- Electrical Equipment & Services

- Industrial Plugs and Sockets Market

Industrial Plugs and Sockets Market Size, Share, and Growth Forecast, 2025 - 2032

Industrial Plugs and Sockets Market by Degree of Protection (IP44, IP55, IP67/IP68, IP69K), Industry Vertical (Manufacturing & Automotive, Oil & Gas, Construction & Infrastructure, Food & Beverage, Energy & Power Generation, Marine & Offshore, Transportation & Rail, Robotics & Automation), Amperage (16A, 32A, 63A, 125A+, Up to 800A), and Regional Analysis for 2025-2032

Industrial Plugs and Sockets Market Share and Trends Analysis

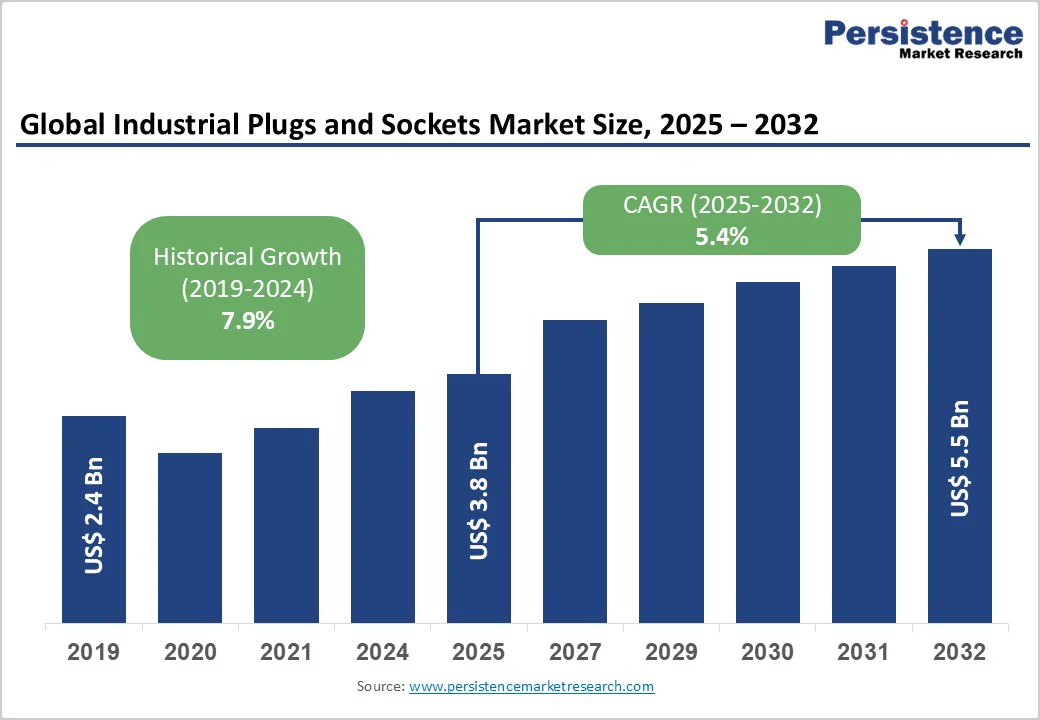

The global industrial plugs and sockets market size is likely to be valued at US$ 3.8 billion in 2025, and is estimated to reach US$ 5.5 billion by 2032, growing at a CAGR of 5.4% during the forecast period 2025−2032, propelled by the continuous modernization of industrial infrastructure and an intensifying emphasis on workplace safety compliance. Resilience-driven supply chain strategies and widening adoption of cutting-edge industrial equipment across renewables, automotive, and advanced manufacturing are shaping the demand for robust and durable connectivity solutions. Key sectors such as oil & gas, construction, transportation, and advanced manufacturing are leveraging plugs and sockets as integral systems for mission-critical power distribution and connectivity. While global trade tensions and cost inflation are marginally moderating growth rates relative to historic peaks, the evolution toward modular and smart connector solutions, accelerated safety regulation adoption, and the migration to renewable energy applications are ensuring the market’s resilience and competitive dynamism.

Key Industry Highlights

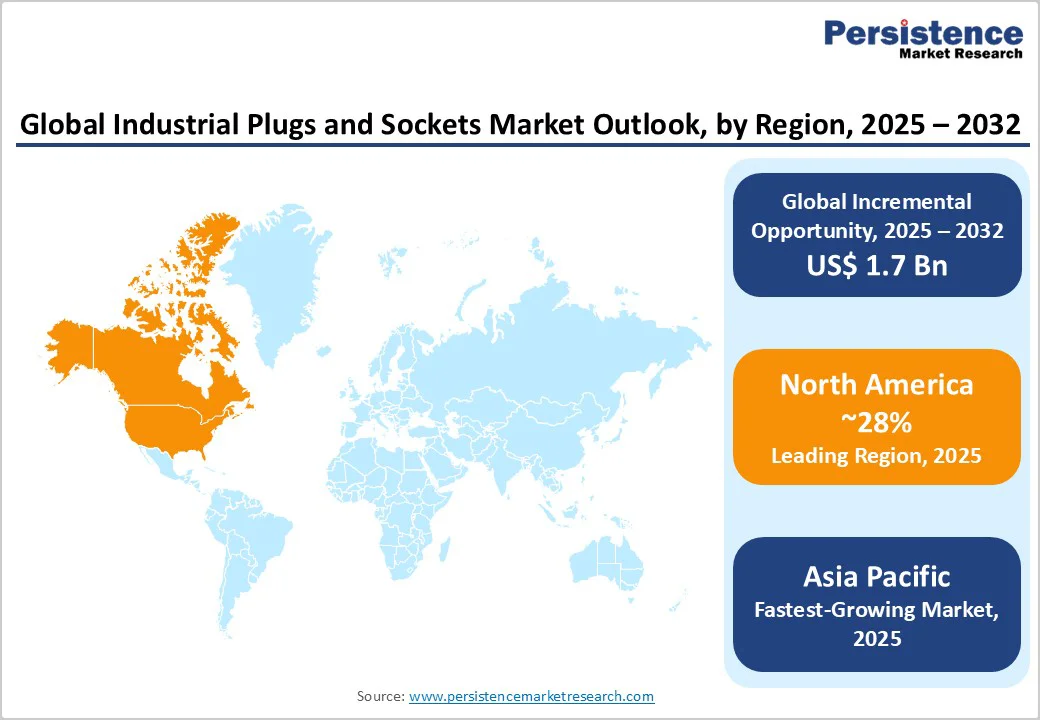

- Dominant Region: North America retains 28% global market share in 2025, led by the U.S. and characterized by rapid innovation cycles, automation investments, and supply chain resilience.

- Fastest-growing Regional Market: Asia Pacific is forecast as the fastest-growing regional market with a 7.4% CAGR from 2025 to 2032, supported by massive investments in smart manufacturing and renewables by China, India, Japan, and the ASEAN bloc.

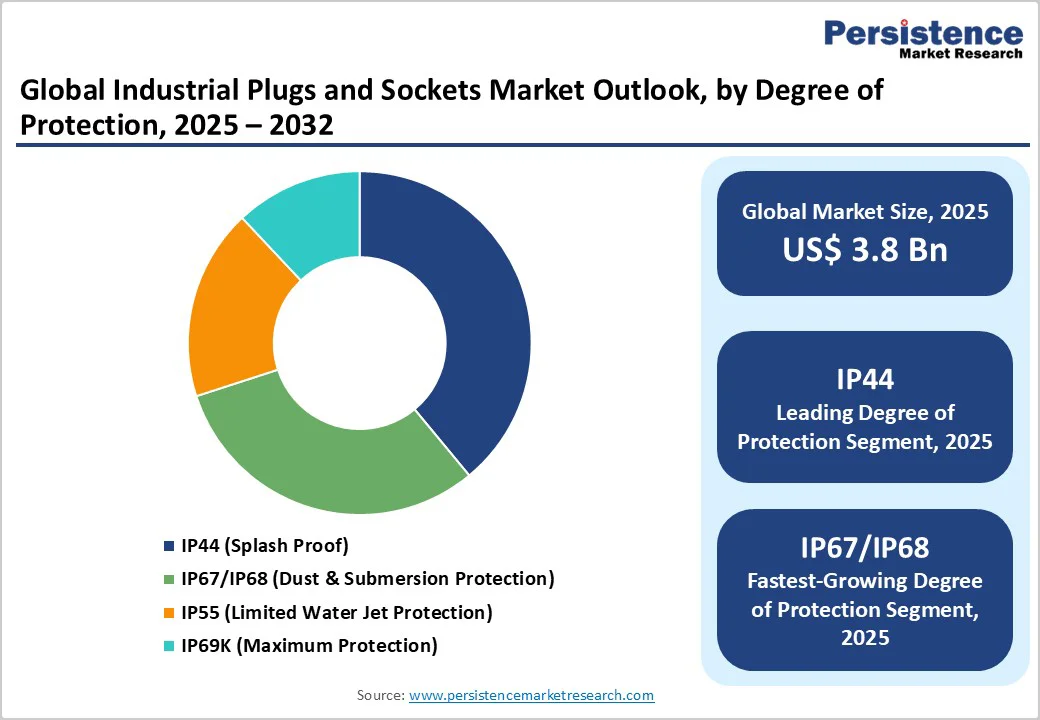

- Leading IP Ratings: IP44-rated plugs and sockets dominate, accounting for roughly 39% of the market revenue share in 2025, while the IP67/IP68 segment is projected to grow at 8.1% CAGR through 2032, driven by regulatory mandates and renewables.

- Dominant Industry Verticals: Manufacturing and automotive are set to capture 45% of the market in 2025, while robotics & automation is likely to emerge as fastest-growing vertical with a 2025-2032 forecast CAGR of 10.4%.

- Industry Developments: Strategic acquisitions, launch of AI-powered industrial equipment, advancements in modularity and diagnostics, and partnerships for accelerating IIoT deployment are the major industry trends.

- Competitive Environment: The industrial plugs and sockets market landscape remains moderately consolidated, with leading firms embracing multi-standard certification, service integration, and sustainability priorities for strategic growth.

| Key Insights | Details |

|---|---|

|

Industrial Plugs and Sockets Market Size (2025E) |

US$ 3.8 Bn |

|

Market Value Forecast (2032F) |

US$ 5.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Accelerating Industrial Electrification in Renewable Energy

With electrification in the renewable energy sector speeding up worldwide, the demand for industrial plugs and sockets, especially those with advanced IP67/IP68 ratings, which are indispensable for offshore wind farms, solar installations, and grid expansion projects, is set to grow steadily. According to the International Energy Agency (IEA), global annual renewable capacity additions are projected to rise from 666 GW in 2024 to around 935 GW by 2030, led by solar PV and wind. Policy frameworks such as the U.S. Inflation Reduction Act and the Fit for 55 initiative of the European Union (EU) are actively incentivizing clean energy adoption, catalyzing thousands of megawatts of new installations from China and India to the U.S. Gulf Coast.

The IEC and ATEX-compliant connectors have become the standard across these deployments, with industrial-grade sockets now capturing up to 60% of total renewable infrastructure connectivity spend. Manufacturers achieving these certifications, offering submersion-proof and corrosion-resistant products, and establishing direct supply chains with renewable operators are commanding higher price premiums, longer-term contracts, and superior market visibility.

Cost-Driven Procurement Pressures in Heavy-Duty Manufacturing

Rising procurement costs and tariff-induced pricing volatility are emerging as significant barriers to sustained growth within heavy-duty manufacturing, threatening both margins and project feasibility for industrial plug and socket suppliers and end-users. As a consequence, facility expansions and new manufacturing investments are encountering marked cost escalations for core connectivity components, evidenced by price increases on high-amperage plugs and IP67-rated sockets from leading German and French suppliers in 2024. Structural supply chain challenges such as port congestion, energy price surges, and inconsistent regulatory harmonization compound these headwinds, resulting in extended lead times and unpredictable capex allocations for original equipment manufacturers (OEMs).

Business decision-makers must therefore modify their strategies to integrate dynamic sourcing and procurement, diversify regional supplier networks, and forward contract negotiations to protect margins and delivery timelines. For investors, heightened sensitivity to tariff trends and regulatory shifts is essential, as cost barriers are likely to persist and shape market leadership and competitive landscape dynamics through 2032.

Modularization and Smart Connector Deployment in Industry 4.0 Environments

The convergence of modular connector architectures and Industrial Internet of Things (IIoT) integration within Industry 4.0 environments is emerging as a transformative opportunity, unlocking new revenue streams for OEMs while enabling operational agility for end-users. Advanced industrial plugs and sockets allow for equipment reconfiguration, predictive maintenance, and real-time energy management, delivering tangible productivity enhancements. Market research indicates that modular plugs and sockets featuring predictive diagnostics, remote monitoring via IoT sensors, and safety interlock functions are experiencing annual adoption growth rates of 10–13% by value, far outpacing traditional fixed-configuration products.

The shift has been accelerated by policy-led initiatives supporting automation in Europe through Horizon 2030, as well as broad manufacturing digitization targets under China’s Made in China 2025 policy and India’s National Digital Manufacturing program. For stakeholders, establishing technical integration partnerships and investing in smart product portfolios is strategically imperative as this niche drives structural differentiation and premium margin realization in mature and growing markets alike.

Category-wise Analysis

Degree of Protection Insights

At approximately 39%, the industrial plugs and sockets market revenue share in 2025 is dominated by IP44-rated products. IP44-rated connectors are widely adopted for their reliable splash protection in indoor manufacturing, general industrial, and workshop environments. Their ample availability, cost-effectiveness, and adherence to IEC 60309 standards have anchored their position as the workhorse of many industrial operations, particularly within sectors requiring moderate environmental protection without the high costs associated with advanced sealing.

The fastest-growing segment in this category from 2025 to 2032 is IP67/IP68, exhibiting an estimated CAGR of 8.1%. Rapid growth is driven by increasing regulatory mandates, such as the EU Machinery Directive and OSHA standards in North America, that oblige manufacturers to enhance workplace safety, especially in exposed or hazardous environments. The surge in renewable energy installation projects, particularly offshore wind farms and solar power plants, further accelerates the demand for these IP67/IP68 connectors due to their complete dust protection and submersion resistance up to 1 meter or more. Moreover, industries such as food and beverage processing and offshore oil and gas prioritize these high-protection connectors for their resistance to high-pressure washing and marine-grade corrosion.

Industry Vertical Insights

The manufacturing and automotive verticals are expected to command an estimated 45% revenue share of industrial plugs and sockets in 2025, reflecting sustained capital expenditure on advanced manufacturing systems, automated assembly lines, and electric vehicle (EV) production facilities. These sectors benefit from continuous replacement cycles and integration of Industry 4.0 technologies, evidenced by incremental upgrades in plug-and-play connectivity systems and modular socket integration. The broad adoption of IEC 60309-compliant standardized connectors ensures compatibility across legacy and emerging equipment, facilitating smooth operational continuity and cost-efficient maintenance schedules.

On the other hand, the robotics and automation segment is likely to be the fastest-growing, projecting a CAGR of about 10.4% between 2025 and 2032. This surge is fueled by ongoing digitalization initiatives, such as EU’s Digital Europe Program, that emphasize connectivity, automation accuracy, and predictive maintenance capabilities enabled by smart socket technologies. End-users are increasingly demanding connectivity solutions integrated with sensors and IoT diagnostics, enabling real-time monitoring and failure prevention. This vertical’s growth reflects the pronounced global shift toward flexible production, reduced downtime, and data-driven maintenance. Firms targeting this segment can focus on modular product lines, seamless device communication protocols, and scalable connectivity solutions.

Amperage Insights

Plugs and sockets with 32A current rating are anticipated to be the leading segment in 2025, accounting for approximately 44% of the market revenue share. This dominance is justified by the universal application of 32A connectors across industrial settings involving medium-power motors, welding equipment, and mid-size automation modules. Their widespread standardization under IEC 60309 and their balance of power delivery and manageable size make them a preferred choice for a variety of large-scale manufacturing and construction projects. The established supply chain efficiency and broad OEM adoption of 32A industrial plugs and sockets underpin their stable demand and competitive pricing structures.

The ultra-high current segment (125A and above) is slated to be the fastest-growing, expected to exhibit an estimated 8.7% CAGR through 2032. This acceleration is based on the expansion of utility-scale power grids, hyperscale data centers, and smart grid modernization projects that require rugged, high-capacity power connectors capable of withstanding elevated voltages and current loads. High-amperage plugs also benefit from integration with smart power management systems and predictive outage detection technologies, which is a necessity in environments where uptime is mission critical.

Regional Insights

North America Industrial Plugs and Sockets Market Trends

North America is predicted to sustain a leading position in the industrial plugs and sockets market share with 28%, dominated by the United States, in 2025. Infrastructural robustness, technologically advanced manufacturing base, and comprehensive regulatory framework, including UL certifications, NEC compliance, and OSHA mandates, underpin steady demand in the region. The growth trajectory of the regional market over the 2025-2032 period is indicative of robust activity in highly regulated sectors such as automotive manufacturing, aerospace, and clean energy generation.

Key growth drivers include ongoing infrastructure renewal programs, aggressive penetration of robotics and automation technologies, and a high-speed transition toward renewable energy sources that prioritize IEC-compliant, environmentally rated connectors. Regional competitive dynamics are governed by supply chain resilience, innovation incorporation, especially AI-driven diagnostics, and reshoring of manufacturing to limit tariff exposure. Investment trends focus on technology partnerships, acquisitions within high-growth digital manufacturing niches, and expansion into smart connector portfolios to address automation-centric opportunities.

Europe Industrial Plugs and Sockets Market Trends

Europe is estimated to accounts for about 23% of the global market share in 2025, led by the industrially advanced economies of Germany, the United Kingdom, and France. Regulatory harmonization under the CE and ATEX directives, coupled with the EU Green Deal and Digital Europe framework, has significantly influenced the uptake of next-generation industrial equipment. The demand for plugs and sockets in Europe is largely fueled by industrial digitization programs, extensive offshore wind capacity, and stringent environmental and safety standards compelling adoption of higher protection-rated plugs and sockets.

Pan-European initiatives have facilitated upgrades to production hubs and renewable infrastructure, generating a cascading effect on demand for advanced connectors with certified compliance. Leading regional players have been aggressively investing in developing smart, modular, and highly interoperable products to meet diverse customer specifications across sectors from automotive to food and beverage processing. Investment opportunities exist in expanding warehousing and after-sales service networks across Eastern and Southern Europe, as well as in cooperative ventures that foster AI-powered predictive maintenance capabilities.

Asia Pacific Industrial Plugs and Sockets Market Trends

Asia Pacific is forecasted to be the fastest-growing regional market with an approximate CAGR of 7.4% between 2025 and 2032. China, Japan, India, and the ASEAN bloc are the regional growth engines, powered by aggressive industrial modernization policies, expansive renewable energy rollouts, and scale manufacturing advantages. China's Made in China 2025 policy and India’s smart manufacturing initiatives continue to stimulate investment in precision connectivity solutions tailored for automated factories and renewable grids. A rapid increase in infrastructure projects, including smart grids and high-speed rail networks, has further escalated the demand for advanced industrial plugs and sockets.

Regulatory convergence toward IEC, UL, and ATEX standards has enhanced transnational product compliance. Strategic investments are presently focused on strengthening local production capacity, expanding high-protection and smart connector manufacturing, and forming synergistic partnerships to serve growing OEM demand effectively. Players operating in Asia Pacific also benefit greatly from a confluence of low production costs, skilled labor, and expanding digital supply chain network infrastructure, offering scalable market entry and expansion prospects.

Competitive Landscape

The global industrial plugs and sockets market structure is moderately consolidated with a dominance of top multinational companies commanding an estimated combined share of approximately 50%. Legrand SA, Schneider Electric SE, ABB Ltd, Eaton Corporation plc, and Siemens AG headline the market, supported by strong R&D investment, global sales networks, and multi-standard certified portfolios. The market exhibits fragmentation beyond the top tier, with a mix of regional and niche players leveraging specialized product lines or geographic focus to gain competitive advantages.

Competitive positioning is increasingly determined by advanced product capabilities such as IIoT integration, modular design innovations, and sustainability certifications. Greater emphasis on lifecycle services, predictive maintenance, smart diagnostics, and digital after-sales support is catalyzing competitive differentiation and industry consolidation trends.

Key Industry Developments

- In October 2025, PEI-Genesis, a global connector and cable expert, showcased its high-performance interconnect and cable management systems at India’s sixteenth International Railway Equipment Exhibition (IREE 2025) in New Delhi. The company focuses on solutions tailored for harsh environments in rail and mass transit, emphasizing rapid assembly and custom cable configurations. PEI-Genesis plans to enhance local production and support through a new factory in Pune starting December 2025, improving responsiveness for the expanding Indian rail network. This engagement allows PEI-Genesis’s to address the growing demands related to capacity expansion, electrification, and safety with rugged, certified connectors designed for the India's complex operational conditions.

- In September 2025, NG Nordic and ABB partnered to develop advanced electrical accessories, focusing on innovation and sustainability. The collaboration aims to enhance product performance and energy efficiency while meeting evolving market demands. This initiative underscores the growing trend of strategic partnerships in electrical components to accelerate technological progress and environmental responsibility.

- In August 2025, Amphenol Industrial Operations launched the GuardXcel cable glands designed for superior environmental sealing and mechanical strain relief. These cable glands address demanding industrial applications by providing enhanced durability, resistance to harsh chemicals, and improved safety. The product range also includes drain plugs, dome plugs, multi-hole seals, gaskets, washers, and ventilation plugs, available in plastic, stainless steel or nickel-plated brass, with sealing materials such as neoprene, silicone and nitrile butadiene rubber (NBR).

Companies Covered in Industrial Plugs and Sockets Market

- Legrand SA

- TE Connectivity

- Eaton Corporation PLC

- Emerson Electric Co.

- ABB Ltd

- Seimens AG

- Schneider Electric

- Havells India Ltd.

- Amphenol Corporation

- Marechal Electric

- Mennekes Elektrotechnik GmbH & Co. KG

- Palazzoli S.p.A.

- Bals Elektrotechnik GmbH & Co.KG

- Ferdinand Walther GmbH

- Andeli Group Co., Ltd.

- Lewden Metal Products Limited

- Scame Parre S.p.A.

Frequently Asked Questions

The global industrial plugs and sockets market is projected to reach US$ 3.8 billion in 2025.

Consistent modernization of industrial infrastructure and an intensifying emphasis on workplace safety compliance are driving the market.

The market is poised to witness a CAGR of 5.4% from 2025 to 2032.

Widening adoption of cutting-edge industrial equipment across renewables, automotive, and advanced manufacturing, and deployment of plugs and sockets by key industries such as oil & gas, construction, transportation, and advanced manufacturing as integral systems for mission-critical power distribution and connectivity are lucrative market opportunities.

Legrand SA, Schneider Electric SE, and ABB Ltd are some of the key players in the market.