- Industrial Machinery

- Industrial Lifting Equipment Market

Industrial Lifting Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Industrial Lifting Equipment Market by Equipment Type (Lifts, Fork lifts, Hoists, Stackers, Pallet trucks, Robotic arms, Others), Mechanism (Manufacturing industry, Process industry, Shipping dockyards, warehouses), Application, and Regional Analysis for 2025 - 2032

Industrial Lifting Equipment Market Size and Trends Analysis

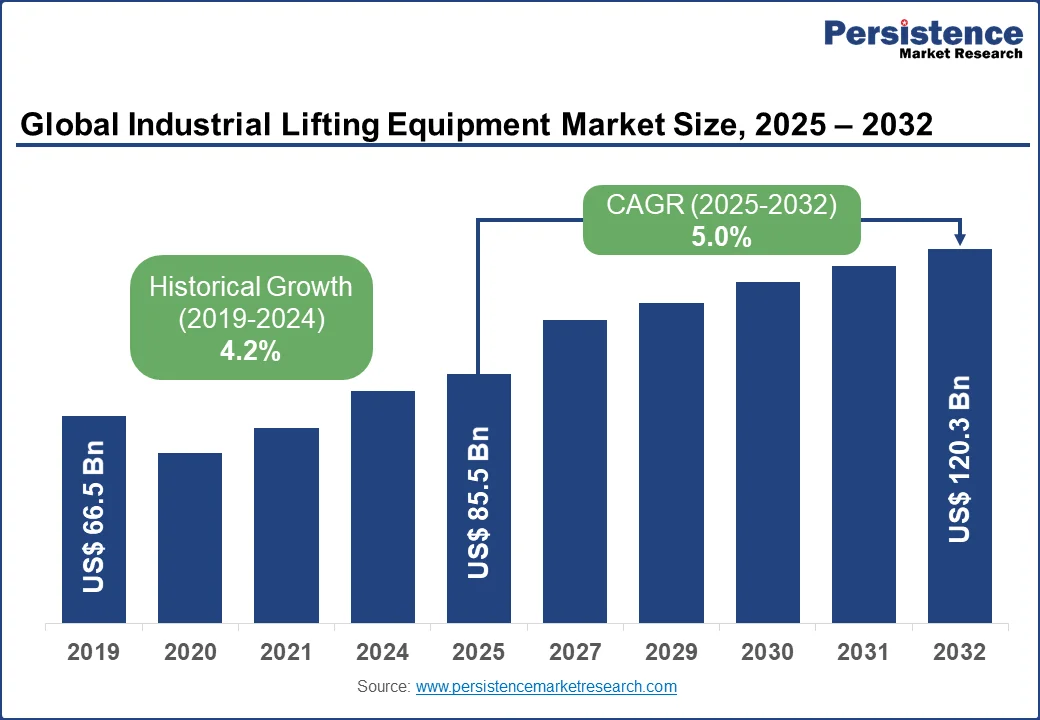

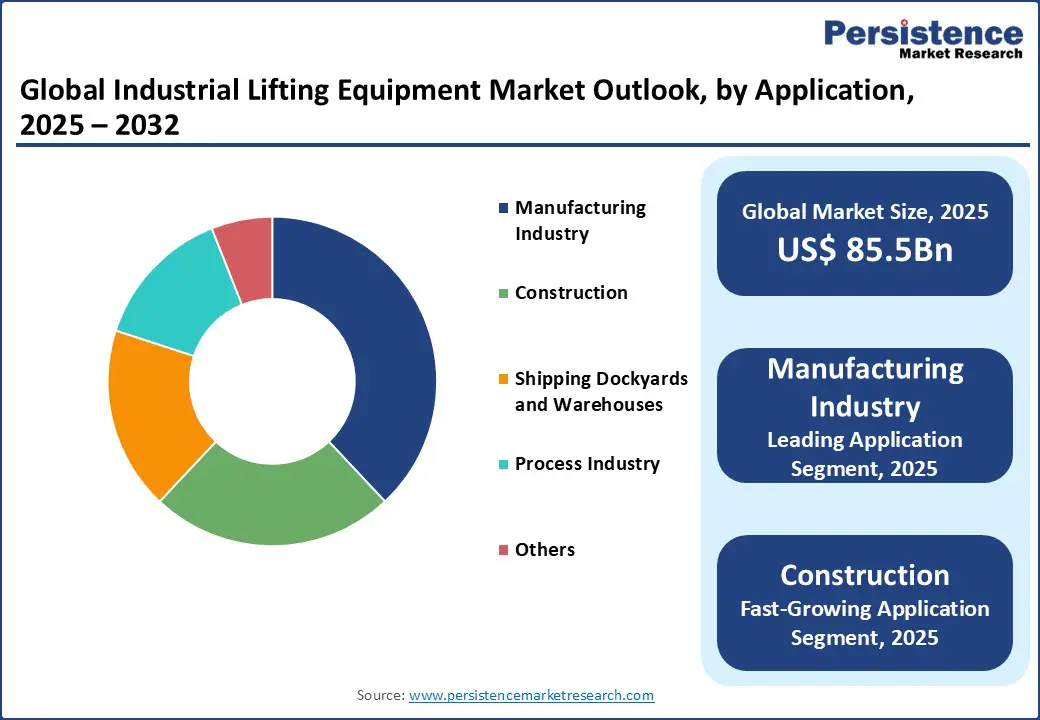

The global industrial lifting equipment market size is likely to be valued at US$ 85.5 Bn in 2025 and is expected to reach US$ 120.3 Bn by 2032, registering a CAGR of 5.0% during the forecast period from 2025 to 2032.

The industry has experienced robust growth, driven by the rising demand for efficient material handling solutions, advancements in automation technologies, and the increasing need for safe and productive industrial operations.

Key Industry Highlights:

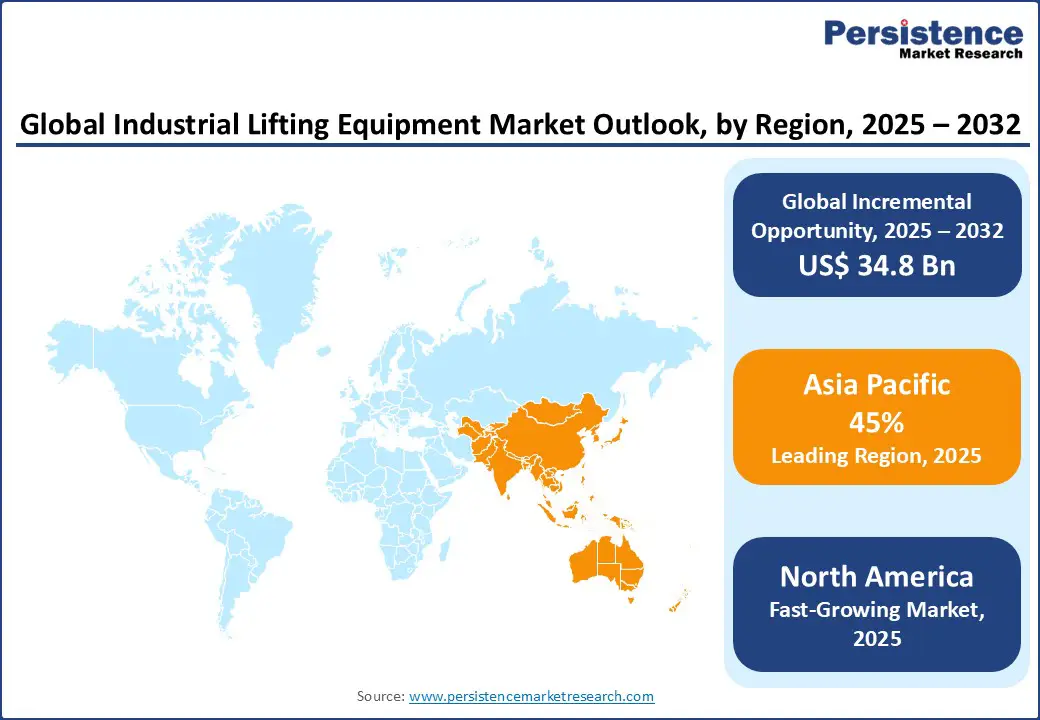

- Leading Region: Asia Pacific holds a 45% market share in 2025, driven by expansive industrial infrastructure, high manufacturing volumes, and widespread adoption of automated lifting technologies.

- Fastest-growing Region: North America, propelled by increasing industrial investments, a high focus on workplace safety, and expanding manufacturing facilities in the U.S. and Canada.

- Dominant Equipment Type: Fork lifts accounts for approximately 35.5% of the industrial lifting equipment market share in 2025, driven by their cost-effective production.

- Leading Application: Manufacturing industry is expected to lead with a 38% share, reflecting its widespread use in production lines and assembly settings.

| Key Insights | Details |

|---|---|

| Industrial Lifting Equipment Market Size (2025E) | US$ 85.5 Bn |

| Market Value Forecast (2032F) | US$ 120.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.2% |

Market Dynamics

Driver - Global Surge in Industrial and Manufacturing Demand

The global surge in industrial and manufacturing demand is a primary driver of the industrial lifting equipment market. According to the United Nations Industrial Development Organization (UNIDO), global manufacturing output is expected to grow steadily through the next decade, with developing regions such as the Asia Pacific leading at higher rates, necessitating advanced lifting solutions to handle increased production volumes.

This rising demand, particularly in sectors with intensive material handling and warehouse operations, underscores the need for efficient lifting equipment, which enhances productivity and safety in moving heavy loads. For instance, the expansion of e-commerce has driven warehouse construction, with the global warehousing market projected to reach significant levels, which is boosting the adoption of forklifts and stackers to optimize logistics.

In developing economies such as India and China, government programs such as India’s Make in India and China’s Made in China initiatives are accelerating manufacturing investments, leading to higher demand for hoists and robotic arms to automate processes and reduce labor costs.

The proliferation of construction projects is projected to exceed several trillion dollars globally. Workplace safety is a key concern, with the U.S. Bureau of Labor Statistics reporting that material handling injuries account for a significant share of workplace incidents, driving adoption of safer equipment such as robotic arms.

Environmental considerations also play a role, as operators adopt energy-efficient equipment to reduce operational costs, with electric and hybrid mechanisms gaining traction; electric forklifts can cut energy costs considerably compared to diesel models. The COVID-19 pandemic highlighted the importance of resilient supply chains for essential goods, prompting investments in lifting equipment for logistics.

In North America, the U.S. National Association of Manufacturers reports consistent annual increases in industrial output, while in Europe, the EU’s Green Deal promotes sustainable industrial solutions. These factors collectively propel the market’s growth, with projections indicating sustained demand through the coming years as Industry 4.0 integrates more automated lifting systems.

Restraint - High Costs and Skilled Personnel Requirements Restrict Adoption

The industry faces significant restraints due to high capital expenditures and the need for skilled personnel. Manufacturing and installing advanced lifting equipment, such as robotic arms or automated hoists, can require substantial investment per unit, depending on complexity and application, with additional expenses for maintenance and training. In emerging markets, the lack of skilled operators for advanced systems such as robotic arms limits adoption, particularly for small and medium-sized enterprises (SMEs).

Regulatory compliance, such as adhering to OSHA safety standards or the EU’s Machinery Directive, increases costs through mandatory certifications and inspections, which can add significantly to project budgets. For example, retrofitting facilities to accommodate automated lifting systems can involve considerable expenses per site, deterring smaller players.

Economic uncertainties, such as fluctuating steel prices noted by the World Steel Association, impact equipment costs. Environmental regulations also pose challenges, as older diesel-powered equipment faces restrictions in regions such as Europe, requiring costly upgrades to electric or hybrid systems.

The shortage of skilled technicians, particularly in developing regions, further complicates maintenance and operation, with training programs adding to overall expenses. These restraints disproportionately affect new entrants and SMEs, slowing market expansion despite strong demand.

Opportunity - Innovation in Sustainable Systems and Multi-Application Use Boosts Consumption

The industry presents significant opportunities through innovations in sustainable and versatile lifting solutions. The global push for sustainability, driven by initiatives such as the Paris Agreement, encourages the development of energy-efficient equipment, such as electric forklifts and hybrid hoists, which help lower energy consumption compared to traditional models.

Advancements in battery technology further enable electric lifts to operate longer, aligning with long-term carbon-neutral goals. Multi-application equipment, capable of handling diverse tasks in manufacturing and warehousing, is gaining traction by enabling shared usage and reducing overall equipment costs.

The rise of Industry 4.0 technologies, such as IoT-enabled lifting systems, creates demand for smart equipment that optimizes operations through real-time data, enhancing efficiency across industrial and logistics processes. In emerging markets, government incentives promote the adoption of robotic arms and automated stackers, further supporting industrial automation.

The integration of AI and robotics in lifting equipment improves precision and safety, helping minimize workplace injuries while boosting productivity. Strategic partnerships between manufacturers and logistics firms, such as those initiated by Toyota Industries, also enhance market reach. These opportunities are set to drive market growth by addressing environmental, cost, and efficiency concerns, fostering long-term expansion.

Segmental Insights

Equipment Type Insights

The global industrial lifting equipment market is segmented into lifts, forklifts, hoists, stackers, pallet trucks, robotic arms, and others. Forklifts dominate, holding approximately 35.5% of the market share in 2025, driven by cost-effective production, scalability, and widespread adoption in manufacturing and warehouse operations worldwide.

Robotic arms represent the fastest-growing segment of the industrial lifting equipment market, fueled by rising demand for automated solutions in manufacturing and warehouse operations. Their ability to enhance precision, efficiency, and safety in material handling is accelerating adoption across diverse industrial applications.

Mechanism Insights

The global industrial lifting equipment market is divided into the manufacturing industry, process industry, shipping dockyards, and warehouses. The manufacturing industry leads with a 55% share in 2025, driven by its critical role in production lines, assembly operations, and overall material handling efficiency.

Warehouses represent the fastest-growing segment of the industrial lifting equipment market, propelled by the e-commerce boom and increasing adoption of logistics automation. The need for efficient material handling, faster order fulfilment, and streamlined inventory management is driving rapid growth in this sector.

Application Insights

The industrial lifting equipment market is segmented into construction, shipping dockyards and warehouses, manufacturing industry, and process industry. The manufacturing industry dominates with a 38% share in 2025, driven by its pivotal role in industrial automation, production efficiency, and streamlined material handling.

Construction is the fastest-growing segment of the industrial lifting equipment market, fueled by expanding global infrastructure projects and rapid urbanization. Rising demand for efficient material handling on construction sites and the adoption of advanced lifting solutions are driving growth in this sector.

Regional Insights

Asia Pacific Industrial Lifting Equipment Market Trends

Asia Pacific dominates the global industrial lifting equipment market, expected to account for 45% share in 2025, driven by rapid industrialization, expanding manufacturing output, and growing investments in automation across the region. Countries such as China and India are at the forefront of this growth.

In China, the Made in China 2025 initiative actively promotes smart manufacturing practices, fostering the adoption of advanced lifting equipment across factories, warehouses, and logistics centers. This initiative is expected to result in the deployment of over one million new lifting equipment units by 2025, significantly enhancing material handling capabilities.

India’s Make in India program further accelerates industrial growth, supporting manufacturing expansion and increasing demand for forklifts, hoists, and other lifting solutions to meet production and logistics needs.

Additionally, Japan and South Korea are recognized for their leadership in advanced automation, driven by widespread robotics integration and smart factory initiatives, which further stimulate the adoption of innovative lifting technologies. Overall, the region’s industrial and technological advancements underpin sustained market growth.

North America Industrial Lifting Equipment Market Trends

North America is emerging as the fastest-growing region in the industrial lifting equipment market, primarily driven by stringent safety regulations and a robust expansion of manufacturing activities. In the United States, substantial investments under the Infrastructure Investment and Jobs Act are fueling demand for lifts, pallet trucks, hoists, and other material handling equipment, supporting large-scale infrastructure and construction projects.

Automotive manufacturing hubs, particularly in states such as Michigan and Ohio, are increasingly integrating robotic arms and automated lifting systems to enhance production efficiency, reduce workplace injuries, and streamline material handling processes.

The emphasis on automation is further reinforced by the need for operational flexibility and cost-effective solutions in competitive industrial environments. Canada exhibits similar growth patterns, with rising adoption of lifting equipment in logistics, warehousing, and mining sectors.

Here, advanced forklifts, stackers, and hoists improve productivity, ensure safety, and support automation initiatives. Collectively, regulatory compliance, infrastructure investments, and technological adoption are driving sustained market growth across North America.

Europe Industrial Lifting Equipment Market Trends

Europe maintains a steady share in the industrial lifting equipment market, with leading countries such as Germany, the UK, and France contributing significantly to growth through EU industrial targets and modernization initiatives.

In Germany, the automotive and machinery sectors are key drivers, increasingly adopting automated hoists and robotic arms to enhance production efficiency and workplace safety. The UK’s Industrial Strategy emphasizes smart manufacturing and advanced automation, stimulating demand for forklifts, stackers, and multi-functional lifting solutions across manufacturing and logistics operations.

France focuses on green and sustainable manufacturing practices, encouraging the use of electric and energy-efficient lifting equipment, supported by regulatory incentives and environmental policies. Across the region, these initiatives collectively promote technological adoption, optimize material handling processes, and ensure compliance with safety and sustainability standards, reinforcing Europe’s stable yet progressive role in the global market.

Competitive Landscape

The global industrial lifting equipment market is highly competitive, with global and regional players vying for share through innovation, competitive pricing, and reliability. The rise of sustainable and automated products intensifies competition, as companies meet stringent regulatory and industrial demands. Strategic partnerships, mergers, and regulatory approvals are key differentiators.

Key Developments

- June 2025: JCB, a UK-based industrial equipment manufacturer, announced plans to expand its under-construction factory in San Antonio, Texas, in response to new U.S. import tariffs. The plant, initially planned at 720,000 square feet, will now span 1 million square feet, aiming to bolster domestic production and offset the short-term impacts of the 10% tariff. This $500 million facility is expected to become JCB’s second-largest globally, following its headquarters in England. The expansion is anticipated to significantly boost the region’s manufacturing sector, providing approximately 1,600 jobs.

- May 2024: Chevron Oronite Company LLC announced plans to build a new manufacturing plant in Ningbo, China, expanding its production footprint. The facility aims to boost capacity and strengthen the supply of key products, including cetane improvers, ensuring reliable distribution across China, Asia, and global markets. The execution phase of this expansion is scheduled to begin in July 2024, with an anticipated completion date in late 2026.

Companies Covered in Industrial Lifting Equipment Market

- Anhui Heli Co., Ltd.

- HAULOTTE GROUP

- Ingersoll-Rand

- SSAB

- Zoomlion Heavy Industry Science&Technology Co., Ltd.

- Hyster-Yale Materials Handling, Inc.

- PALFINGER AG

- Cargotec Corporation

- Columbus McKinnon Corporation

- TOYOTA INDUSTRIES CORPORATION

- KITO CORPORATION

- XCMG Group

- Linamar

- Terex Corporation

- Jungheinrich AG

- Liebherr Group

Frequently Asked Questions

The industrial lifting equipment market is projected to reach US$85.5 Bn in 2025.

Rising industrial demands, technological advancements in automation, and government initiatives for workplace safety are key drivers.

The market is poised to witness a CAGR of 5.0% from 2025 to 2032.

Innovations in sustainable systems and multi-application solutions present significant growth opportunities.

Anhui Heli Co., Ltd., HAULOTTE GROUP, and Toyota Industries Corporation are among the leading players.