- Medical Devices

- Medical Alert Systems Market

Medical Alert Systems Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Medical Alert Systems Market by Product Type (Landline PERS, Mobile PERS, Standalone PERS), End-user (Home-based Users, Nursing Home, Assisted living facilities, Hospices, Others), and Regional Analysis from 2026 to 2033

Medical Alert Systems Market Share and Trends Analysis

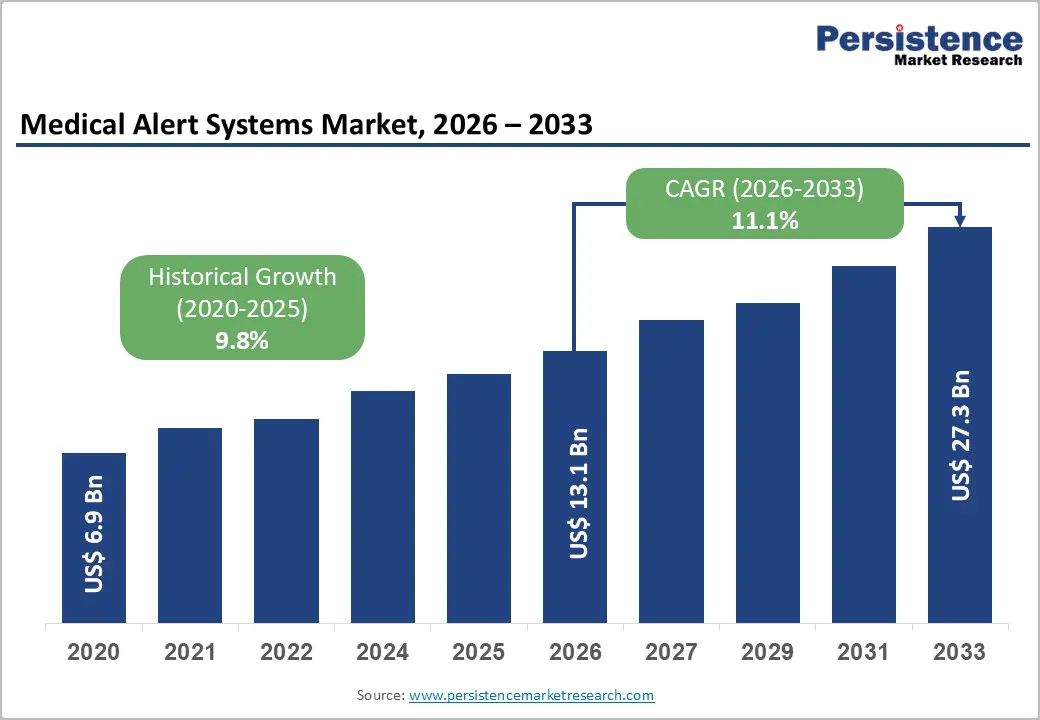

The global medical alert systems market is projected to grow from US$13.1 billion in 2026 to US$27.3 billion by 2033. The market is projected to grow at a CAGR of 11.1% from 2026 to 2033.

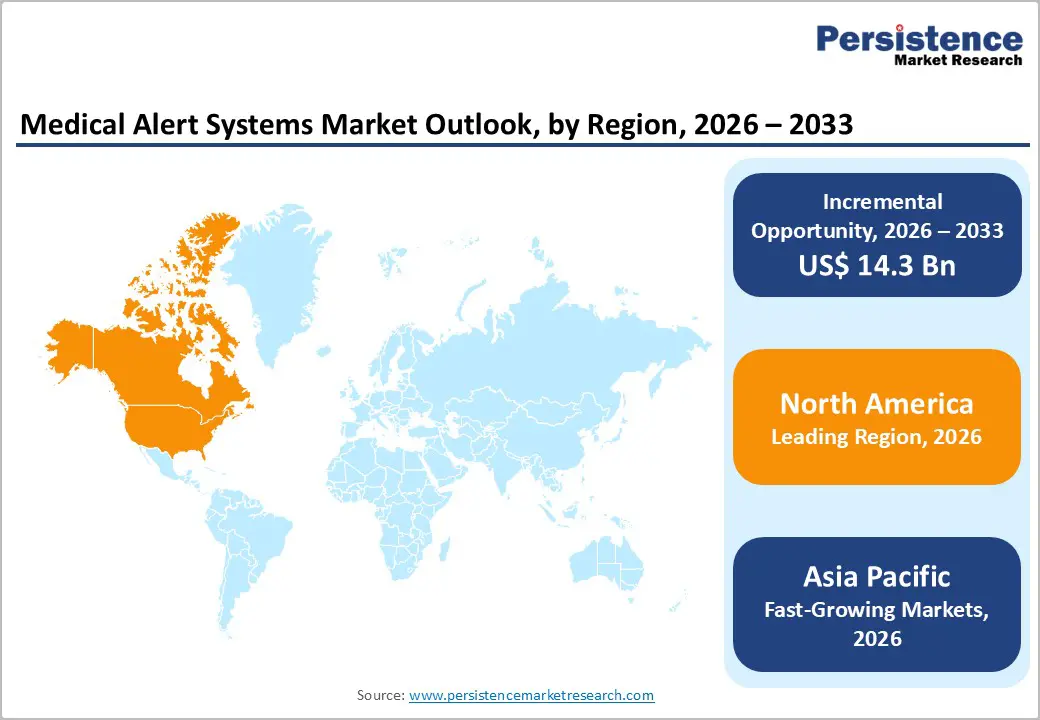

The medical alert systems market is growing rapidly, fueled by rising health awareness, smartphone penetration, and digital health adoption. North America leads with strong consumer spending, wearable device integration, and high app monetization, while Asia-Pacific shows the fastest growth, driven by increasing mobile users, fitness consciousness, affordable solutions, and expanding digital health infrastructure across the region.

Key Industry Highlights:

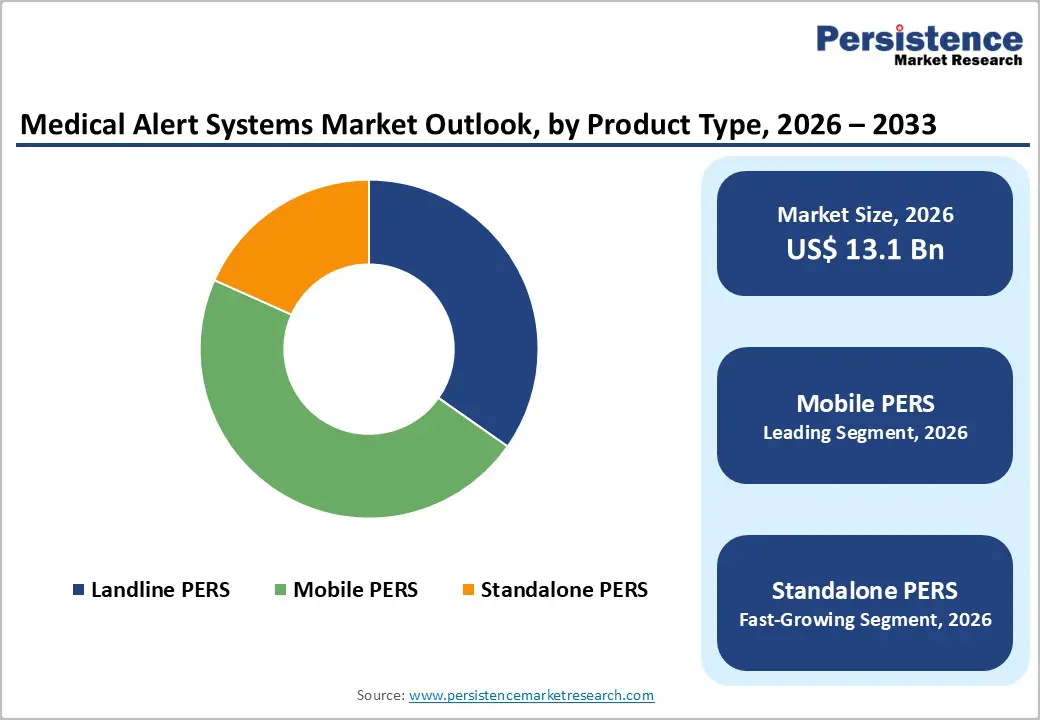

- Dominant Segment: Mobile PERS / Wearable alert devices dominated the medical alert systems market in 2025, holding 46.9% share due to rising demand for independent safety monitoring, fall detection, and on-the-go emergency response. Strong adoption was observed across home-based users, assisted living, and hybrid care models, supported by subscription-based monitoring services.

- Dominant Region: North America led in 2025 with 40.2% share, driven by high smartphone and wearable penetration, strong consumer spending, and early adoption of connected health technologies. Asia-Pacific emerged as the fastest-growing region, driven by expanding mobile adoption, rising health awareness, affordable devices, and expanding digital healthcare ecosystems.

- Market Drivers: Growth is driven by the aging population, rising rates of chronic and lifestyle-related health risks, proliferation of smartphones and wearables, demand for real-time safety monitoring, and increasing adoption of digital health solutions.

- Market Opportunity: Opportunities include deeper IoT and wearable integration, AI-enabled health monitoring, expansion into corporate and community health programs, penetration of emerging markets, partnerships with healthcare providers, and the development of holistic systems that integrate emergency response, health monitoring, and telecare features.

| Global Market Attributes | Key Insights |

|---|---|

| Medical Alert Systems Market Size (2026E) | US$ 13.1 Bn |

| Market Value Forecast (2033F) | US$ 27.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.8% |

Market Dynamics

Driver - Rise in Chronic & Lifestyle Diseases

The increasing prevalence of chronic and lifestyle-related diseases among older adults significantly elevates the risk of acute health events that require rapid emergency response. In the United States, conditions such as hypertension, arthritis, high cholesterol, and diabetes are highly prevalent among adults aged 85 and older, with over two-thirds reporting hypertension and nearly half reporting high cholesterol. Additionally, 37.3% of this age group have four or more chronic conditions, underscoring a heavy burden of multimorbidity that heightens emergency risks. Simultaneously, fall-related fatalities among adults aged 65+ reached approximately 69.9 deaths per 100,000 in 2023, highlighting how chronic conditions contribute to increased falls and emergency incidents requiring prompt response systems

In India, chronic conditions among the elderly are also rising, with an estimated 21% of elderly individuals having at least one chronic disease and around 23% experiencing multiple comorbid conditions such as hypertension and diabetes. These chronic illnesses contribute directly to increased incidents of falls and related injuries, as evidence shows that older adults with multiple chronic conditions have significantly higher odds of experiencing falls than those without. Globally, falls affect roughly 28-35% of individuals aged 65 and older annually, and chronic disease exacerbates this risk. This convergence of chronic disease prevalence and fall risk provides a clear, data-driven rationale for the increasing adoption of medical alert systems, which provide real-time monitoring and rapid response activation for high-risk individuals.

Restraints - High Device & Subscription Costs

High device prices and ongoing subscription fees significantly constrain the adoption of medical alert systems, particularly among older adults with fixed incomes. In the U.S., medical alert monitoring services typically cost between $20 and $55 per month, with additional upfront equipment fees ranging from minimal to several hundred dollars, depending on the provider and selected features. These recurring expenses compound over time; for example, a typical package can cost $350- $500 in the first year alone, even before add-ons such as GPS tracking or automatic fall detection are included. Many older adults and low-income households must prioritize essential living expenses such as food, housing, and healthcare, making long-term subscription costs difficult to justify.

Cost barriers are heightened by limited reimbursement options from public insurance or government programs. In the U.S., traditional Medicare (Parts A and B) does not cover most medical alert systems, leaving beneficiaries to pay out-of-pocket unless they have supplemental plans like Medicare Advantage or specific Medicaid waivers. This lack of universal coverage means that older consumers must bear substantial out-of-pocket expenses, deterring widespread market penetration. A consumer survey found that 1 in 4 older Americans who do not use a medical alert system cite cost as the primary reason, directly illustrating how affordability concerns restrict adoption even among populations that could benefit most.

Opportunity - Corporate & Community Wellness Programs

Corporate and community wellness programs present a significant opportunity for the medical alert systems market by extending safety-oriented monitoring beyond traditional senior care into broader health and productivity initiatives. More than 50% of U.S. employers now offer workplace wellness programs, with 84% of larger companies (200+ employees) reporting formal wellness initiatives designed to improve employee health and reduce the risk of chronic disease. These programs often include digital health tools and physical activity tracking that can integrate with medical alert systems to enable proactive safety monitoring, particularly for workers at elevated health risk. The potential for bundled solutions that combine wellness engagement with emergency response technology addresses employers’ rising interest in comprehensive health offerings.

Moreover, community health initiatives increasingly focus on preventive care, chronic disease management, and real-time monitoring, thereby creating a conducive environment for the adoption of medical alert systems outside formal healthcare settings. For example, local community programs that integrate smart health monitoring devices have achieved high user satisfaction for elderly adults accessing remote healthcare services and emergency support through digital platforms. Embedding medical alert capabilities into community wellness ecosystems, such as senior centers, fitness hubs, and public health collaborations, can enhance both preventive care and emergency responsiveness, broadening market reach while supporting public health goals.

Category-wise Analysis

By Product Type Insights

Mobile PERS dominates with 46.9% share of the global market in 2025, because widespread smartphone penetration and wearable integration make mobile emergency response more accessible and effective than traditional landline solutions. In the United States, over 80% of adults own a smartphone, and adoption among older age groups has been increasing rapidly, with 76% of adults aged 65+ owning one, enabling widespread use of mobile health tools and emergency features. Smartphones also serve as platforms for fall detection and real-time alerts, using built-in sensors such as accelerometers to detect falls and automatically transmit emergency signals. This ubiquity and functionality enable mobile PERS solutions to provide on-the-go protection, location tracking, and immediate connectivity without fixed infrastructure, thereby driving their market preference.

By End-user Insights

Home-based users dominate the medical alert systems market because most older adults prefer to age in place rather than move to institutional settings. In the United States, over 88% of adults aged 65 and older live in their own homes, making independent living the norm. Coupled with the high prevalence of falls, approximately one in four adults aged 65+ experience a fall each year, the need for immediate emergency response at home is critical. Medical alert systems provide real-time monitoring, fall detection, and rapid connection to caregivers or emergency services, enabling safety without requiring relocation. This combination of independent living preferences, a high risk of home incidents, and reliance on timely assistance keeps home-based users the dominant end-user segment for these systems.

Regional Insights

North America Medical Alert Systems Market Trends

North America dominates the medical alert systems market with 40.2% share in 2025, due to its rapidly aging population, high technology adoption, and advanced healthcare infrastructure. In the United States, adults aged 65 and older reached 61.2 million in 2024, representing about 18% of the population, creating strong demand for safety and emergency monitoring solutions. Older adults increasingly use smartphones, wearables, and digital services, with surveys indicating widespread adoption of health and safety apps among adults aged 50 and above. Coupled with high disposable incomes, insurance coverage, and well-established home healthcare networks, these factors enable easier access to medical alert systems. The combination of demographic trends, familiarity with technology, and supportive infrastructure solidifies North America’s leading market share in medical alert solutions.

Europe Medical Alert Systems Market Trends

Europe is an important region in the medical alert systems market because it has one of the fastest aging populations globally, creating strong demand for safety and emergency-oriented health technologies. In the European Union, the share of people aged 65 and over increased from about 16% in 2004 to over 21% in 2024, with projections reaching 29% by 2050 as life expectancy rises and fertility rates fall. This demographic shift means a growing proportion of older adults are at higher risk of falls, chronic conditions, and medical emergencies that benefit from alert systems. Furthermore, countries such as Italy and Portugal report nearly 24% of their populations aged 65+, underscoring regional demand for solutions that support independent living and rapid emergency response.

Asia Pacific Medical Alert Systems Market Trends

Asia-Pacific is the fastest-growing region in the medical alert systems market, owing to a rapidly ageing population and expanding digital connectivity and health technology adoption. The number of people aged 60+ in Asia Pacific has more than doubled since 1990 and is projected to reach nearly 1.3 billion by 2050, representing about one in four residents, which significantly increases demand for remote safety and health monitoring systems. Simultaneously, the region had ~1.5 billion mobile internet users in 2024, with continued growth expected, supporting broader use of mobile health technologies and emergency alert applications. In addition to demographic trends, rising burdens of chronic diseases such as diabetes and cardiovascular conditions, and improvements in smartphone penetration and network infrastructure are accelerating demand for connected health and alert solutions.

Competitive Landscape

The medical alert systems market is competitive, featuring major players like ADT, Life Alert, Bay Alarm Medical, and GreatCall. Innovation in wearable integration, AI-enabled monitoring, fall detection, and mobile connectivity, along with partnerships with healthcare providers and expansion into home-based, assisted living, and community wellness programs, drives differentiation and intensifies market competition globally.

Key Industry Developments:

- In July 2024, Lifeline Canada introduced a new wearable device designed to support individuals prone to wandering, particularly those with cognitive impairments or dementia. The device enables real-time location tracking and emergency alerts, enhancing safety and providing caregivers with timely information.

- In May 2024, Medical Guardian acquired MobileHelp, strengthening its portfolio of senior health care and personal emergency response solutions. The acquisition enables the company to broaden its product offerings, enhance wearable and mobile alert services, and reach a larger customer base across home-based and assisted living markets.

Companies Covered in Medical Alert Systems Market

- Medical Guardian LLC.

- ADT

- GreatCall

- Lifeline

- Rescue Alert

- Life Alert Emergency Response, Inc.

- AlertONE Services Inc.

- LogicMark

- Bay Alarm Medical

- VRI

- Tunstall Group

- Nice North America

- Others

Frequently Asked Questions

The global medical alert systems market is projected to be valued at US$ 13.1 Bn in 2026.

Rising elderly population, chronic diseases, smartphone adoption, wearable integration, and preference for independent living drive growth.

The global medical alert systems market is poised to witness a CAGR of 11.1% between 2026 and 2033.

AI-enabled monitoring, IoT integration, corporate wellness programs, emerging markets, and holistic health solutions present key opportunities.

Medical Guardian LLC., ADT, GreatCall, Lifeline, Rescue Alert, Life Alert Emergency Response, Inc.