- Healthcare IT

- Medical Billing Outsourcing Market

Medical Billing Outsourcing Market Size, Share, and Growth Forecast, 2025 - 2032

Medical Billing Outsourcing Market By Component (Front-End Services, Middle-End Services), Service Type (Onshore Outsourcing, Offshore Outsourcing), End-user, and Regional Analysis for 2025 - 2032

Medical Billing Outsourcing Market Size and Trends Analysis

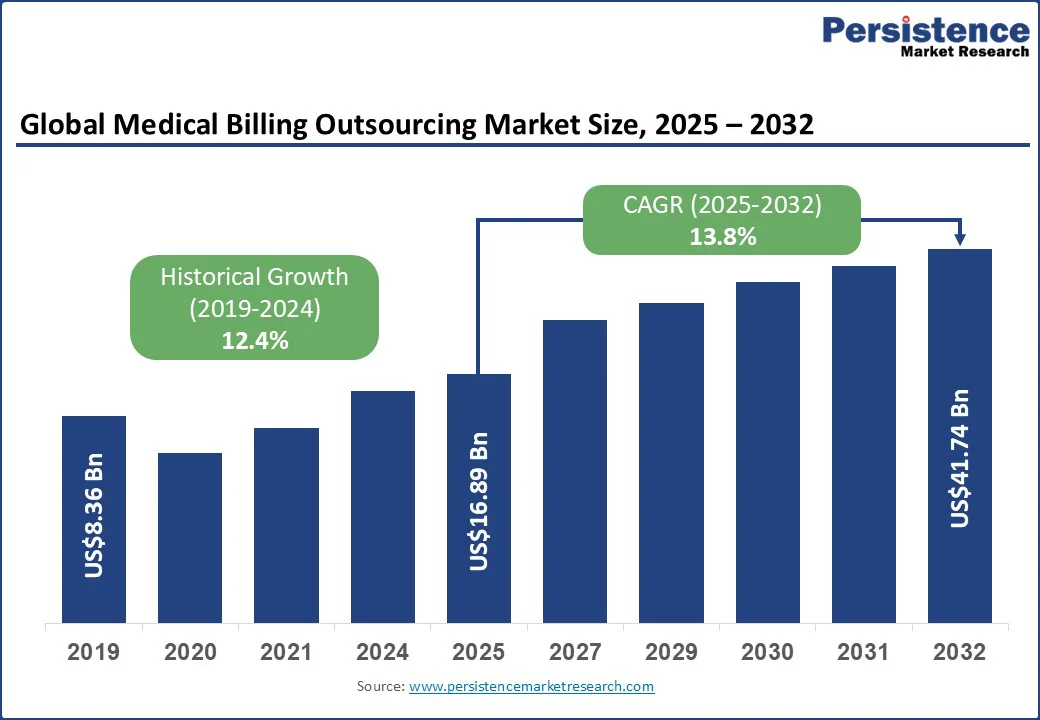

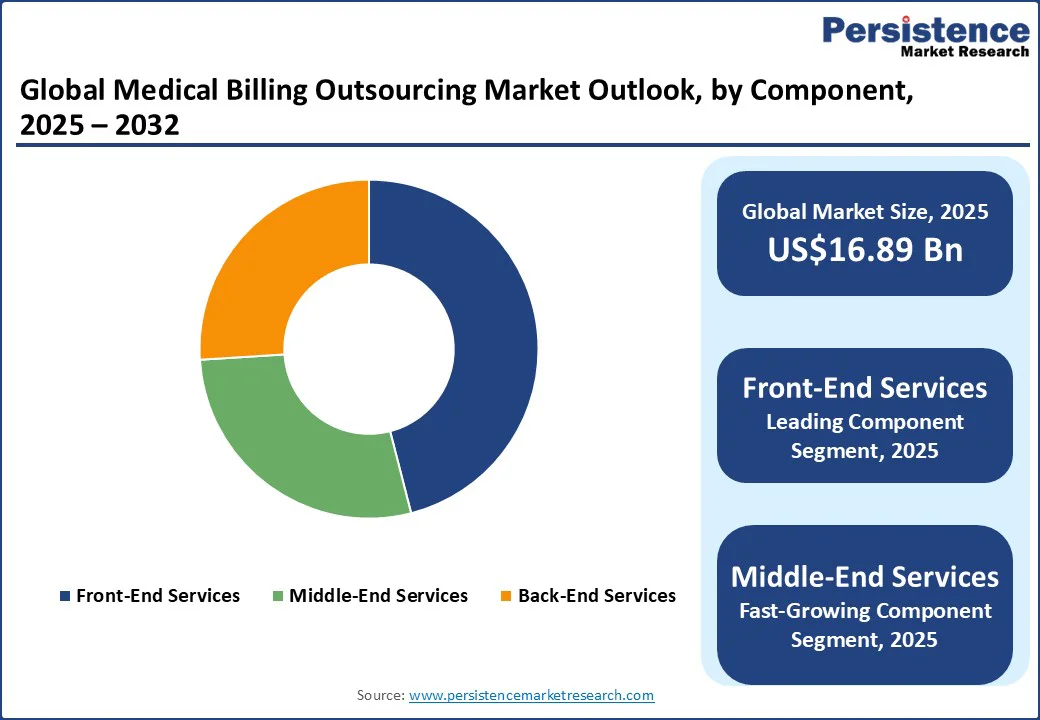

The global medical billing outsourcing market size is likely to be valued at US$16.89 Bn in 2025 and is expected to reach US$41.74 Bn by 2032, growing at a CAGR of 13.8% during the forecast period from 2025 to 2032.

Key Industry Highlights:

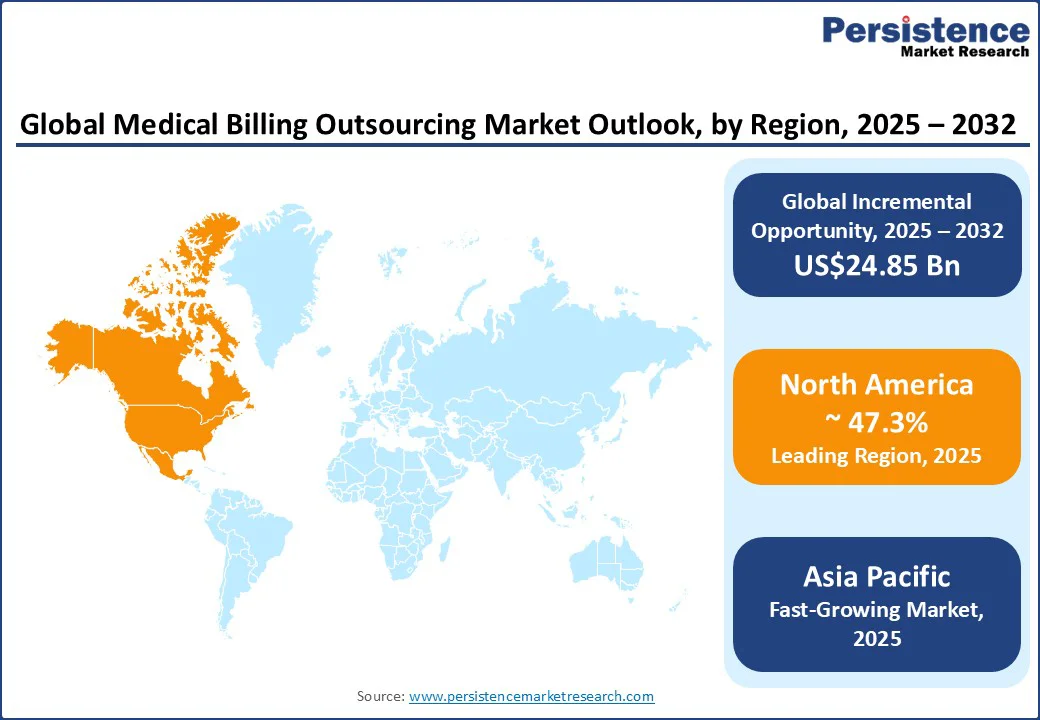

- Leading Region: North America is anticipated to dominate with a market share of 47.3%, driven by advanced healthcare infrastructure, strategic outsourcing partnerships, and the growing adoption of AI-driven revenue cycle management platforms.

- Fastest-growing Region: Asia Pacific is the fastest-expanding region, supported by its dual role as a global outsourcing hub and a rapidly evolving domestic healthcare outsourcing market, with strong contributions from India, the Philippines, China, and Japan.

- Dominant Component: Front-end services are anticipated to hold the largest market share of approximately 45.2%, as accurate patient registration and eligibility verification are critical to reducing claim denials.

- Leading End-user: Hospitals and health systems are anticipated to lead with a market share of 50.7%, due to high claim volumes and long-term outsourcing partnerships for revenue cycle management.

| Global Market Attribute | Key Insights |

|---|---|

| Medical Billing Outsourcing Market Size (2025E) | US$16.89 Bn |

| Market Value Forecast (2032F) | US$41.74 Bn |

| Projected Growth (CAGR 2025 to 2032) | 13.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 12.4% |

The medical billing outsourcing market is rapidly expanding, driven by the rising complexity of billing processes, regulatory requirements, and the growing demand for cost efficiency among healthcare providers.

Growth, Barriers & Opportunity Analysis

Outsourcing Surge Fueled by Specialized Billing Needs and Talent Shortage

The medical billing outsourcing market is expanding as healthcare providers increasingly require specialized expertise to manage complex front-end, middle-end, and denial-management workflows. Tasks such as payer-specific coding, pre-authorization, and denial-analysis remediation demand precision and deep familiarity with the evolving reimbursement models.

Outsourcing partners bring proven capabilities in charge-master optimization and compliance, which help hospitals and clinics minimize claim rejections and recover revenue more efficiently.

The rapid rise of telehealth services has also intensified the need for outsourcing, as virtual care billing requires mastery of new codes, reimbursement policies, and shifting payer rules that many providers struggle to address in-house.

The shortage of certified medical billing professionals is further accelerating outsourcing adoption across the industry. Skilled coders proficient in ICD-11 and value-based care documentation are in short supply, making it increasingly challenging for healthcare facilities to maintain effective in-house billing teams.

Demand is rising for integrated revenue cycle management platforms that leverage cloud computing and AI to automate claim scrubbing, eligibility checks, and coding validation while ensuring seamless interoperability with electronic health records.

Partnering with outsourcing providers enables healthcare organizations to access both advanced technology and specialized talent, positioning them to achieve higher efficiency, regulatory compliance, and financial performance.

Operational Misalignment and Data Security Risks Undermine Outsourcing Efficiency

Medical billing outsourcing often encounters limitations linked to coding integrity and workflow alignment. Healthcare providers rely heavily on accurate payer-specific coding, denial-management procedures, and charge reconciliation, yet outsourcing firms may interpret policies differently or face delays in adapting to frequent payer rule changes. This misalignment can lead to higher claim rejection rates, reimbursement delays, and additional administrative follow-ups.

Integration challenges also add complexity, as outsourced teams may work on platforms that are not fully compatible with a provider’s electronic health records or revenue cycle systems, which can slow down validation processes and reduce transparency in claims tracking.

Data security concerns are another significant restraint shaping market dynamics. Outsourcing inevitably involves transferring sensitive patient information, and centralized billing partners often become prime targets for cyberattacks.

High-profile breaches have revealed vulnerabilities in how protected health information is stored and transmitted, raising concerns about confidentiality, trust, and compliance with privacy standards. Beyond external threats, the risk of insider misuse and weak data anonymization practices within outsourcing firms adds another layer of vulnerability.

These security gaps jeopardize patient trust and also place providers at risk of reputational damage and potential financial penalties, limiting the pace at which organizations expand their reliance on outsourced billing solutions.

AI-Powered Billing Innovation and Emerging Market Expansion Unlock Growth Potential

The market is opening up new avenues through the integration of advanced technologies such as AI-driven denial management and predictive analytics. Service providers that can offer proactive solutions, such as identifying claims at risk of rejection before submission or generating tailored appeal letters using machine learning, are well-positioned to deliver measurable financial improvements for healthcare organizations.

These specialized capabilities streamline reimbursement cycles and also align with the shift toward value-based care, where precision in billing and faster resolution of denied claims are critical to sustaining profitability.

Emerging economies are also creating significant growth potential for outsourcing firms as healthcare infrastructure modernizes and digital health adoption accelerates. The expansion of telehealth services in regions such as Asia Pacific, Latin America, and the Middle East is generating a strong demand for expertise in telehealth-specific billing, remote consultation coding, and seamless integration with electronic health records.

Many providers in these markets lack the in-house expertise or scale to manage complex reimbursement requirements, making outsourcing an attractive option. Companies that deliver scalable, technology-enabled billing solutions tailored to these evolving markets stand to capture early advantage and build long-term partnerships with healthcare systems.

Category-wise Analysis

Component Insights

Front-end services are projected to dominate with an estimated 45.2% of the market share. These services include patient registration, eligibility and benefits verification, and pre-authorization, which are critical to minimizing downstream errors and avoiding claim denials. The demand for outsourcing front-end functions continues to rise as inaccuracies at this stage can lead to significant revenue losses and extended accounts receivable cycles.

Hospitals and healthcare systems increasingly depend on outsourcing providers to manage these processes at scale, ensuring smoother patient access and stronger financial outcomes. Companies such as R1 RCM have highlighted success stories, where outsourced front-end management reduced denial rates and enhanced cash flow, demonstrating why this segment maintains its leadership position.

Middle-end services are emerging as the fastest-growing component. This segment covers medical coding, charge capture, and claim scrubbing, all of which are becoming more complex due to evolving payer rules, the adoption of ICD-11, and the rise of value-based payment models.

Healthcare providers are turning to outsourcing partners with deep coding expertise and AI-enabled platforms that can improve accuracy and reduce revenue leakage. For example, providers that partner with vendors such as Optum or R1 for coding and claim validation have reported significant improvements in reimbursement timelines and reduced reliance on appeals.

This rising complexity and proven efficiency gains position middle-end outsourcing as the highest-growth area within the component segmentation.

End-user Insights

Hospitals and health systems are likely to dominate the market with a share of approximately 50.7% in 2025. These organizations manage large claim volumes across inpatient, outpatient, and specialty service lines, making them the most dependent on outsourced billing support.

The shortage of in-house coding professionals and the scale of their administrative burden further push hospitals to rely on outsourcing partners. Large health systems, such as Ascension, have entered into strategic agreements with vendors such as R1 and Optum to manage their revenue cycle operations, illustrating how outsourcing enables hospitals to maintain financial stability and improve operational efficiency. Their share remains the largest as the financial and operational benefits are particularly compelling at the hospital level.

Physician groups and other ambulatory care providers represent the fastest-growing end-user segment. Their adoption of outsourcing is accelerating rapidly as outpatient care expands and telehealth billing requirements grow more complex. Smaller practices often lack the internal resources to hire certified coders or invest in advanced billing platforms, which makes outsourcing a cost-effective and scalable solution.

Ambulatory practices are especially leveraging outsourced billing partners to handle telehealth-specific coding and remote monitoring claims, areas where expertise is scarce but reimbursement opportunities are significant. This rapid shift toward outsourcing in the physician and clinic segment highlights why it is expected to grow at the fastest pace within the end-user category.

Regional Insights

North America Medical Billing Outsourcing Market Trends - Strategic Outsourcing Drives Efficiency amid Telehealth and RCM Modernization

North America continues to lead with a market share of approximately 47.3%, supported by its mature healthcare infrastructure and the rising demand for automation in revenue cycle management (RCM). The U.S. market, in particular, is witnessing large-scale partnerships between health systems and outsourcing providers.

For example, Ascension Health expanded its multi-year agreement with R1 RCM to manage its end-to-end revenue cycle, reflecting a trend where outsourcing is becoming a strategic lever rather than a transactional service.

Another noteworthy development is the growing reliance on outsourcing firms to handle telehealth billing, as insurers in the U.S. continue to adjust coverage policies for virtual consultations and remote monitoring. Providers are increasingly outsourcing to firms that specialize in payer-specific telehealth coding and compliance management, ensuring fewer delays in reimbursements.

In Canada, the shift toward digital-first healthcare delivery is accelerating outsourcing adoption as private clinics, imaging centers, and community hospitals seek billing partners that can align with electronic claims processing systems. This is particularly critical in provinces such as Ontario, where digital health expansion has created a surge in outpatient and diagnostic claims, pushing smaller facilities to outsource for both efficiency and accuracy.

Asia Pacific Medical Billing Outsourcing Market Trends - Outsourcing Engine and Expanding Healthcare Market

Asia Pacific stands out as the fastest-growing region, driven by its role as both a global outsourcing hub and a growing consumer of outsourced services. India and the Philippines remain the backbone of offshore outsourcing, providing a steady pipeline of certified coders, billing specialists, and denial management experts to North American and European providers.

Companies, including Omega Healthcare and GeBBS Healthcare Solutions, are investing heavily in robotic process automation and AI-enabled tools to differentiate their offerings and increase claim resolution efficiency.

In India, domestic demand is also rising as private hospital chains outsource billing to focus on scaling patient care in urban centers. The Philippines has also positioned itself as a preferred location for back-end billing services due to its English-speaking workforce and cultural alignment with Western healthcare systems.

Beyond the service provider perspective, end-user adoption is also picking up in major Asian economies. In China, large tertiary hospitals are outsourcing claims processing to streamline insurance reimbursement amid rapidly growing patient inflows, while in Japan, outsourcing is helping address chronic workforce shortages in billing departments.

Japanese providers are leaning on outsourced billing platforms that integrate with advanced electronic medical record systems, helping to maintain compliance while easing the burden on internal staff.

Europe Medical Billing Outsourcing Market Trends - Compliance-Centric Outsourcing Gains Traction in Fragmented Healthcare Systems

Europe presents a distinctive landscape where compliance and data protection play as important a role as cost efficiency. The U.K. has seen a growing number of NHS trusts and private hospitals outsource billing functions to reduce backlogs created by staff shortages and post-pandemic care surges. Recent contracts with private outsourcing firms highlight a broader acceptance of external partnerships to sustain financial continuity in publicly funded healthcare systems.

Germany’s highly regulated DRG-based reimbursement model has made billing complex, encouraging both private hospitals and specialty clinics to work with outsourcing providers who can offer expertise in coding precision and denial prevention. France is experiencing growing adoption among diagnostic labs and small clinics, where administrative workloads are high but internal resources remain limited.

These providers are increasingly turning to outsourcing firms that can manage claims under multi-payer systems while ensuring strict GDPR compliance. Across the region, vendors are also tailoring their solutions to local contexts, for example, by integrating with national eHealth initiatives in Germany or working with NHS digital frameworks in the U.K., to ensure both compliance and operational efficiency.

Competitive Landscape

The global medical billing outsourcing market is defined by a mix of global revenue cycle management companies, specialized billing firms, and technology-driven service providers. Leading players such as R1 RCM, Optum, GeBBS Healthcare Solutions, and Omega Healthcare dominate through long-term contracts with large health systems and physician groups. These companies are increasingly differentiating themselves through investments in automation, AI-powered coding tools, and advanced analytics to improve claim accuracy and reduce denial rates.

Smaller and mid-sized outsourcing firms are carving out niche positions by focusing on specific segments such as ambulatory care billing, telehealth claim management, or specialty practice coding. Many of these firms are leveraging cloud-based platforms and payer-specific expertise to deliver cost-effective solutions, particularly for physician groups and diagnostic centers.

Key Industry Developments

- In August 2025, Narayana Health rolled out Aira, an AI-powered clinical documentation assistant built on their in-house EMR platform, Athma. While primarily focused on reducing doctors’ paperwork, Aira also strengthens the accuracy and completeness of documentation, a foundational component of accurate billing and streamlined revenue cycle management.

- In March 2025, R1 RCM collaborated with Palantir to launch R37, an AI-driven innovation lab dedicated to automating medical coding and denial management. This initiative reflects a broader shift toward integrating machine learning into operational RCM infrastructure to expedite claims resolution and minimize administrative overhead.

Companies Covered in Medical Billing Outsourcing Market

- R1 RCM Inc.

- Optum (UnitedHealth Group)

- Omega Healthcare

- GeBBS Healthcare Solutions

- Cognizant Technology Solutions

- Accenture Plc

- Veradigm (formerly Allscripts Healthcare Solutions)

- Cerner Corporation (Oracle Corporation)

- McKesson Corporation

- athenahealth, Inc.

- NextGen Healthcare, Inc.

- Experian Health

- MiraMed Global Services (now part of Coronis Health)

- Coronis Health

- Conifer Health Solutions

- Change Healthcare (UnitedHealth Group/Optum)

- Hinduja Global Solutions (HGS Healthcare)

- Pyramid Healthcare Solutions

- Quest Diagnostics (RCM services segment)

- CareCloud, Inc.

Frequently Asked Questions

The medical billing outsourcing market is estimated to reach US$16.89 Bn in 2025.

By 2032, the medical billing outsourcing market is projected to reach US$41.74 Bn.

Key trends include the integration of AI in coding and denial management, long-term outsourcing contracts between health systems and RCM vendors, increasing demand for telehealth billing expertise, and the rise of offshore outsourcing hubs in India and the Philippines.

By component, front-end services lead the market, as accurate eligibility verification and patient registration are critical to reducing claim denials. By end-user, hospitals and health systems lead due to their large claim volumes and reliance on outsourcing partners for revenue cycle efficiency.

The medical billing outsourcing market is anticipated to grow at a CAGR of 13.8% between 2025 and 2032.

Some leading players with strong portfolios include R1 RCM Inc., Optum (UnitedHealth Group), Omega Healthcare, GeBBS Healthcare Solutions, and Cognizant Technology Solutions.