- Specialty & Fine Chemicals

- India Kaolin Market

India Kaolin Market Size, Share, and Growth Forecast 2025 - 2032

India Kaolin Market by Product (Hydrous Kaolin, Calcined Kaolin, Delaminated Kaolin), Form (Dry Powder Kaolin, Slurry Kaolin, Granular Kaolin), Processing Method (Unprocessed Kaolin, Water-washed Kaolin, Air-floated Kaolin), and Regional Analysis 2025 - 2032

India Kaolin Market Share and Trends Analysis

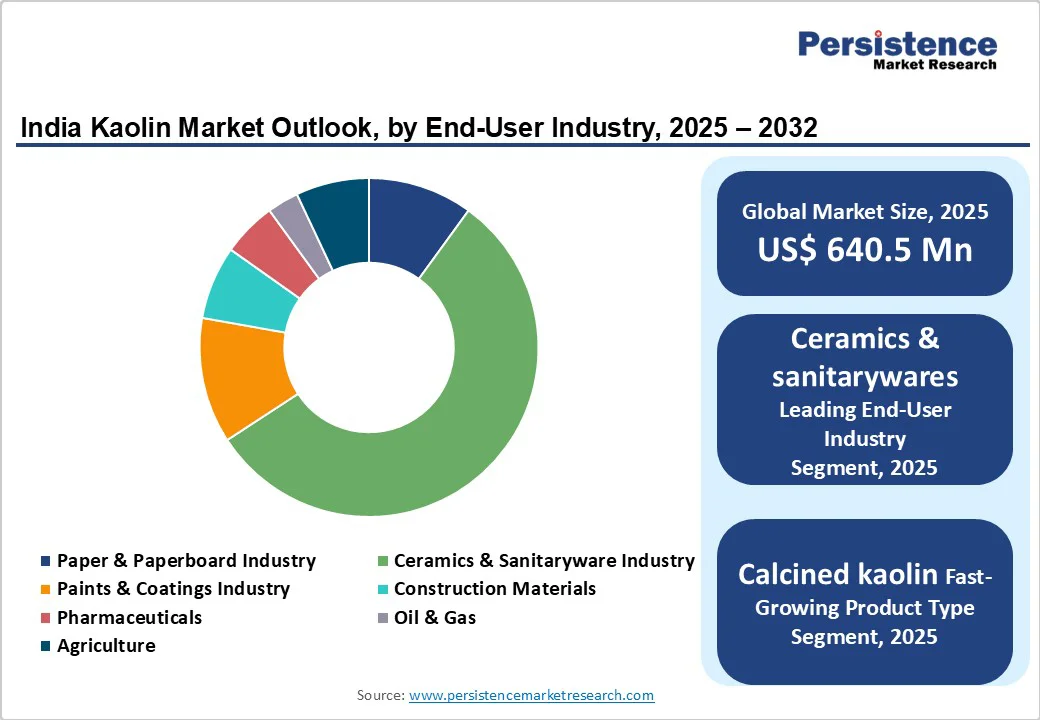

India's kaolin market size is likely to be valued at US$640.5 Million in 2025 and is projected to reach US$919.5 Million by 2032, growing at a CAGR of 5.3% between 2025 and 2032.

Key growth in industrial applications and the rise in infrastructural investments underpin this expansion, while technological improvements in calcination processes and supportive government policies further bolster kaolin demand.

Key Highlights:

- Crude kaolin leads with 37.6% share in 2025; calcined kaolin is fastest-growing.

- Ceramics & sanitarywares dominate at 55.8%; paper & paperboards growing fastest.

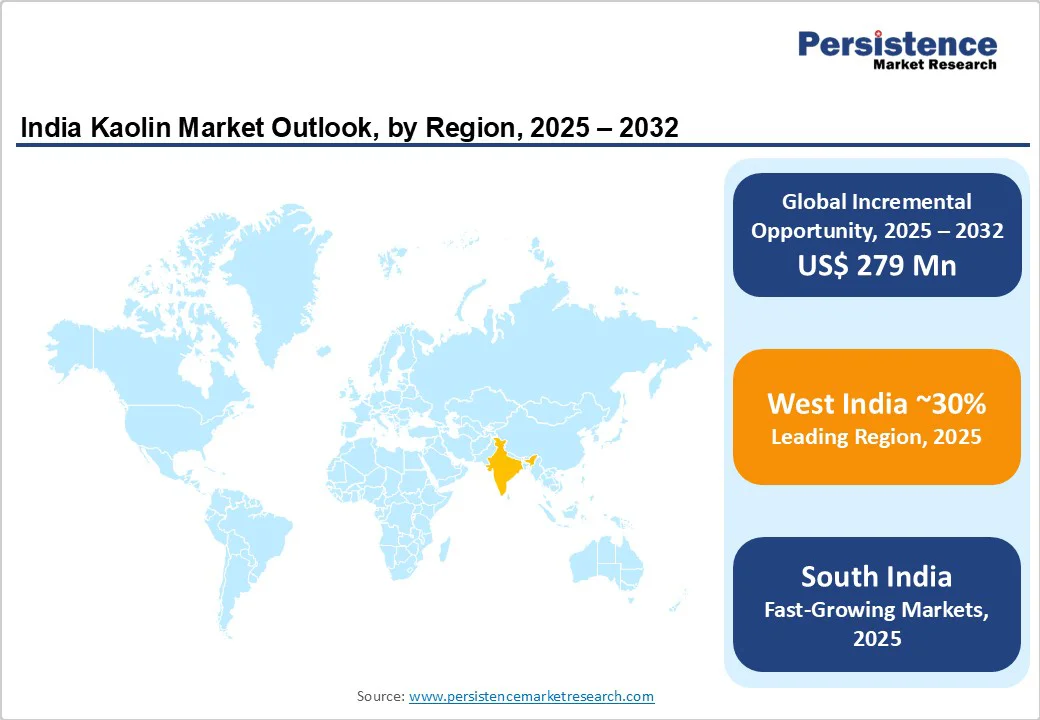

- West India largest region (30% share); South India fastest growth region (20% share).

- Top players control 45% of revenue; competitive focus on integration and innovation.

| Key Insights | Details |

|---|---|

| India Kaolin Market Size (2025E) | US$ 640.5 Million |

| Market Value Forecast (2032F) | US$ 919.5 Million |

| Projected Growth CAGR (2025 - 2032) | 5.3% |

| Historical Market Growth (2019 - 2024) | 2.9% |

Market Dynamics

Driver - Technological Advancement in Calcined Kaolin Production

Advances in rotary kiln and flash calcination technologies have enabled higher whiteness and particle size uniformity for specialty applications. India’s installed calcination capacity rose by 15% between 2022 and 2024, with throughput reaching 120 ktpa, enhancing the competitiveness of domestic producers.

Improved energy efficiency has reduced production costs by 8%, enabling broader adoption in high-performance coatings and plastics compounding. As a result, manufacturers can tailor calcined kaolin grades for optical brightness and rheology control, unlocking new applications in premium paints and advanced ceramics.

Surge in Paper & Paperboard Manufacturing

India’s paper industry, comprising 861 mills and 526 operational units, recorded packaging paperboard capacity of 4,990 kt in 2024, up by 7.2% over 2023. Kaolin’s role as a coating pigment to enhance printability and surface smoothness has driven growth in consumption.

With paper & paperboard identified as the fastest-growing end-use segment, kaolin demand increased by 6.1% in volume terms in 2025. The government’s 100% FDI policy in paper & pulp attracted US$1.74 billion from April 2000 to December 2024, facilitating capacity expansions that underpin sustained kaolin uptake.

Market Restraints

Logistical Constraints and Transportation Costs

Kaolin’s bulk density necessitates cost-intensive rail and road logistics. Average freight accounts for 18-22% of delivered cost, rising to 30% for remote mining sites in West and North India. Periodic rail congestion and inadequate last-mile connectivity have led to shipment delays of up to 10 days, affecting just-in-time supply chains in ceramics clusters.

These challenges pressure margins and may deter smaller processors from expanding capacity despite robust end-use demand.

Environmental Regulations and Resource Scarcity

Stricter mining regulations under the Mines and Minerals (Development and Regulation) Act have imposed environmental clearances and progressive mine-closure obligations, adding compliance costs of US$ 0.5-1.2 per tonne. Limited high-grade reserves in key basins such as Rajasthan and Andhra Pradesh have necessitated longer haulage distances.

As a consequence, some mid-sized producers face operational hurdles, constraining near-term capacity growth despite favorable downstream demand.

Market Opportunities

Expansion into Functional Coatings and Sealants

Delaminated and levigated kaolin grades offer high aspect ratio and improved rheology for advanced paints and adhesives. With India’s construction coatings market projected to exceed US$ 5 billion by 2027, formulators seek low-density fillers to meet performance and sustainability targets.

Strategic partnerships between miners and specialty chemicals firms could unlock co-development of tailored kaolin blends for anticorrosive and self-cleaning surfaces, enhancing value-addition potential.

Functional coatings applications span two key areas. First, architectural paints, where improved opacity and scrub resistance command premium pricing. Second, industrial sealants, leveraging kaolin’s reinforcing properties to deliver durability in harsh environments. This dual focus promises diversified revenue streams beyond traditional paper and ceramics markets.

Domestic Processing and Value-addition

India’s packaging sector, the third-largest globally as of September 2024, recorded domestic consumption growth of 8.2% in paperboard. Current crude kaolin exports represent 22% of output, with most value-addition occurring overseas. Establishing local calcination and delamination facilities could capture downstream margins estimated at US$ 80-120 per tonne.

Government incentives for specialized logistics parks and packaging labs under the National Packaging Initiative further support investments in integrated processing hubs. A two-pronged approach enhances opportunity capture: inward FDI for technology transfer and PPP models for midstream processing infrastructure. Coupled with skill development programs, India can evolve from a raw exporter to a supplier of high-performance kaolin derivatives.

Segmentation Analysis

Product Type Analysis

Crude kaolin is the leading product type, holding 37.6% share in 2025. Its abundance and minimal processing requirements make it the bulk feedstock for paper coatings and ceramic slip formulations. Major producers exploit near-mine beneficiation to supply local paper mills, leveraging existing transportation networks to minimize logistic costs. Demand for hydrous and air-float grades remains steady for refractory and filler applications.

Calcined kaolin is the fastest-growing segment, driven by enhanced whiteness and particle control essential for advanced coatings and plastics. Volume consumption of calcined kaolin grew by 9.4% in 2025, supported by new kiln installations and upgrades in West India. Government-backed loans for energy-efficient equipment under the Make in India initiative have accelerated capacity additions, enabling domestic producers to compete with imported grades in premium end-uses.

End-use Analysis

Ceramics & sanitarywares dominate the end-use landscape with 55.8% share in 2025. Kaolin’s thermal stability and refractory properties underpin its essential role in porcelain tile and sanitaryware body formulations. India’s ceramics production capacity reached 480 million m² in 2024, with investment pipelines for new greenfield plants in Gujarat and Andhra Pradesh. Downstream consolidation among tile manufacturers has further cemented bulk kaolin sourcing agreements.

Paper & paperboards is the fastest-growing end-use segment. Coated paper demand rose by 8.3% in volume terms in 2025, driven by the packaging and printing sectors. Kaolin’s chalk-free surface finish and opacity improvements are critical for high-speed digital and flexographic printing. New paper mills in South India and East India are integrating kaolin coating units to enhance product differentiation.

Regional Market Insights

West India commands the highest estimated share at 30% due to established mining clusters in Rajasthan and Gujarat. Proximity to major ports in Kandla and Mundra facilitates the export of surplus crude kaolin to Southeast Asia. Key growth drivers include government infrastructure projects valued at US$ 150 billion in urban transport and affordable housing. Environmental clearances for new mines under the National Mineral Policy have unlocked allocations of 12 million tonnes yearly.

South India holds 20%, with the fastest growth rate fueled by new ceramics hubs in Andhra Pradesh and Karnataka. Delaminated kaolin plants set up near Visakhapatnam port in 2023 support exports of specialty grades. State-sponsored industrial parks with dedicated rail links and warehousing have reduced lead times by 25%, enhancing competitiveness for both crude and processed kaolin.

North India represents 18%, anchored by smaller deposits in Uttar Pradesh and Madhya Pradesh. Infrastructure investments under the National Highway Development Program have improved rail connectivity, lowering freight costs by 10%. Plans for a dedicated kaolin beneficiation cluster in Chhattisgarh by 2026 aim to aggregate supply and streamline processing for the expanding paper sector in Eastern India.

Competitive Landscape

India kaolin market exhibits moderate concentration, with the top five players accounting for approximately 45% of total revenue. Large integrated miners holding beneficiation, calcination, and export capabilities dominate, while numerous regional players supply niche applications. Competitive positioning hinges on vertical integration and access to energy-efficient calcination technologies.

Key Market Developments

- April 2023: MineralOne Ltd. commissioned a 50 ktpa flash calcination unit in Gujarat to supply automotive coatings segment, enhancing whiteness indices by 2 points.

- July 2024: ClayTech Industries acquired a 75% stake in HydroKaol for US$ 45 million, gaining access to patented delamination processes and expanding into high-performance sealants.

- January 2025: KaolChem Pvt. Ltd. opened a levigated kaolin plant near Visakhapatnam port with an annual capacity of 30 kt, targeting exports to East Asia and specialty paper markets.

Companies Covered in India Kaolin Market

- MineralOne Ltd.

- ClayTech Industries

- KaolChem Pvt. Ltd.

- WhiteClay Corp.

- HydroKaol

- Gujarat Kaolin Works

- Orient Kaolin

- Rajasthan Kaolin

- Asia Kaolin Ltd.

- Elite Minerals

- Spectrum Kaolin

- National Kaolin

- BrightMinerals

- Energize Kaolin

- MetroClay

Frequently Asked Questions

India Kaolin Market was valued at US 640.5 Million in 2025.

Growth in industrial end-use applications especially growing infrastructural investments and technological advancements in calcination processes are the primary drivers of market demand.

Crude kaolin leads the market with a 37.6% share in 2025.

West India commands the highest share at 30%, supported by established mining clusters in Rajasthan and Gujarat.

Expansion into functional coatings and sealants leveraging delaminated and levigated kaolin grades for advanced paints, adhesives, and self-cleaning surfaces represents a major opportunity.

MineralOne Ltd., ClayTech Industries, and KaolChem Pvt. Ltd. are recognized as leading companies based on production capacity, technological leadership, and integrated processing capabilities.