- Non-food Packaging

- India Pallets Market

India Pallets Market Size, Share, and Growth Forecast 2026 - 2033

India Pallet Market by Material Type (Wood Pallets, Plastic Pallets, Metal Pallets, Composite Pallets, Corrugated Pallets), Structural Design (Stringer, Block), Industry (Food & Beverage, Pharmaceutical, Chemical, Retail, Agriculture, Electronics, Construction, Other), and Regional Analysis for 2026 - 2033

India Pallets Market Size and Trend Analysis

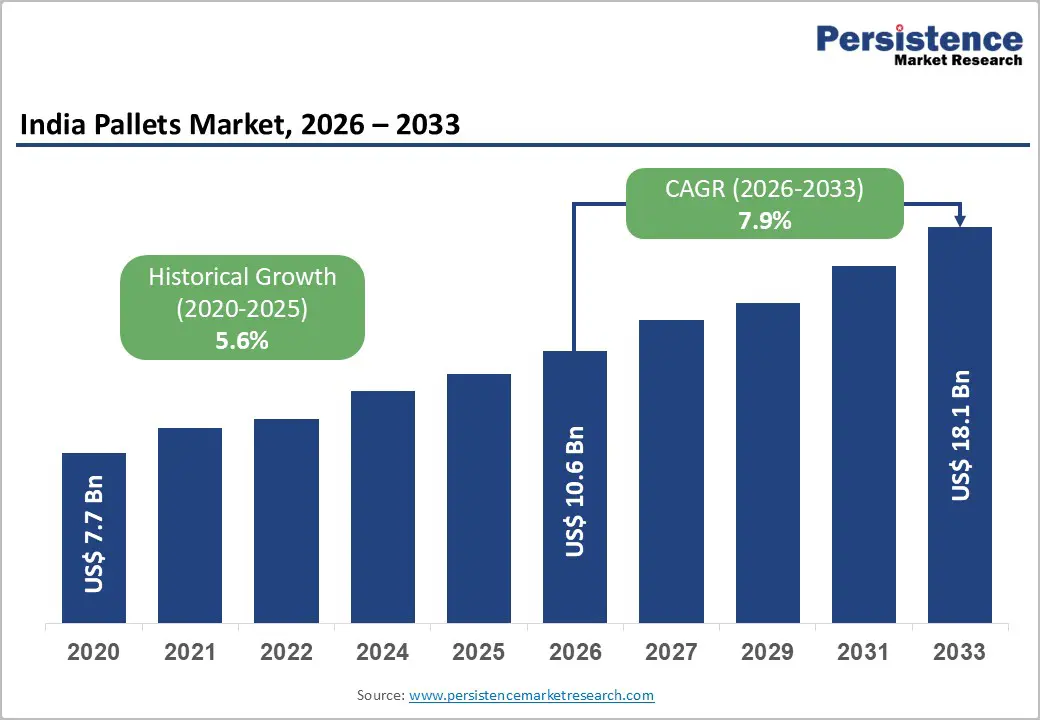

India pallets market size is supposed to be valued at US$ 10.6 billion in 2026 and is projected to reach US$ 18.1 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

Rapid expansion of manufacturing and logistics sectors under initiatives such as Make in India drives growth, supported by rising e-commerce volumes requiring efficient material handling. The government's Production Linked Incentive (PLI) scheme has catalyzed manufacturing growth across 14 strategic sectors with an investment commitment of INR1.76 lakh crore, generating production worth INR16.5 lakh crore by March 2025, thereby amplifying demand for efficient material handling and warehousing solutions.

Key Industry Highlights:

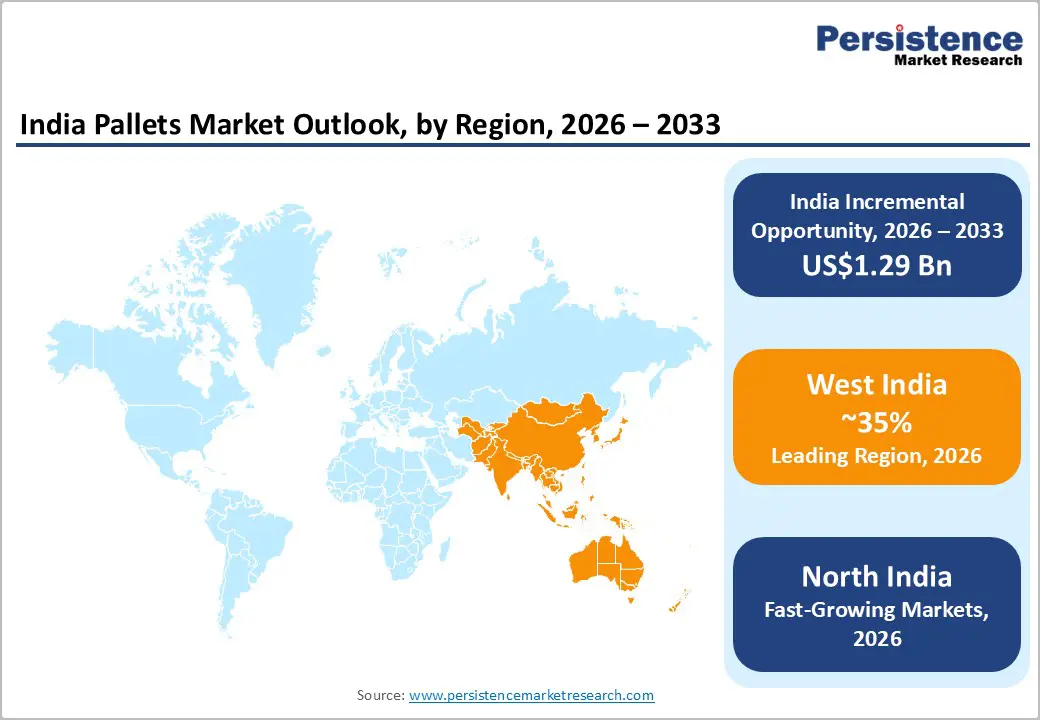

- Regional Leader: West India leads the market, with 35% share, due to industrial hubs in Maharashtra-Gujarat, port proximity, and manufacturing dominance.

- Fastest Growing Region: North India represents the fastest-growing regional market, propelled by Delhi NCR logistics expansion, Uttar Pradesh's dominance in cold storage infrastructure, and manufacturing growth under PLI incentives across pharmaceuticals and food processing sectors.

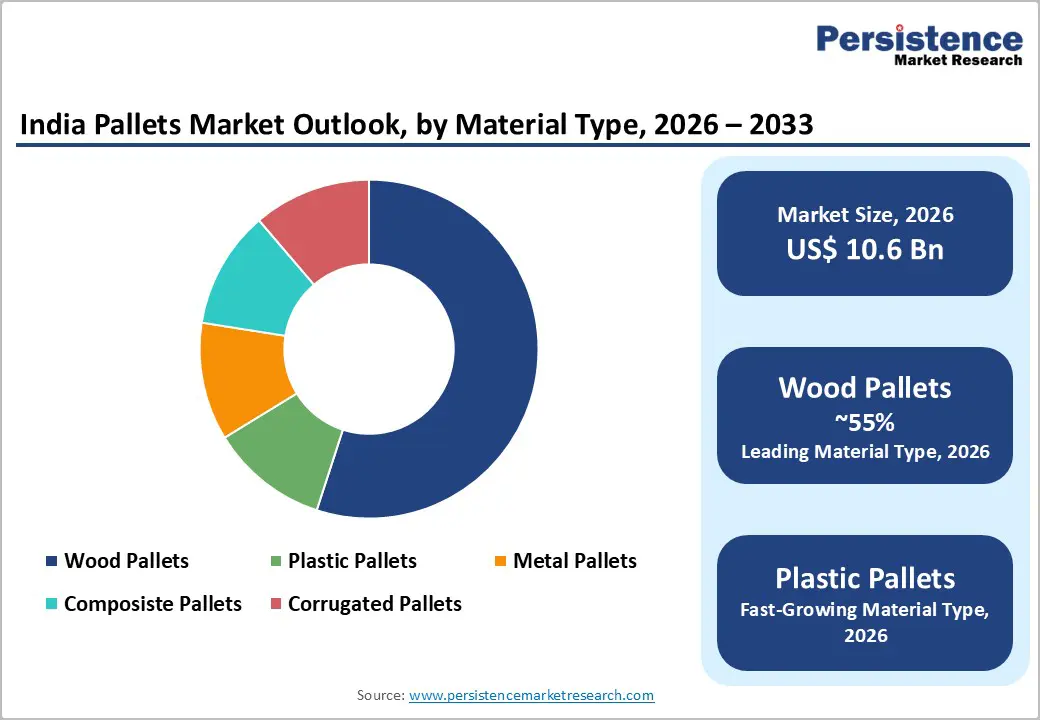

- Leading Segment: Wood Pallets dominate material type with 55% share, attributed to cost-effectiveness, widespread timber availability, superior strength characteristics, and established recycling networks.

- Fastest Growing Segment: Plastic Pallets fastest in materials, driven by pharmaceutical and food & beverage sectors requiring hygienic, moisture-resistant, and HACCP-compliant solutions.

- Key Growth Opportunities: Sustainable packaging integration presents a significant market opportunity with FSSAI regulations permitting recycled plastics from March 2025, and government mandates requiring 30% recycled content, creating demand for eco-friendly pallet solutions aligned with circular economy principles.

| Key Insights | Details |

|---|---|

| India Pallets Market Size (2026E) | US$ 10.6 Bn |

| Market Value Forecast (2033F) | US$ 18.1 Bn |

| Projected Growth CAGR (2026 - 2033) | 7.9% |

| Historical Market Growth (2020 - 2025) | 5.6% |

Market Dynamics

Driver - Exponential E-commerce Expansion and Quick-Commerce Proliferation

The booming e-commerce sector significantly propels the India Pallets Market, as platforms demand reliable palletization for high-volume order fulfillment and warehousing. According to IBEF, India's e-commerce sector has experienced transformative growth, with online retail surpassing INR 12.2 trillion in 2024 and expanding at 18.7% annually. The proliferation of quick-commerce platforms has necessitated robust warehousing infrastructure with standardized pallet systems to facilitate rapid inventory turnover. The National Single Window System has digitized customs processes, reducing clearance times and boosting cross-border shipments that are growing at 6.8% CAGR through 2030.

Government-backed infrastructure like dedicated freight corridors supports seamless palletized transport, ensuring pallets remain integral to scaling operations amid US$5.8 trillion global e-commerce in 2023. This driver fosters sustained demand, particularly in retail and consumer goods distribution.

Government Manufacturing Initiatives and Cold Chain Infrastructure Development

India's manufacturing sector remains resilient, consistently expanding. The Production-Linked Incentive (PLI) scheme, which covers 14 key sectors, has attracted significant investment in manufacturing, leading to increased demand for material handling equipment like pallets. The Make in India initiative, combined with the PLI scheme, has approved 760 applications across industries like pharmaceuticals, automotive, and electronics, attracting over US$ 18.72 billion in investments and creating more than 1.15 million jobs in 2024.

India's cold chain infrastructure is expanding rapidly, with companies like Snowman Logistics operating 154,330 pallets in 21 cities and planning to add 5,900 more in Pune by June 2026. The pharmaceutical and food & beverage sectors require temperature-controlled storage, and with less than 10% of India’s milk output currently packaged, there is significant potential for aseptic packaging and pallet-based distribution systems.

Restraints - Raw Material Price Volatility and Supply Chain Disruptions

Wooden pallet manufacturers face persistent challenges from timber price fluctuations and sustainability concerns regarding deforestation. Environmental regulations increasingly restrict hardwood sourcing, compelling manufacturers to explore alternative materials. India's dependence on imported pinewood exposes the market to global supply chain disruptions, currency fluctuations, and trade regulation changes affecting procurement costs. For plastic pallets, cost inflation in petroleum-based polymers impacts production economics. The aluminum foil price escalation has raised caution among flexible packaging converters, indirectly affecting composite pallet adoption.

The global supply chain disruptions continue to constrain import-dependent raw materials, particularly for specialized composite and metal pallets that require specific alloys or reinforced polymers. These material cost pressures compress profit margins for pallet manufacturers and create pricing uncertainties for end-users across the sustainable packaging market.

Fragmented Market Structure and Standardization Challenges

The pallet market in India is highly fragmented, consisting of numerous unorganized players that offer non-standardized products with varying dimensions, load capacities, and quality specifications. This lack of standardization hinders interoperability across supply chains and complicates the adoption of automated material handling systems that require uniform pallet specifications.

Several small-scale manufacturers do not possess quality certifications or comply with international standards, such as ISPM 15 for wooden pallets used in export applications. The absence of industry-wide standardization protocols creates compatibility issues for multinational corporations that are trying to implement global supply chain systems. The limited awareness among small and medium-sized enterprises (SMEs) regarding the lifecycle cost benefits of high-quality pallets compared to their initial purchase price perpetuates a preference for low-cost, suboptimal solutions.

Opportunity - Sustainable and Circular Economy Packaging Solutions

The Food Safety and Standards Authority of India (FSSAI) updated its packaging regulations on March 28, 2025, allowing the use of recycled plastics that meet safety standards for food packaging. The Plastic Waste Management Rules 2016 and subsequent Extended Producer Responsibility (EPR) regulations have created incentive structures for upcycled plastic pallet manufacturers, with registered producers reporting more than three million tonnes of EPR obligations in 2022-23. Government mandates drive this growth for 30% recycled content in PET bottles and high collection rates.

The 2016 Plastic Waste Management Rules and Swachh Bharat Abhiyan initiatives support recyclable pallet solutions. Manufacturers of pallets made from recycled plastics or bio-composites can leverage this trend towards sustainability. The Bureau of Indian Standards (BIS) guidelines promoting recycled materials enhance opportunities for companies offering circular economy solutions, such as pallet pooling and reverse logistics programs.

Warehouse Automation and Smart Logistics Integration

India's warehousing sector is experiencing a digital transformation through the adoption of Automated Storage and Retrieval Systems (AS/RS), robotic palletizing, and IoT-enabled inventory management. Government initiatives, such as the National Logistics Policy and PM Awas Yojana Urban 2.0, which invests INR 10 lakh crore (about US$ 120.16 billion), are expanding cold storage facilities and logistics parks in metropolitan and Tier 2 cities.

The increased production of vaccines and biologics has raised the demand for pallets compliant with WHO-GMP, FDA, and HACCP standards. Companies like Nilkamal have created injection-molded plastic pallets for automated systems. Furthermore, the Western Dedicated Freight Corridor is reducing transit times and enhancing capacity, which requires compatible pallet systems for multimodal logistics. Smart pallets with RFID tags and tracking technologies offer real-time visibility in supply chains, meeting the needs of the pharmaceutical and high-value electronics sectors.

Category-wise Analysis

Material Type Insights

Wood Pallets lead with 55% market share, favored for cost-effectiveness and availability in heavy-duty applications. Their strength suits manufacturing and logistics, aligning with wood pallets market dynamics where softwood dominates 65% globally. Timber sourcing infrastructure across states like Uttar Pradesh, Maharashtra, and Tamil Nadu supports local manufacturing ecosystems. Wooden pallets offer versatility across industries from agriculture to construction, with load capacities ranging from 500 kg to over 2,000 kg. The material's strong export market presence reflects compliance with ISPM-15 standards, essential for international shipments of agricultural and manufactured goods.

However, environmental concerns regarding deforestation and forest conservation are gradually incentivizing shifts toward certified sustainable timber sources, which add 7-9% to production costs but appeal to environmentally conscious enterprises and regulated sectors. The recycling and circular economy potential of wood makes it attractive for organizations implementing sustainability commitments, with wooden blocks retaining value through multiple use cycles before eventual repurposing as biomass or wood-based composite materials.

Structural Design Insights

Block pallets hold approximately 58% of the market share in India due to their superior load distribution, four-way forklift entry, and improved stability during stacking operations. Their design uses nine cylindrical blocks instead of traditional stringers, which facilitates better weight distribution across warehouse floors and allows for higher stacking heights. This is crucial for maximizing vertical storage capacity in space-constrained Indian warehouses.

Manufacturers such as Schoeller Arca and PalletOne, Inc., produce block pallets with reinforced configurations tailored for heavy industrial applications. Block pallets exhibit superior durability, with service lifespans extending 30-40% longer than equivalent stringer designs under similar load conditions. They are particularly favored by the automotive and pharmaceutical industries due to their compatibility with automated storage and retrieval systems (AS/RS) and their consistent dimensional tolerances, which are essential for efficient automated handling.

Industry Insights

The Food & Beverage sector represents the largest end-user segment, accounting for approximately 32% market share, propelled by stringent hygiene, safety, and supply chain compliance requirements that make pallets a non-negotiable logistics infrastructure. The sector's sensitivity to product contamination drives preference for plastic and stainless steel pallets that facilitate rigorous cleaning and sanitization protocols required by HACCP and FDA standards. Cold chain expansion for perishable goods distribution has exponentially increased pallet demand in this segment, with temperature-controlled logistics requiring pallets capable of withstanding environmental stresses.

The pharmaceutical industry constitutes the fastest-growing segment, driven by PLI scheme incentives and expanding cold chain infrastructure requiring temperature-controlled pallet systems. Companies like B.D. Industries and LEAP India supply specialized pallets for pharmaceutical logistics. The retail sector benefits from organized retail expansion and FMCG distribution networks, while electronics manufacturing growth under Make in India drives demand for anti-static and precision-engineered pallets.

Regional Insights

West India Pallets Market Trends

West India is expected to hold about 35% of the India pallets market in 2025, driven by Maharashtra's diverse industries and Gujarat's port-focused infrastructure. Major manufacturing hubs in Mumbai and Pune, including companies like Spanco Enterprises and DNA Packaging Systems, support sectors like automotive, pharmaceuticals, and FMCG. The region’s proximity to JNPT and Mundra Port enhances export-oriented pallet demand. SIG's Ahmedabad plant, producing 4 billion packaging units annually, highlights the area's packaging capabilities.

The Western Dedicated Freight Corridor improves logistics efficiency, and developing Multi-Modal Logistics Parks bolsters distribution infrastructure. The local regulatory environment encourages innovation, with IoT-enabled smart pallets and BIS-certified recycled materials. Gujarat’s special economic zones also stimulate industrial pallet demand from chemicals and textiles, while integrated logistics solutions promote sustainable packaging growth.

North India Pallets Market Trends

North India is emerging as the fastest-growing region in the country, driven by the logistics corridor in the Delhi NCR area and the expansion of manufacturing in Uttar Pradesh and Haryana. North India accounted for more than 20% of India's e-commerce logistics market, benefiting from established multimodal corridors and the implementation of the National Single Window System. The Delhi NCR region serves as a central gateway for northern consumption markets. Additionally, the newly sanctioned Multi-Modal Logistics Parks are enhancing throughput capacity. The connections provided by the Eastern Dedicated Freight Corridor are also improving accessibility to key manufacturing hubs.

Uttar Pradesh, in particular, holds a dominant position in India's cold storage infrastructure. This dominance is driving a growing demand for specialized pallets within the agricultural logistics sector. Companies like Saraswati Engineering Limited and Mekins Group operate manufacturing units serving northern markets. The region benefits from lower manufacturing costs and skilled labor availability, attracting pallet production investments.

Competitive Landscape

India pallets market exhibits a fragmented structure with numerous regional players alongside established multinational corporations. Market concentration remains low with the top five players collectively holding approximately 28-32% market share. Companies are pursuing vertical integration strategies, with manufacturers like Nilkamal expanding into pallet pooling services and reverse logistics networks. Key differentiators include ISO 9001 quality certifications, automation-compatible designs, and customized solutions for specific industries. Emerging business models emphasize rental and asset-sharing platforms that reduce capital expenditure for SMEs while ensuring standardization. Strategic partnerships between pallet manufacturers and 3PL (third-party logistics) providers are strengthening distribution networks and after-sales service capabilities across tier-2 and tier-3 cities.

Key Market Developments

- October 2025: Snowman Logistics announced construction of a new temperature-controlled warehouse facility in Pune featuring 5,900 pallet capacity under the Built-to-Suit model, scheduled for operational launch by June 2026, expanding their total network to over 160,000 pallets across pharmaceutical and food & beverage cold chain infrastructure.

- December 2024: LEAP India, India's largest pallet pooling company, announced expansion of its asset management operations with additional manufacturing partnerships across Gujarat and Maharashtra, aiming to strengthen its asset pool of 4 million units and enhance service coverage across logistics networks serving 1,250+ customer touch points.

- August 2025: The inauguration of New Sanjali Cargo Terminal near Ahmedabad on the Western Dedicated Freight Corridor marked a significant infrastructure development, enhancing multimodal logistics efficiency, directly stimulating demand for specialized pallets in rail-to-road cargo transfer operations and bulk goods movement.

Top Companies in India Pallets Market

- LEAP India Pvt. Ltd. (Bangalore, India) has established market leadership in the pallet pooling segment with approximately 4 million units in its asset pool, serving supply chains across automotive, FMCG, pharmaceutical, and retail sectors. The company operates 7 outsourced pallet manufacturing facilities across India and maintains 16 regional warehouses, providing logistics companies and manufacturers with cost-effective returnable pallet solutions that reduce capital expenditure while ensuring supply chain reliability.

- Mekins Industries Limited (Hyderabad, India) operates 7 manufacturing facilities across Hyderabad, Pune, Chennai, and Ahmedabad, specializing in steel pallets and material handling equipment. The company achieved EPAL certification as a European Pallet Association-approved manufacturer, enabling it to serve international logistics standards and export-oriented manufacturing sectors.

- Saraswati Engineering Limited (Kanpur, Uttar Pradesh, India) operates specialized manufacturing for steel pallets, plastic pallets, and industrial material handling equipment. The company serves automotive, pharmaceutical, and chemical industries with injection-molded plastic pallet solutions and export-grade steel pallets, maintaining ISO 9001:2008 certification for quality management systems.

Companies Covered in India Pallets Market

- Mekins Group

- Saraswati Engineering Limited

- LEAP India Pvt. Ltd.

- DNA Packaging Systems

- Spanco Enterprises

- Doll Plast Pallets

- Schoeller Arca TIME Material Handling Solutions

- B.D. Industries (India) Pvt. Ltd.

- Aristoplast Products Pvt. Ltd.

- Falkenhahn AG

- PalletOne, Inc.

- Palettes Gestation Services

- Nilkamal Ltd.

- Supreme Industries Ltd.

Frequently Asked Questions

India pallets market is likely to be valued at US$ 10.6 billion in 2026, projected to US$ 18.1 billion by 2033 at 7.9% CAGR, driven by e-commerce logistics expansion and manufacturing sector growth under the PLI scheme.

The primary demand drivers include rapid e-commerce expansion, manufacturing sector growth with industrial production expanding, government initiatives like Make in India and Gati Shakti, and cold chain infrastructure expansion for pharmaceutical and food logistics.

Wood Pallets with 55% share, attributed to cost-effectiveness, widespread timber availability, and versatility across industries from agriculture to construction.

West India dominates the regional market with 35% market share, driven by Maharashtra's diversified industrial base spanning automotive, pharmaceuticals, and FMCG sectors, and Gujarat's port-centric infrastructure, including JNPT and Mundra Port.

Significant opportunities exist in sustainable and eco-friendly pallet solutions meeting circular economy and Extended Producer Responsibility (EPR) regulations, with upcycled plastic pallets commanding premium pricing in regulated sectors.

Key players include Schoeller Arca, LEAP India Pvt. Ltd., Mekins Group, Saraswati Engineering Limited, and Nilkamal Ltd. These companies compete through quality certifications, automation-compatible designs, sustainable material innovations, and strategic partnerships with 3PL providers.