- Hardware & Software IT Services

- Healthcare Revenue Cycle Management Software Market

Healthcare Revenue Cycle Management Software Market Size, Share, and Growth Forecast, 2026 – 2033

Healthcare Revenue Cycle Management Software Market by Deployment Type (Cloud-based, On-Premises, Others), Product Type (Integrated Software, Service, Others), Application (Pharmaceutical & Biotechnology, Cosmetics & Personal Care, Food & Beverages, Agriculture, Chemical Manufacturing, Electronics & Energy), and Regional Analysis for 2026-2033

Healthcare Revenue Cycle Management Software Market Share and Trends Analysis

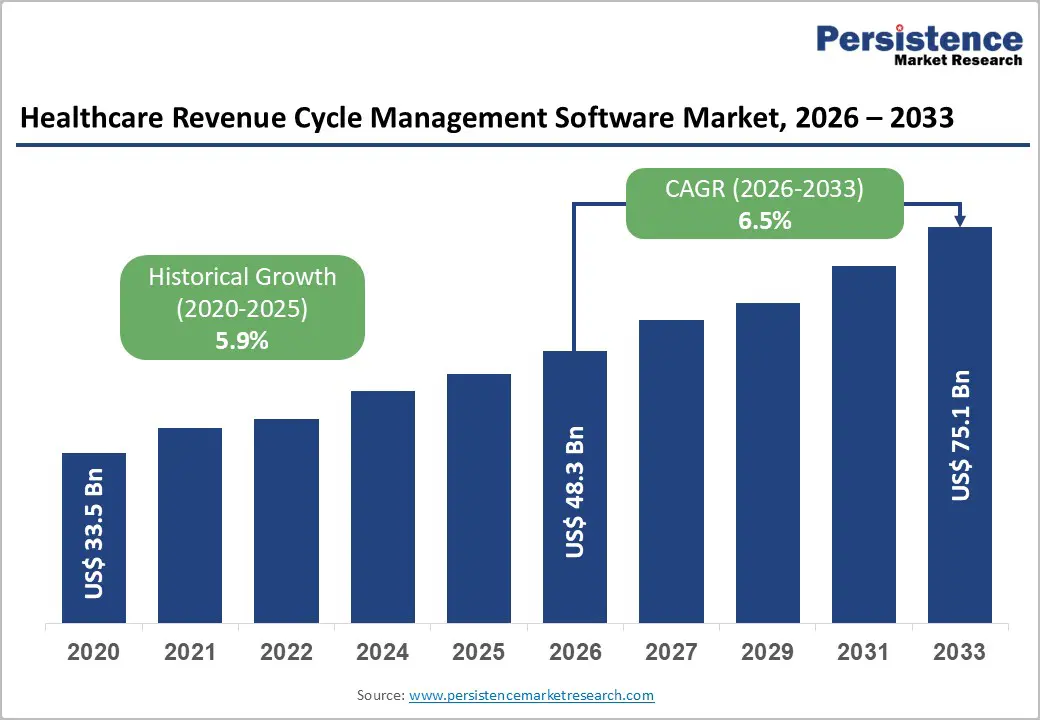

The global healthcare revenue cycle management software market size is likely to be valued at US$ 48.3 billion in 2026, and is projected to reach US$ 75.1 billion by 2033, growing at a CAGR of 6.5% during the forecast period 2026−2033. Revenue integrity, reimbursement velocity, and compliance enforcement increasingly define provider financial sustainability across public and private healthcare systems. Aging population growth, rising chronic disease prevalence, and expanding procedural complexity elevate billing volumes, documentation intensity, and payer interactions, directly increasing reliance on automated revenue cycle platforms.

Clinical awareness related to documentation accuracy and coding precision strengthens alignment between care delivery workflows and reimbursement optimization objectives. Technology integration across Electronic Health Records (EHR), clinical decision support platforms, and payer connectivity frameworks enables end-to-end revenue visibility while reducing exposure to manual intervention. Cloud-based deployment models, Artificial Intelligence (AI)–enabled coding automation, and analytics-driven denial prevention enhance operational resilience across hospitals, physician groups, and ancillary service providers.

Key Industry Highlights

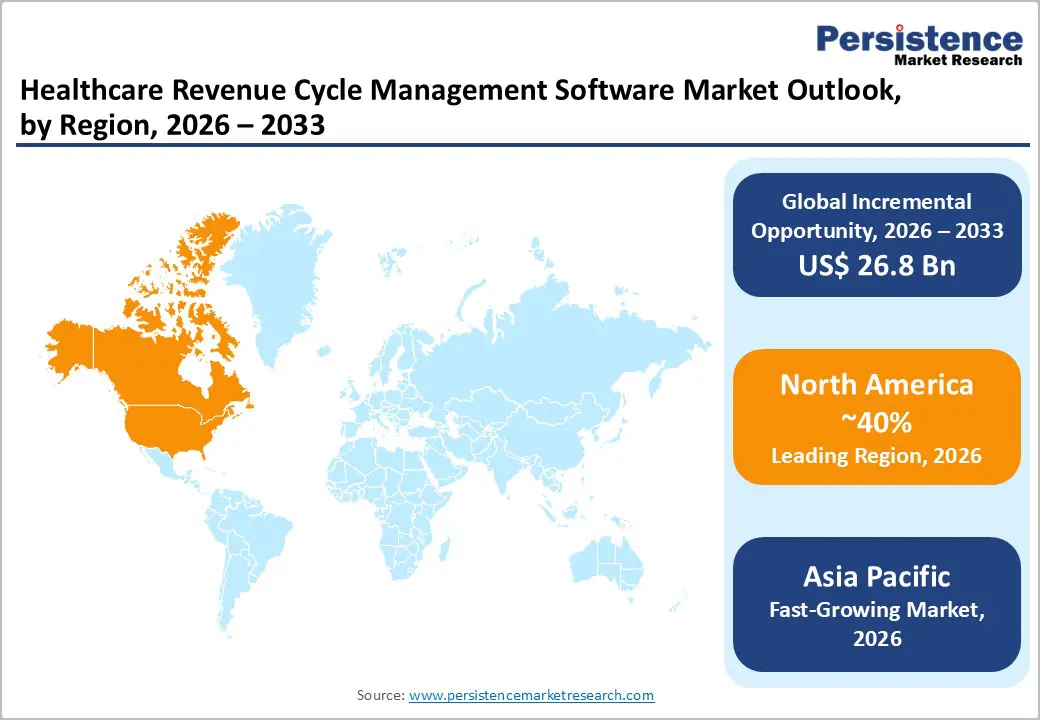

- Dominant Region: North America is expected to dominate in 2026 with 40% market share due to high adoption of automated, interoperable, and compliance-driven revenue cycle solutions.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033 owing to healthcare infrastructure expansion, expanding insurance coverage, and hospital digitization.

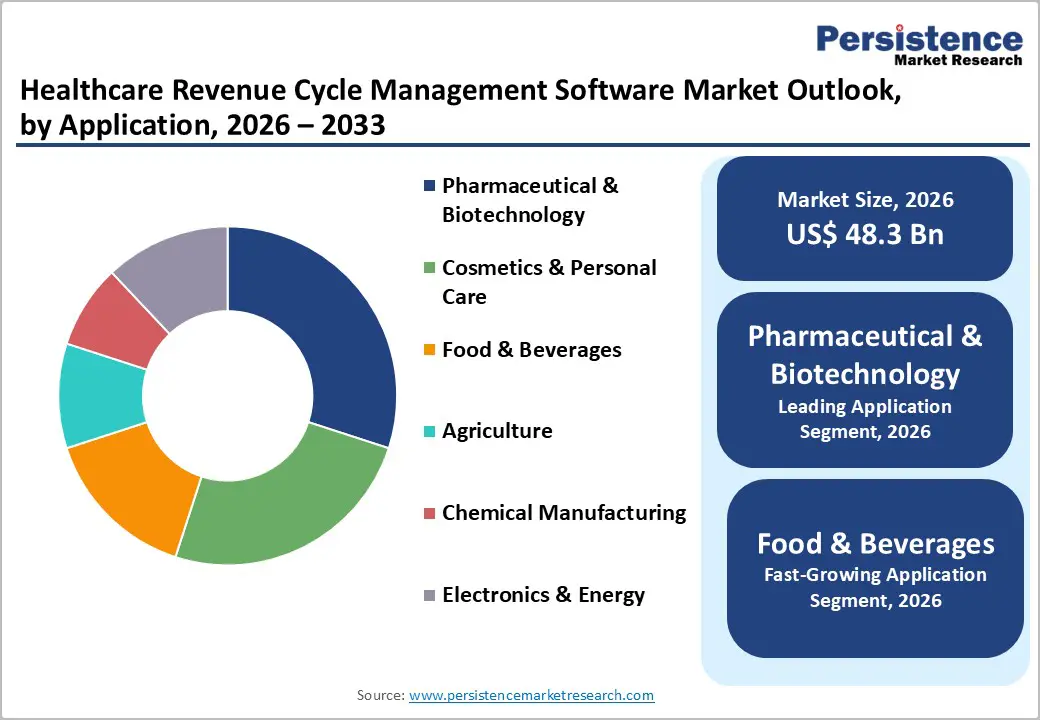

- Leading Application: Pharmaceutical and biotechnology applications are projected to lead in 2026 with about 30% revenue share, driven by high regulatory compliance, complex billing, and integration with clinical and specialty drug systems.

- Fastest-growing Application: Food and beverages are expected to be the fastest-growing through 2033, supported by integration of wellness services and corporate health programs.

- January 2026: Waystar introduced agentic AI capabilities to its cloud-native revenue cycle platform, advancing toward an autonomous revenue cycle that orchestrates automated workflows to reduce denials, accelerate prior authorizations, and enhance claims accuracy.

| Key Insights | Details |

|---|---|

|

Healthcare Revenue Cycle Management Software Market Size (2026E) |

US$ 48.3 Bn |

|

Market Value Forecast (2033F) |

US$ 75.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Administrative Complexity in Healthcare Reimbursement

Escalating reimbursement rules reshape financial operations across healthcare delivery organizations. Government estimates show that Medicare Fee-for-Service recorded an improper payment amount of US$ 28.83 billion in fiscal year 2025 due to insufficient documentation, inaccurate coding, and administrative errors, highlighting the scale of reimbursement complexity within public health programs. The reimbursement process requires providers to conform to a multitude of payer-specific coverage rules, coding standards, and eligibility checks, increasing administrative workload and creating costly claim adjustments. Billing workflows involve navigating complex procedural hierarchies such as hierarchical condition categories, diagnostic-related groups, and extensive modifier requirements, which extend claim adjudication cycles and raise error probability that triggers post-submission reviews and appeals. Administrative operations, therefore, depend on automated validation, rule-based engines, and documentation management systems to align submitted claims with compliance criteria defined by government payers.

The interaction between reimbursement policies and provider revenue flow reflects high financial exposure linked to administrative complexity. Differing documentation requirements across Medicare, Medicaid, and private payers create inconsistent revenue timing and elevate denial frequency when claims lack precise supporting clinical and procedural data. This inefficiency reduces operational predictability and raises staff costs as teams allocate substantial effort to correction and resubmission activities. Standardization and automation of critical administrative steps improve transparency and reduce manual friction in provider-payer exchanges, strengthening financial accuracy and stability. Technology-enabled rule interpretation, real-time eligibility verification, and structured clinical documentation capture shorten turnaround timelines and lower error exposure, supporting consistent revenue realization and fiscal accountability across care delivery organizations.

Data Privacy Concerns Limit Adoption

Data privacy sensitivity acts as a structural adoption barrier as revenue cycle platforms process large volumes of personally identifiable information, clinical records, insurance identifiers, and financial data across multiple internal and external stakeholders. Centralization of this information within integrated platforms elevates exposure to cyber threats, unauthorized access, and data misuse, increasing perceived risk among healthcare providers. Regulatory frameworks governing health information protection impose strict obligations related to consent management, data residency, auditability, and breach notification, raising compliance complexity for software deployments. Variations in privacy regulations across jurisdictions further complicate multi-location implementations, particularly for provider networks and third-party service partners. Decision-makers often view these regulatory and security obligations as operational liabilities that outweigh short-term efficiency gains, slowing procurement cycles and deployment approvals.

Risk aversion intensifies as revenue cycle systems interface with electronic health records, payer portals, and cloud infrastructure, expanding the attack surface across interconnected digital ecosystems. Concerns surrounding vendor accountability, subcontractor access, and cross-border data transfer heighten scrutiny during vendor selection processes. Limited internal cybersecurity capabilities within small and mid-sized healthcare organizations amplify dependence on external vendors, reinforcing hesitation toward cloud-based or Artificial Intelligence (AI)–enabled solutions that rely on continuous data ingestion and algorithmic processing. High-profile data breaches within healthcare environments reinforce reputational risk considerations, influencing executive and board-level resistance to rapid platform adoption.

AI Integration Opens Predictive Pathways

Predictive analytics-powered AI has created measurable foresight from complex operational and clinical data streams, enabling administrative leaders to anticipate outcomes rather than react to them. Public health reporting indicates that hospitals increasingly adopt predictive AI tools embedded in electronic health records. For instance, in 2024, according to a survey, 71% of hospitals reported using predictive AI, with rapid growth in revenue-related applications such as billing and claims forecasting. This integration aligns analytic outputs with key operational levers, such as coding accuracy, denial likelihood, and cash-flow timing, thereby increasing precision in functions that were historically manual and error-prone, thereby strengthening financial performance and the compliance posture.

The ability to translate retrospective patterns into forward-looking insights is valuable because it reduces uncertainty and operational risk while focusing resources where they matter most. Predictive models analyze historical claims and payer behavior to surface high-risk claims before submission, enabling targeted review and remediation, accelerating reimbursements and limiting costly denials. These systems also enrich documentation quality by signalling inadequate clinical narratives or divergent coding patterns, thereby tightening compliance with regulatory frameworks and payer requirements. On the financial planning side, forecasting reimbursement timelines and revenue trends drives more reliable budgeting and liquidity management, supporting provider sustainability in a landscape of tightening margins and evolving payment models.

Category-wise Analysis

Deployment Type Analysis

Cloud-based solutions are anticipated to secure around 45% of the healthcare revenue cycle management software market share in 2026, reflecting widespread adoption driven by accessibility, scalability, and operational efficiency. Providers increasingly prefer cloud platforms because they enable centralized management of patient records, claims, and billing. Interoperability with existing electronic health record (EHR) systems enhances workflow automation and reduces administrative burdens. Cloud deployment facilitates rapid updates, regulatory compliance integration, and remote access, which are critical for multi-location hospitals and clinics. Cost predictability through subscription-based models supports financial planning, while advanced security protocols ensure data protection. High clinical acceptance and provider preference for flexible deployment models reinforce dominance.

On-premises deployment is expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by demand from large healthcare institutions with complex IT infrastructure requirements. These systems offer customized configurations, enhanced data control, and integration with legacy software, appealing to providers seeking robust internal solutions. Growth is further fueled by investments in secure local servers, adherence to internal IT policies, and strategic prioritization of data sovereignty. Adoption trends indicate that hybrid deployment models may also emerge, combining on-premises stability with cloud scalability.

Product Type Insights

Integrated software extracts are poised to dominate with a forecasted market share of over 50% in 2026, powered by comprehensive functionality that combines billing, claims management, reporting, and analytics. Providers benefit from a unified platform that reduces operational silos, ensures consistent compliance, and improves revenue capture efficiency. Integrated solutions streamline end-to-end financial workflows, from patient registration to reimbursement collection, and enhance provider confidence in managing complex transactions. Adoption is strengthened by interoperability with clinical systems, automated coding verification, and intelligent claim adjudication. Stakeholders report improved accuracy, faster revenue realization, and reduced administrative overhead.

Services are expected to be the fastest-growing segment from 2026 to 2033, driven by outsourcing among smaller hospitals, clinics, and specialty care providers. Managed revenue cycle services, consulting, and cloud-based support allow organizations to leverage expertise without extensive capital investment. The service segment benefits from increasing demand for operational efficiency, compliance assurance, and scalable solutions tailored to evolving patient volumes. The expansion of digital commerce and telehealth services further reinforces the potential for adoption.

Application Insights

Pharmaceutical and biotechnology applications are likely to be the leading segment, with a projected 30% share of the healthcare revenue cycle management software market in 2026, driven by high regulatory compliance requirements, large-scale patient billing, and complex reimbursement mechanisms. Providers in this sector rely on automated software to track claims, manage insurance interactions, and ensure timely payments. Integration with clinical trial management and specialty drug distribution systems enhances operational efficiency. Digitalization, data-driven decision-making, and regulatory adherence collectively strengthen adoption, while technology-enabled service delivery improves transparency and accuracy across financial workflows.

Food and beverages are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by increasing integration of health-related nutraceuticals, wellness services, and employee health programs. Revenue cycle management software streamlines billing for corporate wellness initiatives, dietary consultation services, and preventive health programs linked to consumer products. Adoption is strengthened by providers seeking cost efficiency, scalability, and actionable insights from integrated digital systems. Growth is particularly notable in markets emphasizing health-focused product lines and workplace wellness programs.

Regional Insights

North America Healthcare Revenue Cycle Management Software Market Trends

North America is expected to dominate with an estimated 40% of the healthcare revenue cycle management software market share in 2026, reflecting high adoption among hospitals, outpatient networks, and specialty providers. Dominance is primarily driven by the integration of complex healthcare delivery systems with sophisticated financial workflows. Large-scale hospital networks and multi-specialty clinics require automated solutions to manage claim adjudication, patient registration, billing reconciliation, and revenue forecasting. Advanced interoperability between financial systems and electronic health records enables seamless data exchange, reducing administrative bottlenecks and claim denials. Providers prioritize platforms that deliver real-time analytics, predictive revenue modeling, and intelligent denial management, enhancing operational efficiency while minimizing financial leakage. Regulatory enforcement creates an environment where compliance-driven software adoption is not optional but critical, reinforcing market penetration.

Dominance is also reinforced by strong digital infrastructure, high IT maturity, and concentrated healthcare expenditure, which collectively enable rapid deployment of cloud-based and integrated software solutions. Providers benefit from standardized billing codes, mature insurance networks, and advanced payer-provider interfaces, reducing the complexity of claims processing across diverse healthcare services. Strategic collaborations between software developers and large provider networks enhance adoption speed while ensuring compliance with evolving reimbursement guidelines. Operational efficiency gains from automated revenue cycle workflows create measurable improvements in cash flow, resource allocation, and patient satisfaction, establishing a clear value proposition. Market leaders leverage data-driven insights to optimize financial performance and scalability, reinforcing competitive positioning.

Europe Healthcare Revenue Cycle Management Software Market Trends

The market in Europe is set to demonstrate stable expansion through 2033 on account of universal healthcare systems, high regulatory standards, and widespread digitization initiatives. Adoption of healthcare revenue cycle management software is reinforced by complex reimbursement frameworks, standardized coding requirements, and multi-layered insurance systems that necessitate automated claim processing and financial tracking. Large hospital networks and multi-specialty clinics prioritize integrated and cloud-based platforms to enhance operational efficiency, reduce administrative bottlenecks, and improve cash flow management. Interoperability with electronic health records, telemedicine platforms, and patient management systems enables seamless coordination across clinical and administrative workflows. Strategic collaborations between software providers and healthcare consortia facilitate localized deployment, technical support, and compliance alignment, allowing rapid adoption across mature markets.

Investment in digital infrastructure, training programs, and modular software capabilities ensures scalable integration while maintaining adherence to national and European Union (EU)-level regulations. Growth is further reinforced by value-based care initiatives, expanding insurance coverage, and rising demand for analytics-driven financial management. Providers increasingly utilize software for predictive revenue modeling, intelligent denial management, and real-time financial reporting to optimize resource allocation and operational performance. Competitive dynamics favor vendors offering adaptable solutions, AI-assisted claim adjudication, and advanced reporting functionalities that address regulatory complexity. Public and private healthcare funding, modernization of hospital networks, and focus on cost-efficiency amplify adoption potential across diverse care settings.

Revenue Cycle Management Software Market Trends

Asia Pacific is forecasted to be the fastest-growing market for healthcare revenue cycle management software between 2026 and 2033, stimulated by rapid expansion of healthcare infrastructure, rising insurance coverage, and increasing digitization of hospital and outpatient operations. Growth is driven by large-scale modernization of hospital networks, which requires automated revenue cycle solutions capable of handling high patient volumes and complex claim processing. Providers are investing in cloud-based and AI-enabled platforms to streamline billing, reduce denials, and optimize revenue forecasting across decentralized networks. The adoption of electronic health records, telemedicine services, and remote care delivery further amplifies demand, as integrated financial systems become essential for coordinating reimbursement and operational efficiency. Public and private healthcare initiatives, supported by government funding, create opportunities for scalable deployment of software solutions tailored to local regulatory requirements. High patient inflow, growing chronic disease prevalence, and increasing outpatient service penetration reinforce adoption, providing a substantial addressable base.

Sustained growth is also propelled by rising IT maturity, investment in digital health infrastructure, and strategic collaborations between technology vendors and large hospital networks. Providers prioritize interoperability with clinical systems, real-time analytics for revenue performance, and automated compliance tools to navigate diverse reimbursement regulations. Expansion of health insurance schemes and increased awareness among healthcare administrators about operational efficiency drives software adoption beyond urban centers into semi-urban and tier-2 markets. Market players leverage cloud deployment, predictive analytics, and intelligent denial management to enhance cash flow and reduce administrative burden. Competitive dynamics favor vendors offering localized support, adaptive solutions, and training services, allowing rapid scalability and long-term client retention.

Competitive Landscape

The global healthcare revenue cycle management software market features a moderately fragmented structure with multiple global software vendors, regional specialists, and service-oriented providers, creating a competitive environment characterized by diverse offerings and overlapping capabilities. Leading companies such as McKesson Corp., Quest Diagnostics, Inc., athenahealth, Inc., Epic Systems Corporation, and EMC Corp. collectively hold a significant but non-dominant share, reflecting balanced market influence without monopolistic control. Competition within the Healthcare Revenue Cycle Management Software market is driven by the ability to deliver end-to-end revenue management solutions that integrate seamlessly with electronic health records, telemedicine platforms, and hospital financial systems. Vendors differentiate through depth of automation, enabling streamlined claim processing, intelligent denial management, and predictive revenue analytics.

Strategic positioning within the Healthcare Revenue Cycle Management Software market emphasizes technological sophistication, client-centric customization, and scalability. Companies like McKesson Corp. and Epic Systems Corporation leverage broad infrastructure integration and cloud capabilities to capture enterprise-scale clients, while athenahealth, Inc. and Quest Diagnostics focus on specialized modules and service-enabled solutions for targeted segments. EMC Corp. contributes with robust data management and analytics platforms, reinforcing operational efficiency. Providers compete not only on functional features but also on implementation support, training, and ongoing compliance assistance. The cumulative effect maintains high competitive intensity, with differentiation arising from software capability, client support, and regulatory adherence rather than market share dominance.

Key Industry Developments

- In October 2025, athenahealth launched AInative updates to its Revenue Cycle Management platform at no extra cost, embedding agentic artificial intelligence into core workflows to automate billing tasks, eliminate manual work, and improve claims accuracy and payment speed for tens of thousands of ambulatory providers.

- In June 2025, Knowtion Health acquired Switch RCM, combining its revenue recovery expertise with Switch’s data driven automation capabilities to enhance intelligent reimbursement solutions and accelerate cash recovery for healthcare providers.

- In May 2025, Infinx completed a US$ 96 million acquisition of i3 Verticals’ Healthcare Revenue Cycle Management business, securing proprietary technology and client relationships to expand its AI driven RCM portfolio and strengthen market presence in academic medical centers and large provider groups.

- In May 2025, New Mountain Capital launched Smarter Technologies, an artificial intelligence enabled revenue cycle management platform by combining three portfolio companies, Access Healthcare, SmarterDx, and Thoughtful.ai, aimed at automating administrative workflows and strengthening financial performance across healthcare organizations.

Companies Covered in Healthcare Revenue Cycle Management Software Market

- McKesson Corp.

- Quest Diagnostics, Inc.

- athenahealth, Inc.

- Epic Systems Corporation

- EMC Corp.

- CareCloud Corporation

- Greenway Health, LLC

- Allscripts Healthcare

- Solutions, Inc.

- Qsi Management LLC

Frequently Asked Questions

The global healthcare revenue cycle management software market is projected to reach US$ 48.3 billion in 2026.

Rising healthcare complexity, increasing patient volumes, and demand for automated, compliant, and efficient revenue processes are driving the market.

The market is poised to witness a CAGR of 6.5% from 2026 to 2033.

Widening adoption of AI-driven analytics, cloud-based solutions, and predictive revenue management are creating key market opportunities.

Some of the key market players include McKesson Corp., Quest Diagnostics, Inc., athenahealth, Inc., Epic Systems Corporation, and EMC Corp.