Developed with design and engineering support from Ensera Design, the discreet, user-friendly wearable integrates Neupulse’s neurotechnology into an everyday device that can be activated at the touch of a button.

- In December 2025, the Singapore-MIT Alliance for Research and Technology (SMART) launched a new research center focused on developing the world’s first wearable ultrasound imaging system for real-time monitoring of chronic conditions. Under the Wearable Imaging for Transforming Elderly Care (WITEC) project, the initiative aims to enable continuous, personalized diagnosis of conditions such as hypertension and heart failure.

Companies Covered in Wearable Healthcare Devices Market

- Koninklijke Philips N.V.

- Fitbit

- Basis Science

- Garmin

- Medtronic

- Omron Corp.

- Withings

- Vital Connect

- Polar Electro

- Everist Genomics

- Intelesens Ltd.

- Sotera Wireless

- Apple

- Others

Frequently Asked Questions

The global wearable healthcare devices market is projected to be valued at US$ 52.6 Bn in 2026.

The market is driven by the rising prevalence of chronic diseases, growing health awareness and preventive healthcare, rapid technological advancements (sensors, AI/ML, connectivity), and expanding remote patient monitoring demand.

The global wearable healthcare devices market is poised to witness a CAGR of 6.1% between 2026 and 2033.

Key opportunities include integration of AI and IoT for predictive health insights, expansion in emerging markets, and growing adoption of remote patient monitoring and telehealth ecosystems.