- Pharmaceuticals

- Medical Foods Market

Medical Foods Market Size, Share, and Growth Forecast 2026 – 2033

Medical Foods Market by Form (Pills, Powders, Liquids, Others), by Application (Chronic Kidney Disease [CKD], Alzheimer's Disease, Diabetic Neuropathy, ADHD, Depression, Orphan Diseases, Cancer, Others), Sales Channel, and Regional Analysis, 2026–2033

Medical Foods Market Size and Trend Analysis

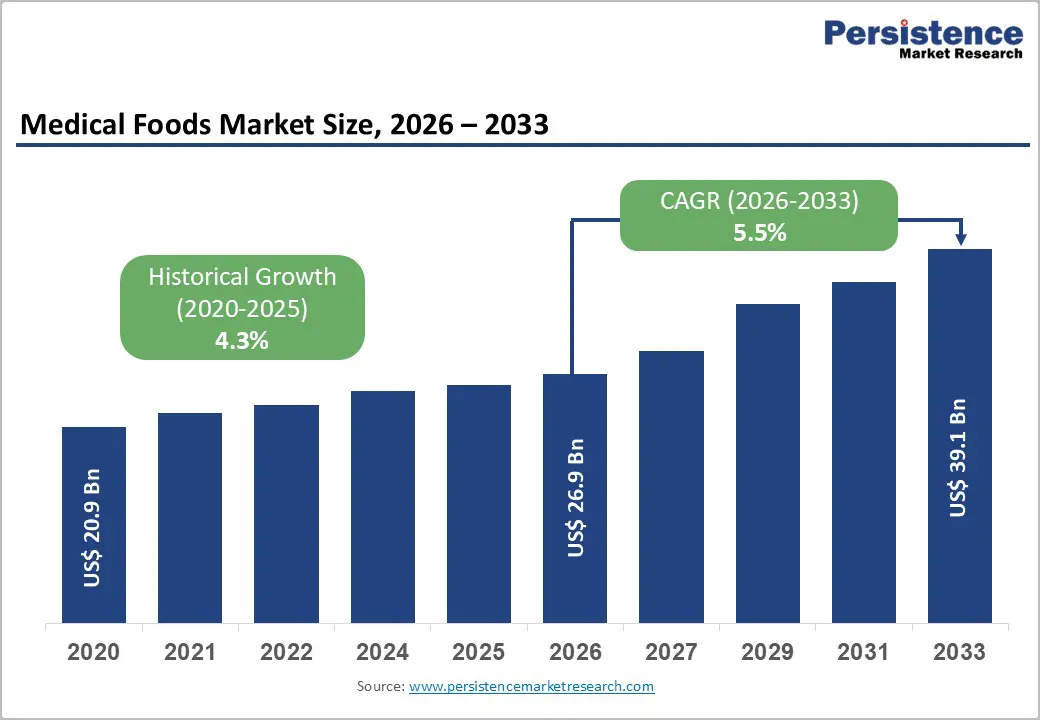

The global medical foods market size is expected to be valued at US$ 26.9 billion in 2026 and projected to reach US$ 39.1 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

The medical food market is evolving rapidly, driven by the rising prevalence of chronic conditions like Alzheimer’s, cancer, and diabetes. These specialized nutritional products, formulated under medical supervision, are gaining traction for their role in disease-specific dietary management. Increasing healthcare awareness, an aging population, and shifting preferences toward personalized nutrition further propel growth. Innovations in delivery formats such as powders, ready-to-drink solutions, and capsules enhance compliance and accessibility. Additionally, regulatory support and investment in clinical nutrition R&D are expanding therapeutic applications. As patient-centric care becomes a healthcare priority, the medical food market is poised for strong, innovation-led global expansion.

Key Industry Highlights

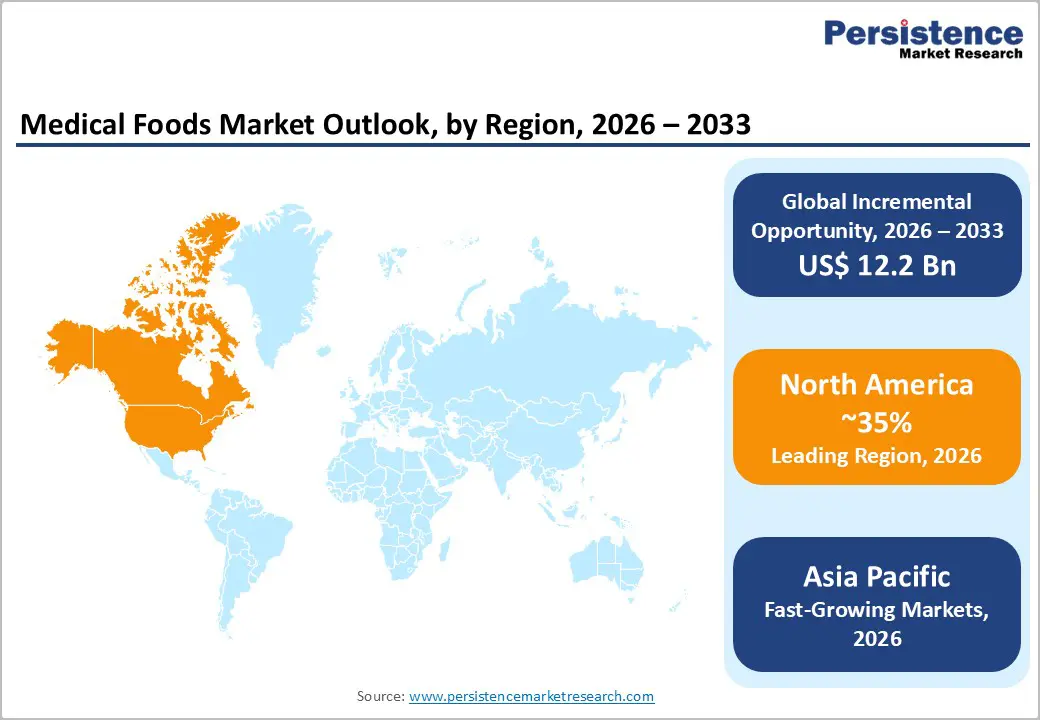

- Leading Region –North America is poised for ~35% of the global share in 2026, anchored by the U.S.'s FDA-regulated medical food framework, Medicare/Medicaid enteral nutrition reimbursement, and large chronic disease populations 37 million CKD and 34 million diabetes patients per National Kidney Foundation and CDC data.

- Fastest Growing Region –Asia Pacific is the fastest-growing Medical Foods region through 2033, driven by China's 130 million CKD patients per Chinese Society of Nephrology, Japan's aging population demand for FSMP products under MHLW regulation, and India's 77 million diabetes patients per IDF, representing a major untapped addressable market.

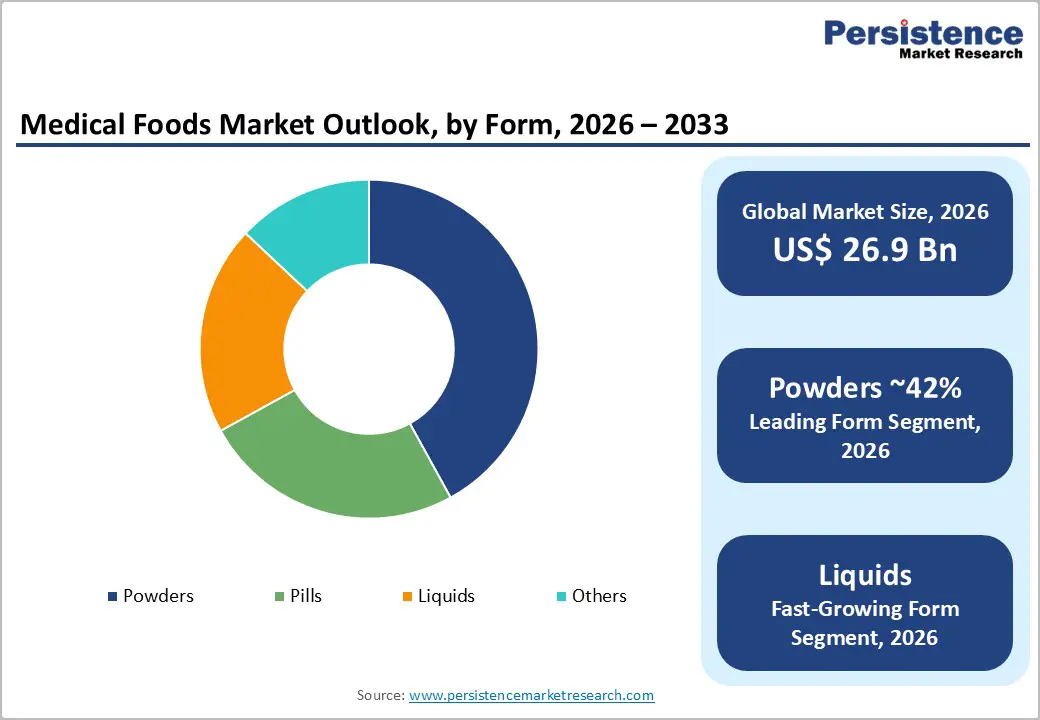

- Dominant Segment –Powders are likely to lead the form category with ~42% share in 2026, anchored by versatility for inherited metabolic disorders including phenylketonuria (PKU), extended shelf stability advantages, and cost-effective logistics enabling high-volume distribution across both premium and price-sensitive medical food markets globally.

- Fastest Growing Segment –Liquid medical foods are the fastest-growing form segment through 2033, driven by ESPEN-guideline-endorsed oral nutritional supplement adoption for malnutrition prevention, home enteral nutrition expansion, and growing consumer preference for ready-to-drink formats supported by Abbott's Ensure® and Nestlé Health Science's clinical nutrition portfolio.

- Key Opportunity: Asia Pacific's rapidly aging population, particularly China's 130 million CKD patients and Japan's world-leading elderly proportion, combined with expanding FSMP regulatory frameworks and private healthcare infrastructure, represents the most transformative geographic medical food market opportunity for global nutrition companies.

Market Dynamics

Drivers – Rise in Global Prevalence of Chronic Diseases Requiring Disease-Specific Nutritional Management

The accelerating global burden of chronic diseases for which specialized, condition-specific nutritional formulations are clinically indicated. The International Diabetes Federation (IDF) estimates that 537 million adults worldwide live with diabetes as of 2021, projected to reach 783 million by 2045, generating extensive demand for medical foods targeting diabetic neuropathy and metabolic management. The Global Burden of Disease Study estimates that 850 million people globally have chronic kidney disease (CKD), for whom protein-modified medical foods are often the cornerstone of pre-dialysis nutritional management. Alzheimer's disease is projected to affect 139 million people by 2050, per Alzheimer's Disease International (ADI), and the broader neurodegenerative disease burden further amplifies demand for medical foods specifically formulated to address disease-associated nutrient deficiencies and metabolic dysfunctions.

Restraints - Limited Reimbursement Coverage and Out-of-Pocket Cost Burden Constraining Patient Access

Reimbursement for medical foods remains limited and highly variable across healthcare systems, creating a significant patient access barrier that suppresses demand below the therapeutic need. In the United States, Medicare Part D generally does not cover oral medical foods for outpatient use, restricting reimbursed access primarily to tube-fed enteral nutrition products. The American Academy of Pediatrics (AAP) and patient advocacy groups have documented significant affordability challenges for families of children with inherited metabolic disorders, including phenylketonuria (PKU) who depend on amino acid-based medical foods. European reimbursement systems are more favourable in markets including the UK and Germany, but coverage gaps remain substantial across lower-income EU member states, limiting market penetration in potentially high-volume patient populations.

Opportunities - Liquid Medical Foods and Online Pharmacy Channels Emerging as High-Growth Revenue Corridors

Liquid medical foods encompassing ready-to-drink (RTD) enteral nutrition formulas, oral nutritional supplements (ONS), and disease-specific liquid formulations represent the fastest-growing product form segment, driven by growing home-based patient preferences, ease of administration, and expanding clinical validation for liquid ONS in reducing hospital malnutrition. ESPEN guidelines recommend ONS supplementation for at-risk patients across a broad spectrum of chronic diseases, generating consistent clinical demand for liquid formats. Simultaneously, the online pharmacy and e-commerce channel is the fastest-growing distribution segment, accelerated by the COVID-19 pandemic-driven shift to online healthcare purchasing, enabling direct-to-consumer access to specialized medical food products that are difficult to find in conventional retail settings. Companies including Nestlé Health Science and Abbott (Ensure®, Glucerna®) are investing heavily in digital direct-to-consumer channels, subscription models, and telehealth-integrated medical food prescription platforms to capture this rapidly expanding revenue opportunity.

Category-wise Insights

Form Analysis

Powders dominate the medical foods market by form, accounting for ~42% share in 2026. Powder-form medical foods maintain their leading position through versatility in dosing flexibility, extended shelf life compared to liquid formulations, and cost-effective production and logistics, particularly important for price-sensitive markets in the Asia Pacific and Latin America. Amino acid-based powdered formulas are the standard treatment for inherited metabolic disorders, including phenylketonuria (PKU), maple syrup urine disease (MSUD), and glutaric aciduria, where precise amino acid composition control is clinically essential. According to the National PKU Alliance (NPKUA), PKU-specific amino acid formula is the primary therapeutic intervention for the estimated 16,500 Americans living with PKU, and similar patient populations globally generate consistent, lifelong powder medical food demand that creates predictable recurring revenue for manufacturers such as Ajinomoto Cambrooke and Vitaflo International.

Sales Channel Insights

Drug stores & pharmacies represent the leading sales channel in the medical foods market, commanding ~38% of total channel revenue in 2026. This leadership reflects the clinical prescription-driven nature of medical food procurement most condition-specific medical foods are recommended by physicians, dietitians, or specialist nurses, directing patients toward pharmacy-based dispensing channels rather than general retail.

Hospital pharmacies and community pharmacies serve as the primary access points for patients prescribed medical foods for CKD, metabolic disorders, and neurological conditions. The FDA's position that medical foods must be used under physician supervision reinforces the pharmacy channel's dominant distribution role in the U.S. and most regulated markets. Chain pharmacies including CVS, Walgreens, and specialist pharmacy networks have expanded dedicated medical nutrition sections, further consolidating the channel's market position.

Regional Insights

North America Medical Foods Market Trends and Insights

North America leads the global medical foods market with ~35% share in 2026, driven by the United States' well-established regulatory framework for medical foods under FDA oversight, broad physician awareness of disease-specific nutritional management, and Medicare/Medicaid reimbursement for enteral nutrition products. The region benefits from a high density of specialist dietitians, active clinical nutrition research programs, and strong market presence of global medical nutrition leaders including Abbott and Nestlé Health Science.

U.S. Medical Foods Market Size

The United States accounts for ~90% of North American Medical Foods market revenue, anchored by the country's large chronic disease patient population 37 million Americans with CKD per the National Kidney Foundation, 34 million with diabetes per the CDC combined with established medical nutrition reimbursement infrastructure and high per-capita healthcare expenditure supporting premium medical food adoption.

Europe Medical Foods Market Trends and Insights

Europe is the second-largest medical foods market, characterized by well-developed regulatory harmonization under EU Regulation No 609/2013 on foods for special medical purposes and strong clinical nutrition infrastructure overseen by national dietetic associations and ESPEN guidelines. The region has mature reimbursement frameworks in Germany, France, and the UK that drive consistent institutional procurement, and growing awareness of medical nutrition among general practitioners and hospital-based dietitians sustains steady demand.

Germany Medical Foods Market Size

Germany leads the European medical foods market, accounting for ~22% of regional revenue in 2026. Germany's statutory health insurance (GKV) system provides structured reimbursement for FSMP products prescribed for specific medical conditions, and the country's high healthcare standards and dense specialist nutrition clinic network support consistent high-value medical food procurement, particularly for CKD, oncology nutrition, and metabolic disease applications.

UK Medical Foods Market Size

The UK accounts for ~19% of European market revenue, supported by NHS dietitian-directed prescribing of medical foods and structured ACBS (Advisory Committee on Borderline Substances) approval framework that enables NHS reimbursement for approved medical foods. The UK's active clinical nutrition research community including work published in Clinical Nutrition journal sustains evidence-based physician adoption of medical foods across inpatient and community settings.

France Medical Foods Market Size

France holds ~16% of European Medical Foods market share in 2025. France's Haute Autorité de Santé (HAS) regulates reimbursable FSMP products, and the country's network of hospital nutrition support teams established under national clinical nutrition plans drives consistent medical food prescribing, particularly for oncology, CKD, and elderly care nutritional support applications across French hospital systems.

Asia Pacific Medical Foods Market Trends and Insights

Asia Pacific is the fastest-growing regional market, driven by the world's largest CKD, diabetes, and aging patient populations concentrated across China, Japan, India, and South Korea. China is the region's largest national market the country's estimated 130 million CKD patients per Chinese Society of Nephrology data and rapidly expanding private hospital network are driving substantial medical nutrition demand, with domestic companies and international players including Nestlé and Abbott scaling operations. Regulatory modernization in China under the National Medical Products Administration (NMPA) is further facilitating FSMP market formalization and growth.

India Medical Foods Market Size

India accounts for ~15% of Asia Pacific medical foods market share, with the market driven by the country's 77 million diabetes patients (second globally per IDF), growing CKD prevalence, and expanding organized hospital nutrition support programs. The National Institute of Nutrition (NIN) and specialist dietitian associations are progressively raising physician awareness of FSMP-category medical foods across Indian clinical practice.

Japan Medical Foods Market Size

Japan contributes ~22% of Asia Pacific market shares the region's most mature FSMP market. Japan's Ministry of Health, Labour and Welfare (MHLW) classification of foods for special dietary uses (FOSDU) and foods with function claims provides a structured regulatory environment, while the world's highest elderly population proportion generates exceptional demand for medical foods addressing sarcopenia, dysphagia, CKD, and cognitive decline applications.

Southeast Asia Medical Foods Market Size

Southeast Asia accounts for ~12% of Asia Pacific medical foods market share, with Thailand, Indonesia, Malaysia, and Vietnam as key growth markets. Rising chronic disease prevalence, expanding private healthcare networks, and growing nutrition awareness among healthcare professionals are driving medical food adoption, with Indonesia's and Vietnam's large and rapidly expanding diabetic populations representing particularly significant long-term demand potential.

Competitive Landscape

The global medical foods market is moderately consolidated, with multinational nutrition leaders Nestlé Health Science, Abbott Laboratories (Ensure®, Glucerna®, Nepro®), Danone S.A. (Nutricia Advanced Medical Nutrition), and Fresenius Kabi AG collectively commanding dominant global market share through comprehensive product portfolios, extensive clinical evidence libraries, and global distribution networks. Key competitive differentiators include clinical evidence depth, dietitian and physician relationship management programs, hospital formulary inclusion, and regulatory approval breadth across multiple markets. Specialized players including Ajinomoto Cambrooke (metabolic disorder formulas), Targeted Medical Pharma, and Alfasigma compete in niche therapeutic segments. Emerging business trends include digital prescription platforms, telehealth-integrated medical food programs, and condition-specific product line extensions.

Key Developments:

- In April 2024, Nestlé India Limited and Dr. Reddy’s Laboratories Ltd, collectively referred to as the “JV Partners,” entered into a definitive agreement to form a joint venture (“JV Company”) aimed at bringing innovative nutraceutical brands to consumers in India and other agreed territories. The partnership combined the globally recognized range of nutritional health solutions, including vitamins, minerals, herbals, and supplements from Nestlé Health Science (NHSc) with the strong and established commercial strengths of Dr. Reddy’s in the Indian market.

- In November 2023, Danone launched its first medical nutrition product for adults in China, Fortimel, under the category of Foods for Special Medical Purposes (FSMP). This launch marked a significant milestone in Danone’s strategy to expand its presence in the Chinese healthcare market. By introducing Fortimel, Danone aimed to leverage its scientific expertise to support nutritional needs across all life stages, with a particular focus on advancing the adult medical nutrition segment.

Global Medical Foods Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 20.9 billion |

|

Current Market Value (2026) |

US$ 26.9 billion |

|

Projected Market Value (2033) |

US$ 39.1 billion |

|

CAGR (2026–2033) |

5.5% |

|

Leading Region |

North America, ~35% market share in 2026 |

|

Dominant Form |

Powders, ~42% market share in 2026 |

|

Top-ranking Application |

Chronic Kidney Disease (CKD), ~32% market share in 2026 |

|

Incremental Opportunity |

US$ 12.2 billion (2026–2033) |

Companies Covered in Medical Foods Market

- Nestlé Health Science

- Abbott Laboratories

- Danone S.A. (Nutricia Advanced Medical Nutrition)

- Fresenius Kabi AG

- Mead Johnson Nutrition (part of Reckitt Benckiser)

- Primus Pharmaceuticals, Inc.

- Targeted Medical Pharma, Inc.

- Medtrition, Inc.

- Metagenics, Inc.

- Alfasigma S.p.A.

- Ajinomoto Cambrooke, Inc.

- BioMedical Nutrition, Inc.

- Meiji Holdings Co., Ltd.

- B. Braun Melsungen AG

- Others

Frequently Asked Questions

The global medical foods market is projected to be valued at US$ 26.9 billion in 2026.

The global medical foods market is propelled by the rising prevalence of chronic diseases such as diabetes, cancer, and neurological disorders, which require condition-specific nutritional support.

North America leads the global market with ~35% of total market share in 2025.

Development of personalized nutrition aligned with genetic, microbiome, and metabolic profiles.

The Medical Foods market is led by Nestlé Health Science, Abbott Laboratories, Danone S.A., Fresenius Kabi AG, and Vitaflo International Ltd., among others, competing on clinical evidence, physician engagement, and regulatory approval breadth.