- Smart Packaging

- Latin America In-Mold Labels Market

Latin America In-Mold Labels Market Size, Share, and Growth Forecast, 2026 - 2033

Latin America In-Mold Labels Market by Material Type (Polypropylene (PP), Polypropylene (PP), Others), Manufacturing Process (Injection Molding, Thermoforming, Others), End-Use Industry, and Country Analysis for 2026 - 2033

Latin America In-Mold Labels Market Size and Trends Analysis

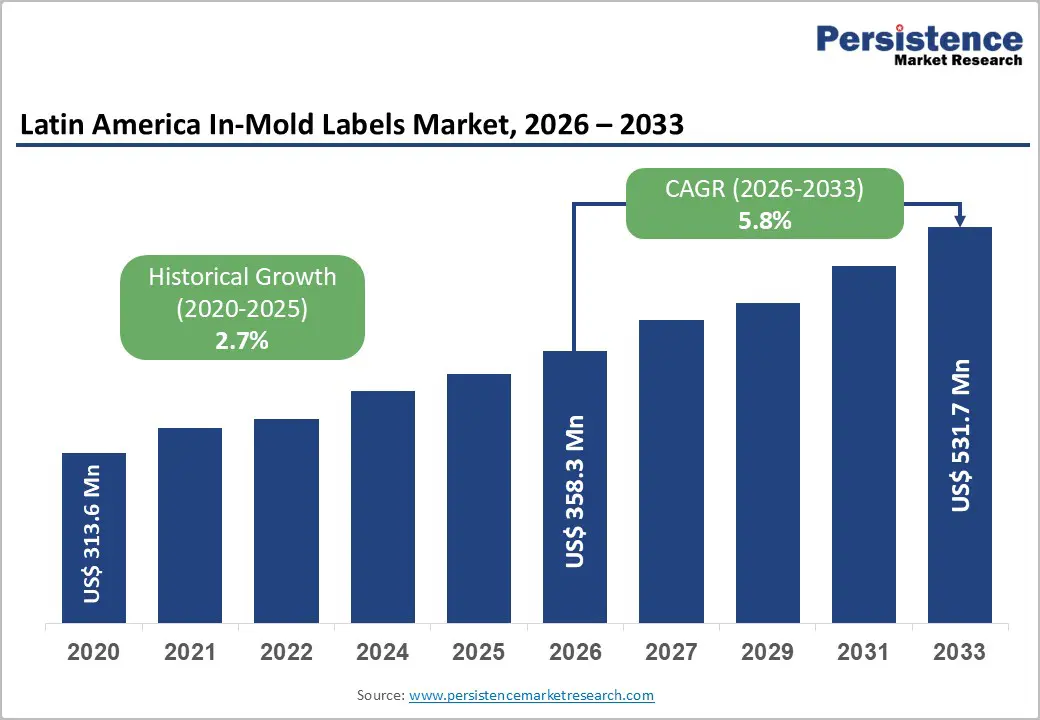

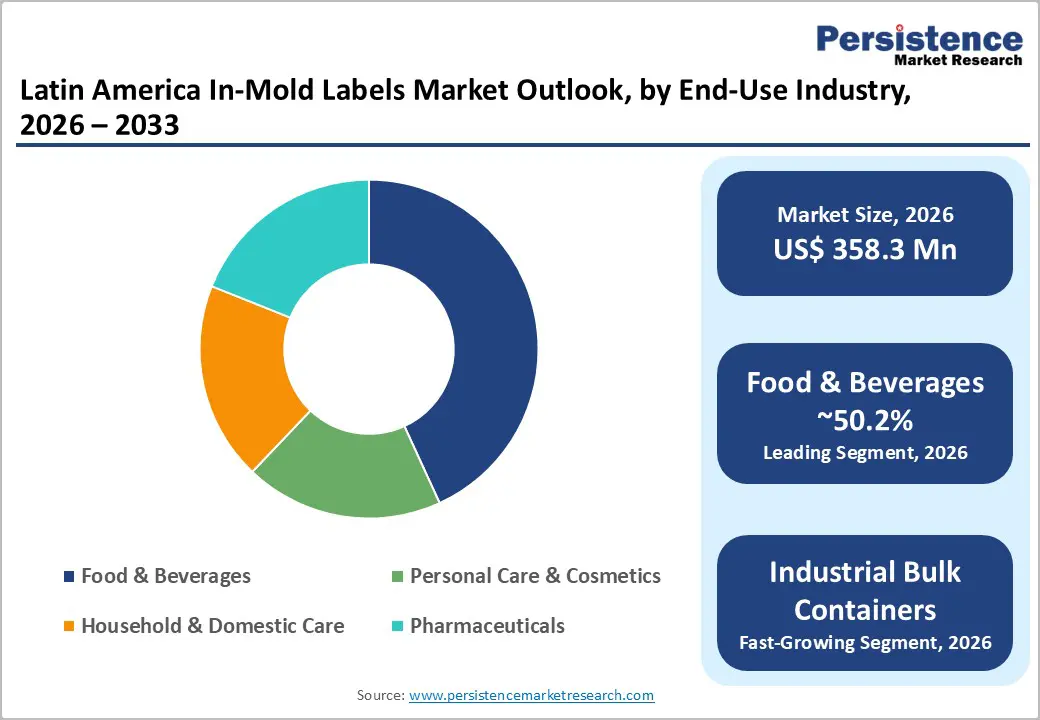

The Latin America in-mold labels market size is likely to be valued at US$358.3 million in 2026 and is expected to reach US$531.7 million by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033, driven by rising demand for durable and high-quality labeling solutions in the packaging industry, the Latin America in-mold labels market is witnessing steady growth across food, beverage, personal care, and household product segments.

In-mold labeling integrates the label directly into plastic containers during the molding process, enhancing product aesthetics, resistance to moisture, and shelf appeal. Growing urbanization, expanding retail infrastructure, and increasing consumption of packaged goods in countries such as Brazil, Mexico, and Argentina are strengthening market expansion. Technological advancements in printing and injection molding processes further accelerate adoption across rigid plastic packaging applications in the region.

Key Industry Highlights

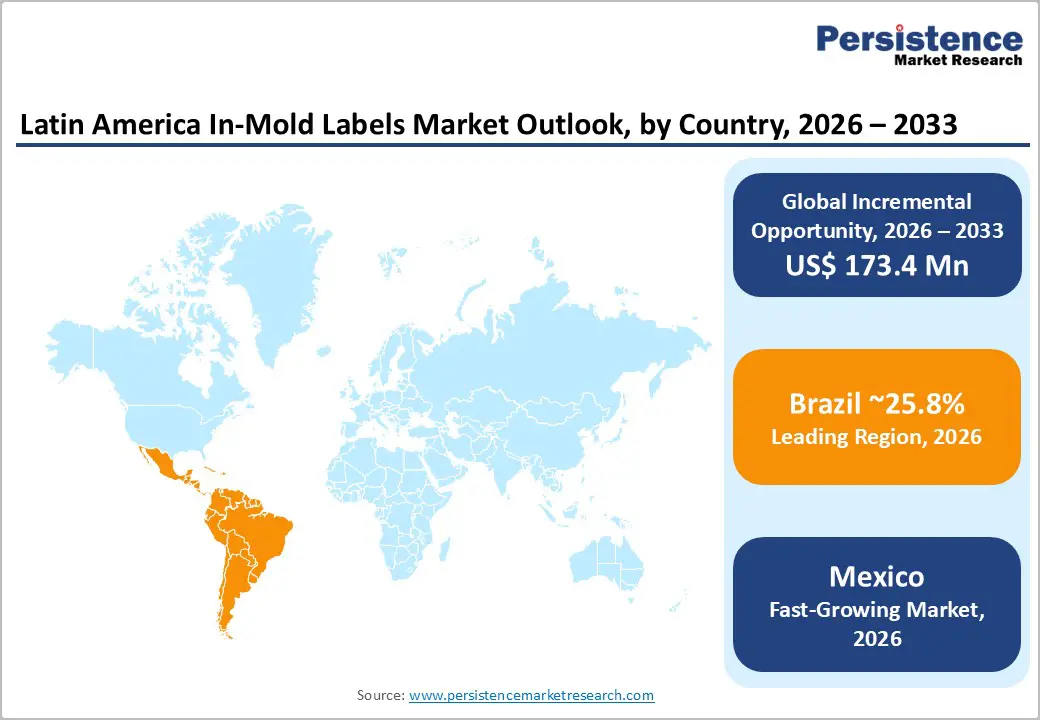

- Leading Region: Brazil is projected to lead the market, with an anticipated 25.8% market share, supported by its strong rigid plastic packaging base and high-volume dairy and FMCG production.

- Fastest-growing Region: Mexico is the fastest-growing country, driven by the expansion of automated injection molding facilities and the increasing adoption of premium decorative packaging.

- Investment Plans: Regional converters are investing in robot-assisted in-mold label placement systems and high-cavitation injection molding lines, particularly in Brazil and Mexico, to enhance production efficiency and support recyclable polypropylene (PP) packaging initiatives.

- Dominant Material Type: Polypropylene (PP) leads the market with an anticipated 50.2% share, owing to its compatibility with mono-material recyclable packaging and injection-molded container applications.

- Leading End-use Industry: The food & beverages segment is estimated to dominate with over 41.8% market share, driven by strong demand for durable, moisture-resistant labeling solutions in dairy, frozen desserts, and edible spreads packaging.

| Key Insights | Details |

|---|---|

| Latin America In-Mold Labels Market Size (2026E) | US$358.3 Mn |

| Market Value Forecast (2033F) | US$531.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rapid Expansion of Consumer Packaged Goods and Branded Rigid Packaging Demand

Rising demand for premium branded rigid plastic packaging in the fast-moving consumer goods (FMCG) sector is accelerating the adoption of in-mold labels across Latin America. Food processors, dairy producers, and personal care manufacturers increasingly prefer high-definition in-mold label printing for injection-molded containers to enhance shelf visibility and product differentiation in modern retail channels. The technology offers superior scuff resistance, moisture durability, and tamper evidence, which are critical for refrigerated dairy tubs, edible oil containers, and paint buckets. As organized retail and private-label expansion grow in Brazil and Mexico, brand owners are investing in decorative rigid packaging solutions with integrated labeling systems. For example, leading dairy brands in Brazil have adopted in-mold labeled polypropylene containers to strengthen brand recognition while maintaining structural integrity during cold-chain distribution.

Sustainability Mandates and Eco-efficient Packaging Adoption

Sustainability frameworks and circular economy initiatives across the region are also reinforcing the shift toward mono-material polypropylene (PP) packaging with recyclable in-mold labeling technology. Unlike pressure-sensitive labels, IML eliminates secondary adhesives, enabling improved recyclability and simplified material recovery processes. This aligns with extended producer responsibility (EPR) regulations and corporate ESG commitments adopted by multinational and regional packaging converters. Growing preference for adhesive-free labeling solutions in rigid plastic packaging supports waste reduction targets while maintaining premium visual appeal. In sectors such as household chemicals and edible spreads, manufacturers are transitioning to fully recyclable injection-molded containers with integrated IML films, reducing post-consumer contamination and strengthening compliance with evolving environmental policies in Latin American markets.

Barrier Analysis - Operational Complexity in High-Speed Injection Molding Environments

Seamless execution of robot-assisted in-mold label placement in high-cavitation injection molding systems remains a technical challenge for several Latin American converters. Precise synchronization between label feeding units, electrostatic charging systems, and mold closing cycles is critical to prevent wrinkling, air entrapment, or misalignment. In facilities operating mixed production lines, frequent mold changes and shorter production runs complicate automated in-mold labeling for multi-SKU rigid packaging, limiting efficiency gains. Variability in humidity and temperature conditions across tropical regions can also affect static-based label positioning accuracy, leading to inconsistent bonding performance in polypropylene containers used for dairy, margarine, and paint packaging.

Supply Chain Sensitivity to Polypropylene Film and Specialty Ink Availability

The regional IML ecosystem is highly dependent on steady access to BOPP in-mold label films with high-gloss and reverse-printing capabilities, many of which are sourced through international supply channels. Fluctuations in polypropylene resin allocation and shipping timelines can disrupt converter planning cycles, particularly for short-lead-time FMCG contracts. Limited domestic production of heat-resistant offset and UV-curable inks for in-mold labeling applications further constrains flexibility, as specialized inks are required to withstand molding temperatures without color distortion. These supply-side dependencies reduce agility for local packaging manufacturers seeking rapid design customization or seasonal product launches across Latin American retail markets.

Opportunity Analysis - Growth through Expansion of Specialty Food & Beverage Rigid Packaging Applications

An emerging opportunity for the Latin America in-mold labels market lies in the premium beverage and specialty food container segments, particularly for high-barrier IML solutions on PET and PP jars that improve shelf differentiation and moisture/UV protection. As craft beverage producers and healthy snack brands scale distribution into modern trade channels across Brazil and Chile, demand for clarity-enhanced in-mold labeling on recyclable rigid packaging is rising. For example, a growing number of artisanal kombucha and cold-brew brands are adopting IML on PET bottles to maintain vibrant full-body graphics while meeting recyclability expectations, unlocking higher retail price points and stronger brand recall.

Digital Print Integration in Local Converter Ecosystems

The adoption of digital in-mold label printing for short-run and customized rigid packaging is creating a niche growth vector across Latin American converter networks. By leveraging digital presses capable of variable data and quick changeovers, converters can serve regional food and personal care brands seeking on-demand IML designs with localized language, promotions, and seasonal motifs without the cost penalty of traditional plate-based processes. This trend aligns with rising e-commerce penetration and promotional packaging demand in markets such as Mexico and Argentina, enabling converters to offer fast-turnaround digital IML services that drive incremental revenue and reduce inventory obsolescence.

Category-wise Analysis

Material Type Insights

Polypropylene (PP) is anticipated to account for 50.2% of the market share in 2026, positioning it as the leading material segment. Its dominance is rooted in its superior compatibility with injection-molded polypropylene containers, which represent the bulk of rigid packaging used in dairy, margarine, ice cream, paint pails, and edible oil tubs. PP offers high impact strength, chemical resistance, and dimensional stability under varying temperature conditions, making it ideal for refrigerated and moisture-sensitive applications. The material also supports reverse-printed BOPP in-mold labeling technology, enabling high-gloss finishes and long-lasting graphic clarity. PP is also projected to be the fastest-growing material segment, driven by the shift toward mono-material recyclable rigid packaging systems. As converters increasingly adopt polypropylene containers paired with PP-based IML films, recycling efficiency improves because both components share the same polymer family. This structural advantage aligns with corporate sustainability targets and circular packaging initiatives across Brazil and Mexico. For example, leading dairy processors in Brazil are transitioning to fully polypropylene injection-molded tubs with integrated IML films to streamline recyclability while maintaining strong shelf differentiation.

End-use Industry Insights

The food & beverages segment is anticipated to hold over 41.8% of market share in 2026, making it the largest end-use industry. High consumption of packaged dairy products, frozen desserts, ready-to-eat meals, and edible spreads across urban centers in Brazil, Mexico, and Argentina sustains strong demand for durable labeling formats. In-mold labeling provides moisture-resistant, scratch-proof, and tamper-evident decoration for rigid food containers, ensuring compliance with labeling standards while enhancing visual appeal. The technology also enables 360-degree high-resolution graphics, which are critical in competitive supermarket environments. A relevant example includes margarine and yogurt brands using in-mold labeled polypropylene tubs to preserve brand identity under cold-chain distribution conditions.

The personal care & cosmetics segment is projected to be the fastest-growing end-use segment in the regional market. Growth is fueled by increasing demand for premium packaging aesthetics, particularly in skincare creams, hair masks, and body care jars. In-mold labeling enables metallic finishes, matte textures, and high-definition decorative effects on rigid cosmetic containers, supporting brand positioning in mid- to premium-tier product categories. Rising middle-class spending and expansion of regional beauty brands are accelerating the adoption of decorative injection-molded packaging with integrated IML technology. For instance, several Latin American skincare brands are adopting in-mold labeled PP jars to achieve a seamless, label-free appearance while improving resistance to oil-based formulations and repeated consumer handling.

Country Insights

Brazil

Brazil is anticipated to account for 25.8% of the market share in 2026, making it the leading country in the region. Its dominance is supported by a well-established rigid plastic packaging industry, strong domestic consumption of packaged food and beverages, and the presence of large-scale injection molding and label conversion facilities. The country’s expansive dairy, margarine, frozen dessert, and household chemical sectors drive consistent demand for high-volume polypropylene in-mold labeling applications. Brazil also benefits from a mature FMCG manufacturing ecosystem and organized retail penetration, which increases the need for visually differentiated, durable packaging formats. For example, leading Brazilian dairy producers widely use in-mold labeled PP tubs to enhance shelf visibility while ensuring structural durability under refrigerated distribution conditions.

Mexico

Mexico is projected to be the fastest-growing country in the regional market. Growth is supported by expanding food processing exports, rising domestic consumption of packaged goods, and increasing investment in automated injection molding and robotic in-mold labeling systems. Mexico’s proximity to North American supply chains also strengthens technology transfer and modernization within packaging operations. The rapid expansion of private-label food brands and personal care manufacturers is accelerating the adoption of premium decorative rigid packaging with integrated IML technology. A relevant example includes Mexican edible spread and ice cream manufacturers upgrading to high-definition in-mold labeled containers to compete effectively in both domestic supermarkets and export markets.

Competitive Landscape

The Latin America in-mold labels market is moderately consolidated, with a mix of global labeling specialists and regional converters competing across high-volume FMCG and industrial packaging applications. Multinational players leverage advanced reverse-printing BOPP film technology, robotic label insertion systems, and high-cavitation injection molding compatibility to secure long-term contracts with leading food, beverage, and household product manufacturers. Their competitive strength lies in technical expertise, integrated production capabilities, and the ability to deliver consistent graphic precision across large production runs.

Regional and mid-sized converters compete through flexible order quantities, localized supply chains, and faster turnaround times for customized packaging designs. Increasing investments in digital in-mold label printing and automated mold-label synchronization systems are intensifying competition, particularly in Brazil and Mexico. Strategic collaborations between packaging manufacturers and FMCG brands to develop mono-material recyclable containers are further shaping differentiation strategies, with innovation, sustainability alignment, and operational efficiency emerging as key competitive pillars.

Key Industry Developments

- In January 2025, CCL Industries completed the acquisition of McGavigan Holdings Ltd., a well-known supplier of in-mold components for automotive interiors, enhancing its product offerings and technical capabilities.

Companies Covered in Latin America In-Mold Labels Market

- CCL Industries Inc.

- Avery Dennison Corporation

- Multi-Color Corporation

- Constantia Flexibles Group GmbH

- Huhtamaki Oyj

- Coveris Holdings S.A.

- Fuji Seal International, Inc.

- Inland Packaging

- Smyth Companies, LLC

- Yupo Corporation

- Sato Holdings Corporation

- Innovia Films Ltd.

- Polinas Plastik Sanayi ve Ticaret A.Ş.

- Treofan Group

- Korsini-Saf S.A.

- Logoplaste

- Plastipak Holdings, Inc.

- Amcor plc

Frequently Asked Questions

The Latin America in-mold labels market is projected to reach approximately US$358.3 million in 2026.

By 2033, the Latin America in-mold labels market is expected to attain a value of US$531.7 million.

Key trends include growing adoption of recyclable polypropylene (PP) mono-material packaging systems, integration of robotic label placement in high-cavitation injection molding, rising demand for premium decorative finishes in personal care packaging, and expansion of digital in-mold label printing for short-run customized production.

By material type, polypropylene (PP) leads the market, expected to account for a 50.2% share, owing to its compatibility with injection-molded rigid containers and its recyclability advantages.

The Latin America in-mold labels market is projected to grow at a CAGR of 5.8% over the forecast period.

Major companies include CCL Industries Inc., Avery Dennison Corporation, Constantia Flexibles Group GmbH, Multi-Color Corporation (MCC), and Huhtamaki Oyj.